873 Photos and videos

$INV

Wow. Very cool!

Linus has a causal 16m followers on YouTube. Knows his stuff.

Last week, Accelsius was featured in a Linus Tech Tips video!

Our NeuCool® 2P D2C technology was shouted out as a solution built to handle "skyrocketing power requirements" and density increases in mission critical data centers.

Watch here: youtu.be/fJduAvm70Ds?si=RQLm…

1

8

694

$inv @AccelsiusATX

Directionally positive for liquid cooling

Taiwanese Media: Vera Rubin to Adopt 800V HVDC, With Small-Volume Shipments Starting in Q3

ctee.com.tw/news/20260615700…

8

944

$INV @AccelsiusATX

Missed this recent deal.

$BX Blackstone Energy Transition Partners (“Blackstone”) have entered into a definitive agreement to acquire a majority stake in ACT, a leading U.S. manufacturer of highly-engineered thermal management and energy efficiency solutions.

ACT also developing a 2 phase solution.

Another strategic layering in next gen thermal solutions.

I haven’t heard much on ACTs 2 phase tech and how far along they are. But it’s positive to see for theme.

blackstone.com/news/press/bl…

1-act.com/about/news/blackst…

H/T to @Mr_InZanity for highlighting it.

Jun 13

ACT seems to be another player in this field. They traditionally focuses on the aero & defense field but acquired 2-phase cooling assets from $PH before COVID. From what I'm seeing, it's similar to Accelsius's flow boiling solution. (1/2)

1-act.com/thermal-solutions/…

6

1,385

Watching $eose from the sidelines and seeing more and more frustrated long term holders.

Kinda making me bullish again.

Hard to see myself sizing up with Joe at the helm still.

Honestly don’t know how I feel about them hitting guidance again this year.

Not far from halfway through the year with no significant orders or backlog additions.

Still no Frontier or NYSERDA. So most likely delays to those projects timelines already.

Having said that there is still things to like and the price is starting to get enticing again

7

17

3,214

$inv

recommend watching.

Jun 10

"Technology under data centers is changing dramatically—and we're an example of that." Now it's up to industry leaders to communicate these hard-won efficiency gains to local communities, says CEO Josh Claman in a recent DCD webinar.

Watch here: datacenterdynamics.com/en/dc…

2

6

941

$INV @AccelsiusATX $JCI $VRT $AMD $NVDA $CARR

The real potential. Accelsius is mispriced

Start with the size of the TAM. If liquid cooling is a $30b market by 2030 and two‑phase gets 30 to 40 percent penetration, that is $9-12b a year of spend flowing into 2‑phase.

Even if you haircut the whole story and use 20%, you still get $6b. These are not 2040 numbers. They sit in the 2030 window that current strategic and public buyers are looking to underwrite.

Now layer in mkt share. Accelsius is not fighting in a field of 50 vendors. On commercially deployed, rack centric, two phase direct to chip, the realistic competitor set is 2 for now.

If you assume a duopoly where Accelsius plus zutacore own the serious deployments, then 20 to 30 percent medium term share for Accelsius is not aggressive.

At 20% of a $9 to 12b two‑phase slice, you are at 1.8 to 2.4b of annual revenue. At 30%, you are at 2.7 to 3.6b. Even if those are 2030 run rates, the market will price that trajectory years in advance.

You do not even need those full numbers to justify a $2b value today. Take a much more conservative view: assume two‑phase is 9b of the 30b liquid TAM and Accelsius only ever gets 10 percent share. That is $900m of annual revenue. Assume they get halfway there by the early 2030s and are running at 400 to 500m a year.

Now apply comps. CoolIT was bought for roughly $4.75b on around 500m of forward revenue. Call it a 9 to 10x.

This is being paid today, for a company that lived most of its life as a niche copper plate manufacturer, not as one of two gatekeepers to two‑phase D2C for Rubin and Feynman class racks.

If strategic buyers are willing to pay 10x revenue for a mature single phase centric business, the right multiple for a faster growing, two phase heavy platform with defensible IP and strategic distribution is not lower.

Run the math. Accelsius at $200m of revenue on a 10x multiple is already worth 2b. At 250m, even a 8x multiple is 2b. At 300m and 7x, you are at 2.1b.

All of those revenue numbers are consistent with low double digit share of a 9 to 12b 2phase market and well below the 20 to 30% share that a duopoly framing implies.

Then look at where the company actually is in the lifecycle. They have commercial products: IR150 integrated racks and MR250 row systems.

They have strategic distribution through $JCI and Legrand. They have real deployments, a pipeline running into the billions, and a path to positive cash flow in the near term.

The business is not pre‑revenue. It is in the “bookings inflect, revenue follows” zone where growth investors usually pre‑empt.

You also have the structural constraint argument that the market is only beginning to price.

