On a mission to build 100,000 starter homes in existing neighborhoods.

Joined September 2022

- Tweets 77

- Following 64

- Followers 764

- Likes 596

6 Photos and videos

Pinned Tweet

26 Feb 2025

Thrilled to announce @BuildCasa's partnership with @ChanZuckerberg to build homeownership opportunities for low income Californians. These units will be built without government subsidies for a fraction of the cost of government funded affordable housing.

26 Feb 2025

The Chan Zuckerberg Initiative is investing $750,000 in BuildCasa, which aims to seamlessly add more affordable housing in residential areas. f-st.co/lnaAk1T

1

4

26

5,069

I haven’t been this excited about a political candidate since Obama ran for president in ‘08.

Matt Mahan is the rare politician who both a world class talker and doer. He cares about people but is not anti-business/progress. He’s willing to speak truth to power even when it upsets the ruling class.

A quick anecdote: we were facing a silly permitting delay on new starter homes @BuildCasa was developing in SJ which is one of the first for sale ADU AB-1033 projects in the state. @MattMahanSJ jumped in personally to help @DonovanBuilds and @benjamintink cut through the red tape and his team had continued to stay engaged through approval.

More here on the incident from the excellent @pahlkadot eatingpolicy.com/p/better-po…

Jan 29

A couple weeks ago, I came home and my wife, Silvia, said something I almost couldn’t believe.

She looked at me and she said, “I think our state needs you.” Because she believed I could help our kids. Help San José. And help California.

And if you know anything about Silvia — when she talks, you listen.

So I’m running for Governor of California — because we can do better.

I know we can, because we’re proving it in San Jose.

We’ve reduced unsheltered homelessness by nearly 1/3rd after a decade of growth. We were rated the safest big city in America last year for the first time in over 20 years. We’re the only city to have solved 100% of homicides nearly 4 years running. And we’re taking on affordability with urgency and honesty — unlocking thousands of housing units in the past couple years.

We need to stand up for our rights, for our freedoms and for our neighbors. We need to use the tools we have at hand to protect our democracy.

One tool is the law. The other tool is our results. We have to use both.

That’s how we fix California.

We don’t just need to be against something. We need to be for something — a government that proves it can solve problems for working people again.

And before we ask Californians to give more, we owe them proof that their government can do better.

So I’m running to bring focus back to government. To give cities the tools they need to succeed. To show that the best resistance to division is results.

And to prove that California can work again — for everyone.

That’s why I’m running.

And that’s the future Silvia and I are fighting for.

mahanforcalifornia.com/

36

7

167

14,263

BuildCasa retweeted

Jan 29

In a public meeting for our 1 story duplex in Sacramento that @BuildCasa is building in partnership with @czi.

This is for separate condos so that the units can be owned by folks making less than the 80% AMI.

We are getting comments about the number of stop signs in the area.😂

1

1

7

232

“Buy land, they’re not making any more of it” - Mark Twain

Exception: we literally are making more buildable land through small lot subdivision @BuildCasa

Feb 1

Datacenters, raw materials, and land

If intelligence is rapidly becoming free, expect a rapid rotation out of bytes and into bits.

A lot of “blue chip” assets will soon be repriced.

3

9

954

Even though institutions who own >1K homes only make up .5% of the market, I get the populist appeal of this proposal.

Key make or break Q's:

- how do you define an institutional investor?

- does this apply to home flippers like Opendoor?

- what about developers who buy homes to build more through upzoning?

cnbc.com/2026/01/07/trump-ho…

3

3

12

859

Thanks to @TobiasPeterAEI from @AEI for mentioning the benefit of treating development profits on homes built and sold to homeowners as a capital gain vs. ordinary income in his testimony to the House Committee on Financial Services.

Today the tax code favors developing homes to sell to PE vs. homeowners. If you want more supply for homeownership, you need to incentivize it!

1

6

12

5,747

Had a great time chatting about new strategies in infill housing development like SB684 on the Risk of Ruin podcast featuring @KAErdmann and a Portland homebuilder.

8 Dec 2025

How did we go from The Big Short, to a housing shortage?

