Dad of 3, Husband, 2300 ELO, MBA MS, BJJ Blue Belt, Staccato Fan, Yoga, Christian, and America First. No DMs please.

Joined October 2022

- Tweets 4,290

- Following 4,144

- Followers 2,464

- Likes 21,966

298 Photos and videos

Pinned Tweet

5 Dec 2025

Understanding that the only barrier between what you want and reality is the friction you create.

3

3

42

5,570

Jun 10

Native South Carolinian here. Whoever voted for Lindsay Graham failed the mission. Not sure how a warmonger, and swamp creature, keeps making the cut.

2

3

153

Jun 2

X is a big wealth transfer engine. All noise and little signal.

Once you see it you can't unsee it.

2

9

543

May 29

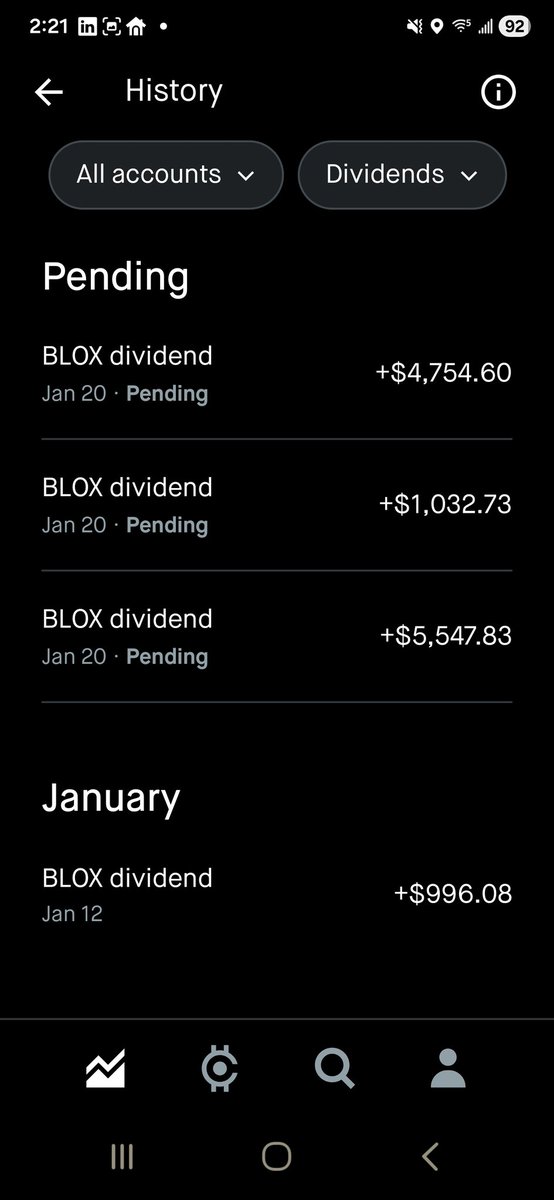

$BLOX holdings file 5/27 vs 5/29:

NAV: $17.23 → $17.74 ( 2.95%) AUM: $323.5M → $333.0M ( $9.5M) Shares Outstanding: 18.775M → 18.775M (0 creations) Cash FGXXX: 1.08% → 1.60% Equity sleeve: 98.87% → 98.54% Sleeve count: 21 → 21 (no adds/drops)

Miner concentration: 39.4% → 40.9% Spot BTC/ETH ETF: 19.3% → 18.2%

$9.5M AUM on zero creations — pure mark-to-market, not inflows. Book keeps tilting into miners (HUT 10.4%, RIOT 9.1%, IREN 7.7%, CIFR 7.4%) while spot bleeds down.

NAV grinding higher in a soft BTC tape.

@XFunds_

8

1

96

7,597

May 11

Bitcoin gets more expensive every day. Even when the price doesn't move.

The power law trend, which BTC has tracked for 16 years, adds about $125 to fair value daily. That's $46,000 a year, regardless of spot.

