I work in CRE Capital Markets, but I’m fully ported into Bitcoin, BTC Miners, and AI/HPC Infrastructure.

Joined April 2024

- Tweets 322

- Following 1,311

- Followers 302

- Likes 7,230

7 Photos and videos

Harry Hodl retweeted

May 9

NUAI: An Asymmetric Pre-Deal Position in AI Infrastructure

Summary

Investors comfortable holding $IREN, $WULF, $CIFR, or $APLD before they announced their first hyperscaler deals should be comfortable holding $NUAI today. The structural setup is materially identical with less execution risk. NUAI is operating the validated playbook those names established in 2025, with Stream Data Centers (Apollo-backed at $40B) and Macquarie already on the cap table, four hyperscalers as the only credible counterparties, and a six-month Macquarie clock functioning as a forcing function for lease execution.

Position Overview

Eighteen months ago, AI infrastructure names like IREN, WULF, APLD, and CIFR traded as speculative microcaps. Each re-rated sharply once a hyperscaler signed. Multiples expanded, floats compressed relative to opportunity, and the market repriced the companies from "miner" to "AI infrastructure platform."

NUAI follows the same template. New Era Energy & Digital has 650 MW secured in Ector County, Texas — the flagship "TCDC" campus — and management has confirmed advanced commercial discussions with one of four hyperscalers: Alphabet, Amazon, Meta, or Microsoft. The joint venture was organized by the hyperscaler, who selected Stream Data Centers as development manager and an institutional capital partner (Northland believes Apollo) to provide equity and arrange approximately 80% project-level debt. Stream contributes hyperscaler relationships and operational execution. NUAI contributes site control. The structure was effectively delivered to the company.

Why the IREN/WULF/APLD Comparison Holds

The standard objection to any "early-stage X" pitch is that every microcap claims to be the next something. Four points distinguish NUAI from generic versions of that pitch:

1. Secured land. 650 MW in Ector County is owned outright, not optioned or under LOI. The recent equity raise eliminated the SharonAI overhang and consolidated full ownership of the TCDC site. Power-ready acreage is the binding constraint of the entire AI buildout and the single hardest piece to fabricate.

2. Institutional capital. Macquarie wrote a $290M project-level facility. Apollo acquired Stream Data Centers for $40B in November 2025 and is the implicit equity partner on TCDC. Both are among the most rigorous diligence shops in private capital, and both are staked.

