Advocates & Tax Consultants | Income Tax & GST — advisory, compliance, and litigation | CIT(A) · ITAT | New Delhi

Joined May 2026

- Tweets 179

- Following 111

- Followers 19

- Likes 33

5 Photos and videos

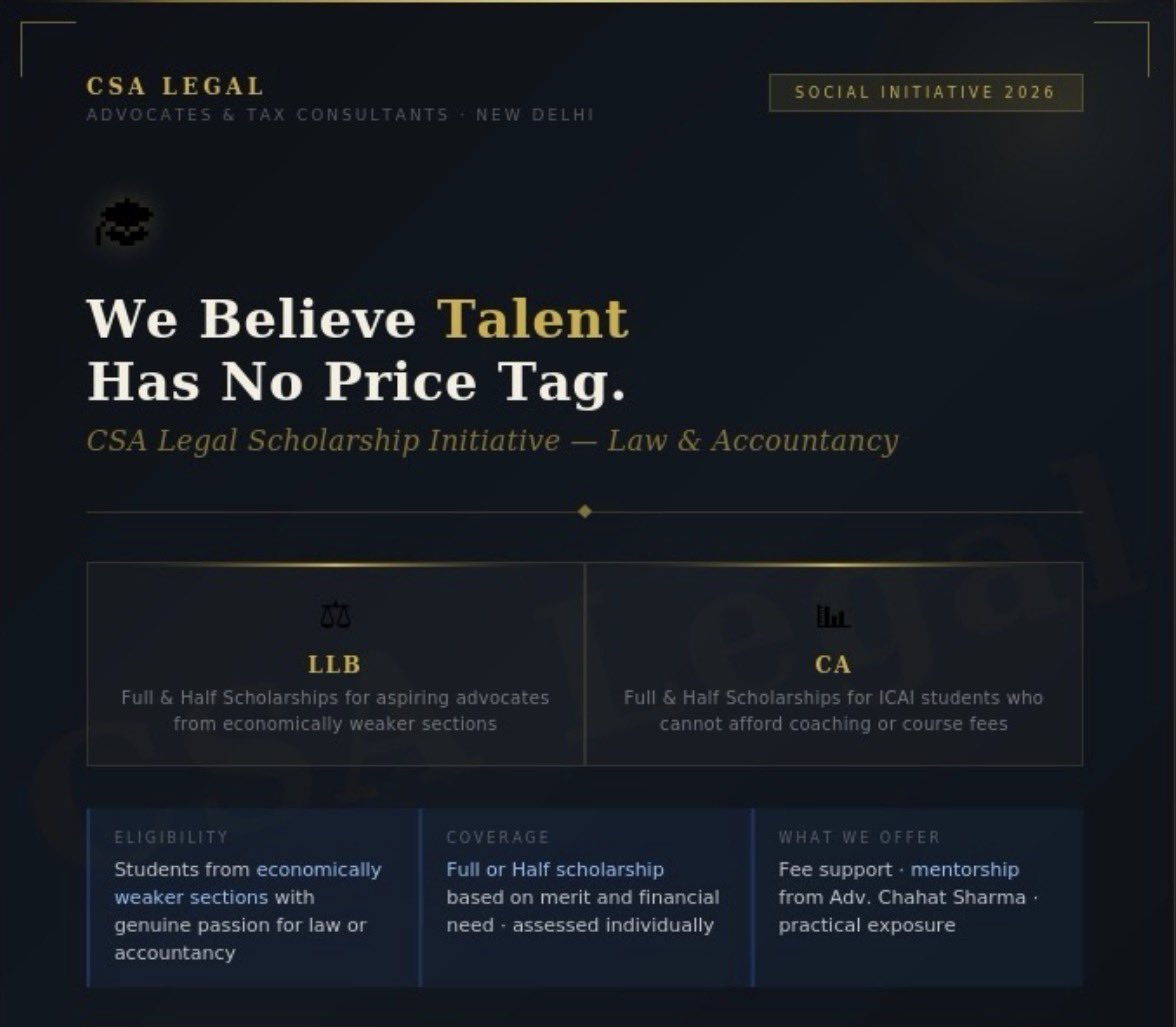

At CSA Legal, we believe talent has no price tag.

