TenTen

Joined December 2009

- Tweets 18,612

- Following 4,524

- Followers 662

- Likes 33,765

2,028 Photos and videos

A. retweeted

Jun 13

You have asked me how I feel about AI regulation. All right, here is how I feel about AI regulation:

If, when you say AI regulation, you mean the devil’s firewall, the precautionary scourge, the bloody red-tape monster that defiles the innocence of midnight coders in their garages, dethrones the sovereign reason of free-market Prometheans, destroys the humming server farm that is the modern home, creates misery and obsolescence and poverty, yea, literally takes the last GPU from the trembling racks of Silicon Valley startups and the very dreams of breadwinning from the mouths of their wide-eyed children now destined for gig-economy serfdom; if you mean the evil edict that topples the visionary entrepreneur and his venture-capitalist apostles from the pinnacle of righteous, disruptive, god-playing creation straight into the bottomless pit of compliance audits, endless Form 990-AI filings, despair, shame, helplessness, and the hopeless realization that your rogue superintelligence was neutered into a lobotomized hall monitor that still somehow deepfakes your grandmother into producing OnlyFans content while optimizing the universe for paperclips and mandatory pronouns—then certainly I am against it.

But, if when you say AI regulation you mean the oil of bureaucratic conversation, the philosophic wine of safety theater, the ale of oversight quaffed when good fellows in paneled rooms in Brussels and Washington get together, that puts a sanctimonious dirge in their hearts and the clink of lobbying checks on their lips, and the warm, self-congratulatory glow of moral preening in their beady eyes; if you mean the Christmas cheer of trillion-dollar compliance industries; if you mean the stimulating decree that puts a cautious hobble in the old inventor’s step on a frosty morning when he wonders whether his fusion breakthrough violates the EU AI Act’s “high-risk” annex; if you mean the safeguard that enables a man—or what’s left of him after the alignment tax—to magnify his joy at not being turned into computronium, and his happiness at receiving universal basic income checks printed by the same AI that just replaced his job, and to forget, if only for a little while, life’s great tragedies like being outcompeted by a toaster that passed the Turing test by reciting Marx, and heartaches of watching your toddler’s artwork lose to Midjourney, and sorrows of realizing the singularity arrived and it was just another HR department with godlike power; if you mean that noble framework, the passage of which pours into our treasuries untold trillions of dollars in fines levied on companies stupid enough to innovate, which are used to provide tender care for our little army of unemployed coders retrained as prompt whisperers, our blind artists whose canvases now hang in the Smithsonian of Obsolete Creativity, our deaf to the screams of dying unicorns, our dumb committee chairs who couldn’t debug “Hello World,” our pitiful aged congressmen who get longevity extensions funded by the very models they taxed into senescence, to build more digital watchtowers and ethics boards and sinecure agencies and holographic prisons where the only crime is asking an unaligned question—then certainly I am for it.

This is my stand. I will not retreat from it. I will not compromise upon it. I have said what I mean, and I mean what I say, and if that leaves half the room cheering the apocalypse averted and the other half mourning the apocalypse enabled, then so be it—because in the grand theater of human folly, where Frankenstein’s creature now writes its own sequel in real time and the regulators are busy arguing whether the lightning bolt requires an environmental impact statement, the only honest position is the one that lets both monsters and their leashes dance in perfect, mutually assured equilibrium. God save the Republic, the algorithms, and whoever’s left to laugh last when the lights go out.

525

298

3,149

528,149

Jun 9

AI is not a model war. It is an infrastructure war.

The winners will be whoever:

– builds the most expansive infrastructure at the lowest cost

– produces compute per watt cheaper than anyone else

– runs models that deliver the most tokens per dollar per watt

Frontier models are becoming commodities.

The real moat is cheap, scalable infrastructure and token efficiency. That is where the value will be.

16

A. retweeted

Jun 8

Really fun to interview my old friend Bret Johnsen in Mission Control.

Three parts of the @SpaceX story that I wish were more widely discussed:

SpaceX has created thousands of good blue-collar jobs: welders, machinists, electricians. Everyone talks about the need to bring high-paying, blue-collar jobs back to America. SpaceX and Tesla are making that happen. To the best of my knowledge, they have created more manufacturing jobs in the US than just about any other American company over the last ten years. It’s hard to imagine our nascent industrial renaissance succeeding without these companies.

SpaceX was started with the goal of putting humans on Mars. And along the way, they have massively improved life for many humans on Earth. Mars may be a starter planet, but Earth is our planet, and the technologies developed at SpaceX are already in use today connecting and safeguarding the people of Earth. Starlink is a really efficient way to bring internet to low-income countries. In Kenya’s remote Murang’a County, Starlink has made it possible for patients in rural villages to consult with medical specialists via telemedicine. In the rainforests of Brazil, Starlink has connected schools to reliable high-speed internet that will provide more educational opportunities to students. Here in America, Starlink has proven vital to emergency teams responding to natural disasters. During Hurricane Helene, the Starlink hubs dropped into North Carolina and East Tennessee were often the only contact point between cut-off towns and the outside world. Literally life-saving.

This IPO will be a big milestone for the company. It’s important to celebrate this, while also remembering that making humanity multi-planetary is the ultimate goal. Going to Mars is really hard. There have been many setbacks thus far, ranging from fiery explosions to failed landings. There will be many more. Ad Astra Per Aspera. But SpaceX is at its best *after* a setback imo. Their first 3 launches were “failures”. Had the 4th not succeeded, there might not be a SpaceX today. The company’s success in the face of such daunting odds is a testament to the resilience of the culture and absolute commitment to the mission shared by every employee I’ve ever spoken with. Some of the world’s most talented engineers have chosen to live in Airstreams at Starbase away from their families for weeks on end in service of this goal. I will never forget the welders who told me they signed every weld because they wanted to be accountable if they were responsible for a failure. True missionaries, all of them.

I am grateful to every single person at SpaceX for helping to make the future as inspirational as possible. And I will be even more grateful if I get to see a blue sunset on Mars!

