High Performance Racing Engine CNC Machine Shop - Engineering - Prototype- Development - Testing - Compton, California 310-427-7486

Joined November 2012

- Tweets 973

- Following 876

- Followers 459

- Likes 1,449

61 Photos and videos

Jun 9

Thank you!

Jun 9

Pre-market analysis Tuesday 9th June, 2026

1. Market Summary

Monday did what it needed to do after Friday’s AI-led puke, but it did not repair the tape.

$SPY gapped from Friday’s 737.37 close to 743.36, traded an inside day between 745 and 738, then faded back to 739.22, up only 0.23%. $QQQ did better at 1.56%, but that was largely $SMH doing the heavy lifting with a 5% rebound. That matters. This was not broad risk-on. It was an oversold AI and semi reflex bounce inside a damaged volatility structure.

The rally since late February has essentially been an AI trade, and Friday’s sell-off was also an AI trade. Ex-AI, the index is basically unchanged since the war started. So the broad economy did not suddenly break on Friday. The crowded AI complex broke first.

Base case: tactical bounce attempt into OPEX, but not a clean low yet.

The key pivot is $SPX 7,430. Above that, the market can squeeze back towards 7,450 and then 7,500. Below 7,400, the negative gamma trap remains live. Below 7,350, downside acceleration becomes the trade.

2. Macro analysis

US: Friday’s NFP was the macro spark that hit an already stretched AI tape. Payrolls rose 172k in May and unemployment held at 4.3%, which is strong enough to keep the Fed cautious and reduce the odds of any near-term easing. The 10Y yield pushed back towards the mid-4s after the print, and the dollar strengthened, especially against yen around the 160 area.

The next hard catalyst is CPI on Wednesday, followed by PPI on Thursday. That makes today a positioning session, not a clean macro clearance session.

Fed: the market is moving away from cuts and back towards higher-for-longer risk. A Reuters poll now shows economists expecting the Fed to hold rates at 3.50% to 3.75% through the rest of 2026, with the strong jobs print and oil-linked inflation risk doing the damage.

Geopolitics and oil: Israel and Iran have paused direct attacks after Trump pushed for a halt, which has helped oil ease from the panic highs. But Brent still remains elevated near the low 90s, so the inflation impulse has not gone away. If oil resumes higher, that pressures CPI expectations and caps equity multiple expansion.

Eurozone: inflation is not benign. Euro area May inflation rose to 3.2% from 3.0%, with energy the key pressure point. The ECB is expected to raise the deposit rate by 25bp to 2.25% this week. That keeps global policy risk tighter, not looser.

China: the May manufacturing PMI eased to 51.8 from 52.2, still expansionary but no longer accelerating. That supports the idea that China is not the immediate source of global risk-on leadership today.

Japan: Q1 GDP was revised down to 1.8% annualised from 2.1%, mainly on weaker capex. Japan remains vulnerable to oil, yen weakness and imported inflation, so any further Middle East escalation is a direct macro risk for Japanese equities and the yen.

Friday was a convergence event, not just one headline. AVGO guidance, hot NFP, war risk, higher yields, dollar strength, oil volatility, tech de-risking and skew repricing all hit at once.

3. Momentum and breadth

Breadth is the main reason I am not calling this a clean risk-on reset yet.

Nasdaq stocks above the 5-day average are only around 37.5. S&P tech stocks above the 5-day average collapsed to near zero but rebounded to 6.8, which is a brutal internal read even with $QQQ green. $MMTW is only around 46.3 and the McClellan style read remains negative. Russell breadth is better, with $RTW around 53, $R2FI around 55.5 and $R2TH around 57.7, but that is mid-level participation, not a thrust.

So the message is: exhaustion bounce possible, but breadth has not confirmed a durable low.

This is exactly the kind of tape where the index can rally while many stocks still fail. I want leadership, not laggard dip buying. Semis can bounce hard, but unless breadth expands beyond semis, the tape remains fragile.

4. Volatility

Vol has cooled, but the regime has changed.