GPUs are moving from roughly 80‑100 kilowatts per rack to Rubin and Kyber to Feynman racks in the 200 to 600 and 1000kilowatt range.

Air and simple water loops do not scale linearly. Power limits, water regulations and PUE targets force operators into two‑phase if they want those densities.

Every Rubin‑class rack added after 2027 is more likely to need a two‑phase or at least two‑phase‑capable architecture than not.

The demand driver is not discretionary. It is physics and policy.

If you combine those facts, the mismatch becomes clear. A company that can plausibly grow into 200 to 300 million dollars of annual revenue in a year or 2, with a realistic path to 500 million plus and structural technology scarcity, should not still be priced sub billion.

A $2b mark today simply assumes Accelsius achieves the kind of scale where a CoolIT style take out becomes feasible, and that the market is willing to pay similar revenue multiples for a more strategic, more growthy asset.

Put differently: if you believe in a $30b liquid‑cooling market by 2030, a 9 to 12b 2 phase slice, and a future where Accelsius holds even 10% of that slice, then a 2 billion dollar valuation today is not aggressive.

1

1

7

1,099

$INV

If liquid cooling is a $30B market by 2030 and 2‑phase takes 30–40%, that’s a $9–12B 2‑phase TAM.

In a practical duopoly now, Accelsius only needs 10–20% share to be doing $1–2B of revenue. At CoolIT’s ~10x sales take‑out multiple, that supports a $10–20B valuation vs ~$1B today.

You can half that market share too and still be at a 5x from today.

Accelsius and Zutacore are the only companies I know of now that have a commercially ready product.

Fair to assume they will take a good chuck of this initial market.

The AI rack wave still isn’t fully priced into two‑phase cooling.

$INV @AccelsiusATX $JCI

Cooling in next‑gen AI data centers is about to be a massive market

Rubin‑class AI racks (~220 kW) carry ~$120k of cooling hardware per rack, or roughly $0.9–1.5m of cooling capex per MW (including rack facility‑side liquid/2‑phase systems).

Global DC capacity could add ~115–135 GW of greenfield build from 2028–35, mostly driven by AI.

If 40–60% of that is AI‑dense and 80–95% of that AI load is liquid‑cooled, you get ~40–77 GW of new liquid‑cooled capacity over that period.

With two‑phase capturing just 10–25% of liquid deployments in ultra‑dense zones, that implies ~5–15 GW of new two‑phase‑cooled IT load and roughly $9–15B of two‑phase cooling hardware spend on greenfield alone.

If 2‑phase ends up with 40% of liquid‑cooled AI capacity, it’s not a niche. On 2028–35 greenfield alone, that’s 16–30 GW of 2‑phase‑cooled load and roughly $15–45B of cooling hardware tied directly to AI racks.

Source MS

5

2

17

3,185

$INV @AccelsiusATX $JCI

Cooling in next‑gen AI data centers is about to be a massive market

Rubin‑class AI racks (~220 kW) carry ~$120k of cooling hardware per rack, or roughly $0.9–1.5m of cooling capex per MW (including rack facility‑side liquid/2‑phase systems).

Global DC capacity could add ~115–135 GW of greenfield build from 2028–35, mostly driven by AI.

If 40–60% of that is AI‑dense and 80–95% of that AI load is liquid‑cooled, you get ~40–77 GW of new liquid‑cooled capacity over that period.

With two‑phase capturing just 10–25% of liquid deployments in ultra‑dense zones, that implies ~5–15 GW of new two‑phase‑cooled IT load and roughly $9–15B of two‑phase cooling hardware spend on greenfield alone.

If 2‑phase ends up with 40% of liquid‑cooled AI capacity, it’s not a niche. On 2028–35 greenfield alone, that’s 16–30 GW of 2‑phase‑cooled load and roughly $15–45B of cooling hardware tied directly to AI racks.

Source MS

1

2

14

4,225

$INV

I’ve got 2028 as a ~$2-3b market for 2 phase cooling.

@AccelsiusATX and @ZutaCore are the 2 leaders and will be poised to take a fair chuck of that market early on.

@AccelsiusATX are already working with hyperscalers and silicon developers to develop architectures for the next iteration of chips.

IMO they will be supply constrained when this tech is needed in a couple of years.

1

6

653

I’m conflicted in the possible outcomes here.

You’ve got a TAM which is about to hockey stick for 2 phase. $10b 2030 2 phase market.

Multiple sources are forecasting this. But this is 2028 revenue. Bookings and partnerships should start to materialise over the next 12 ish.

I think INV would be crazy to let this go sub $2b

I would love to see them do a carve out IPO of Accelsius.

INV can sell just enough via a secondary to get their $300m to keep their buffer.