New episode featuring @KAErdmann, a homebuilder/AP named Cody, and @BenBear

We talk about how housing became such a pain point, and also a very specific housing related bet.

Link 🔽

2

5

2,580

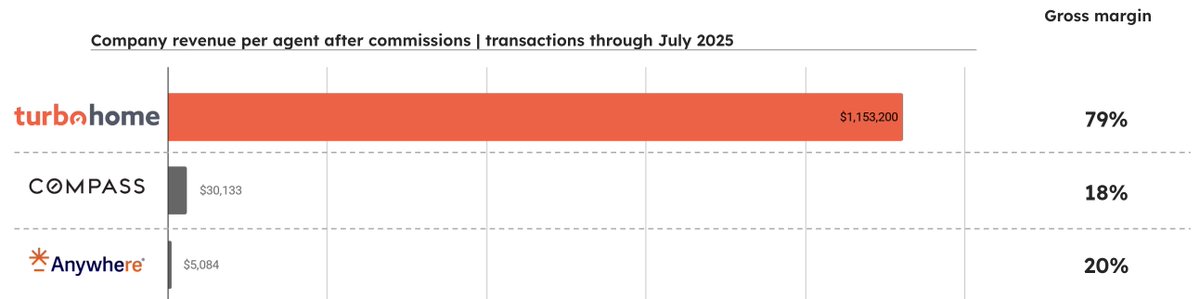

The proposed merger between Compass and Anywhere will create the largest real estate brokerage in America. Together they will have >300K agents, earn $13B in revenue, and have ~18% market share in the US.

I've seen two common reactions to the news:

1) Why isn't the market cap higher than $10B given the revenue scale? Answer: Traditional brokerages only have 10-20% gross margins because almost all of the revenue goes out the door in agent commissions.

2) Does this merger mean that new entrants like TurboHome are DOA? Our view is that Compass is the final boss of brokerage 1.0 for traditional agents. They've done a fantastic job of getting to scale through M&A and building great tech for agents.

What they don't do and structurally can't do with their business model is voluntarily lower fees for consumers and introduce direct to consumer experiences. If you have a 20% gross margin business, you can't voluntarily lower agent commissions. This the classic innovator's dilemma challenge that big incumbents face. For traditional brokerages like Compass, the agent is the primary customer. The goal is to have as many agents as possible charging the highest possible commissions.

There will always be a place for traditional agents. If you look at tax preparation as an analogy, roughly half of consumers still use a traditional CPA and half use an online platform. Of the half that use an online platform, TurboTax has 80% marketshare similar to what you see in other online businesses with power law dynamics.

At TurboHome, we've redesigned the entire homebuying process to serve the consumer. Our business model is built around leveraging technology to increase the number of clients an agent can serve without reducing quality of service.

As a result, our net revenue per agent is nearly 35X higher than traditional brokerages and our gross margin is 4X higher. We do this while winning 50% of offers and maintaining an NPS of 90. Because we allow consumers to leverage their savings to lower their interest rate, ~70% of buyers we introduce to a lender end up attaching mortgage compared to ~15% for traditional brokerages.

As Robinhood shows in stocks with a 30X revenue multiple, brokerage can be a very valuable business model. The transactional scale is massive, you don't have to do collections since fees are paid through escrow, and if you have software like margins and prove the ability to attach adjacent services you can get software like multiples.

Nobody has done this in real estate yet, but the lane is wide open. Transaction costs in the US are 4-5X higher than other developed countries like the UK and a disruptor is needed to make homeownership affordable again and put money back in the pockets of consumers, not agents.

