Not financial advice. We may hold long or short positions in any securities mentioned, and may buy or sell such securities without prior disclosure.

Joined February 2019

- Tweets 17,555

- Following 2,489

- Followers 13,712

- Likes 101,420

1,371 Photos and videos

BDC retweeted

Jun 11

That happened yesterday in Malibu. Photo by Billy Watts.

25

58

1,033

44,493

Jun 10

Token pricing wobbling, data points such as the below, $ORCL balance sheet and capital intensity slop without associated material upside to rev estimates, 1/3 $SPY market cap concentrated in like 20 tech names... should be good for small cap health care stocks that are cheap and maybe not so good for $QQQ

Jun 10

1

1

5

1,851

BDC retweeted

Jun 9

$AIRS talking much more about new site growth today in public appearance.

Why do they keep saying “we are just getting started”? Because there is a path to $300M in EBITDA (putting the business around 1x).

Here is the math:

- ~$150M of revenue today at 31 sites

- new site openings “soon to follow” debt refi that is imminent

- “at least another 100 locations” that can be opened

- with 131 sites and current utilization levels, revenue is over $500M

- at utilization levels from just a few years ago (before GLP-1 tailwind), revenue is over $1B at 131 sites

- prior peak margins were over 30%

That is $300M in EBITDA in the not-so-distant future, before any GLP-1 and new procedure contribution, with company valued at $350M.

“Early innings” indeed.

2

15

1,527

BDC retweeted

$LQDA - The court holds that Amarin, a drug maker, has failed to state a claim for active infringement of its patent.

🫳🎤

3

2

49

4,325

Jun 3

Exciting turnaround underway at $AIRS. Think this new management team has really got things cooking.

We are long the stock but may sell at any time. We may not share future positioning. This is not advice, we could be wrong, and please do your own research to arrive at your own conclusions.

Jun 3

Best $AIRS mgmt has ever sounded in public webcast just now: “Investment community is just starting to see the progress we are making, and we are in the early innings.”

Expressed high confidence in their guide, which includes no GLP-1 linked volume despite already being 10-15% of total.

Noted path to doubling margins and resuming highly profitable new store growth into “huge population we can’t serve”

Signed off by noting the aesthetics industry “is just getting started”

1

6

1,685

Jun 2

Garbage in, garbage out. Major issues here w/ $mrna data, in our view.

Disclaimer: we have been negative on the $mrna tech and clinical viability for years. We have been short the stock but also trade around volatility. Do your own research and don't take investment or trading recommendations from X.

$MRNA shareholders really need to be asking questions here. From yesterday's ASCO paper.

"Treatment-related adverse events occurred in 104/104 patients (100%) in the intismeran plus pembrolizumab arm and 42/50 (84%) in the pembrolizumab arm"

Every single patient on combo had a treatment-related AE.

"Direct functional linkage between post-treatment T-cell clonotypes and specific intismeran-encoded neoantigens remains to be established."

5-yr OS: HR 0.471, CI 0.165-1.345. So INT reducing death risk by 84% is as equally true as INT increasing death risk by 34%.

Among the myriad of imbalances in the trial, the ctDNA imbalance is particularly telling.

Combo: 13 ctDNA (12.1%). Pembro: 2 ctDNA (4.0%).

With only TWO ctDNA-positive patients in the entire control arm, the ctDNA-positive subgroup HR is mathematically "not estimable."

So the highest risk subgroup, the patients who biologically need adjuvant therapy most, cannot be analyzed against a control. After 5 years and three publications, we still don't know if INT works in patients with detectable residual disease.

The pembro arm has 30% "not evaluable" ctDNA vs 16.8% in combo. 13 percentage points of unknown ctDNA status in the control arm.

In an expensive Phase 2 trial run by two of the largest pharma companies in the world, you would expect cleaner biomarker characterization.

Is this simply a coincidence? You be the judge of that.

2

2,627

BDC retweeted

Jun 1

Quick thoughts on the $GOOG raise:

1) Management is old enough to remember when this stock traded at much lower multiples for YEARS, good time to raise capital and it's not that much relative to the market cap.

2) The demands of data center build out/token cost are even more insatiable than we thought (see $HPE, $DELL, or the $NVDA overnight news)

3) Profitability/cash flow could be headed lower in a meaningful way at some point in the not too distant future for the search business. This is the most important take away IMO. Someone explain to me how you take the greatest business model ever created in Search/Adwords where you have 90% share and replace it with LLM's/AEO, while somehow maintaining the same profitability. The structural economics are WORSE and market share is materially worse. Search traffic is DOWN in many categories and that will only get worse from here as consumers engage with #openAI, #claude, #gemini at higher rates.