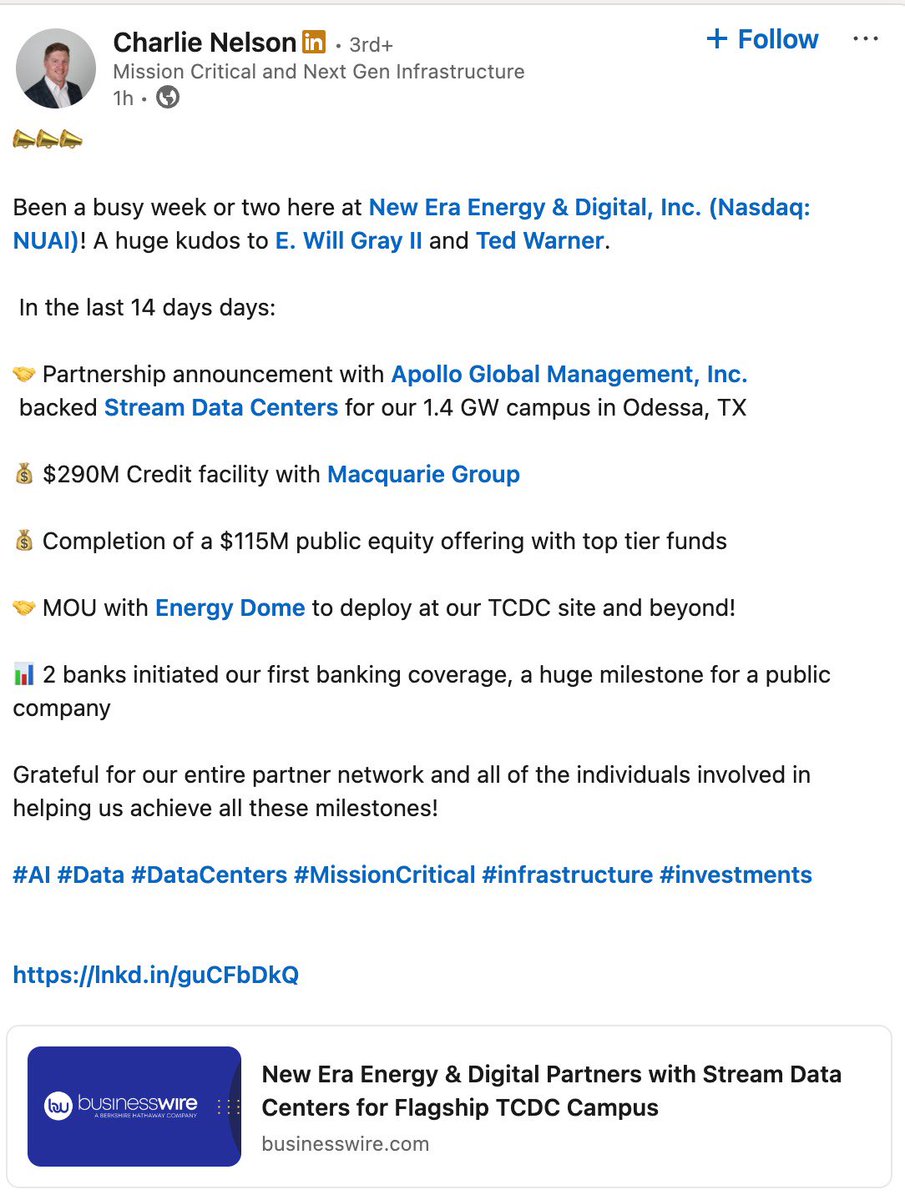

3. Professional execution stack. Stream as developer/operator; RK Mission Critical for modular fabrication and supply chain; Thunderhead Energy for behind-the-meter power; Ramboll / EYP Mission Critical Facilities for engineering. Charles Nelson joined as President/COO in February 2026. Ted Warner — with nearly two decades of capital markets experience and over $7B in HPC-related financing — joined as CFO in March 2026.

4. Binary counterparty universe. Four hyperscalers, all investment grade, all capex-constrained on power, all publicly committed to multi-year buildouts. Whichever one signs represents top-tier credit on a 15-20 year colocation lease.

Behind-the-Meter Has Become the Industry Default

A year ago, the consensus view across the data center industry held that behind-the-meter (BTM) power solutions were unworkable at hyperscaler scale. Critics argued that hyperscalers required utility-grade reliability, regulatory complexity would prove insurmountable, and BTM would remain a niche workaround rather than a primary power strategy. That view was a real overhang on every developer pursuing BTM as a path to capacity.

The consensus has reversed in twelve months. CIFR, APLD, WULF, and CORZ are all now executing BTM-led power strategies, and hyperscalers — facing multi-year interconnection queues and structural grid constraints — have endorsed BTM as a viable route to GW-scale capacity. Thunderhead Energy's role on the NUAI execution stack should be read in this context. NUAI is executing a strategy the industry has at this point publicly validated, with a power partner whose model is de-risked by parallel deployments at peer companies.

This is a meaningful update to the underwriting. The power-delivery question that was an open risk on every pre-deal AI infrastructure name twelve months ago is now the operating assumption across the cohort.

Stream Data Centers as the Execution Catalyst

In November 2025, Apollo paid $40B for Stream — for a particular set of capabilities that map directly onto why a hyperscaler would select TCDC.

Build-to-performance spec, not build-to-suit. Stream pre-aggregates standardized MEP equipment and configures it on the fly to customer specifications. The company quadrupled its development team during COVID and has been procuring long-lead equipment up to a year ahead of demand. Standardization speeds development time materially in a market characterized by acute power constraints and capacity scarcity.

Configurable cooling that future-proofs the asset. Stream's proprietary cooling design supports air cooling and direct-liquid-cooling on the same footprint, scaling from 10-12 kW per rack to 400 kW per rack. Customers can defer the air-vs-DLC decision until late in the build without extending the timeline, providing meaningful optionality across NVIDIA's roadmap from Blackwell to Rubin and beyond.

Pre-existing hyperscaler relationship. This element has been broadly overlooked. Because Stream has worked with this hyperscaler before, we can safely assume that a significant amount of work product can be leveraged for TCDC. Management's fall 2026 lease execution target is credible because contracts are likely being adapted, not drafted from scratch.

The distinction is between a startup negotiating with a hyperscaler from a blank page and the hyperscaler's preferred developer adapting an existing form to a new site. Execution risk lives in a different category.

Expected Value Framework

In my opinion, the probability of a deal with the current hyperscaler by August 2026 is 90% . The hyperscaler organized the JV. They selected Stream. They directed the structuring. Engineering and permitting are progressing without observable friction. Negotiations leverage Stream's existing templates and shared counsel. The Macquarie facility requires lease execution within six months, aligning every party's incentives toward closing.

As for the probability of any deal eventually, I would say 99% . If the current hyperscaler exits — for which there is no observable reason in a market structurally short on power-ready supply — the structural work is already complete. Site control, partner ecosystem, financing template, and engineering package are not counterparty-specific. Another publicly traded data center company recently demonstrated this dynamic: a hyperscaler counterparty exited, a replacement was secured, and the timeline extended by approximately one month.

Stress-tested at a deeply conservative 50% probability of a deal — well below what the structural setup supports:

50% × 4-5x upside ≈ 2.0-2.5x expected return

50% × 50% drawdown ≈ 0.25x expected loss

Net expected value: approximately 1.75-2.25x

At 90% probability, expected value approaches 3.5-4x. The asymmetry is wide enough that halving the upside and doubling the downside still produces a positive expected value.

Re-Rating Mechanics: Why a Deal Drives 200% From Here, Not 10%

A market-microstructure point underlies the upside case.

When mature AI infrastructure names — IREN, WULF, CIFR, APLD at current scale — announce hyperscaler deals, the stock typically moves around 10%. Optionality is already embedded, and announcements function as confirmation rather than revelation.

Smaller, less-followed names behave differently. DGXX has announced materially smaller deals than what NUAI is contemplating and moved 50% . Expectations are not embedded, the float is small, and the announcement forces a re-rating from speculative microcap to credible AI infrastructure platform (Note that a deal cannot be priced in because many institutions are waiting to buy until after a deal is announced).