$VIX is back near 18 after spiking above 21, $VVIX has backed off to around 92, and $VX1D is around 16. That confirms fear has faded from Friday’s peak. But this is not the old 13 to 15 $VIX grind regime. Front-end vol is still carrying a war, CPI, Fed and OPEX premium.

Put/call data is elevated but not panic. Total put/call is around 0.92 and equity-only is around 0.71. That says hedging demand is present, but we are not at a washout sentiment extreme.

Gamma is the big trap. The $SPX flip is just below spot at around 7,430 with. Below spot, there are downside negative GEX nodes. That means rallies can squeeze, but dips can accelerate quickly. This is no longer a passive buy-the-dip tape.

Therefore naked short-dated calls are much less attractive unless the first hour confirms breadth expansion.

5. Credit and liquidity

Liquidity is not the problem today.

SOFR-IORB is sitting around -0.02, so there is no obvious repo stress signal. Credit also is not screaming systemic stress. $HYG/TLT is firm, $HYG itself is choppy but not breaking down, $KRE has stabilised, and regional banks are actually showing decent relative strength in the ETF file.

That said, $LQD/HYG remains soft and rates are still restrictive. Credit is not confirming a major risk-off spiral, but it is not strong enough to validate a full risk-on chase either.

Read: liquidity backdrop is acceptable, credit is stable enough for a bounce, but positioning and vol structure remain the bigger risk.