Honestly, I don't know why this isn't the primary narrative around $GOOG currently. I'm sure there are people that will have different perspectives on this, but ask around to people that rely on search. Volumes are down in many areas already.

19

14

199

47,703

Jun 1

Pretty bullish $XGN

"Uniquely identified ~25% of the SLE patients who would otherwise be missed by conventional markers"

investors.exagen.com/news-re…

4

1,768

Jun 1

The entire platform is a fraud

The data published by $MRNA at ASCO makes complete sense. See mgmt's statements from Barclays in March:

"Even seeing a 0.8 hazard ratio, I think, would be a clinically meaningful result."

Translation: management is already conditioning the market for a Phase 3 HR of 0.75-0.80.

Need I even explain what a 0.8 HR in MELANOMA — the friendliest tumor for immunotherapy — implies for NSCLC, RCC, and bladder?

cc: @BlueDuckCap

1

1,622

May 28

Best part about the $MOB call last night was the implicit message that revenues will hockey stick in the 2H and sustain higher for years. Orders accelerating. Awards compounding. Unique in their FTC and Blue UAS validations. Exceptionally well positioned here.

3

1

15

1,707

May 28

“The government is going to buy all of the properties that GEO Group and CoreCivic own,” one source said in a phone call. Three others confirmed that purchasing properties is a plan under serious consideration and is already seeing early movement.

$GEO

washingtonexaminer.com/polic…

1

1

17

1,506

May 28

$AIRS hitting the road hard. They have a term loan maturing which we believe they are going to refi soon.

They wouldn't be doing this marketing tour if not.

And my context here is that when I first met the CEO, Yogi Jashnani, the business was on shakier ground and while I urged him to get out in front of investors he indicated that they weren't ready for that. Now they are. And they are doing it aggressively. As a new CEO, you seek out investors to pitch your story when things are humming, not when you are battening down the hatches.

Event path:

-term loan refi

-continued SSS growth through the year

-continued acceleration skin tightening procedure growth

-Start expanding the store count next year (has been paused as they get house in order)

Not advice, as always. We are long AIRS, but may sell at any time without any disclosure.

May 28

$AIRS announcing 2 more high-profile conferences appearances (5 in 2 months, after no IR effort in prior year).

It is almost as if they think their stock is still too cheap. Meanwhile, fundamentals keep getting better.

What new could come out of these?

1. Category and company-specific data (search interest, web traffic, social media engagement) continues to strengthen each month

2. The consumer backdrop has improved (rates, oil, spending reports)

3. Interest in new procedures CK tjnues to grow

investors.elitebodysculpture…

10

1,755

BDC retweeted

May 27

You could own $XGN with all of the tailwinds below, or you could own a competitive, capital intensive knife fight in MCD at a much higher valuation… choose your fighter.

May 27

$XGN valuation makes no sense. A mgmt team with history of value creation, cornering one of the fastest growing diagnostics end markets with test solutions that make sense for the patient (faster diagnosis/treatment), MD (faster timeline to more lucrative treatment solutions and happier, healthier patients) and the payers who save on repeated multi-year doctor visits that otherwise struggle to diagnose illness such as Lupus). And new indications coming in 2027 which will accelerate growth and expand the TAM.

1

9

3,790

May 27

Love this

May 26

It’s my 19th birthday today, and my birthday wish is Bill Ackman sees this!

@BillAckman

Dear Bill Ackman,

My dream is to become the best investor I can possibly be

My name is Caleb. I’m going to be a freshman at the University of Oregon studying accounting and finance while running D1 XC and track

Since I was 15 years old, I had one dream, to go D1

To get there, I learned true work ethic

I skipped hangouts

I sacrificed weekends

I trained every single day no matter how I felt

Running taught me something most people never learn

Consistency and hard work beats everyone else

Now I want to bring that same obsession, discipline, and competitiveness into investing and business

In my investing journey, I’ve really looked up to you. You’ve become an unofficial mentor to me, similar to how Warren Buffett was for you early on.

I’m asking for an opportunity.

I’m willing to work harder than anyone else in the world

I’ll work for free

I’ll scrub floors

I just want the chance to learn, contribute, and prove myself

I just need a shot, you won’t regret it

Thank you!