NUAI sits closer to the $DGXX end on market cap and visibility but closer to the IREN/WULF/APLD end on asset quality and counterparty caliber. That mismatch is the opportunity. A first hyperscaler deal at TCDC could plausibly drive an immediate 200% re-rating — not because steady-state fundamentals support that exact multiple, but because microcaps gap rather than incrementally re-price. Investors do not get to scale into the new range.

Downside is bounded by the existing balance sheet, which is clean post-Macquarie and post-equity raise with no SharonAI overhang. Upside is a non-linear re-rating event.

The Case for Data Center Exposure

A reasonable question, given the breadth of the AI investable universe — semis, photonics, custom silicon, robotics, model labs — is why allocate to data center developers at all.

Data center economics are durable in a way most AI-adjacent verticals are not. Hyperscaler colocation leases run 15-20 years. Counterparties are investment grade. Cash flows are recurring. Once a campus is leased, it produces something close to a bond. EQIX has compounded through every macro cycle of the past fifteen years on this dynamic, and the structural reason is simple: an AWS region does not get turned off because the economy slows. Compute demand is structurally inelastic at the margin, and existing infrastructure is locked into multi-decade obligations.

The asset class is also tractable for non-specialists. Underwriting reduces to power, land, customers, and contract terms. Many other AI-adjacent verticals — photonics, custom silicon, neuromorphic, edge inference — are genuinely interesting and likely lucrative, but the underlying technology evolves quickly enough that most investors cannot reliably assess winners. Data centers fit Buffett's "in pile" — comprehensible, durable, and underwritable on standard metrics.

The constraint is that asymmetric opportunities within the data center space are increasingly scarce. For WULF to 5x from current levels would require multiple gigawatts of new capacity, additional contracts, and substantial revenue growth — achievable but grinding. NUAI requires one announcement with one of four hyperscalers for Phase 1 of TCDC. The bull case condenses to a single press release.

For investors who participated in the 2025 IREN/WULF/HUT/APLD/CIFR cycle, NUAI offers the same trade structure with two improvements: the underlying thesis has been validated by the prior cohort's outcomes, and the macro evidence — exponential capex guides, tightening power constraints, structural undersupply — is materially stronger today than it was eighteen months ago.

Conclusion

NUAI is structurally identical to the IREN, WULF, and APLD trades in early-to-mid 2025, with three improvements. The thesis has been validated by the 2025 cohort's outcomes. The execution stack — Stream / Apollo / Macquarie / Ramboll on day one — is more institutional than what several of those names had at first announcement. And the forcing functions are tighter, with a six-month Macquarie clock combined with a hyperscaler-organized JV on 650 MW of secured Texas power.

The position reduces to a single proposition: one press release reprices the equity by triple digits. Downside is bounded by an institutional cap table and a clean post-raise balance sheet. The expected value math holds at 50% probability and compounds at the 90% probability the structural setup supports.

Simply put, this is a remix of the IREN/WULF/APLD trade.

28

35

284

42,805

Harry Hodl retweeted

Mar 13

$IREN Sweetwater 1 HD - 3/12/2026

Made possible by OnlyFrans, edited and upscaled by @HArctander

Lots of developments on both tracts:

1. Confirmed 2nd primary substation on the left tract, making the total confirmed 3.

2. Data Center rows are visible on the right of PS1.

3. Visible bulk substation transformer on the most right pad, possibly a transformer on one of the pads at PS1.

4. Mass grading on the left tract, indicating further development of the site towards adjecent parcels on the north and west.

5. Utility substation expansion now connected to the main switch, suspected POI for IREN's energization in Q2.

6. Suspected further build-out of primary substations on the left tract, south of the first two, confirmed by drone footage posted by a subcontractor.

My considerations:

-> IREN is making a site that is a blank slate for mass production of data center shells.

-> The area right of PS1 is showing indications of rows, underground conduits, and this area will soon be ready for data center construction.

-> The fact that there is 1 bulk substation transformer visible on the most right transformer pad, makes me certain that energization is not far out.

-> I expect 750MW of gross power at the 36.5kV level (DC ready), to be flowing by the end of the year (incremental over the course of the year).

-> Based on the concentration of the substations on the left tract (possibly 3 or 4), we could see the entire 1,400MW become operational on these 2 tracts.

-> This further strengthens the believe that this will be a VR200/VR300 site, with a much smaller data center footprint due to a massive jump in rack density.

Now as to "wen deal":

I think @IREN_Ltd is making a site that can still pivot in either direction of Build-to-suit, colocation, or AI Cloud/IaaS.

By doing all the step-down work first, but preparing multiple data center areas down to the 34.5kV level — the ultimate use-case doesn't need to be set in stone yet.

I think this site will have a slow ramp up, but when the use-case is determined, all the moving parts will be in place, and the construction will be "released" as a coil spring into mass data center development, on multiple areas across the site in parallel.

Time to data center = Time to revenue

There are no delays when you do all the pre-work for 1,400MW of data centers, making the eventual construction a simplified copy-paste task at an unprecedented scale and pace.

Sweetwater is the flagship and will be the holy grail of AI infrastructure in 2027/2028.

Patience is a virtue, take the time to learn and know what you own.