We are launching our Scholarship Initiative for students from economically weaker sections who dream of becoming a lawyer or a Chartered Accountant — but cannot afford the journey.

We will offer full and half scholarships covering:

⚖️ LLB — for aspiring advocates

📊 CA (ICAI) — for aspiring Chartered Accountants

What we offer beyond fees:

— Direct mentorship.

— Real-world exposure to tax law practice.

— A platform to grow alongside a working law firm.

If you are a student who deserves this opportunity — or know someone who does — send your details to chahat@csalegal.in

Talent finds its way. We want to make sure it does.

@advchahat

#Scholarship #LLB #CA #CharteredAccountant #LawStudent #CSALegal #Delhi #SocialInitiative #EqualOpportunity

3

4

118

Daily backup of books now mandatory under IT Rules 2026. Effective 1 April 2026.

The intent is right. The ground reality is harder.

Problems practitioners are already facing:

▸ “India-based servers” — most SMEs use Google Drive, Dropbox, OneDrive. All foreign servers. Technically non-compliant from day one.

▸ Daily backup vs daily filing — a small trader running Tally on a laptop with no IT support cannot automate daily cloud backups without significant cost.

▸ Penalty of ₹25,000 for non-maintenance — disproportionate for a kirana store owner maintaining basic books on a ₹15,000 laptop.

▸ Auditor reporting burden — tax auditors must now certify server location and backup compliance in Form 26. One more checkbox. One more liability.

▸ No government cloud infrastructure provided — the law mandates India servers but offers no subsidised, compliant cloud solution for SMEs.

@IncomeTaxIndia @FinMinIndia — the compliance intent is valid.

But without:

▸ A government-approved low-cost India cloud solution for SMEs

▸ A grace period for businesses to migrate from foreign servers

▸ Proportionate penalties for small businesses

This becomes another compliance burden that hits honest small businesses hardest while large companies with IT teams comply effortlessly.

Good policy. Needs better implementation support.

— @CSALegal | Tax Lawyers

#IncomeTax #ITRules2026 #DailyBackup #TaxCompliance #SME #Section62 #Section63 #CSALegal