2

4

18

2,499

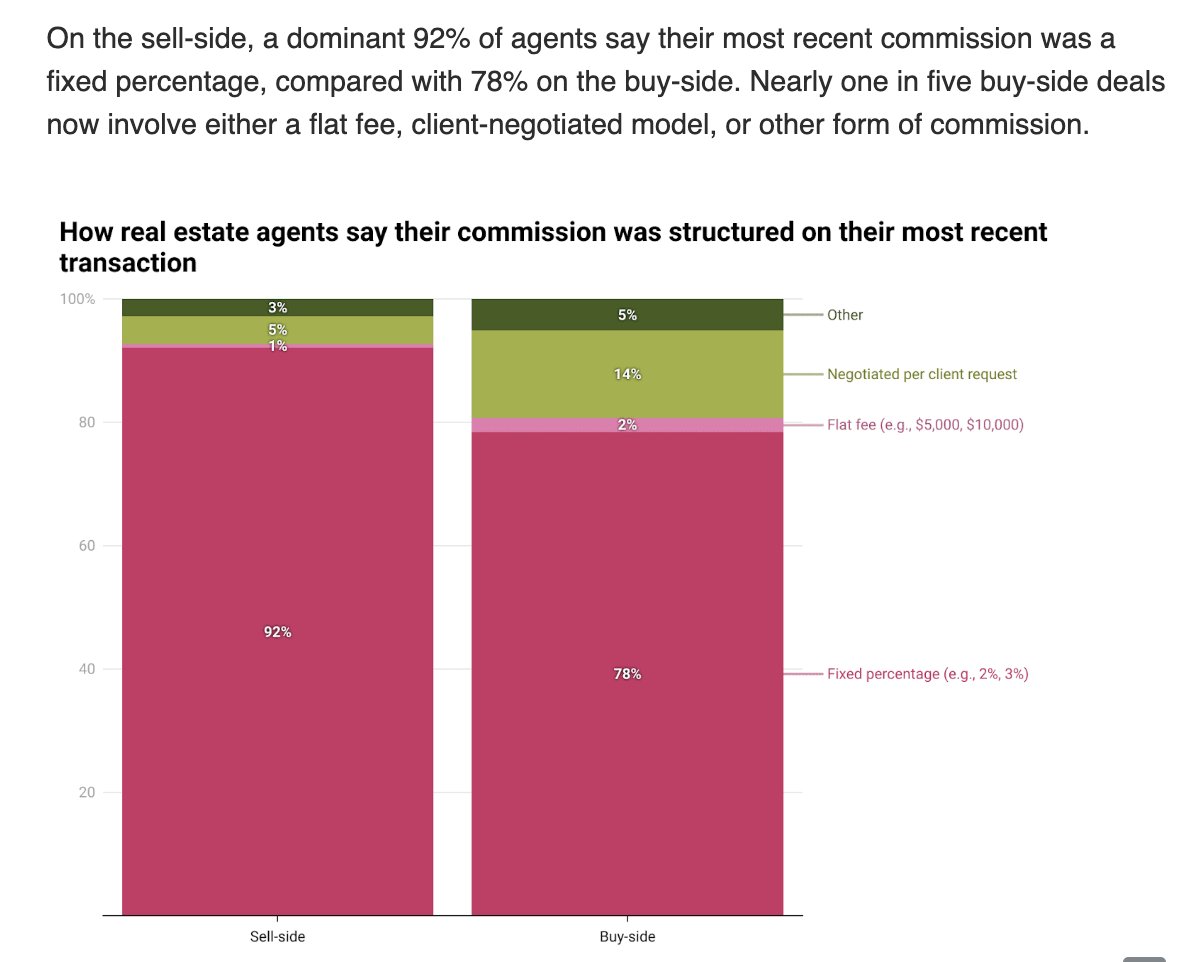

It's early days, but agent commission models are starting to change for homebuyers.

New data from @NewsLambert shows that 1/5 buyside transactions now include either flat fee or negotiated commission rates.

3% really doesn't make sense in a world where ~80% of buyers are finding the home themselves.