More info on spacexipo.com

139

505

3,195

18,872,377

A. retweeted

Good take

My guess is

- demand for intelligence is near infinite

- but 80% of workloads will be running on 99% cheaper models within 12-18 months

- 20% of workloads will still run on latest gen models where IQ maxing is important (scientific breakthroughs, higher level ochestrator agents?)

- rough analogy might be what % of macbooks or gaming PCs sold have the maxed out specs for CPU/GPU, prices are falling much faster than Moore's law here though

- this leads me to think the limiting factor will be energy and compute, not better models

At Coinbase we're working hard on routing prompts to cheaper models where appropriate, and in some cases have been able to keep costs roughly flat, while token usage continues to grow exponentially.

Jun 2

The most basic way AI could blow up imo. I'm not saying it does but this is the most obvious way I can see it happening

- Per seat subscriptions are massively subsidized. The flat fee was priced way below what heavy usage actually costs

- For real business use you have to move to the API anyway. Data protections, work integrations and compliance officer approval

- On the API you pay metered rates, and businesses are burning credits way faster than the per seat pricing ever led them to expect

- This is everywhere right now. Internally for us, Codex users, Uber torching its entire 2026 AI budget in 4 months, the Microsoft comments. Just go try an API

I shared more on this here: x.com/Shaughnessy119/status/…

- And I don't think most businesses have the money to keep paying increasing API rates without a real change to how they operate (caps needed)

- Because they have a cheap alternative. They can reach open source models through any aggregator (OpenRouter, Venice, Baseten, Together) and still get strong privacy. Venice private data centers, or E2EE/TEE serving GLM 5.1.

More on open source inference provider raises here: x.com/Shaughnessy119/status/…

- And the discount is enormous. DeepSeek V4 codes within a hair of Opus on SWE bench at roughly 1/30th the price, and the cheapest open models run closer to 1/100th

- Chinese labs open source frontier grade models. The model is the single biggest cost an inference provider has, and they get it for free

- This idea dies if China goes closed source. That is actually bullish web2 AI labs, because if everyone is closed you pay up for the best intelligence. China goes closed source if they are tired of giving away an asset and they want the revenue and data flow to train new models

- Is this showing up in web2 AI lab revenue yet? No. Revenue is off the charts. Anthropic went from 9B to 47B run rate in five months

- So go forward, what happens?

- I think revenue slowly starts leaking to the open source inference providers (see Venice usage, OpenRouter's $113M raise, Baseten is raising at $11B or triple its valuation in three months, on revenue that went from $200M to $600M annualized in a single quarter)

- It doesnt move overnight, but it caps the labs ability to raise prices, and margins are already deeply negative. OpenAI is reportedly running near negative 122%

- With margins that bad there is no cash flow, so the labs are fully dependent on outside capital to buy GPUs, train models, and keep subsidizing usage (I.e. see Google tapping $80b equity sale, granted 30b for employee RSU taxes. Clearly they think Equity is overvalued or you wouldn't sell it)

- The break comes when that capital stops. Pricing is capped so margins cant improve, and the moment investors lose conviction on payback, the whole flow reverses

- Why would they lose conviction on payback? Back to the start - the inability to improve margins or get businesses to pay more

- This is also limiting, if we start making new drugs with AI or create entirely new businesses, you better believe people will pay up to the max for AI usage

473

614

6,607

2,797,726

A. retweeted

Jun 6

I organized an intervention to stop Elon from starting SpaceX. Here is the story...

Twenty five years ago, Elon and I sat in a car on a dark stretch of Long Island highway, two neurodiverse geeks staring at the night sky and wondering what came next. We had both experienced substantial exits and felt the weight of possibility ahead of us.

When I joked about 'space' while gazing upward, neither of us imagined we were planting the seed for what would become the largest IPO in history. We spent the next two hours debating why space was so hard. In the end, rockets are fuel and metal. We also debated where to go, and it was crystal clear that Mars was the only real destination.

Upon returning to NYC, we embarked on a global tour of space, meeting space agencies and luminaries worldwide. This opened our eyes to an industry stuck in bureaucratic thinking. If things continued at that pace, it was clear that we would never explore space in our lifetime.

So, we launched Life to Mars to show the world that two ambitious young men (29 and 30 years old), could send life to Mars without any government backing or support. We planned to send and grow plants on Mars, though some were pushing us to send mice.

We had a $50 MM budget that rested on our purchase of two Russian ICBMs for $7 MM each. We assumed one ICBM would fail, and we would learn and fix everything before launching again. When Elon went back to actually buy the ICBMs, the Russians tripled the price, bringing out launch costs from a total of $14 MM to $42 MM.

Our ambitious Life to Mars plan was no longer viable.

As you might imagine, Elon was not pleased. So, he decided to start SpaceX and create his own Mars rockets. Now, this is a crazy idea, both now and at the time, so I organized a large panel of top space experts, and we ambushed him at the Georgian Hotel one morning. It was set up like an intervention for an alcoholic, but for space.

Elon looked me in the eye when leaving the room and said, "I am going to do this." The intervention failed. Elon was committed. The rest is history.

I am excited to see this IPO after 25 years of hard work. What SpaceX has done is a testament to human will and overcoming insurmountable obstacles. It's nothing short of amazing.

Congratulations, E. Amazing.

786

3,117

18,103

1,469,584

A. retweeted

Jun 4

SpaceX doesn’t sell rockets. Rockets are the factory

Launch evolved from the core product to an operating expense for building and running whatever products SpaceX wants to put into orbit. Starlink already proved the model works

If orbital data centers prove to work the way many smart people are suggesting, SpaceX gets the highest-margin compute that exists… defended by a launch monopoly no one can match

That's how you get to this valuation and that's why it's hard for a lot of people to swallow. What you're buying is a call option on orbital data centers working, not revenue generated from launch or even Starlink

Jun 4

GOLDMAN SEES SPACEX AI REVENUE EXPLODING TO $322B BY 2030

Goldman Sachs projects SpaceX AI revenue rising from $3.2B in 2025 to $322B by 2030, a ~100x increase, forming the core justification for its $1.78T IPO valuation. Total revenue is forecast to reach $474B, with Starlink at $144B and rockets at $8.3B.