This achieves three things

•Gives you liquid price discovery on Accelsius while $INV is still the main beneficiary of upside.

•De‑risks the platform (buffer cleaner balance sheet) so $INV can survive execution volatility on the way to 2028 and bring to market new technologies

•Minimizes near‑term dilution and avoids forced capital raises at the parent at bad prices because Accelsius can increasingly fund itself directly.

For $INV holders, this is superior to a private sale imo.

We will get a mark to market value on Accelsius.

Get more of a pure play valuation.

With a private sale we will miss out entirely on that giant TAM capture.

Jun 11

IMO, doubtful. My guess at this point in time maybe around $100mm in 2027. Don't forget, INV mgmt is guiding cash flow breakeven for INV in mid 2028, so I doubt they are expecting Accelsius to hit anything near $300mm in 2027.

2

1

5

1,425

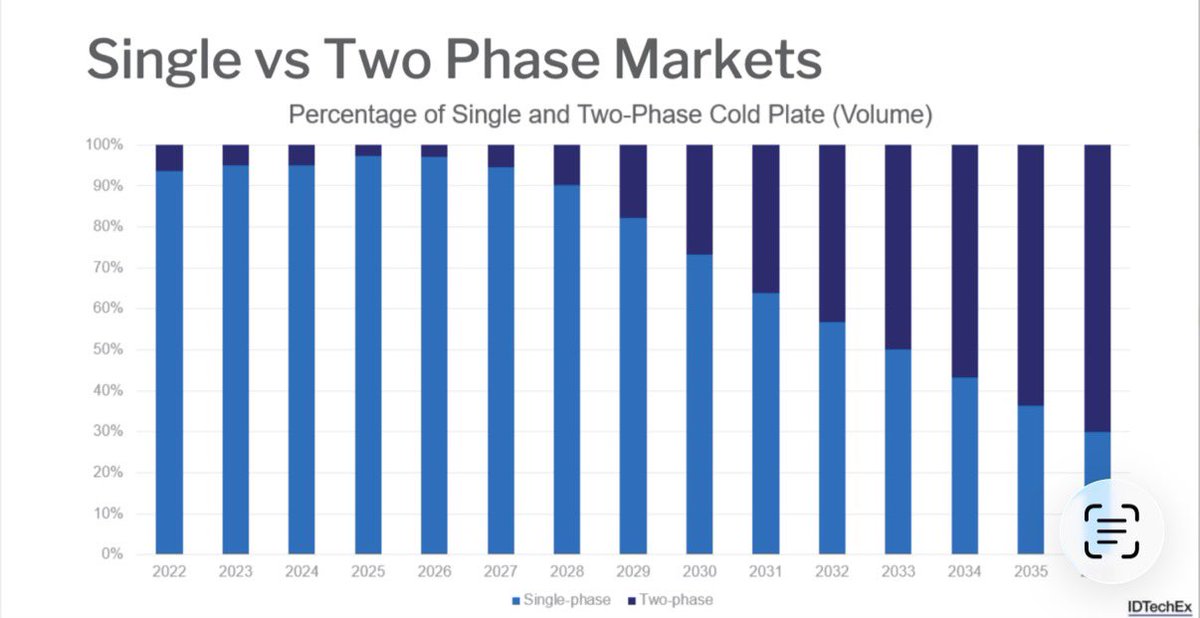

Little bit of colour on 2 phase and the future of cooling from Zutacore and open compute

It’s going to be a huge market for 2 phase

opencompute.org/events/past-…

4

9

1,068

LM retweeted

Jun 10

"Technology under data centers is changing dramatically—and we're an example of that." Now it's up to industry leaders to communicate these hard-won efficiency gains to local communities, says CEO Josh Claman in a recent DCD webinar.