5

4

17

2,301

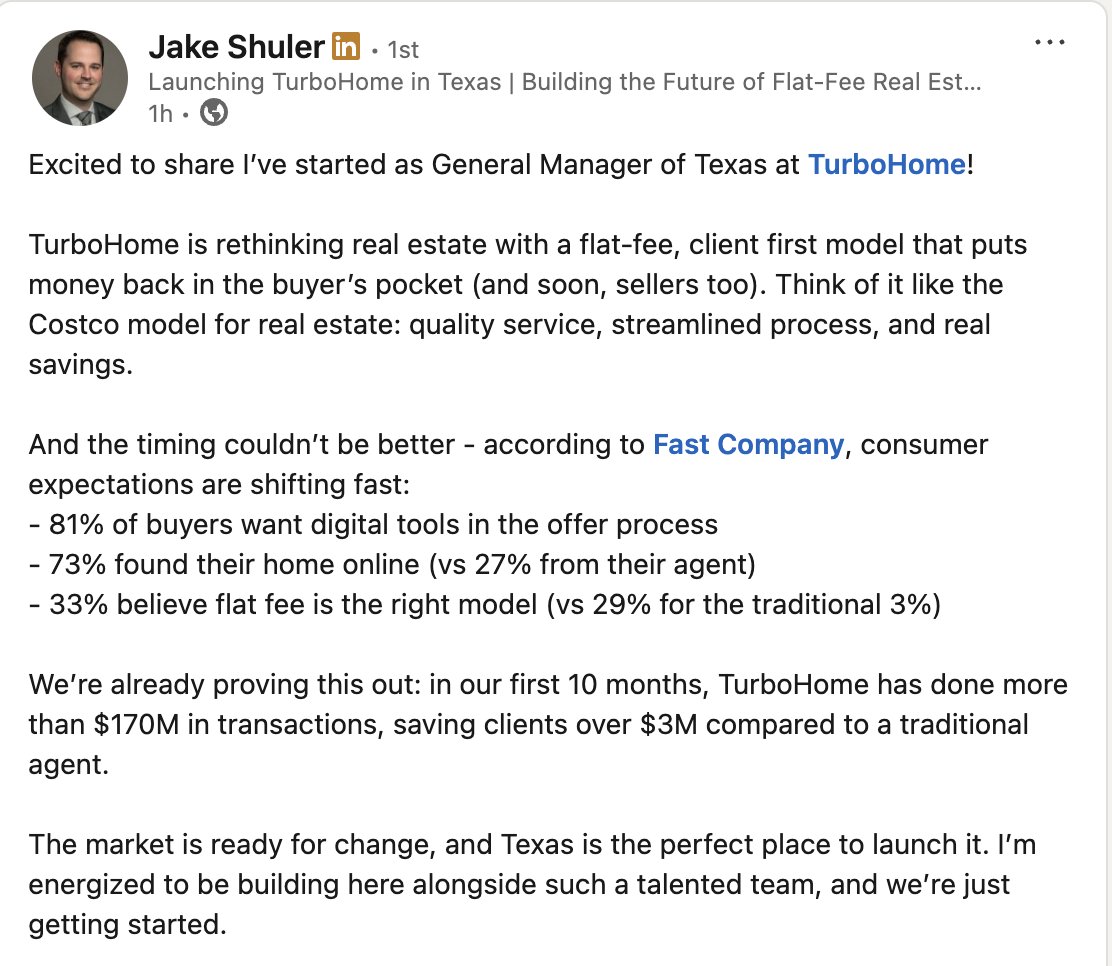

Thrilled to welcome Jake Shuler to the @_TurboHome team as GM for Texas. Jake's most recent role was running the 0-> 1 bets for @Opendoor working directly with their leadership team.

We already have several hundred leads coming in through our lender partners in TX and we couldn't ask for a better leader than Jake to drive our expansion.