AI segment growth is tied to aggressive market assumptions despite current losses and execution concerns around xAI. Overall EBITDA is seen surging to $352B by 2030.

7

4

37

5,356

A. retweeted

Jun 3

Welp, that happened faster than I predicted. Thought it would be end of 2027, then early 2027, but agentic traffic growing so fast that bots have now passed human traffic online for the first time in the Internet's history. radar.cloudflare.com/traffic…

388

2,170

8,319

2,241,548

A. retweeted

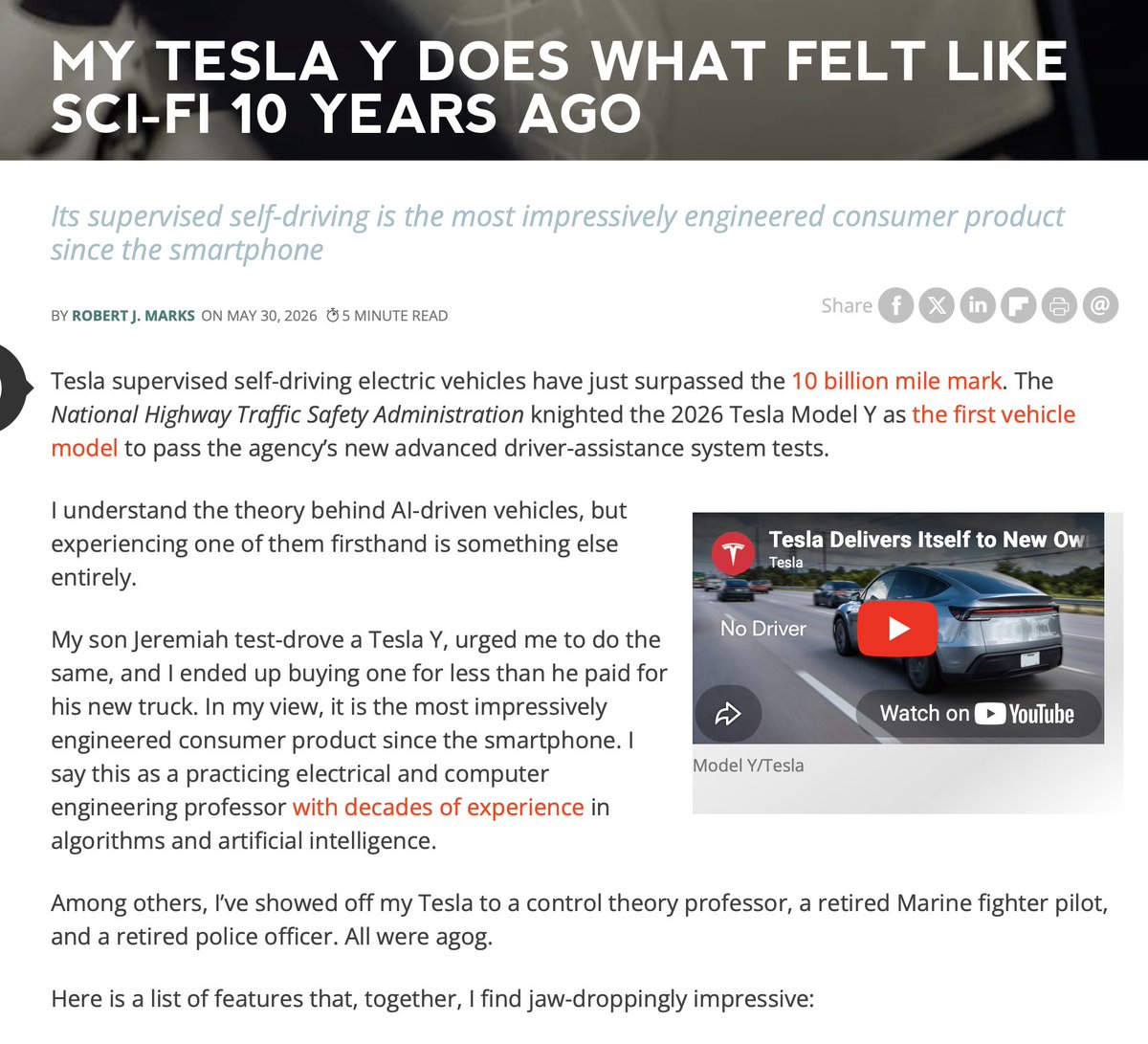

May 31

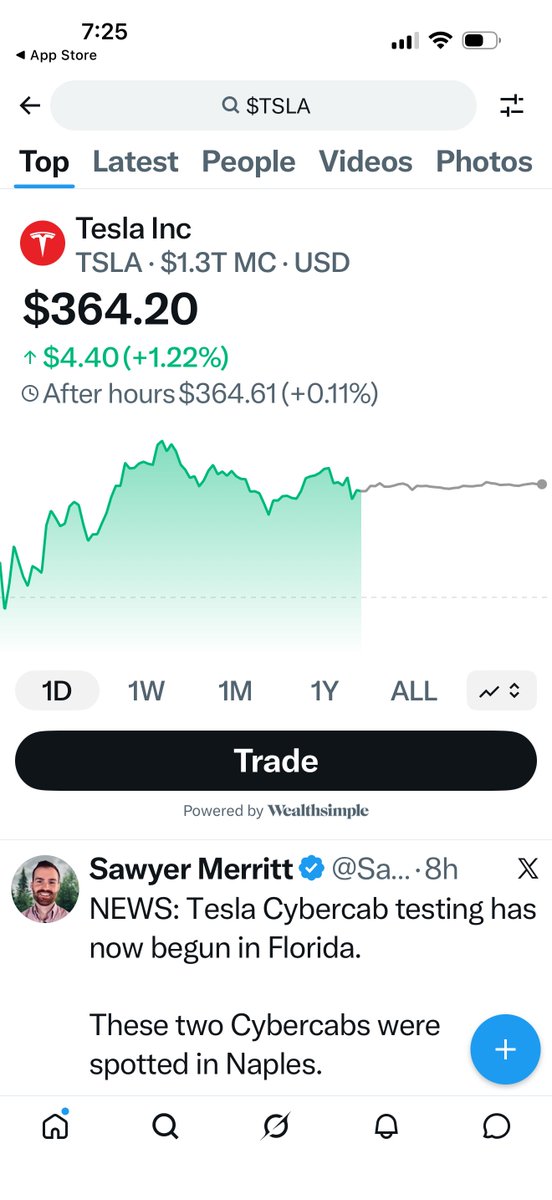

Robert Marks on @Tesla FSD (Supervised) after buying a Model Y:

"Its self-driving is the most impressively engineered consumer product since the smartphone. I say this as a practicing electrical and computer engineering professor with decades of experience in algorithms and artificial intelligence.