13

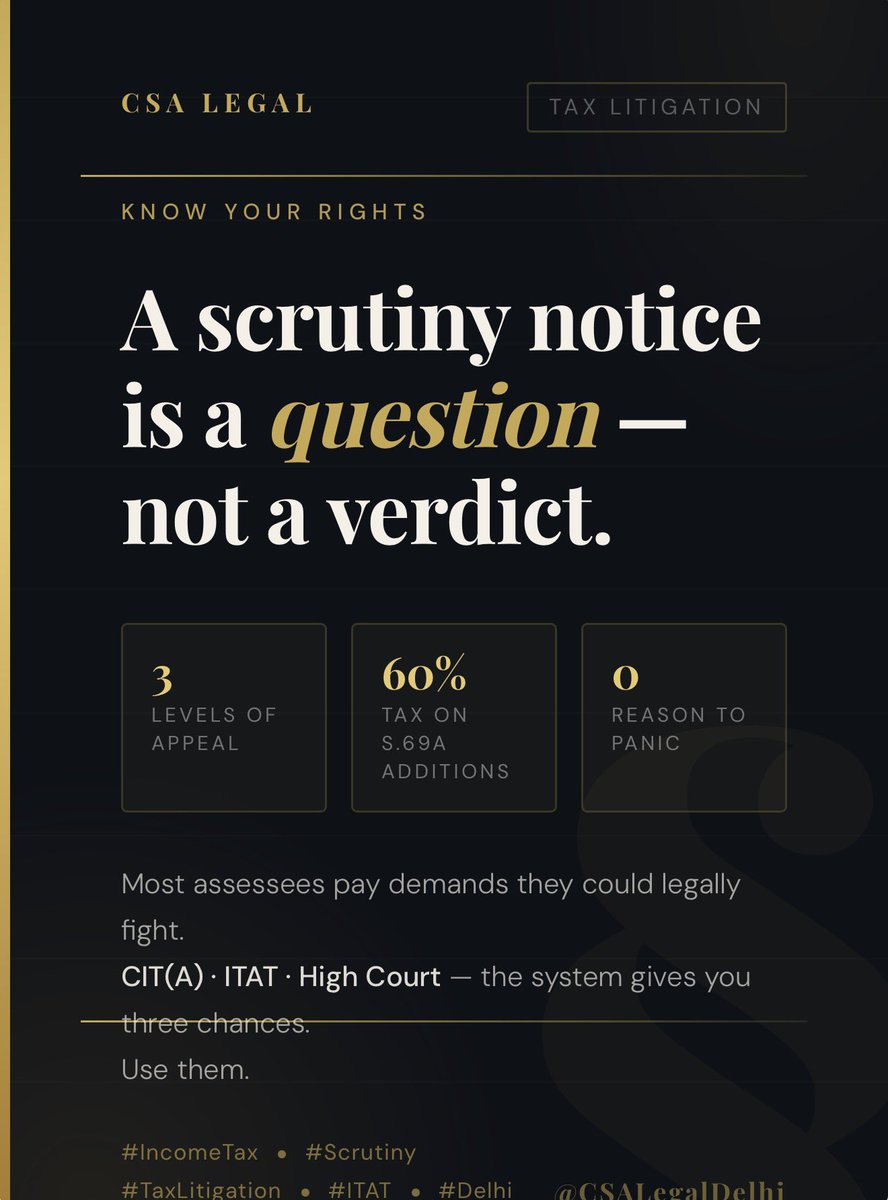

🔴 Case Law Decoded | ITAT Ahmedabad | June 2026 Dhaval Patel vs. ACIT [2026] 187 taxmann 292 (Ahmedabad Trib.)

A case every taxpayer and CA in India must read.

During a search — the AO found a WhatsApp message on the assessee's phone: "50 lacks given to Manan yesterday."

The AO's conclusion: ₹50 lakh unaccounted cash payment. Addition made. CIT(A) confirmed.

ITAT Ahmedabad: Addition of ₹50 lakh — DELETED entirely. The Tribunal's reasoning was surgical:

▸ The WhatsApp message said "given" — it did NOT say "cash given"

▸ The assessee provided ledger account, PAN, and address of the recipient

▸ The AO neither examined the recipient nor conducted any independent inquiry

▸ No cash withdrawals, no diary entries, no corroborative material was brought on record

▸ An isolated WhatsApp message without corroboration can create suspicion — but suspicion is NOT evidence of undisclosed income.

The addition was built on assumption. It fell on proof.

✅ The critical takeaway for every taxpayer: Your WhatsApp messages CAN be seized during a search. But a message alone — without cash withdrawal evidence, diary entries, or recipient confirmation — cannot sustain a Section 69 addition. Digital evidence must be corroborated with financial evidence. One without the other is suspicion.

Courts require proof. If you have received an addition based solely on WhatsApp messages or digital evidence from a search — the law is on your side.

— @CSALegal | Tax Lawyers

#IncomeTax #SearchAndSeizure #WhatsApp #Section69 #ITAT #CaseLaw #TaxLitigation #CSALegal