Watch here: datacenterdynamics.com/en/dc…

2

11

2,012

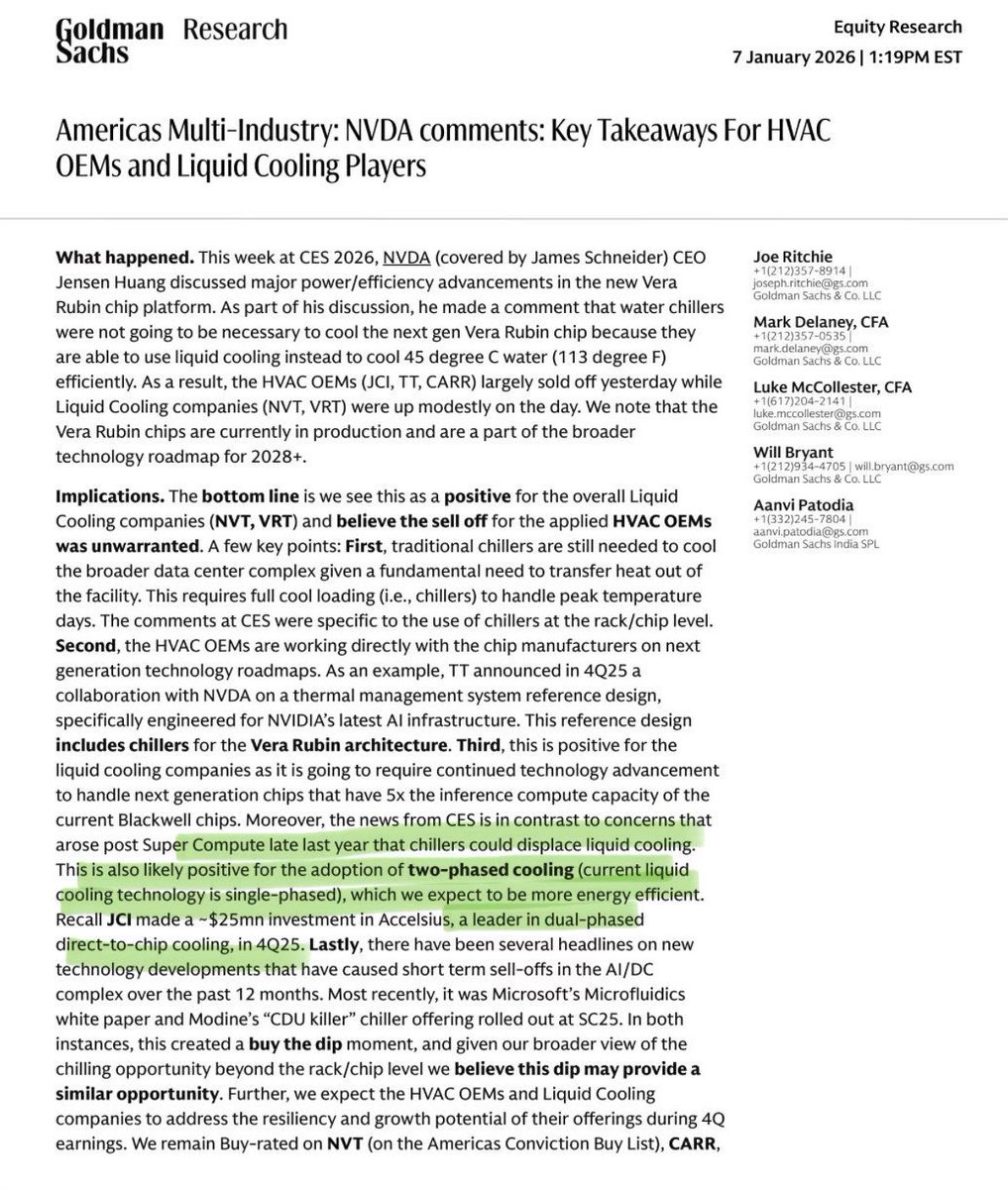

CEO of $CARR David Gitlin on 2 phase liquid cooling- "it's not whether, it's when"

"I think with the demand we're seeing for cooling and the properties of a refrigerant over water, I do think we move into that 2-phase direction"

$CARR are an important player in the 2 phase space with their investment in Zutacore which they just increased.

Therefore listen to what they have to say as it relates to $INV $JCI and @AccelsiusATX

This aligns with what Josh at Accelsius is saying too. This is a theme that is starting to materialise and will probably start to accelerate in the next couple of years epically with the Feynman generation of chips in 2028

1

3

7

3,143

Same ol’ story with $eose

God I’m bullish on the theme.

But it’s been the same story for a couple of years now. No organic backlog growth.

Shares have gone from ~50m in late ‘22.

600m fully diluted as of today’s

Now there is a potential for 800m shares.

Incredible destruction of value.

They’ve got to start doing something soon.

There is no denying the opportunity. $flnc is proof of that.

Where are the so called hyperscaler orders Nathan?

$EOSE

Today feels like another round of mechanical price action disconnected from the broader market - just like before previous offerings.

Can't wait for the day Eos generates organic orders without having to dilute shareholders to fund them. Feels like it'll never come.

4

21

13,322

What a hypocrite

This guy resides in Monaco to evade taxes

Plus he’s dating a Billionaire

Lewis Hamilton says there should be a limit to how much wealth one person can have

"One of the things that I struggle with every day is that there is such a disparity between the wealthy and the poor”

"When you drive around LA there's still so many people living on the streets. You shouldn't be able to have billions"

"I think there should be a limit to how much you can have because there's enough to go around for everyone”

Community note

In order to avoid tax, Lewis Hamilton lives in Monaco and Switzerland. He also used a corporate leasing structure to save over £3 million in taxes when buying his £16 million private jet in 2013.

x.com/exRAF_Al/statu…

3

687