1

1

7

6,273

May 22

We are sometimes early - even for months. But when we tweet about stuff, it tends to be the higher conviction bets.

That said, always underwrite your own thesis and do your homework and I do not recommend trading off of anything you see on X.

$zm

Mar 6

$ZM owns between 0.5% and 1% of Anthropic. Their core biz continues to grow and throw off cash to tune of $1.9B ttm fcf. 1/3 of their market cap is in cash. If Anthropic is going to eat the world - and it might - or just if Anthropic continues to grow like a weed - which it will - $ZM is worth a lot more.

8

3,190

May 22

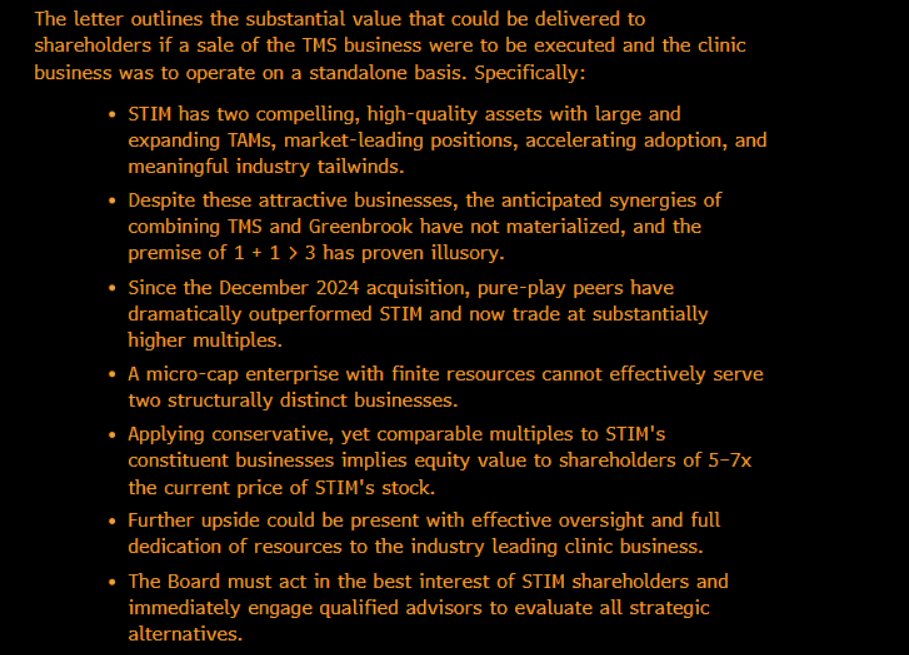

Dont know when, obviously. But one of these days we are going to wake up and $STIM is 100%.

Just my opinion, not advice, we are long the stock but may sell at any time without any disclosure.

May 22

👀

5

1

10

5,136

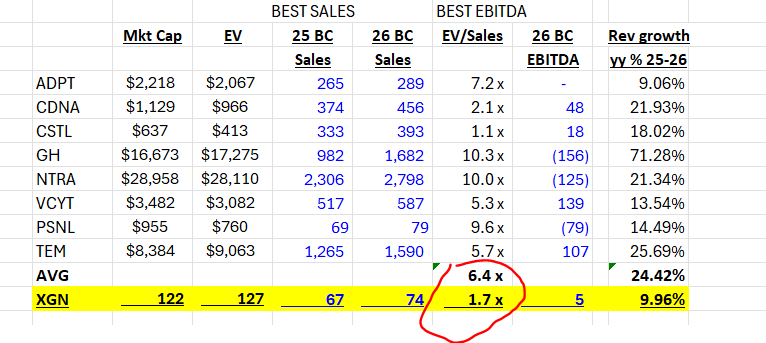

May 21

$XGN fell out of bed late last year when Citrini blasted it. We added a lot recently and own ~2% of the shares. Had a great call with mgmt - great team. Conservative in their guidance, I believe.

ASPs have stabilized after a 1x issue in Q3 last year and volumes are solid. New indications coming next year.

Selling that stock in the hole at 1.25x revenues for a business that is cornering the autoimmune diagnostics vertical (famously difficult to address) is a mistake imho. Note that diagnostic comps trade in the 2-11x range on 2026 revenues - none of which have cornered a large and growing (sadly) market like autoimmune.

Not advice - just my opinion.

3

6

4,475