5

2

19

1,937

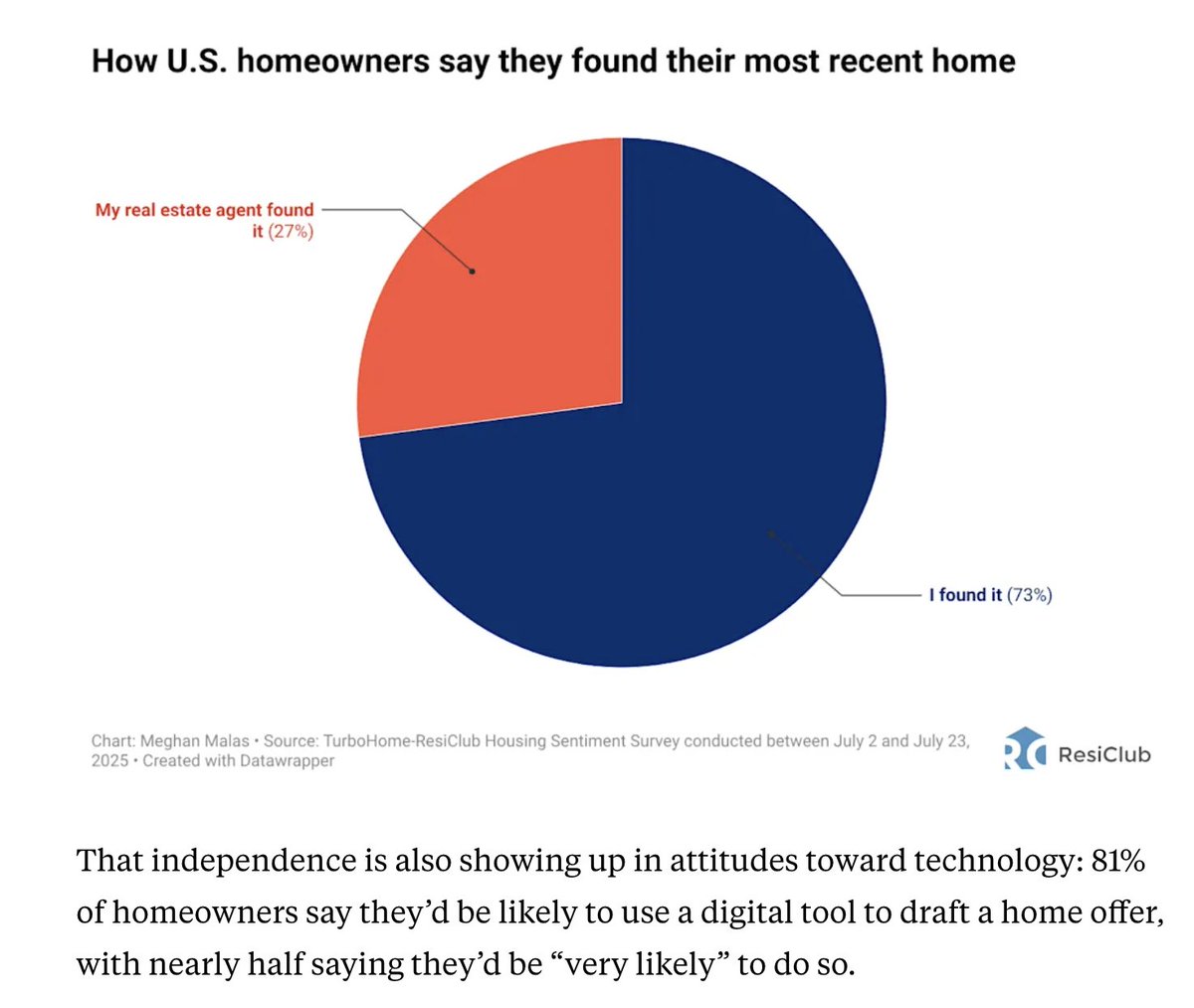

Real estate agents used to find the house for you, now they don't and yet commission models haven't changed.

Great survey data from @NewsLambert in @FastCompany:

- 73% of homebuyers found the home vs. 27% found by their realtor

- 33% think agents should be paid a flat fee vs. 29% for commission

Buckle up, things are about to change fast. Link below.

7

9

45

5,459

BuildCasa retweeted

5 Aug 2025

Next week, I'll be joining @BuildCasa to explain how small developers can use SB 1123 to build cottage courts, townhouses, and small-lot single-family homes across the state. Tune in!

5

9

35

9,274

BuildCasa retweeted

4 Aug 2025

You are going to love what @DonovanBuilds and @BuildCasa are doing in SD.

1

3

206

Big Fortune 500 builders pay 21% tax on both for rent and for sale housing. Small builders and their investors pay up to 37% on units built for homeownership.

Want more small builders and housing overall? Level the tax playing field.

8 Jul 2025

Big builders are taking over.

In 2024, the top 10 homebuilders closed 44.7% of all new single family homes sold, up 5x since 1989.

The top 10 homebuilders now account for 30.1% of all SF homes completed (which includes custom homes).