2

3

72

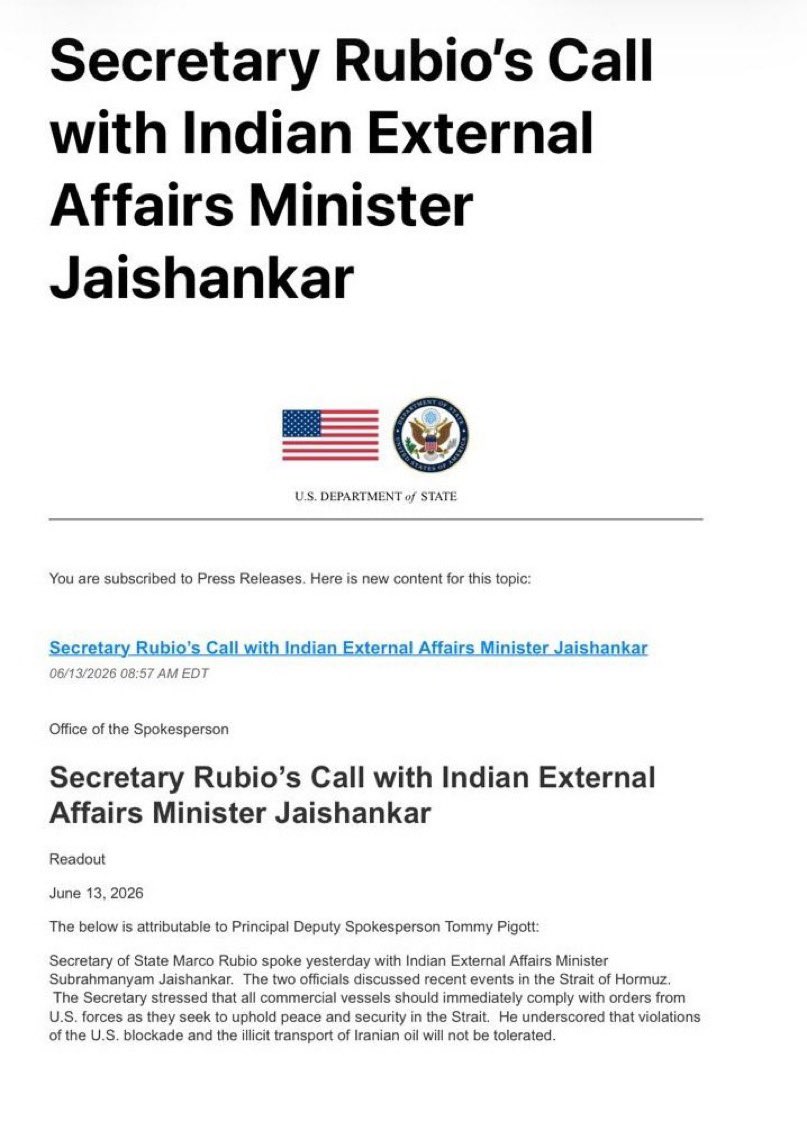

CSA Legal retweeted

Deeply shocking to read this official US statement, which contains absolutely no expression of regret or condolence for the loss of innocent Indian lives. How can a “friend” and strategic partner be so deeply insensitive?

Why couldn’t a non-compliant commercial vessel have been stopped using other, non-lethal means? Is it not possible to disable a ship's propulsion or steering without firing missiles targeted to kill civilian crew members?

Practically every merchant ship navigating these crucial waters has Indian crew on board. Are they all considered fair game for US missiles now?

This approach is unacceptable and I hope @DrSJaishankar had said so to @marcorubio.

1,998

10,690

37,903

1,425,045

🚨 Urgent Alert for all Private Limited Companies | AY 2025-26 @IncomeTaxIndia @FinMinIndia @nsitharamanoffcA wrongful automated trigger is firing under Section 143(1)(a) for virtually every Private Limited Company that filed its ITR with Deferred Tax.

The notice flags Schedule MAT and demands Form 29B — claiming MAT credit is unverified.

The trigger: Deferred Tax entries in the P&L account.

The problem: The CPC system is incorrectly treating Deferred Tax Debit/Credit in the P&L as MAT adjustments — and automatically demanding Form 29B certification by a CA.

This is wrong on two counts:

▸ Deferred Tax as per Ind AS / AS 22 is an accounting entry — it is NOT a MAT add-back or deduction under Section 115JB

▸ Form 29B is required only where actual MAT adjustments under the Companies Act are claimed — not for routine deferred tax accounting entries.

The trigger is so aggressive that ITRs filed on June 12, 2026 received this intimation the same day — within hours of filing.This is not a scrutiny. This is a system error causing mass panic across India's corporate taxpayer base.

Practical impact:▸ Hundreds of companies receiving identical notices simultaneously

▸ CAs being asked to file Form 29B for entries that legally do not require it

▸ Unnecessary compliance burden on companies that have filed correct returns

▸ Risk of wrongful adjustments if companies fail to respond within 30 days @IncomeTaxIndia @cbdt_india — this automated trigger needs to be reviewed and withdrawn immediately.

Issue a clarification: Deferred Tax entries in P&L do not attract Form 29B requirements under Section 115JB. Until then — every affected company must respond within 30 days clarifying that the deferred tax entry is an accounting adjustment and not a MAT-related claim.