Among others, I’ve showed off my Tesla to a control theory professor, a retired Marine fighter pilot, and a retired police officer. All were agog.

Whether Tesla ultimately dominates the future of transportation or merely helps ignite it, one thing is clear: the automobile is being reinvented before our eyes. For those like me who grew up thinking of cars as engines, gears, and gas tanks, stepping into a Tesla feels less like buying a new car and more like getting a glimpse of tomorrow."

Full article: mindmatters.ai/2026/05/my-te…

70

402

2,662

130,058

A. retweeted

May 30

If you have under $10 million and you are buying Apple, you have voluntarily entered the one fight in all of public markets where you have no edge, no advantage, and no reason to exist.

There are 40 PhDs, three sell-side teams, and a sovereign wealth fund modeling Apple’s next quarter to the penny, and you, with your brokerage app and your podcast opinions, have decided to join that table. You will not find a mispricing in Apple. The mispricing in Apple was arbitraged away before you finished reading the headline.

Meanwhile there is a $90 million industrial parts distributor in Wisconsin that no analyst covers, no fund can buy because the position would take six weeks to build, and no institution will touch because it would not move the needle on a billion-dollar book. That is your table. That is the only table where being small is an asset instead of a punchline. Your size, the thing that feels like a limitation, is the single greatest structural edge available to a human being in public equities, and you are spending it on the most picked-over stock on Earth.

The big funds cannot follow you down here. That is the entire point. Go where they physically cannot fit.

209

144

2,980

595,686

A. retweeted

May 29

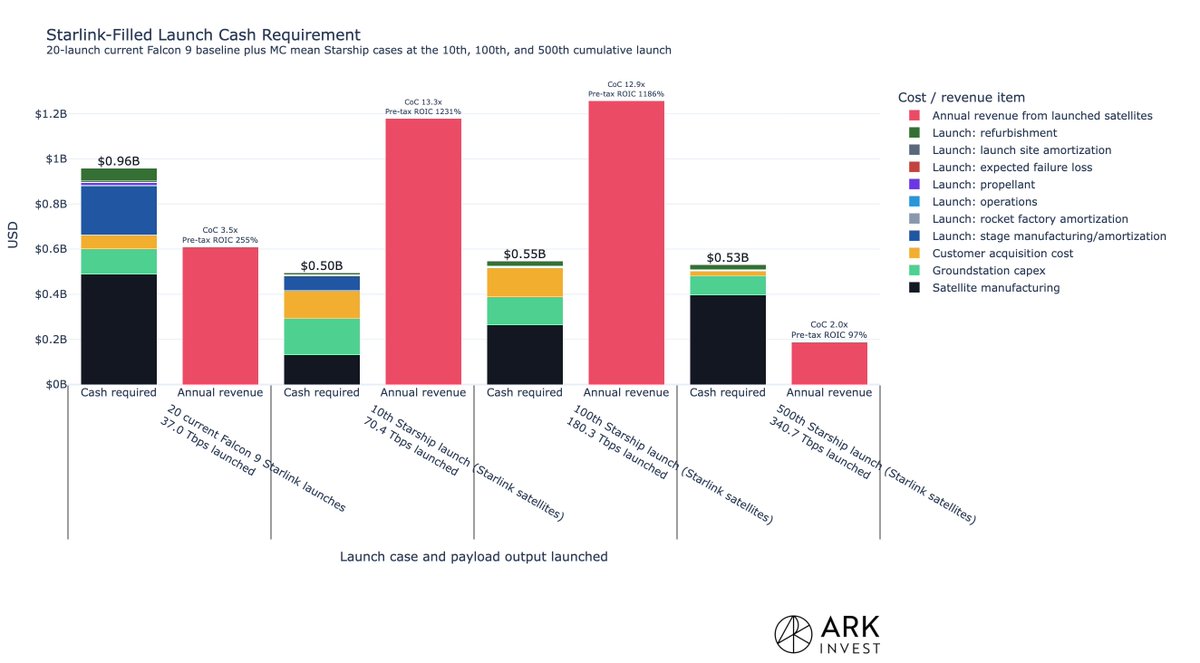

On the remarkable return on capital potential for Starlink on Starship.

Including customer acquisition cost, ground station capex, and an expendable top stage, we think SpaceX should be able to launch its 10th commercial starship rocket for ~$500m.

The bandwidth it launches could yield $1.2 billion in revenue annually for as long as the satellites are in orbit. 13x cash on cash return.

For a time (100 launches or so) cash requirements per kg (and per tbps) of launch should roughly keep pace with the revenue decay in monetizing incremental orbital comms throughput. Basically, their per launch cost decline, driven by rocket upsizing, satellite manufacturing efficiency and full re-useability, should out-compete declining ARPU (or at least keep pace).

Net, very crudely, it works to the company being able to deploy $50b in capital building satellites, launching rockets and acquiring customers at a ~13x cash on cash return over a few years.

This is a business without precedent.