Months of sideways action? BTC is still appreciating. The floor climbs underneath.

Apply this to bear calls. "$50K by October" sounds reasonable. But fair value in October will be near $160K. A $50K print would be 31% of fair value, the deepest discount in BTC history. Worse than 2015, 2018, or 2022.

Dismiss these calls unless they can explain why this cycle prints the worst dislocation ever.

A flat chart looks like nothing is happening. Fair value is still doing $125 a day of work.

3

3

24

871

May 5

$BLOX holdings file 5/4 vs 5/5:

Cash FGXXX: 31.04% → 0.81%

Equity sleeve: 69.01% → 99.62%

NAV: $15.79 → $16.28 ( 3.16%)

AUM: $274.3M → $288.6M ( $14.4M)

Shares Outstanding: 17.375M → 17.725M ( 350K creations)

FBTC, RIOT, IREN, ETHA all back in size. MSTR new add. Synthetic ETHA unwound to physical equity. Equity sleeve count 18 → 21.

The cash buildup wasn't drift. It was pre-positioning. Manager deployed the entire reserve in one session into the Clarity catalyst. Clean execution, good work!

@XFunds_

9

5

128

5,537

Apr 30

Been studying $BLOX mechanics deeply and wanted to share some observations.

The fund harvests roughly 50% annually from its options positions but only distributes 36%. That 14% buffer is what's keeping NAV roughly flat while BTC is down 40% from ATH. The options overlay is absorbing the drawdown in real time. Most holders don't realize this is happening under the hood.

What's interesting is that same buffer works differently depending on the regime. In a bear it's the shock absorber protecting NAV. In a bull it becomes genuine NAV accretion on top of the underlying appreciation. Same mechanism, completely different outcome depending on where we are in the cycle.

The fund is also adapting in real time. BHDG provides tail hedge protection. NGHT reduces daytime BTC volatility exposure. Credit spreads profit when the underlying declines, partially offsetting losses on the bull put book. These aren't random positions. They're building blocks of a more resilient fund.

Given that the fund's primary investment objective is capital appreciation with income as a secondary consideration, I fully expect yield compression over time. That's a feature not a bug. A sustainable 25% yield with contained drawdowns is worth far more than an unsustainable 40% yield that bleeds NAV every bear cycle.

If you're DRIPing through this bear you're buying shares at $15 that the cycle math has significantly higher. The boring weeks are the most productive ones.

41

21

248

14,805

Apr 27

$BLOX architecture observations

Been studying the holdings evolution. A few structural reads worth surfacing:

The 9.2% combined allocation to NGHT and BHDG (~$25M) looks like systemic hedge infrastructure rather than basket diversification.NGHT smooths intraday vol on the BTC sleeve. BHDG carries tail risk.

If the satellites handle those jobs, the credit spread overlay on the miner basket doesn't need to wear two hats. It could free the options book to harvest more efficiently per dollar of notional with narrower spreads, closer-to-the-money strikes, more premium per dollar of defined risk.

The barbell seems to be getting more deliberate as AUM scales.

High-beta crypto-equity on one end. Defensive infrastructure on the other. Passive BTC/ETH exposure as the anchor in the middle. The satellite additions are growing the defensive end without giving up offense.

Capacity-extending infrastructure rather than basket bloat.

Curious about the design intent @XFunds_ @DavidANicholas. Thank you, as always - still buying daily.

8

2

52

5,556

Apr 7

Trump, you are about to cross the Rubicon.

A foreign adversary bombing the global economic system we built and depend on, energy, rail, trade, financial infrastructure, all of it, would be called a war crime. You are doing it yourself.

I voted for you three times, with pride.

Your instincts are right. Your execution is compounding risk on top of risk in a system that is already cracking, with no off-ramp in sight.

You've lost me.

@realDonaldTrump

1

9

516

Mar 6

The Iran war has exposed something uncomfortable: our military has learned nothing from Ukraine.