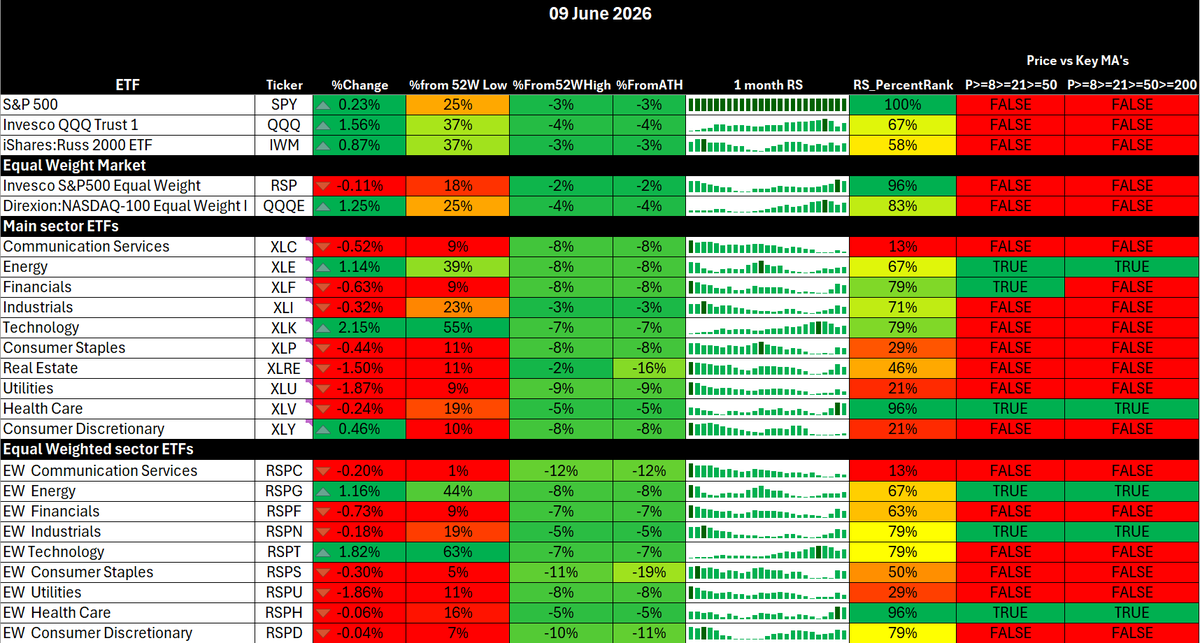

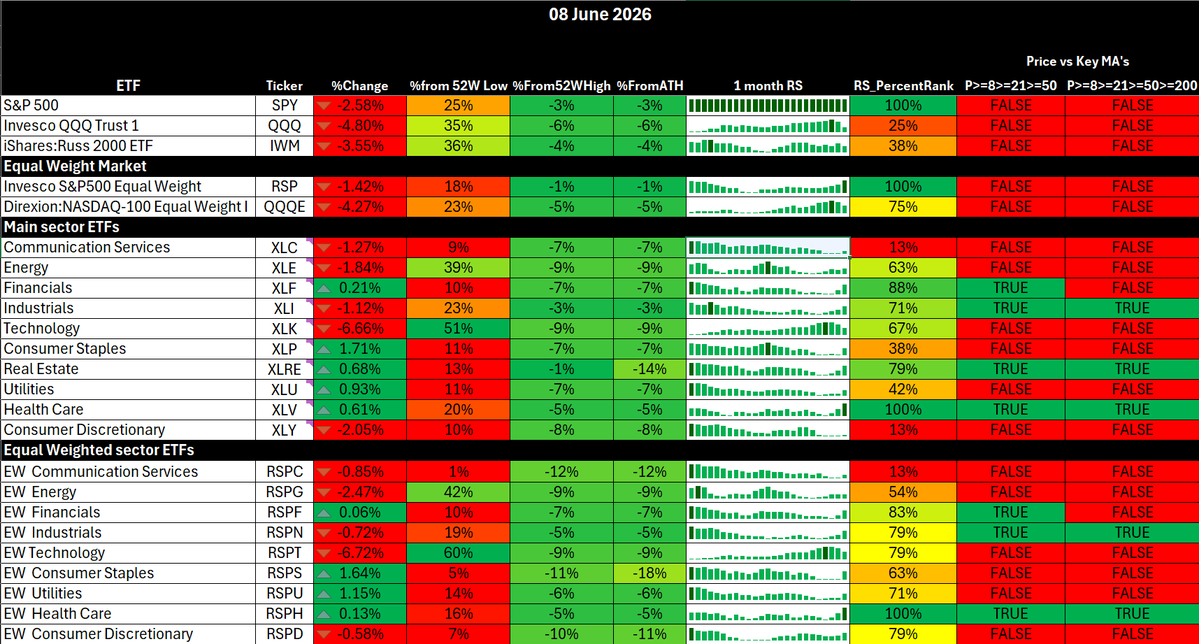

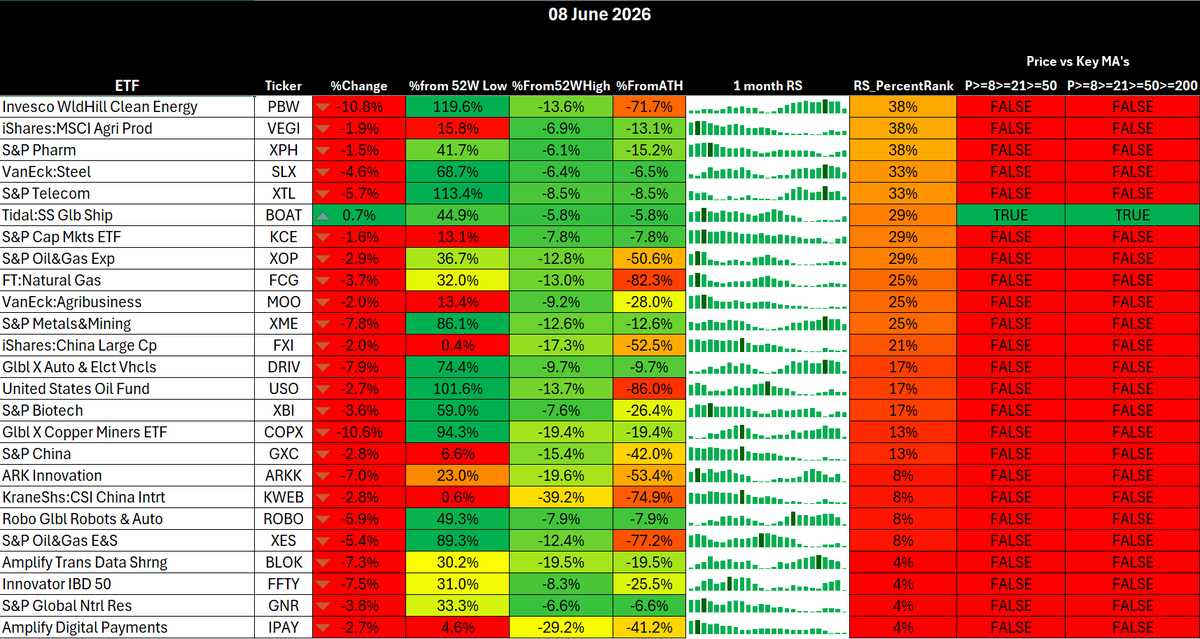

6. ETF and Sector rotation

ETF snapshot: the market is split. It is not defensive panic, but it is also not broad growth leadership.

High RS pockets with MA confirmation: $XTN, $XLV, $RSPH, $XHS, $PEJ and $KRE.

That is not a pure AI risk-on leaderboard. It is a weird but useful mix: transports, healthcare, leisure and regional banks. The market is rewarding selective value, healthcare stability and parts of cyclicals, while still giving semis a powerful oversold bounce.

Growth and cyclicals were the clear tactical winners, with with $SMH 5%, $XLK 2.15%, $IGM 1.82%, $RSPT 1.82% and $SPHB 1.85% also bouncing. But the MA condition is still not confirmed for $SMH, $SOXX, $XLK or $QQQ, so this is a rebound, not yet a repaired trend.

Defensives: $XLV remains the standout defensive leader with MA confirmation. $XLP is soft, $XLU is weak and $XLRE is lagging on the day. So this is not classic defensive leadership across the board. It is healthcare-specific defensive strength.

Cyclicals: $XLE is still constructive and has MA confirmation, but it is not top-tier leadership. $XLF is decent but not clean enough above the longer MA stack. $KRE and $KBE look better than broad financials, which is notable because regional banks are not behaving like credit stress is building.

7. Summary

Tactically I'm mildly bullish for a bounce into FOMC and OpEx, but not structurally risk-on yet.

The tape can squeeze if $SPX reclaims 7,430 and holds above 7,450. That would favour semis and tech and defined-risk index upside. But below 7,400, the negative gamma structure is still live. Below 7,350, I stop thinking bounce and start thinking downside acceleration.