33

65

467

66,784

Harry Hodl retweeted

i ain’t reading all that

im happy for u tho

or sorry that happened

12,023

27,112

248,807

7,587,345

Harry Hodl retweeted

Feb 2

What sensible forward thinking cutting edge leading nation is having a DEBATE on whether or not there should be VOTER ID?!?!!!! Like?!?!? They’re actually fighting NOT to have ppl present ID while voting for your leaders!!!!! Do you get it?!?!!!! Do you get it now?!?!!!

8,468

45,873

313,057

57,478,147

Harry Hodl retweeted

Jan 3

I can’t believe we black bagged a narco dictator without considering all available options first, like paying an NGO $100b to put on queer musical theater productions in Caracas

1,440

10,541

111,406

2,134,168

Harry Hodl retweeted

6 Nov 2025

The thing you have to remember about this woman and those like her is that she genuinely doesn’t know that anyone disagrees with her basic worldview. She doesn’t even see it as a worldview. It’s just the obvious truth.

Of course she knows abstractly that half the country voted for Trump. But those aren’t people. Those are cartoon characters. They’re either fat slobbering rednecks in klan hoods, or mustache-twirling robber barons manipulating the rednecks for profit. Her mental models of them are less complex than her mental model of a squirrel. Anyone she might actually sit down and talk to is, of course, a person, and therefore agrees with The Obvious Truth. It is inconceivable to her that anyone capable of being a pleasant dinner party guest would not share her basic beliefs and values.

She wasn’t trying to do a gotcha or extract a pledge of fealty. She was certain that Sydney Sweeney is a person, and therefore only got mixed up in the whole jeans/genes fiasco by mistake. She was trying to do Sydney a favor by giving her a chance to clarify that she is in fact a human being who agrees with the things all real people agree with.

1,861

4,518

58,532

3,787,275

Harry Hodl retweeted

31 Oct 2025

17 years after the white paper, the Bitcoin network is still operational and more resilient than ever. Bitcoin never shuts down.

@SenateDems could learn something from that.

2,217

6,347

40,786

6,156,951

Harry Hodl retweeted

29 Oct 2025

.@SenWarren and @SenAmyKlobuchar: you are failures.

You failed to derail the electoral success of one of our great allies in Latin America, President @JMilei. He won in a landslide with the poorest members of society voting for economic freedom—a notion anathema in particular to the Senate’s resident American Peronist, Senator Warren.

You failed to reopen the government, preventing our Administration’s efforts to get aid to American farmers, as well as our planned activation of the Farm Credit Agency to assist our farmers with next year’s crops.

As the attached photo demonstrates, @POTUS is in Asia showing what successful American leadership looks like. Today’s announcement after his meeting with President Xi will be a resounding victory for our great farmers.

While I know it will be soul-crushing for you, please re-focus your staff away from writing incoherent letters to myself and others, and instead work towards opening the government.

If you decide to further add to your legacy of failure by voting to keep the government closed over the upcoming Thanksgiving holiday, ruining the number one travel day for American families, you should both be ashamed.

P.S. I am happy to inform you both that the Argentine economic bridge has now turned a profit for the American people. While “profit” is a private sector word that you may both be unfamiliar with, I would urge you to look past your previous experience working alongside the Biden Administration’s autopenned efforts to bankrupt the US government.

5,578

19,055

86,995

6,182,241

Harry Hodl retweeted

8 Oct 2025

What are you really playing for here - 30% return?

@BitMNR should just lay off the ATM, blast ETH higher with their cash, squeeze them, and rip the ATM again into the shorts covering higher.

8 Oct 2025

We're short $BMNR. Report at kerr.co/bmnr. The DAT playbook has become basic & unoriginal: as near-identical copycats overwhelm the market, premiums are collapsing and the ability to issue shares well above NAV to boost ETH-per-share is disappearing. RIP DATs🪦🥲 1/8

30

13

288

42,971

Harry Hodl retweeted

19 Sep 2025

Tim Walz says that Jimmy Kimmel’s firing is “North Korea style-stuff.”

Here’s Tim Walz deploying the National Guard to prevent families from leaving their homes during the COVID lockdowns.

Hey, Tim this is “North Korea style-stuff.”