The economics of modern warfare are now fundamentally against us. We are firing $4 million interceptors at $500 drones. We cannot sustain that math against Iran, let alone China. Magazine depth is already a crisis and nobody in Washington is saying it plainly.

Carriers are no longer a show of force. In a hypersonic missile world they are a $13 billion target with 5,000 American lives on board. China has spent 20 years building systems specifically to kill them. Sailing one near Taiwan isn't deterrence. It's an invitation.

The battlefield is drones, long range precision artillery, anti-air defense, and autonomous systems at massive scale. Not hundreds. Hundreds of thousands. Ukraine proved this two years ago on live television. We watched and did nothing.

The countries that figure out mass production of cheap autonomous systems win the next war. China already has the manufacturing infrastructure. We have defense contractors protecting $50 billion programs that belong in a museum.

I love American airpower as much as anyone. But loving something that no longer fits the threat environment is not patriotism. It's denial.

This will cost American lives. The only question is whether we change before or after we find out the hard way.

3

3

13

916

Feb 6

I've read a lot of theories on what happened to BTC and there are a TON - Iran, Fed Sec., Intrest Rates, Greenland, AI implosion of Software Firms, etc.

My working theory is that these all played a factor, but the two things that ignited the fuse were:

-Japan Yields Rising on cheap debt, which forced selling (bond prices plummet for the borrower).

-Insane amounts of leverage in BTC which caused a domino effect

No one knows, but there are lot of other things I likely missed, but these two seem to have set it all off with the Saturday fire sale.

1

15

2,028

Feb 6

I know I can't be the only one that thinks retail was totally destroyed in order to build bags of banks, billionaires, and others in the aristocratic class.

Not much of a conspiracy theorist but this "don't look right" as they say.

For the record, I couldn't hold BTC below 60k but by god's will I am somehow still in this crazy game.

Good luck to everyone and especially those that are struggling still today. I am feeling for you.

8

1

35

2,720

Chad retweeted

Feb 6

Two interesting theories on the parabolic sell off yesterday:

@TheOtherParker_ theorizes that HK-based hedge funds, likely non-crypto natives, blew up on massively leveraged $IBIT options trades.

Key evidence: record $10.7B IBIT volume (2x prior high), $900M options premiums, and BTC/SOL lockstep drop with low CeFi liquidations.

These funds held 100% in $IBIT for margin isolation, per 13F filings. Tied to JPY carry unwind raising funding costs, silver’s 20% crash (2nd largest ever), and a summer short-vol squeeze compressing BTC vol to record lows - until Oct 10’s spike blew holes in balances, spiraling into desperation trades and full liquidation.

In-kind ETF creations since July ’25 enabled OG Bitcoiners to shift stacks tax-free for covered calls, amplifying vol suppression and eventual unwind.

@TheShortBear attributes it to a leverage-driven unwind from the yen carry trade, hitting correlated risk assets like $BTC and software stocks ($IGV). No single blow-up, but systemic positioning stress: funding tightens, vol spikes, forcing sales across yield-seeking channels (crypto, software, private credit).

Unwind started ~quarter ago, aligning with risk momentum loss; plays out in waves over quarters with grace periods. Binance’s heavy Asian-hour selling suggests regional funds/traders dumping during US liquidity. Long crypto positions now liquidated at 20:1 skew, resetting extremes.

Always remember: financialization of BTC via ETFs/options introduces systemic macro and derivatives risks -like carry trades, vol squeezes, and cross-asset contagion - wholly unrelated to BTC’s fundamentals.

This dovetails with my theory that much “OG selling” was likely rotation into $IBIT for access to margin leverage and its ultra-liquid options market, fueling the powder keg.

18

30

288

23,912

Feb 4

I figured it out. The market doesn't like the threat of prolonged Wars, Tarriffs, Fed Uncertanty, High Intrest Rates, Gov't Shutdowns, delayed Cyrpto Legislation, and USA over taking Greenland.

Took me a minute, but I got there.