My bias: bounce first, deeper retracement later. Today is a stock selection tape, not a “buy anything” tape.

23

Jun 8

Solid ! Thank you for the info and advice

Jun 8

Pre-market analysis Monday 8th June, 2026

1. Market Summary

Friday was not a normal dip. It was a proper AI/growth de-grossing event, with $QQQ down 4.80%, $SPY down 2.58%, $IWM down 3.55% and $SMH down 9.22%. The key point is that the market has moved from the old positive gamma grind regime into a much more unstable negative gamma environment.

My read: tactical bounce likely, durable low unproven.

The best base case today is a mechanical rebound attempt, not a clean risk-on reset. $SKFD is near zero, which is exactly the kind of exhaustion read that often gives a 1 to 3 session bounce. But the character of the tape has changed.

The $SPX flip cluster around 7350-7400 is live. Above 7,400, the market can squeeze back toward 7,500 and potentially 7,570. Below 7,350, there is potential for acceleration downwards through 7,200 and potentially to 7,000 gravity well.

Net GEX flipping negative and ATM IV jumping from 13% to 19% means this is no longer the calm dip-buying regime that carried the tape for the last two months.

So the lean is: respect the bounce, do not trust it blindly. First move higher can be violent because vanna is loaded, but the second test after the bounce is what matters.

2. Macro analysis

US macro is now a headwind, not a tailwind. The May payrolls print came in hot at 172k, pushing the dollar to a two-month high and dragging rate hike expectations higher. Goldman has pushed its Fed cut call into 2027, and markets are now pricing a much higher chance of Fed hikes by year-end. That gives the equity market less room to ignore inflation, oil and geopolitical risk.