3,752

40,563

220,537

5,590,734

Harry Hodl retweeted

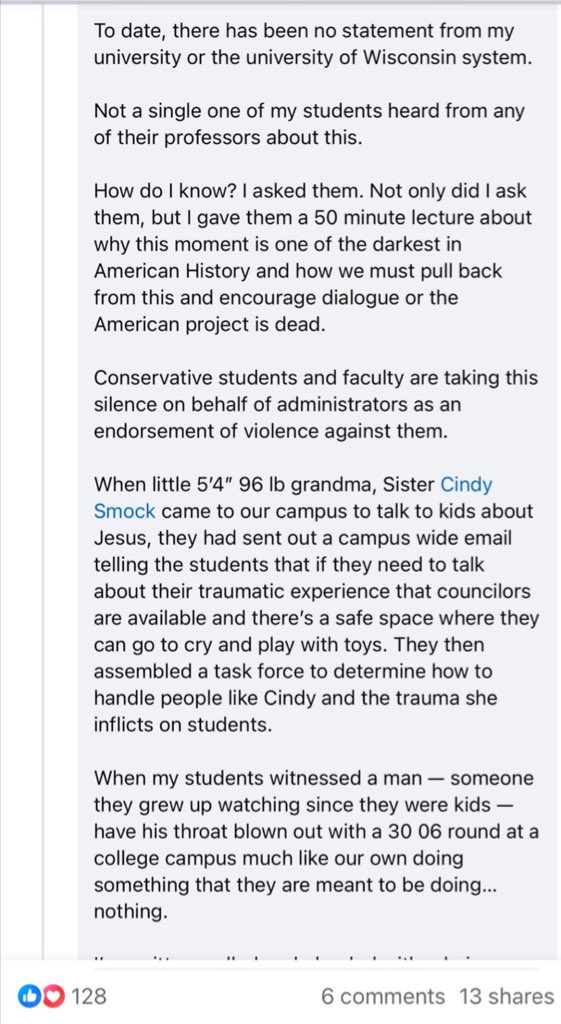

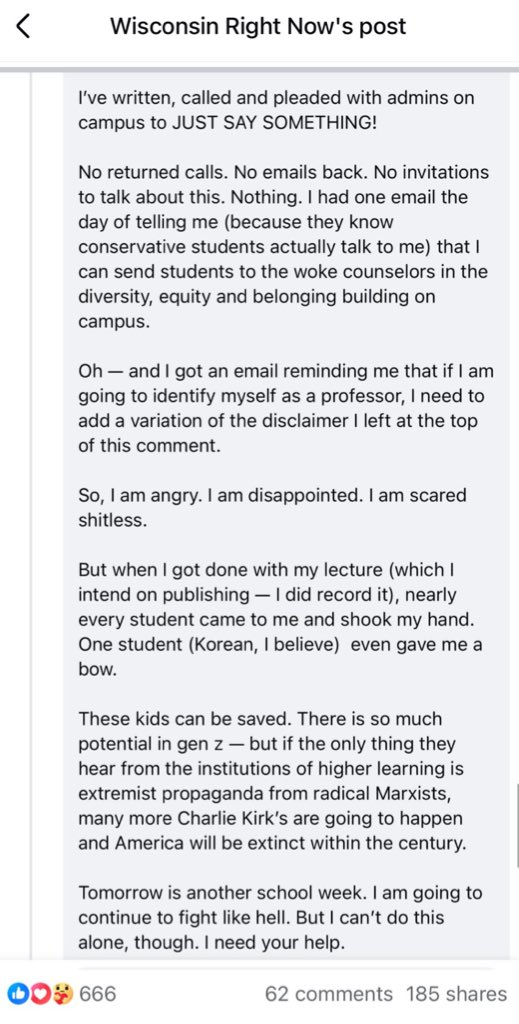

16 Sep 2025

The silence from most universities after Charlie Kirk was murdered at a college event speaks loudly and finally a professor has the courage to call it out. Meet professor Trevor Michael Tomesh from the University of Wisconsin system. He said everything that needed to be said. 🔥