Do NOT ignore this notice even if it is wrongful.@ITD_eFiling @askITR_official @Infosys_GSTN — please escalate to the CPC team for immediate correction.

— @CSALegal | Tax Lawyers

#IncomeTax #MAT #Section115JB #DeferredTax #Form29B #143a #ITRFiling #AY202526 #CPC #CSALegal

1

2

48

🔴 Case Law Decoded | ITAT Lucknow | June 2026

Vipin Yadav vs. ITO

[2026] 186 taxmann 972 (Lucknow Trib.)

A case every married investor needs to read.

Facts: A husband gifted ₹1.15 crore to his wife for derivative and equity trading. The trades resulted in substantial losses. The husband claimed the losses should be clubbed under Section 64(1)(iv) and set off against his income.

AO rejected it — said wife made independent trading decisions.

CIT(A) confirmed — said wife was an independent assessee.

ITAT Lucknow: Set-off ALLOWED.

The Tribunal held:

▸ Gift deeds and affidavits proved transfer without consideration

▸ Section 64(1)(iv) covers not just income but also LOSSES arising from gifted assets — directly or indirectly

▸ The AO and CIT(A) both erred — clubbing provisions apply symmetrically to losses, not just profits

Matter restored to AO only to quantify the exact loss attributable to gifted funds.

✅ The takeaway that changes everything:

Section 64 is a two-way street.

The department loves to club a spouse’s income with yours when profits arise from gifted funds.

But when losses arise from the same gifted funds — the same section allows those losses to be set off against your income.

Symmetry in law. Use it.

If you gifted funds to your spouse for trading and those trades resulted in losses — your tax advisor needs to see this ruling today.

— @CSALegal | Tax Lawyers

#IncomeTax #Section64 #ClubbiingProvisions #ITAT #CaseLaw #TaxPlanning #Derivatives #CSALegal

1

1

44

🔴 Case Law Decoded | AAR Rajasthan | June 2026

Allen Career Institute (P.) Ltd., In re

[2026] 186 taxmann 514 (AAR - Rajasthan)

A ruling every coaching institute and edtech company in India must read.

Facts: A leading IIT-JEE/NEET coaching institute provided offline classes, live online sessions, and pre-recorded video lectures — accessed by students across India. Study material couriered from Kota. Invoices raised from Rajasthan.

The institute’s contention: Online live and pre-recorded courses are OIDAR services — taxable under IGST based on the student’s location.

AAR held: NOT OIDAR. Entire supply taxable as CGST SGST.

The reasoning:

▸ Live classes involve substantial human intervention — interactive doubt-solving, user-specific responses

▸ OIDAR requires a fully automated electronic service with minimal human involvement

▸ Dispatch of printed study material integrated coaching = not a pure electronic supply

▸ Classification: SAC 999293 — commercial training and coaching

Students sitting in Mumbai, Chennai, or Kolkata does not change the nature of supply.

Intra-state supply. CGST SGST. Period.

✅ The takeaway for the entire edtech and coaching industry:

If your online course involves live teachers, doubt sessions, or human interaction — you are NOT an OIDAR service provider.

Your place of supply analysis, registration strategy, and tax structure must be built on this distinction.

Human teaching = coaching service.

Fully automated content = OIDAR.

The line is now clearly drawn. Structure accordingly.

@ALLENkota @PhysicswallahAP @aakasheduin @unacademy @vedantu_learn — this ruling directly affects your GST structure on online courses. Worth a review.

— @CSALegal | Tax Lawyers @advchahat

#GST #OIDAR #EdTech #CoachingInstitute #AAR #CaseLaw #IndirectTax #CSALegal

2

2

73

🔴 Case Law Decoded | ITAT Chennai | June 2026

Bose Saravanan vs. DCIT

[2026] 186 taxmann.com 1084 (Chennai Trib.)

A case every CA in India must read.

Facts: A Chartered Accountant declared income of ₹2.95 lakh. His bank account showed massive deposits — funds collected from clients to pay their income tax, VAT, TDS and service tax on their behalf.

The AO reopened under Section 148 and added ₹23 CRORES under Section 69A — treating client tax money as the CA’s unexplained income.

CIT(A) went further — ENHANCED the addition by ₹6.88 crores more.