If you're trying to build today, you're competing with giants.

3

6

763

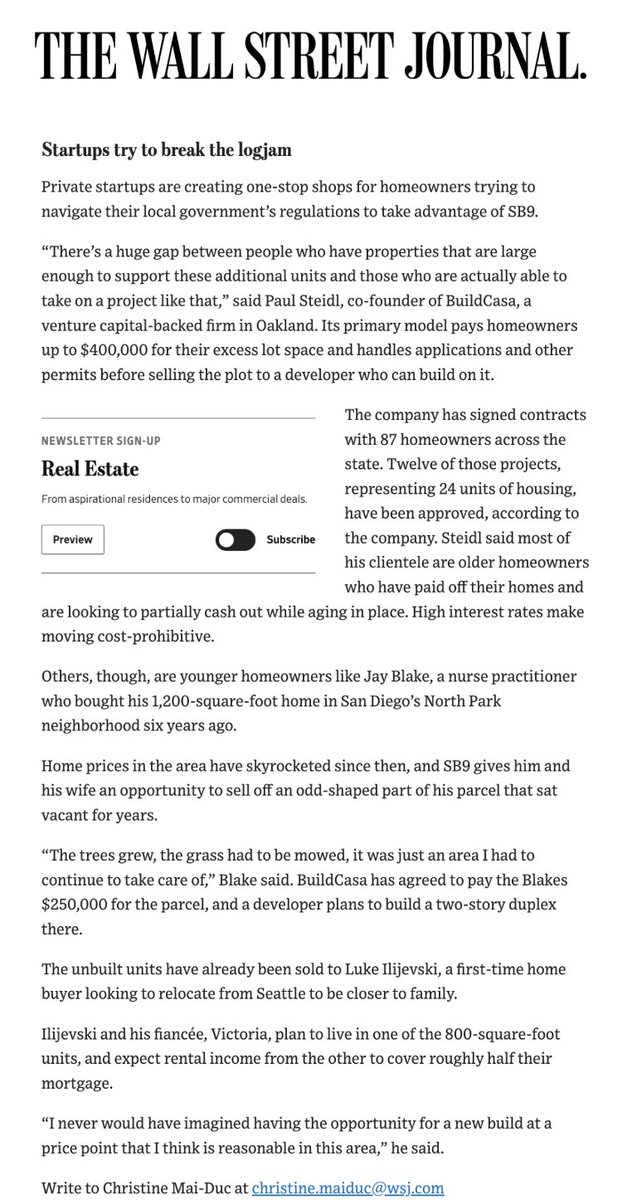

Excited to share that the first 2 condos built via @BuildCasa’s partnership with @ChanZuckerberg are now available for reservation in Sacramento for $329K (30% cheaper than typical home).

Homeownership has always been the most reliable path, but with high rates and limited starter home supply the door has been slammed shut.

These units are being built using a combination of SB9 and AB1033 to unlock homeownership opportunities affordable to low income Californians without government subsidy.

The first unit was reserved in less than a week, but we have one available to qualifying 80% AMI buyers.

Link below.

5

11

70

20,415

If you’re curious to learn more about SB1123/SB684 check out a free webinar @BuildCasa is hosting led by @DonovanBuilds and @benjamintink. Link below.

1 Jul 2025

Overshadowed by yesterday's CEQA news, but:

SB 1123 goes into effect today.

You can now build 3-10 townhomes or condos on most vacant or uninhabited single-family lots in CA, as long as there have been no rental tenants in the past 5 years

2

3

11

3,473

Thought provoking piece from @ConorDougherty in the @nytimes on the role underutilized single family homes and lots could make in easing the housing shortage. One of the cool things we see @BuildCasa is homeowners willingly giving up their extra lot space to make room for new homeowners.

3

2

21

1,780

BuildCasa retweeted

29 Apr 2025

2

1

8

244

Great deep dive from @jamie_rod at @BusinessInsider on how the landscape has changed for buyers post NAR settlement featuring a @_TurboHome buyer along with insights from Leo Pareja, CEO at eXp. Since launching late last year, we've helped buyers save $1.5M. Link in the comments.

1

6

10

2,973