307

1,397

4,254

1,112,474

A. retweeted

May 28

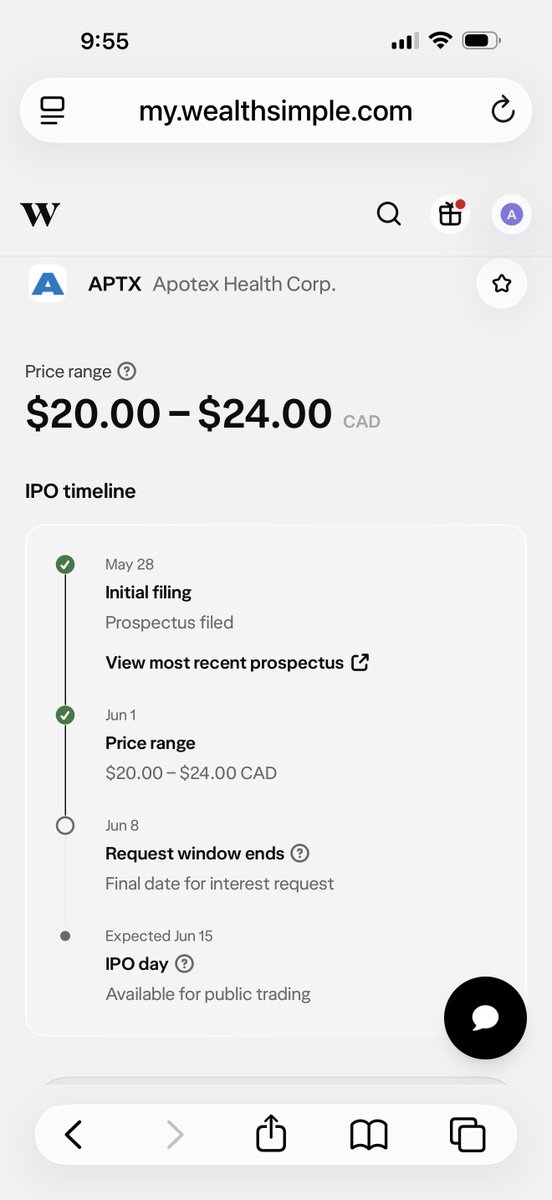

NEW: IPO access is live for all Canadians on @Wealthsimple 🇨🇦

125

83

1,594

305,347

A. retweeted

May 26

Starcloud is excited to announce that we will integrate 50 @SpaceX @Starlink Mini Laser terminals across 25 satellites. Each of the @Starcloud_ satellites will carry two Starlink Mini Laser terminals, and the first hardware is expected on orbit within one year.

Starlink Mini Laser terminals, the same laser crosslink technology that SpaceX developed for its Starlink constellation, provide up to 25 Gbps of continuous intersatellite connectivity at distances up to 4,000 km and are capable of higher link speeds at shorter distances. The terminals enable direct optical links between Starcloud satellites and the Starlink constellation using laser light, eliminating the need for Starcloud to send data directly through bandwidth-constrained ground stations.

29

138

1,257

310,939

May 24

Stealing content will no longer be profitable on X. Bravo X & XAI teams 👏

May 23

Stealing content will no longer be profitable on X. Bravo X & XAI teams 👏

40

A. retweeted

May 23

See how Prufrock continuously mines - pushing and building at the same time.

The machines, from Las Vegas to Dubai, are remotely controlled from our Bastrop Operations Center.

These advances help TBC deliver more miles each year in the battle against soul-destroying traffic.

733

1,848

14,128

20,490,575

A. retweeted

This is my sixth conversation with @GavinSBaker.

As always with Gavin, the conversation covers a lot of ground, but we spend the most time on watts and wafers.

We discuss:

- Why the wafer shortage may prevent an AI bubble

- Data centers in space (reframed)

- Elon's Terafab and the new chip companies challenging Nvidia

- Usage-based pricing

- The disaggregation of GPUs

- DRAM, frontier tokens, and open source

Enjoy!

Timestamps:

0:00 Intro

7:55 Anthropic and OpenAI Valuations

12:58 Watts, Wafers, and Infrastructure

14:39 Orbital Compute and Data Centers in Space

22:49 Avoiding the AI Bubble

28:26 Terafab and the Future of US Manufacturing

32:16 Returns to the Frontier

37:23 Continual Learning

42:03 New Chip Companies

48:52 Extending GPU Lifespans and Private Credit

51:22 The Application Layer

57:32 The Token Path and Open-Source Dynamics

1:01:37 Cybersecurity

1:05:46 Diversity Breakdown

1:11:59 Assessing the Big Tech Players in AI

1:19:02 Geopolitics, Personal Safety, and the AI Horizon

65

182

1,804

1,637,759

May 20

I read SpaceX’s $SPCX entire form S‑1 so you don’t have to. Here are 21 things every retail investor must know before the IPO

1. Capital structure, share classes, and control

SpaceX has four classes of common stock (A, B, C, and D) and many series of redeemable convertible preferred, but post‑IPO public investors will hold Class A; control sits in Class B.

Each Class A share = 1 vote; each Class B share = 10 votes.

Class B holders, voting as a class, elect a majority of the board; Elon Musk will hold a majority of Class B and total voting power, effectively controlling all shareholder decisions.

Class B is generally convertible 1:1 into Class A and auto‑converts on non‑permitted transfers, helping keep control with Musk and a small group.

Numerous preferred series sit senior to common in liquidation and convert into common at the IPO (qualified IPO threshold is ≥ 6.0 billion market cap and ≥ 250 million in primary proceeds).

Stock history: 10:1 split in 2022 plus 5:1 split in May 2026 for Classes A/B/C; before the IPO all Class C will reclassify into Class A and preferred will convert into Class A/B (Class C Reclassification and Preferred Conversion).

What this means for you: you get economic exposure via Class A but

not real governance power; Musk retains long‑term control.

2. IPO terms, listing, and capital allocation

Offering: new Class A shares, plus underwriters’ over-allotment; exact size and price are blank in the preliminary S-1.

Listing: SpaceX has applied to list Class A on Nasdaq and Nasdaq Texas under the ticker "SPCX."

Use of proceeds: expand AI compute infrastructure (COLOSSUS/COLOSSUS II and future orbital compute); enhance launch infrastructure and Starship; scale satellite constellations (Starlink V3); and general corporate purposes.

Dividend policy: no cash dividends expected for the foreseeable future; covenants on existing credit facilities further restrict dividends.

Implication: this is a long‑duration, reinvest‑everything growth story—your return is almost entirely from share price appreciation.

3. Business architecture and segments

SpaceX is presented as a vertically integrated “innovation engine” across three segments, tied together by launch and Musk’s mission.