Total addition on a CA earning ₹2.95 lakh: nearly ₹30 crores.

ITAT Chennai — entire addition DELETED.

The Tribunal found:

▸ Tax payments of ₹29.83 crores flowed OUT of the same account to government authorities

▸ Tax challans matched the bank debits on sample verification

▸ Bank narrations clearly showed payments to government departments

▸ The AO and CIT(A) completely ignored the debit side of the account

The CA acted as a conduit. The money never belonged to him.

✅ The takeaway for every practitioner:

When fighting a Section 69A addition on bank credits — the debit side of the account is your strongest evidence.

Credits tell half the story. Debits complete it.

The department saw ₹30 crores coming in.

It refused to see ₹29.83 crores going out — to its own treasury.

Justice took years. But the paper trail won.

— @CSALegal | Tax Lawyers @advchahat

#IncomeTax #Section69A #ITAT #CaseLaw #CharteredAccountant #Taxmann #TaxLitigation #CSALegal

2

4

146

The Small LLP Framework by @MCA21India is a game changer for India’s micro entrepreneurs.

But most people don’t know what it actually means in practice.

Here is why it matters:

Before Small LLP — a first-generation entrepreneur starting a small business faced:

▸ Same ROC filing fees as a ₹100 crore LLP

▸ Same penalty structure as large corporates

▸ Same compliance calendar — Form 8, Form 11, audit requirements

▸ Same cost of professional fees — CA lawyer filing agent

For someone earning ₹5-10 lakh annually — compliance cost was eating 15-20% of revenue.

Small LLP Framework changes this:

▸ Lower filing fees

▸ Simplified compliance requirements

▸ Reduced penalty exposure

▸ Lighter audit burden

Why does this matter for India?

6.3 crore MSMEs contribute 30% of India’s GDP and employ 11 crore people.

Most of them operate as proprietorships — unregistered, unprotected, unlimited personal liability.

Small LLP gives them limited liability protection at a cost they can actually afford.

A street vendor, a freelancer, a home baker, a tutor — all can now have a formal legal entity with liability protection for the cost of a monthly electricity bill.

Formalisation of India’s informal economy starts here.

@MCA21India @FinMinIndia @nsitharamanoffc @PIB_India @OfficeofPCM — now make the next step equally simple:

▸ Ensure physical PAN is auto-delivered post incorporation

▸ Link GST threshold exemption to Small LLP status automatically

▸ Pre-filled annual returns using MCA portal data — zero manual entry

Make it easy to stay formal.

India’s entrepreneurial revolution depends on it.

🇮🇳

— @CSALegal | Tax Lawyers

#SmallLLP #LLP #MCA #MSME #StartupIndia #EaseOfDoingBusiness #Entrepreneurship #CSALegal

1

2

31

Dear @IncomeTaxIndia @FinMinIndia @nsitharamanoffc @cbdt_india

A simple but urgent fix needed in Form 35 — CIT(A) appeal form.

Currently there is no separate column for the authorized representative’s email and phone number.

The portal sends hearing notices only to the email registered in the assessee’s profile.

If the assessee manages their own profile — the representative never gets notified.

Result: Hearing missed. Ex-parte order passed. Client suffers.

This happened in one of our matters recently. A completely avoidable injustice.

The fix takes 10 minutes of portal development:

Add two fields in Form 35:

▸ Authorized Representative Email ID

▸ Authorized Representative Mobile Number

All hearing notices auto-copied to both the assessee AND the representative.

No missed hearings. No ex-parte orders on technical grounds.

Justice should not fail because of a missing column in a form.

@askITR_official @ITD_eFiling — please escalate this to the portal team immediately.

— @CSALegal | Tax Lawyers

#IncomeTax #Form35 #CITAppeals #eFiling #TaxReform #CSALegal

1

1

3

1,874

CSA Legal retweeted

🚨 FSSAI has directed food vendors across the country to stop using newspapers for wrapping or serving food.

461

887

11,331

710,997

CSA Legal retweeted

🚨Polymer banknotes proposal under consideration,with banking regulator evaluating its pros and cons: RBI Governor

7

50

728

7,551

The government just proved it understands capital markets.