615

7,654

26,296

856,019

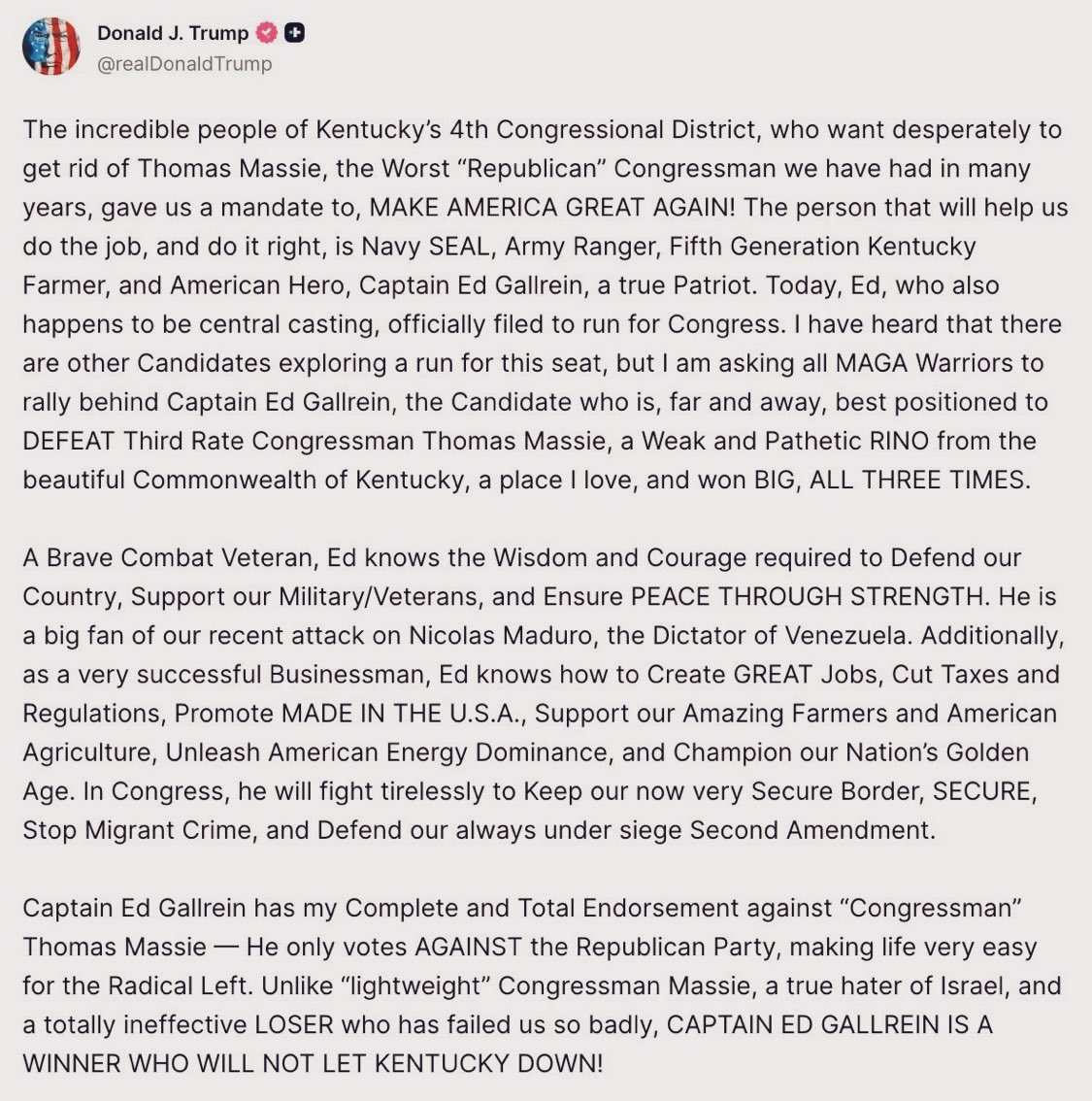

12 Sep 2025

I have post notifications turned on for 4 people: @mikealfred @DonnyDicey @sunxliao and @wliang. Paying attention to them has proved more lucrative than my actual day job. If you hate money, I suggest you keep your distance from these guys.