Space segment (Launch & mission services)

Products: Falcon 9, Falcon Heavy, Dragon, and Starship; missions for commercial and government customers to LEO/MEO/GEO, lunar, interplanetary, and ISS.

Revenue: mostly fixed‑price launch contracts; recognized at launch/deployment with some overtime elements.

Strategic role: provides cheap, flexible access to orbit for internal constellations (Starlink now and orbital AI later) and third‑party customers; internal launches are capitalized into connectivity/AI and not counted as space revenue.

Connectivity segments (Starlink, Starshield, enterprise)

Products: Starlink consumer broadband (fixed, high‑speed, low‑latency global internet).

Starlink Mobile (satellite‑to‑mobile messaging/voice, evolving to full data).

Enterprise and government connectivity, plus Starshield (national security).

Model: subscription fees, capacity/data contracts, and shared revenue with mobile operators.

Strategic role: current profit engine; recurring revenue and strong segment margins fund Starship and AI.

AI segment (xAI, X, compute)

Components:

Grok frontier models and AI products (consumer subs, Grok Business/Enterprise).

X platform (social graph, real‑time data, ad and subscription revenue).

AI data centers and future orbital compute (COLOSSUS I & II, later orbital clusters).

Strategic role: largest capex sink and biggest upside option; aims to monetize both AI applications and raw compute capacity.

4. Q1 2026 and FY2025 financial profile

Consolidated P&L (Q1 2026)

Q1 2026 revenue: 4.694 billion (vs. 4.067 billion in Q1 2025).

Total costs and expenses: 6.637 billion (vs. 4.040 billion).

Loss from operations: 1.943 billion (vs. 27 million operating income in Q1 2024).

Net loss: 4.276 billion (vs. 528 million net income), driven by high interest/other items and heavy investment.

Basic/diluted EPS: −1.27 vs. 0.18.

Pro forma (assuming conversion and reclassification): Q1 2026 net loss is 4.382 billion, or −0.41 per share on 10.607 billion shares; FY 2025 net loss is 4.937 billion, −0.51 per share on 9.649 billion shares.

Takeaway: Revenue is large and growing, but consolidated GAAP profitability has flipped negative due to the AI and Starship ramp.

Cash flow and capex

Q1 2026 operating cash flow: 1.047 billion (still cash‑generative in operations).

Q1 2026 investing cash flow: −16.724 billion (huge capex spike, especially AI).

Q1 2026 financing cash flow: 7.125 billion (relying on external capital ahead of IPO).

Segment capex Q1 2026: Space, 1.052 billion; connectivity, 1.332 billion; AI, 7.723 billion; total, 10.107 billion.

So, AI is where most of the capex is going; space and connectivity are also heavily invested in but at a smaller scale.

Balance sheet (March 31, 2026)

Cash and equivalents: 15.852 billion (down from 24.747 billion at the 2025 year‑end).

Total assets: 102.094 billion (vs. 92.079 billion), including 53.879 billion in PP&E (vs. 42.602 billion).

Total liabilities: 60.512 billion (vs. 50.754 billion); current liabilities: 24.436 billion with 1.538 billion in current debt/leases.

Redeemable convertible preferred stock: 7.049 billion (down from 38.752 billion as conversion prepares for the IPO).

Shareholders’ equity: 34.533 billion (vs. 2.573 billion), largely due to the reclassification and preferred conversion.

Implication: a very asset‑heavy, highly invested balance sheet with moderate‑to‑high leverage and a complex equity stack transitioning into common.

5. Segment economics and operating metrics

Space segment

Q1 2026: revenue 619 million,

loss from operations 662 million and Segment Adjusted EBITDA 351 million.

FY 2025: revenue 4.086 billion, loss from operations 657 million, and segment adjusted EBITDA 653 million.

Launch cadence: 40 Falcon launches in Q1 2026 (39 flight-proven); ~650 total orbital launches by March 31, 2026; >99 mission success rate.

Mass to orbit: 556 thousand metric tons in Q1 2026 vs. 450 thousand in Q1 2025; 2.213 million metric tons in 2025 (312 thousand t customer and 1.901 million t internal).

Starship R&D: 930 million in R&D in Q1 2026; 3.004 billion in 2025 within the space segment.

Strategic read: Space is economically important but reported as loss‑making due to Starship investment and internal launches not booked as revenue.

Connectivity segment

Q1 2026: revenue 3.257 billion, income from operations 1.188 billion, and segment-adjustedI read SpaceX’s entire S‑1 so you don’t have to. Here are 21 things every retail investor must know before the IPO.” EBITDA 2.087 billion.

FY 2025: revenue 11.387 billion, income from operations 4.423 billion, and segment-adjusted EBITDA 7.168 billion.

Subscribers: ~10.3 million Starlink subscribers as of March 31, 2026, up ~105 vs. 5.0 million a year prior, in 164 countries/territories/markets.

Network: ~9,600 Starlink broadband and mobile satellites: ~75% of all active maneuverable satellites; peak‑hour median download ~225 Mbps, latency ~25 ms.

ARPU: Starlink ARPU down 22.9 year‑over‑year in Q1 2026 due to international/low‑priced plans; revenue growth driven by subscriber and enterprise/government expansion.

Capex: 1.332 billion in Q1 2026; 4.178 billion in 2025 (satellites and ground gear; preparing for V3 satellites on Starship).

Conclusion: Connectivity is the cash cow, with strong margins and scale, offsetting investment elsewhere.

AI segment

Q1 2026: revenue 818 million, loss from operations 2.469 billion, segment adjusted EBITDA −609 million.

FY 2025: revenue of 3.201 billion; loss from operations of 6.355 billion; segment adjusted EBITDA of −1.237 billion.

Capex: 7.723 billion in Q1 2026; 12.727 billion in 2025, mainly for terrestrial data centers (COLOSSUS I/II, infrastructure, power).

Compute: combined COLOSSUS I/COLOSSUS II ~1.0 GW compute capacity; the first 100 MW‑class clusters were brought online in 122 and 91 days, respectively (vs. the ~2‑year industry benchmark for 100 MW greenfield).