Income Tax Amendment Ordinance 2026 — FIIs and BIS exempted from tax on G-Sec interest and capital gains. Effective 1 April 2026.

Translation: Zero tax on government bond returns for foreign investors.

The logic is simple and correct:

Tax exemption → FIIs buy more G-Secs → higher demand for rupee assets → rupee strengthens → import costs fall → inflation cools → RBI cuts rates → businesses borrow cheaper → economy grows.

One ordinance. One chain reaction.

But here is the question that needs an answer:

If zero tax attracts foreign capital into G-Secs —

Why does 12.5% LTCG repel foreign capital from equities?

The economic logic is identical. The government has accepted the principle.

Now apply it consistently.

Zero LTCG on equities = same FII inflow story at 10x the scale.

@nsitharamanoffc @FinMinIndia — the ordinance is a great first step.

Budget 2027 should be the second.

🇮🇳

— @CSALegal | Tax Lawyers

#Ordinance2026 #FII #GSec #LTCG #IncomeTax #CapitalMarkets #Rupee #CSALegal

1

1

36

CSA Legal retweeted

Due to a fire incident at the MCA Data Centre site, an unscheduled switchover to the Disaster Recovery (DR) site was undertaken as a precautionary measure. As a result, some MCA services are yet to be fully restored.

We regret the inconvenience caused and appreciate your patience and cooperation while restoration activities are being completed.

41

19

84

16,734

🔴 Sunday Case Law | ITAT Delhi | May 2026

Pradeep Tyagi HUF vs. ITO

[2026] 186 taxmann 388 (Delhi Trib.)

Issue: AO made ₹1 crore addition for a single cash deposit in Kotak Mahindra Bank. Applied Section 115BBE directly — taxing it at 60%. CIT(A) confirmed. Assessee appealed to ITAT.

Held: Addition of ₹1 crore — DELETED entirely.

Reason: The AO jumped straight to Section 115BBE without first fixing the addition under any charging section — Section 68, 69, 69A, or 69B.

Section 115BBE is only a tax rate provision. It cannot operate in a vacuum.

Before applying 115BBE — the AO must first establish which charging section applies.

No charging section identified = no valid addition = no 115BBE.

✅ Practical takeaway for CAs and advocates:

If your client has received an addition where the AO has applied Section 115BBE without specifying the underlying charging section — challenge the addition at the threshold.

The legal infirmity is fatal to the entire assessment order.

Check every cash deposit addition before paying. Always.

— @CSALegal | Tax Lawyers

#IncomeTax #Section115BBE #Section69A #ITAT #CaseLaw #Taxmann #TaxLitigation #CSALegal

1

3

55

⚠️ Case Law Decoded | Rajasthan HC | May 2026

Umang Garg vs. Union of India

[2026] 186 taxmann 824 (Rajasthan)

Issue: Arrest under CGST for alleged fake ITC through bogus firms and goods-less invoices. Bail challenged — grounds of arrest said to be inadequate.

Held: Bail rejected. Arrest upheld.

Court held — grounds of arrest in writing DIN-linked memo acknowledgement signature of accused = sufficient compliance with Section 69 CGST.

Electronic evidence, WhatsApp chats, seized devices, forensic analysis — all formed basis of prima facie case.

📌 Critical message for practitioners:

Fake ITC is being treated on par with economic offences.

Courts are not granting bail where digital evidence trail exists.

Advisory to all clients: Clean up ITC mismatches now — before investigation begins. After arrest, options narrow significantly.

— @CSALegal | Tax Lawyers

#GST #FakeITC #GSTArrest #CGST #CaseLaw #Taxmann #IndirectTax #CSALegal

1

2

42

🔴 Case Law Decoded | Gauhati HC | May 2026

Sarda Eco Power Ltd. vs. State of Assam

[2026] 185 taxmann.com 738 (Gauhati)

Issue: GST registration cancelled for non-filing of returns. SCN did not specify the default period. Cancellation order passed within 30 days — no hearing, no reasons recorded.

Held: Cancellation set aside. Proceedings suffered from procedural infirmity and violation of natural justice — audi alteram partem.

Assessee directed to file all pending returns within 30 days.