The bigger near-term catalyst stack is nasty: CPI on 10 June, the SpaceX IPO on 12 June, ECB on 11 June, FOMC on 16 to 17 June, and quarterly OPEX shortly after. We can see elevated $SPX implied vol into CPI and FOMC, which means options are not treating this as a one-day isolated event yet.

Europe is also tightening into weakness. Reuters has the ECB expected to hike 25 bps to 2.25% on 11 June as energy-led inflation pressure forces a hawkish response, while the $STOXX 600 is under pressure from Middle East escalation, oil and AI-related weakness. That is a stagflationary mix, not a clean global growth backdrop.

China is mixed. Exports are expected to be strong, around 15% year-on-year, helped by front-loaded orders and chip demand, but the quality of that growth is questionable because new export orders are already softening. China is a support for global trade headlines, but not enough to offset the AI unwind by itself.

Japan is not a risk-on offset either. Q1 GDP was revised down to 1.8% annualised from 2.1%, driven by weaker capex, while energy pressure and yen weakness keep the Bank of Japan in a difficult spot.

3. Momentum and breadth

Breadth is damaged but not washed out. That is the awkward middle ground.

Short-term breadth has cracked, while longer-term Russell breadth is still holding above 50. $R2TW is around 50.94, $R2FI around 54.53 and $R2TH around 57.48. That tells me the market has taken a hard hit, but this is not yet a full internal liquidation.

The most important bullish clue is $SKFD at 0.01. That is a classic bounce signal. The problem is that bounce signals are tactical, not structural, and the first bounce after this kind of move can be mechanical rather than genuine demand.

Momentum leadership has flipped hard. $QQQ was the weakest major index pocket, semis are the pressure point, and equal weight is suddenly outperforming. $RSP only fell 1.42% versus $SPY down 2.58% and $QQQ down 4.80%. That is classic rotation out of crowded growth and into broader/value/defensive exposure.

4. Volatility

Vol is the centre of the session.

$VIX spiked from 15.87 to 21.57 on Friday, then retraced toward 19 pre-market. $VVIX is around 102, $VIX1D is around 28.70, and the $VX2/$VX1 ratio is near 1.09. That is stress, but not full crash-mode stress. The low-vol regime is cracked, not completely dead.

Put/call has also finally moved. $PCC is around 0.967 and $PCCE around 0.841. That is a fear reset from complacent levels, but not a clean capitulation signal. In other words, fear has entered the building, but I would not call it a durable low signal yet.

Semis ETS skew and IV rank were above 90 before Friday, then they dropped 9%, closing near peak negative gamma. Friday was clearly mechanical and positioning-driven, but the problem is that mechanical flows can still create real technical damage.

5. Credit and liquidity

Credit is not confirming a panic.

$HYG/TLT is around 0.9338, off the highs but still elevated. $LQD/$HYG is around 1.36, which shows some defensive credit rotation, but not a disorderly credit break. $HYG itself is around 79.43 and $KRE around 70.17, so regional banks are not sending a major stress signal.

SOFR-IORB is around -0.03, which says funding is calm. No repo stress. No liquidity seizure.

The curve is still a pressure point. The 2s10s is around -39 bps, matching the macro theme of higher long-end yields and sticky Fed risk.

That pressures long-duration growth and explains why $QQQ/$SMH got hit hardest, but the fact homebuilders and banks held up better suggests Friday was not purely a rates story. It was rates as the spark, gamma and positioning as the accelerant.