38

30

442

20,759

Feb 4

Hard lesson that I learned. If you're buying BTC and you don't know where it is relative to this model you're guessing.

The LPPL (Log-Period Power Law)

DYOR, Understand FIBs, etc. but I HIGHLY recommend you follow this model closely.

1

10

971

Feb 4

Post 1/2

5 Key Metrics to Confirm a BTC Bottom (updated Feb 3, 2026)

Fear & Greed Index <20 (Extreme Fear) → capitulation

MVRV Ratio <1 → undervalued vs. realized price

Puell Multiple <0.5 → miners capitulating

LTH Net Inflows → smart money accumulating

Weekly RSI <30 → extreme oversold

Current confluence: ~88–92% there. Not advice, DYOR. #BTC #Bitcoin

2

10

838

Feb 4

Post 2/2

Table of current levels:

Fear & Greed: 17 (100% there)

MVRV: ~1.05–1.08 (90–95% there)

Puell: ~0.58–0.60 (70–80% there)

LTH Net: Selling slowing (75–80% there)

Weekly RSI: ~26–27 (100% there)

This is the strongest bottom cluster we've seen in this drawdown. Compression near maxed.

6

436

Feb 4

$BLOX is now holding 59% of the entire portfolio FGXXX (near cash).

Yields likely to drop, but I really appreciate this defensive slant in times like this. Tons of dry powder to ride it back up when bottom is confirmed.

Nice work.

20

11

216

10,345

Feb 1

17 years of math.

Feb 1

Why Math Says This Is the Largest Pricing Error in Bitcoin History (≈105% Implied 12-Month CAGR)

Bitcoin is trading at a −35.5% deviation below its 15-year power-law trend. That is not an opinion; it is a statistical displacement the market is currently ignoring.

Power-law fair value today: $122,425

Spot price: ~$79K

That places Bitcoin firmly in the historical “oversold” regime (Z-score: −0.63).

At this depth, price doesn’t just "drift" back to trend.

It snaps.

I back tested every comparable oversold event since 2010.

Results over the following 12 months:

Win rate: 100%

Average return: 100%

Sentiment was irrelevant every time. The Ornstein-Uhlenbeck (OU) mean reversion process was not.

This deviation has a measurable Half-Life: 133 days.

In simple terms: The market historically corrects 50% of its pricing error every 4.4 months, 100% in ~9 months.

The $43,457 gap is a compressed spring. As it relaxes, the "snap-back" velocity dictates the path:

June 2026: $113K

October 2026: $145K

January 2027: $162K

Model fit: R^2 = 0.96 (Solid)

18-month predictive correlation: 0.55

(55% of the price movement 18 months from now is statistically explained solely by the Z-score (deviation).

We are at the extreme left tail of the distribution. This is where expected value concentrates. Math supports an aggressive ~0.6x Half-Kelly allocation.

The market is offering a significant discount.

Closing the Gap

Today

Bitcoin is ~$43.5k below its power-law trend value, a −35.5% deviation. This is the extreme left tail. Historically, this is where forward returns concentrate because the error is too large to persist.

Oct 2026

The gap compresses to ~$11k (−6.8%).

That implies roughly 75% of the anomaly has already reverted. At this point, the trade is no longer “deep value” it’s transitioning into normalization.

Implied fair value ≈ $155k

Implied Bitcoin price ≈ $145k

Jan 2027

The gap shrinks to ~$7k (−4%).

Implied fair value ≈ $168k

Implied Bitcoin price ≈ $162k

CAGR ~105% (Next 12 Months)

Why This Analysis Is Robust:

The Power Law captures Bitcoin's diminishing returns and logarithmic adoption curve (R² = 0.96).

It’s Mean-Reverting: The OU Process proves that price is tethered to value. The further it stretches (Z-score), the stronger the force pulling it back.

It’s Statistically Significant: The 18-month predictive correlation is 0.55. This means 55% of Bitcoin's future price action is explained solely by today's deviation. That is an incredibly high signal-to-noise ratio for any asset class.

1

6

835