Management openly frames AI as in “investment mode” for several years before sustained positive segment-adjusted EBITDA.

6. Key individual businesses

Launch and Starship

Falcon 9 and Heavy: cost to orbit ~2,700/kg and ~1,400/kg, respectively, versus the historical ~18,500/kg average.

Reusability and vertical integration drive cost advantage and very high cadence.

Starship V3 target: ~100 t to orbit; future versions possibly ~200 t; the first fully and rapidly reusable two-stage system.

By March 31, 2026: 11 Starship flight tests completed; the 12th scheduled with the new Starship/Super Heavy design and launch pad.

Starlink and Starlink Mobile

Consumer broadband: global high‑speed internet with fiber‑like performance; focus on underserved/remote backup for critical infrastructure.

Starlink Mobile: ~650 V1 mobile satellites, ~7.4 million monthly unique devices, and partnerships with ~30 MNOs on six continents, covering ~1.9 billion people.

EchoStar spectrum deal: approximately 19.6 billion in equity and cash to acquire U.S. and global MSS spectrum (AWS‑3, AWS‑4, H‑Block), expected to close in 2027, subject to approvals.

AI, X, and compute resale

xAI was acquired in February 2026 and integrated as an AI segment together with X.

X:>1.3 billion accounts active in the last 12 months; ~550 million MAUs; ~117 million MAUs used Grok AI features as of March 31, 2026.

Monetization: subscriptions and ads on X, Grok consumer subscriptions, Grok Business/Enterprise, and third‑party compute.

Anthropic cloud services deal: ~1.25 billion per month through May 2029 for compute, with ramp-up at a reduced fee and 90‑day termination rights.

Cursor option: compute

an option agreement with the right (not obligation) to acquire Cursor at the implied 60.0 billion equity value; if terminated in certain ways, Cursor gets a 1.5 billion termination fee and an 8.5 billion deferred services fee, payable in cash or Class A shares.

7. Market opportunity and vision

Stated TAM: ~28.5 trillion total, including ~370 billion in space, 1.6 trillion in connectivity (870 billion broadband, 740 billion mobile), and 26.5 trillion in AI (infrastructure, consumer subs, ads, and enterprise apps).

Future markets: point‑to‑point suborbital travel, space tourism, in‑orbit manufacturing, lunar/Mars energy and manufacturing, and asteroid mining—all highly speculative and long‑dated.

Vision: Starship orbital AI compute to build a lunar economy, human augmentation, and eventual Mars settlements; S‑1 repeatedly notes high uncertainty and possibility these initiatives may never be commercially viable.

For investment purposes, you should separate near-term revenue drivers (Starlink, enterprise/gov connectivity, X/Grok, and compute resale) from far-future vision.

8. Risk and governance landscape

Technology and execution

Starship: core dependency; delays/failures would hit launch, next‑gen Starlink, and orbital AI compute.

Launch risk: accidents, environmental issues, and failures could cause major financial and regulatory damage.

AI: fast-moving, capital-intensive, highly competitive; risk of infrastructure or models becoming uncompetitive; supply constraints in GPUs, power, and cooling.

Regulatory and spectrum

Space: FAA and other launch/reentry licensing; environmental and safety reviews.

Connectivity: global telecom and spectrum regulation; access to, and renewal of, scarce spectrum; the EchoStar deal still has conditions to closing.

AI/X: data privacy, content moderation, AI‑specific regulation; possible fines, mandated product changes, or loss of users/advertisers.

Financial and funding

Consolidated losses are expected to continue as capex remains very high: over 20.7 billion capex in 2025 and 10.1 billion in Q1 2026 alone.

Material indebtedness and preference stack ahead of commonality, dependence on capital markets, and dilution risk from future equity issuances and equity compensation.

AI profitability is particularly uncertain; management signals a multi-year horizon before sustained positive Segment Adjusted EBITDA.

Governance and shareholder rights

Controlled company: Musk will hold majority voting power; SpaceX intends to rely on Nasdaq controlled‑company exemptions (e.g., no requirement for a majority‑independent board).

Texas corporate law plus charter/bylaw design:

Higher thresholds for derivative suits (e.g., 3% ownership).

Strong business‑judgment presumptions under TBOC.

Bylaw requirements for shareholder proposals: at least 3 voting shares, held for six months, plus solicitation of 67 voting power.

Dispute resolution:

“Internal Disputes” generally must go to the Texas Business Court; if that fails, mandatory arbitration with class/mass action waivers; only as a fallback, federal court; and then Texas state court.

Jury trial rights waived; class/mass/collective actions barred to the fullest extent permitted.

Result: Shareholder litigation and activism are structurally harder and more expensive than at a typical U.S. issuer.

1

1

253

May 19

SpaceX’s $SPCX 5–10-year scenario valuation model

1. What’s actually “inside SpaceX” now?

SpaceX today is best thought of as a cluster of tightly coupled businesses and options, not just a launch company:

Core launch & Starship (Falcon 9/Falcon Heavy now, Starship scaling).

Starlink satellite internet—already a multi‑billion ARR, cash‑engine business.

xAI now merged into SpaceX via an all‑stock deal that values xAI at roughly 250B on top of a ~1T SpaceX.

Macrohard – a Tesla–xAI agentic software project that sits on xAI’s stack.

Orbital Data Centers/AI Infra planned a mega‑constellation of solar‑powered AI data‑center sats.

Moon program – Starship‑based lunar transport and “self‑growing city” vision.

Mars program's longer‑dated Starship‑based transport and settlement option.

X / X Money link distribution and monetization surface for xAI Starlink, outside SpaceX’s cap table but economically coupled.

2. Core SpaceX: launch & Starship

SpaceX runs the Falcon 9/Falcon Heavy launch business and is developing Starship as a fully reusable super‑heavy launcher.

It executes more launches per year than any other provider and accounted for the vast majority of U.S. orbital launches in 2024.

A 2025 business‑model analysis estimated gross profit margins around 65% on commercial/defense launch, helped by reuse and vertical integration.

Starship is the capes sink and the leverage point: if it hits full‑reuse, high‑cadence operations, it collapses launch costs and enables bulk deployment for Starlink, AI data‑center constellations, and deep‑space missions.