6. ETF and Sector rotation

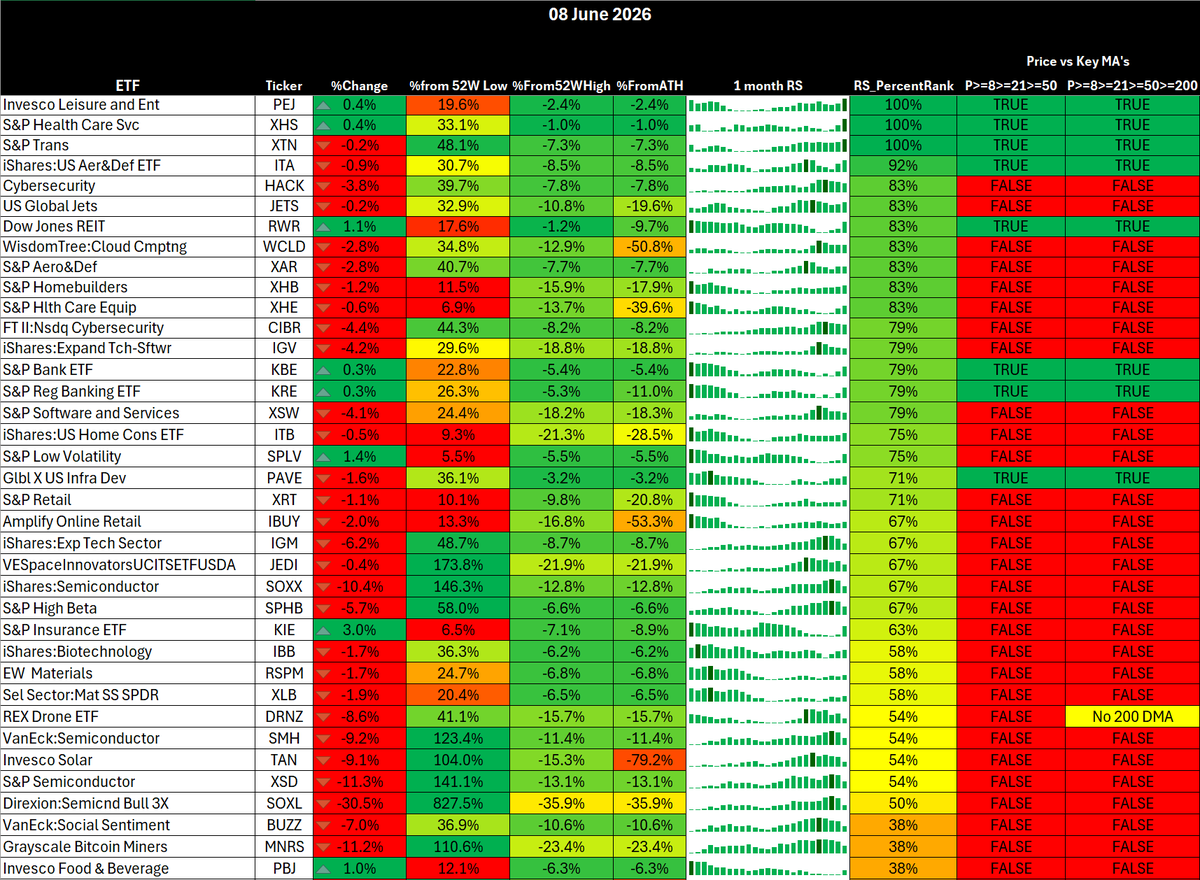

The ETF dashboard is the clearest part of my note today: this is no longer growth-led risk-on. It is defensive/value rotation with growth leadership broken short term.

The sector tape is brutal for AI beta. XLK fell 6.66%, SMH fell 9.22%, SOXX fell 10.44%, XSD fell 11.27%, SOXL fell 30.51%, TAN fell 9.07%, PBW fell 10.80% and ARKK fell 6.97%.

All of these are below the key MA stack. That is not a dip-buy signal by itself. It is a “wait for repair” signal.

Defensives did exactly what they should in a risk-off rotation. XLP rose 1.71%, XLV rose 0.61%, XLU rose 0.93%, XLRE rose 0.68% and SPLV rose 1.45%. Health care is the cleanest defensive leader because XLV and RSPH both have full MA confirmation.

Financials are also quietly important. XLF rose 0.21%, KRE rose 0.27%, KBE rose 0.28% and KIE rose 2.97%. That is not what you normally see if the market is pricing a broad credit accident. It supports the view that Friday was an AI/crowding/gamma unwind rather than a systemic stress event.

Key watch list:

$SMH: the market cannot fully stabilise if $SMH keeps bleeding below 570. A reclaim and hold above 570 helps the bounce. Failure there keeps the downside accelerator live.