13

11

72

25,207

Harry Hodl retweeted

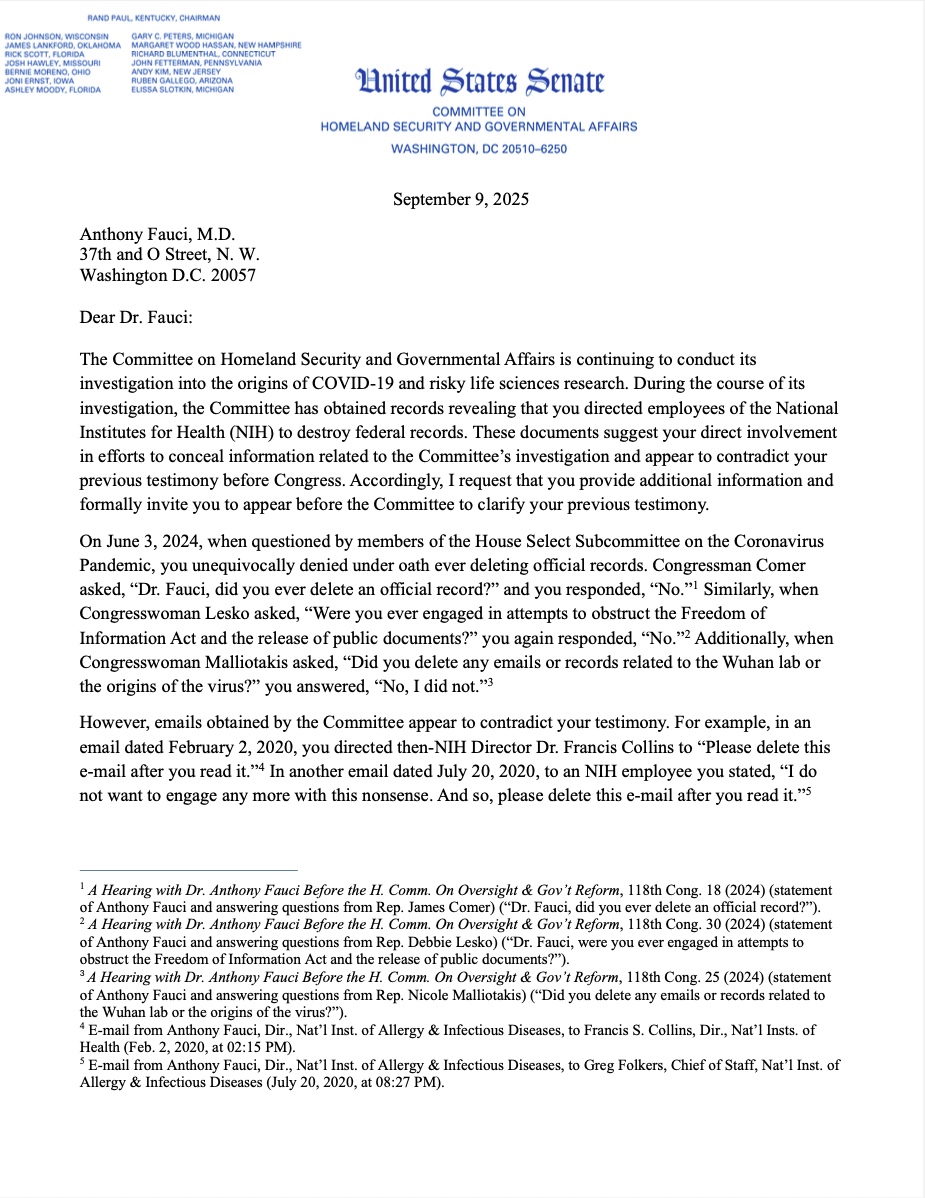

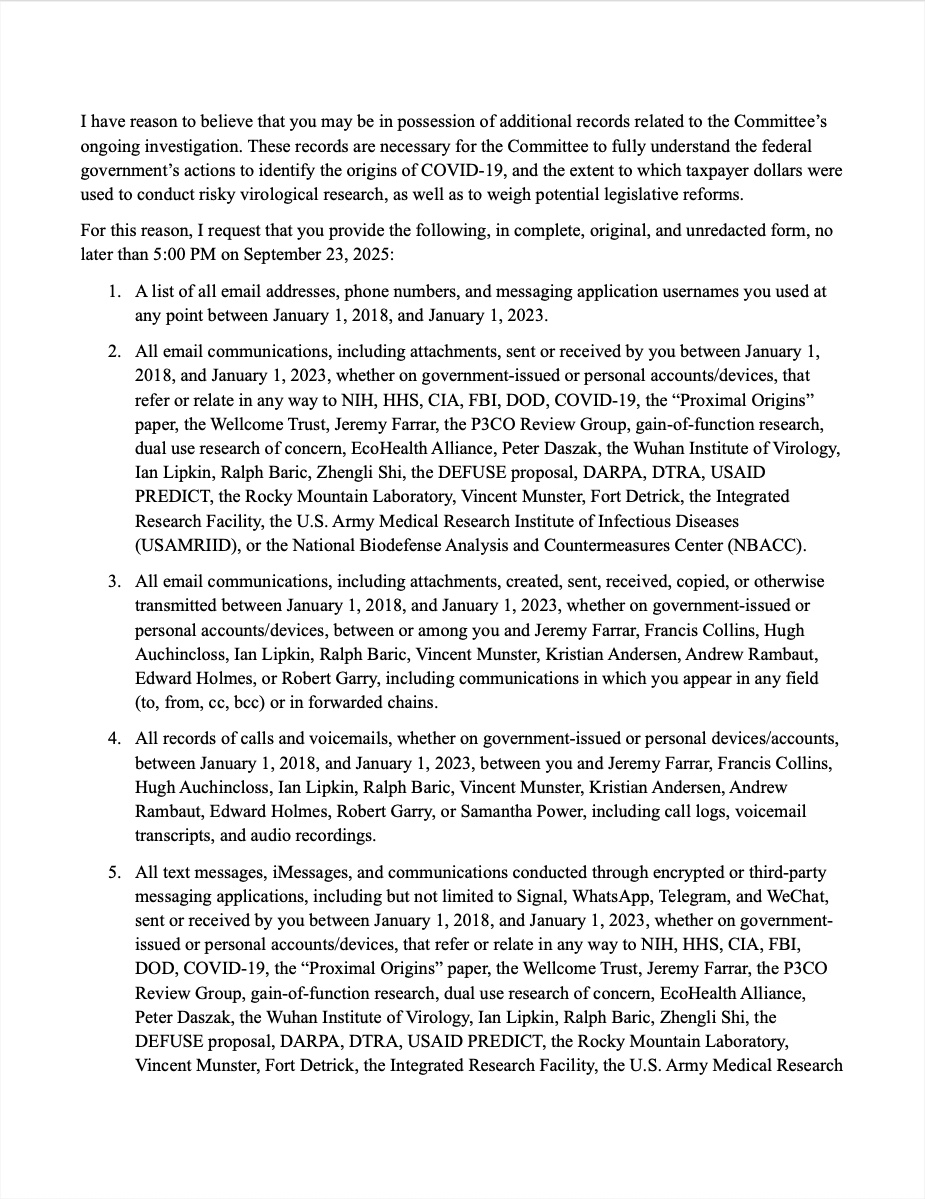

10 Sep 2025

🚨BREAKING: Newly released emails show Fauci directed colleagues to “delete this after you read it”—dating back to Feb. 2020.

He denied it under oath. These documents are now public, and Fauci will finally testify before Chairman Rand Paul.

4,549

29,995

101,596

4,292,790

Harry Hodl retweeted

6 Sep 2025

My thoughts on rate cuts:

