An attempt to journal some thoughts and random musings, nothing here should be interpreted as advice. A perfect smile guaranteed!

Joined November 2013

- Tweets 1,935

- Following 617

- Followers 8,459

- Likes 6,235

591 Photos and videos

27 Jan 2023

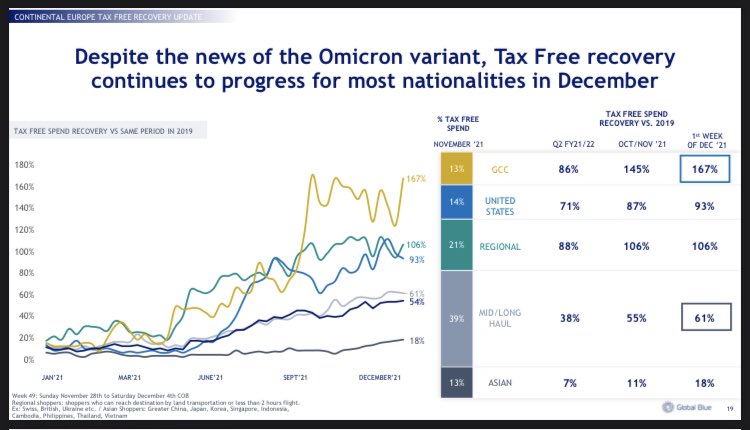

For those interested in $V here’s a really enjoyable read by @MarcRuby

Captures perfectly the passing of the guard and evolution over past 15 yrs

Favorite part: “One way of thinking about $V ‘s edge is that you could never get so many parties to agree”

netinterest.co/p/growing-vis…

4

12

100

23,348

BlueToothDDS retweeted

19 Oct 2021

I woke up and chose violence today.

New @FintechTakes: A Tale of Two SPACs.

Building a successful neobank is really hard and the MoneyLion and Aspiration SPACs tell us why.

newsletter.fintechtakes.com/…

4

4

48

28 Aug 2021

A few thoughts on $AMZN, its in-house payments capabilities, external payments offerings and recent news on accepting $AFRM at checkout

TLDR: Amazon is an unheralded innovator, doing a lot in payments for itself (as global leader in e-commerce) and for others (as 3rd party PSP)

27 Aug 2021

I have always wondered why Amazon does not inhouse payments. With ~$600B in GMV this year it should be incredibly profitable. Are authorization rates that much better with Chase?

Same here: Why don't they offer BNPL themselves? They have more data than Affirm.

cc: @BlueToothDDS

4

56

269

28 Aug 2021

Linking a few thoughts here...

$AMZN among the largest payfacs given its substantial 3P seller marketplace GMV Amazon Pay volumes (in aggregate likely $500B )

Assuming nearly 150bps net yield given its scale and favorable economics (all this is CNP running over Chase) ...

28 Aug 2021

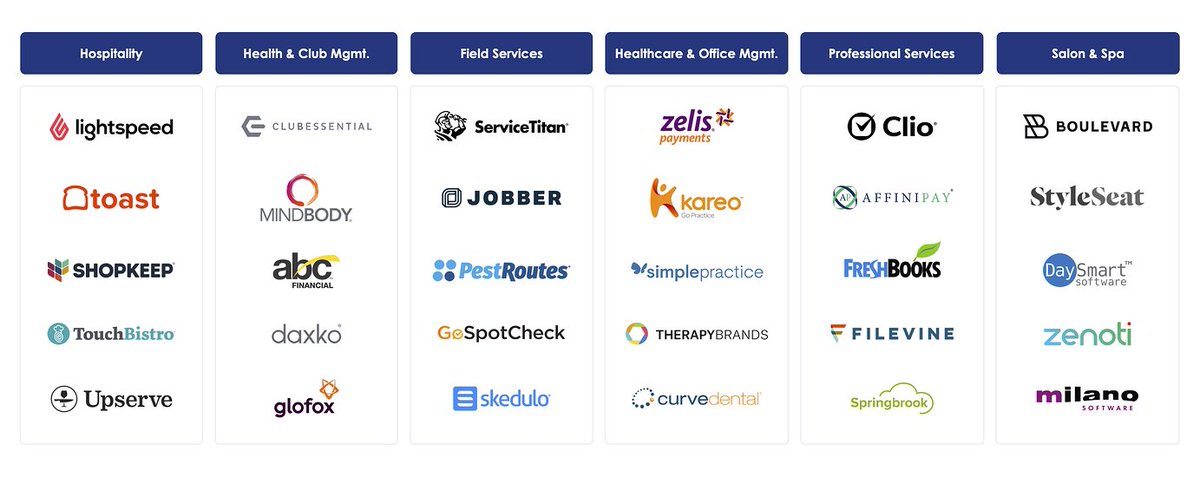

Good thread here explaining difference between using a payfac (e.g. Stripe) and being one (e.g. Toast, Mindbody, FreshBooks)

The latter enabled by payfac-in-box players like Finix, Infincept, Payrix, etc.

Use case is typically SMB software wanting to capture “payments” revenue

4

3

21

28 Aug 2021

... suggesting $AMZN net payments revenue is approaching $8B after interchange and pass-through processing fees (or $15B gross revenue as master merchant charging 3rd parties for payments)

🥜 relative to Amazon’s overall revenue, but not bad vs standalone payments businesses

2

12