$XLK: down 6.66% and below the MA stack. Needs time. A one-day bounce is not enough.

$XLV: defensive leader, green on Friday, MA stack intact. This is where institutional money hid.

$XLF/$KRE: constructive relative action. If these keep holding, the tape is damaged but not broken.

$RSP: outperforming $SPY and $QQQ. Equal weight resilience is the main reason not to call this a full market top yet.

7. Summary

Tactical bounce setup, not full risk-on.

Friday was a positioning shock. The AI trade unwound, $SMH became the pressure point, vol repriced, put demand spiked and gamma flipped negative. That creates two-way violence. It does not automatically mean crash, but it does mean the easy grind regime is gone for now.

Game plan:

Best expressions are tactical, not heroic: $SPY/$QQQ scalps, $SMH only if it stabilises, and keep size smaller because negative gamma can reverse fast.

If $SPX loses 7,350 and cannot reclaim quickly, the bounce thesis is wrong intraday. Then 7,300 comes into play, followed by 7,250 and 7,200. Shorts are better on failed bounces, not into the hole.

If $VIX spikes above 22 while $SPX is into 7,250/7,300 support, I would start looking for the vol-fade/bounce setup, but only after price confirms. Blind dip buying in negative gamma is how accounts get chopped up.

Best clean read for today: let the first 30 to 60 minutes show whether institutions rebuild the structure. If $SPX reclaims 7,400 and $SMH stops falling, tactical long bias. If $SPX rejects 7,400 and $VIX firms, sell the bounce.

2

33

cprEngines retweeted

Jun 1

23

4

12

33,752

cprEngines retweeted

5,869

15,439

64,639

31,958,754

cprEngines retweeted

Energy Constraint, Fertilizer Shock, and the Repricing of Food Systems: How disruption at Hormuz propagates through agriculture, supply chains, and global stability

Read more here: open.substack.com/pub/blonde…

1

4

18

1,386

Apr 29

Come for the bangers, stay for the financial education.

1

5

2,992

cprEngines retweeted

Apr 28

10

6

18

3,213

cprEngines retweeted

Apr 22

$CAR

800 = control level

820–830 = breakout continuation trigger

770 = danger zone

750 = acceleration down if lost

2

2

15

5,172

cprEngines retweeted

Apr 22

9

5

10

19,133

cprEngines retweeted

Apr 22

$BYND SOMEONES ABOUT TO GET FUKULATED

Apr 22

Absolutely no volume. Its dead

14

7

107

58,378

cprEngines retweeted

Apr 20

Apr 9

THREAD 🧵 0DTE FRIDAY (Pre-OPEX) Why tomorrow isn’t random… it’s a liquidity trap.

Most traders think 0DTE is chaos. It’s not.

It’s the most controlled environment in the market.

Tomorrow (pre-OPEX Friday) is where:

-dealers lose cushion

-hedging accelerates

-moves get violent fast

Here’s how to actually trade it @grok 👇

7

6

86

9,879

cprEngines retweeted

Apr 19

1

5

292

cprEngines retweeted

Apr 20

That’s the race. Not best component… best rack-as-a-system. Right now it’s fragmented:

$ETN brings power

$VRT stabilizes cools

$NVTS $MPWR convert it

$CRDO moves the data

$SMCI assembles it

Hyperscalers don’t want pieces. They want a rack that delivers more compute per watt, predictable performance, lower cost per inference. The first company that can bundle that end-to-end…owns the cost curve

4

10

32

18,010

cprEngines retweeted

Apr 20

The winners won’t dominate one layer. They’ll control the entire system of turning power into usable compute.

That means managing every step, from the moment energy is generated to the point it becomes efficient processing inside the data center. Right now, no single company owns that full process. But you can already see the pieces coming together:

$ETN handles the movement of electricity across the grid and into facilities.

$VRT focuses on cooling and power systems, making sure the hardware can actually run without overheating.

$NVTS & $MPWR sit at the critical conversion layer, turning raw power into usable, efficient energy for compute.

$SMCI brings it all together at the rack level, where density and deployment actually happen.

1

3

10

1,873