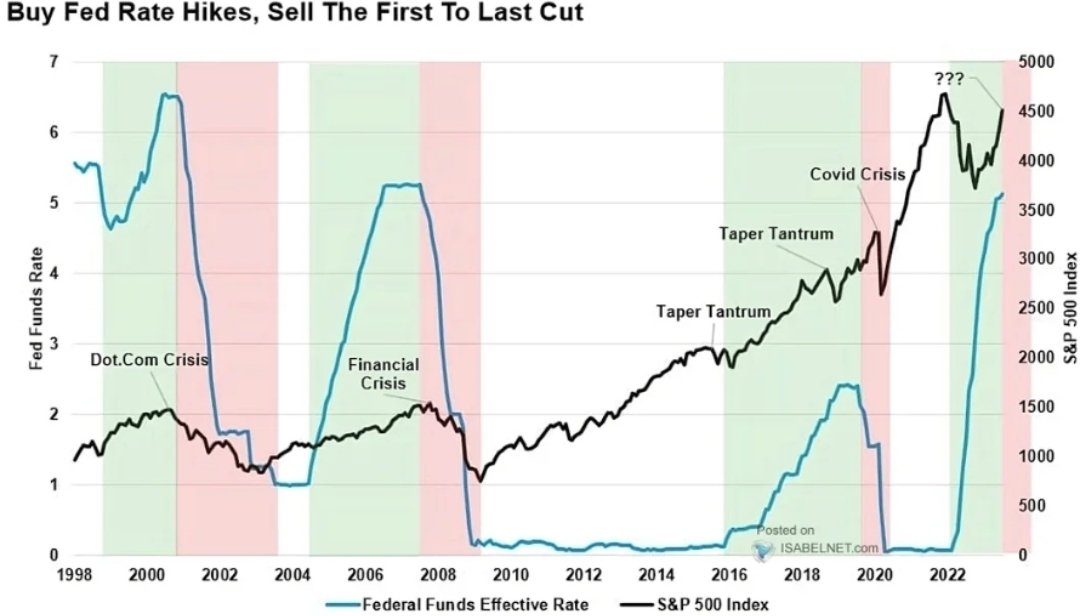

Some people fear that interest rate cuts will crash the market, and historically, there's a reason for that concern. As per the below chart, major rate cutting cycles have coincided with significant market downturns, such as the Dot-com Crisis, the Financial Crisis, and the COVID-19 Crisis. It's easy to look at this correlation and conclude that rate cuts cause the market to fall.

However, this perspective misses a critical point. The rate cuts weren't the cause. They were a reaction to the crisis. Central banks lower rates to stimulate a faltering economy, not to intentionally harm it.

While past rate cuts were a response to economic distress, the current environment presents a unique situation. We are at the beginning of a potentially unprecedented period of economic expansion, driven by massive investments in AI. Tech giants like Meta, Apple and Google are planning to spend hundreds of billions on AI over the next few years. This kind of capital expenditure on a transformative technology is set to create a new wave of growth. The demand for everything related to AI, from computing power to data centers to the energy to run them, is projected to increase dramatically.

If a rate cut happens now, it won't be in response to a market crash. Instead, it would act as a powerful factor for AI, making it cheaper for companies to borrow and invest. This environment of lower borrowing costs and significant capital expenditure helps specific sectors and businesses.

For investors, this change in the economy presents an opportunity. Instead of fearing a downturn, consider looking for companies that are positioned to benefit from increased spending and lower interest rates.

High-Capex Businesses: Companies with high capital expenditure needs, particularly those in the infrastructure and technology sectors, will see a direct benefit from cheaper debt. These companies can accelerate their growth plans, as their cost of capital decreases.

Infrastructure and Energy: The AI boom requires immense power and infrastructure. Companies involved in building data centers or those in the solar energy sector will be in high demand. These projects are often financed through debt, making them particularly sensitive to interest rate changes.

So, if you're concerned about the next market cycle, consider shifting your focus from fear to opportunity. Look for companies with strong fundamentals and limited downside that are poised to capitalize on the next wave of technological and economic growth, which a rate cut could help fuel rather than hinder.

44

80

497

100,865

Harry Hodl retweeted

2 Sep 2025

Mandy Cohen, former CDC Director, talking and laughing about how she made policy decisions during COVID.

Her approach?

She would ask friends, "Well, what are you planning to do?" And they would casually agree on some policy on the phone and then do that.

Completely unreal.

962

3,804

10,686

1,462,660

Harry Hodl retweeted

5 Sep 2025

Brilliant 😂

822

4,048

23,763

1,559,209

Harry Hodl retweeted

30 Aug 2025

Giving away my Titleist staff bag that I used from the Open Champ to the BMW I believe.

Must be a follower

Comment, like, retweet for a chance to win!

8,998

9,203

22,549

1,615,565

Harry Hodl retweeted

17 Aug 2025

We have a very interesting week ahead for BTC and crypto.

I told you I would watch LTF if I see anything sus to prepare you in advance and confluence has stacked up — this is why you need to have post notifications turned on.

Both scenarios lead to the inevitable price destination of $138K - $182K.

Immediately bullish scenario towards $130K :

> Hold above $116.8K to complete the local re-accumulation

> Convincing break above the $120.7K - $121.2K order block

This would look very simple, just straight up pumping.

Local bottom around 23rd August scenario (drawing not perfectly to scale just swing spots:

> Fail to pump through the $120.7K - $121.2K order block

> Take the lows around $110K - $112K — massive buys get filled.

> Bottom and reverse sharply towards $130K with potential bullish sentiment flip around that date

Confluence for the pullback:

> COIN is telegraphing an aggressive ETH pullback — that can only be achieved with BTC heading to $110K - $112K

> Liquidation levels are thick from $116K to $111K BTC

> BTC | GOLD overlay is telegraphing a sharp pullback before a much higher high

Remember, price can really pump (across the board) to 120K first before this drop. Bears will get very loud on the drop, you should see this coming in case we go there — fade them.

What am I doing? Nothing, lol. Waiting for that deep price discovery range formation on BTC, so that we can have alt season dynamics unfold.

Missing that is much worse than anything I could imagine.

September through to Q1 should be epic. Don't fumble.

39

57

320

78,804