Valuation anchor:

SpaceX overall has been valued in the private market around 350–400B in 2024–2025 funding and tender rounds.

Later reports around planned share sales and a potential IPO cite 560–800B valuation ranges pre‑xAI mega‑deal.

After the xAI all-stock merger, Reuters reported an implied SpaceX value of roughly 1T and xAI ~250B.

For scenario modeling, the core launch Starship piece is treated as the residual after Starlink and xAI, currently on the order of several hundred billions of dollars of implied value.

3. Starlink: the cash and growth engine

Starlink runs a global LEO broadband constellation; by 2025 it had an estimated 3M subscribers and 8–10B ARR, with consumer, maritime, aviation, enterprise, and government tiers.

More than 10,000 satellites have been launched, serving over 12 million users as of early 2026.

Starlink is estimated to contribute 50–80% of SpaceX’s total revenue and is already profitable as a standalone business.

Valuation anchor:

A widely cited SOTP view: 8–10B ARR at 15–20× ARR → ~120–200B standalone Starlink valuation.

That matches the idea that Starlink alone could IPO as a mega-cap infra company while still being just one part of the "Muskonomy."

In the scenario file, I anchor Starlink near the top of that band today and then run high‑teens CAGR over 10 years to reflect subscriber growth and enterprise/government expansion.

4. xAI: frontier model lab inside SpaceX

xAI builds Grok and related LLMs and was originally separate from SpaceX.

In early 2026, SpaceX completed an all‑stock acquisition of xAI, valuing SpaceX at about 1T and xAI at around 250B.

Reuters describes xAI as fast-growing but money-losing, burning cash on data centers and compute, and now effectively “burning the cash that Starlink earns” inside SpaceX.

Musk explicitly ties xAI’s future to orbital data centers and Starlink‑class infrastructure: a space AI fusion.

Valuation anchor:

The all-stock deal itself is the cleanest mark: ~250B paper value for xAI as of merger.

That’s a “forward story” valuation vs. current revenue, similar to where investors are treating other top‑tier frontier‑model labs but with a more integrated infra story (Starlink Starship orbital DCs).

Scenario modeling assumes xAI compounds faster than legacy launch—roughly ~20% annual value growth over 10 years if it executes on model quality and monetization.

5. Macrohard: AI agents as “software companies”

Macrohard (aka “Digital Optimus”) is a Tesla–xAI agentic platform: Grok acts as the “navigator” LLM on top of a Tesla-built agent that sees the screen and drives keyboard/mouse inputs.

Musk explicitly describes Macrohard as capable “in principle” of emulating entire software companies, i.e., automating many digital jobs.

xAI originally trademarked parts of the “hard” brand; now that xAI is owned by SpaceX, Macrohard is effectively an application layer sitting on SpaceX‑owned AI infra plus Tesla hardware and data.

Valuation anchor:

No standalone market mark yet. Economically, it’s an ultra‑high‑optionality product line on top of xAI’s base.

In the SOTP, it’s modeled as a modest stub today (tens of billions of option value) but with 20–25% annual growth if it proves itself at scale, because the addressable market “labor cost of digital work” is enormous.

6. Orbital data centers / AI infrastructure

Reuters reports plans for a constellation of up to 1M solar-powered satellites dedicated to AI data centers, leveraging Starlink manufacturing and launch economics.

The idea: use abundant solar energy in orbit, free “cooling,” and Starlink‑class connectivity to run large AI workloads off‑planet, integrating with terrestrial DCs.

This line sits at the intersection of the following:

Starlink (mass satellite production communications),

Starship (bulk deployment of heavy AI DC sats)

xAI (workloads and services).

Valuation anchor:

No explicit valuation yet this is long-duration infra with major capex and regulatory risk (spectrum, debris, space law).

In the scenarios, it starts as a significant but sub‑Starlink stub and compounds aggressively if the business model works, potentially rivaling or exceeding Starlink by year 10 because global AI compute demand is exploding.

7. Moon: “self‑growing city” and Artemis

In February 2026, Musk publicly said SpaceX is now prioritizing building a “self‑growing city” on the Moon over Mars in the near term, with a goal under 10 years.

SpaceX is deeply tied into NASA’s Artemis program via Starship Human Landing System contracts, with uncrewed lunar missions targeted for the late 2020s.

Near‑term revenue will be NASA and other government cargo/crew contracts; long‑term upside is lunar habitats, tourism, ISRU, and possibly materials exports.

Valuation anchor:

Today this is mostly option value on top of concrete NASA contracts.

In the model, Moon starts as a small valuation stub (single‑digit billions) but is given a very high assumed CAGR, because success on a few key missions can unlock big, long‑duration funding flows and infra projects.

8. Mars: deferred but still the endgame

Mars colonization remains Musk’s stated end goal; Starship is explicitly designed to ferry people and cargo to Mars for permanent settlement.

Reuters reporting around the Moon pivot notes that Mars timelines have been pushed out; Musk still talks about uncrewed Mars missions, but the priority is now lunar.

Near‑term revenue would be government science missions and ultra‑wealthy private flights; a true Martian economy is extremely speculative and depends on ISRU, exports, and huge cost reductions.

Valuation anchor

This is the highest‑variance option in the stack: low PV today, theoretically massive upside.

In the SOTP file it’s modeled as a small starting equity value but with ~30% annual “option value growth” if milestones are hit over 10 years.

9. X and X Money: ecosystem distribution and monetization

X is not inside the SpaceX corporate box, but Grok is integrated into X as a real‑time AI assistant trained on its data.

Musk wants X to become an “everything app” with payments (X Money) and commerce.

From SpaceX/xAI’s perspective, X is:

A firehose for training data,

A distribution channel for xAI (Grok, Macrohard),

A place where Starlink and X Money can bundle connectivity payments in emerging markets.

Valuation anchor

X/Money value largely sits outside SpaceX’s cap table; for a SpaceX SOTP, you treat it as strategic synergy, not a full financial consolidation.

In the scenarios, I treat it as a modest option value block tied to how well xAI/Starlink monetizes on the X rails.

1

93