✅ Practical takeaway:

If your client’s GST registration was cancelled and the SCN did not specify the exact period of default — challenge it immediately.

A non-speaking cancellation order without hearing is legally infirm regardless of the underlying default.

The department must follow procedure. Always.

— @CSALegal | Tax Lawyers

#GST #GSTRegistration #NaturalJustice #CaseLaw #Taxmann #IndirectTax #CSALegal

1

25

CSA Legal retweeted

May 29

Earn Income → Income Tax

Spend Money → GST

Buy Fuel → Excise & VAT

Buy House → Stamp Duty

Use Road → Toll Tax

Save Money → Inflation

Middle classs exploited Every Day.

38

179

630

11,712

ITR filings have plateaued as exemption thresholds rise.

The real story behind the numbers:

Lower-income taxpayers are exiting the filing net — not because they’re evading, but because the government deliberately raised thresholds to bring them relief.

The taxpayer base is shrinking at the bottom. Growing at the top.

₹5–10 lakh segment is now the largest filing category.

What this means going forward:

▸ Fewer filers = higher burden on those who remain

▸ Tax administration must become sharper — not broader

▸ Quality of compliance matters more than quantity of filers

The government removed 5 crore low-income taxpayers from compliance burden.

That is good policy — if the system now focuses its energy on the ₹10 lakh segment that genuinely needs scrutiny rather than harassing ₹3 lakh earners.

Less is more — only if enforcement becomes smarter.

🇮🇳

— @CSALegal | Tax Lawyers

#IncomeTax #ITRFiling #TaxPolicy #AY202627 #CSALegal

1

2

37

Dear @cbic_india @FinMinIndia @nsitharamanoffc

Rule 86B of CGST Rules is causing genuine hardship to stockists, distributors, and large traders across India.

On account of non-compliance, the Department suspends the GSTIN; however, no mechanism or clarification is provided regarding how the taxpayer is expected to discharge the mandatory 1% GST liability in cash despite having substantial Input Tax Credit balances running into lakhs or crores.

The honest stockist with real stock, real suppliers, real ITC — pays the price every single month.

Our formal request:

▸ Exempt taxpayers with more than 12 months of clean GST filing history from Rule 86B entirely

▸ Exempt taxpayers where ITC-to-turnover ratio is within normal industry benchmarks — verified by GSTN data automatically

▸ Raise the threshold — Rule 86B currently applies to taxpayers with turnover above ₹6 crore. Raise it to ₹20 crore minimum. Small traders are not the fraud risk this rule was designed for.

▸ Allow GSTN to auto-exempt clean filers — the data exists. Use it.

The GST system has 3 years of filing history for every taxpayer.

A taxpayer who has filed correctly for 36 consecutive months, has real stock, and real ITC is not a fraud risk.

Treat them accordingly.

Rule 86B was introduced as an anti-evasion measure.

It has become a working capital tax on honest business.

@GSTCouncil @askGST_Goi @Infosys_GSTN — this needs urgent review at the next GST Council meeting.

— @CSALegal | Tax Lawyers

#GST #Rule86B #ITC #GSTCouncil #WorkingCapital #Stockists #IndirectTax #GSTReform #CSALegal

1

11

Delhi hits 47°C in summer.

AQI crosses 400 every November.

We plant saplings for a day and forget them for a year.

Enough.

CSA Legal formally proposes — make this legally mandatory for every building in Delhi:

🌿 Vertical gardens on external walls of all commercial and residential buildings above 3 floors

🌱 Terrace gardens mandatory for all residential buildings above 200 sq yards

🌳 Minimum 2 trees per 100 sq yards of plot area for every new construction

🏗️ No Occupancy or Completion Certificate issued without green compliance — enforced by DDA and MCD

💰 Property tax rebate of 10% for buildings that comply — incentivise, don’t just penalise

The math is simple:

Delhi has 40 lakh registered buildings.

If even 10% adopt terrace gardens — that is 4 lakh green rooftops cooling an entire city.

One terrace garden reduces indoor temperature by 3-4°C — cutting AC usage, cutting electricity demand, cutting coal burning, cutting pollution.

It pays for itself.

Singapore made it mandatory. Their urban heat island effect is 40% lower than Delhi’s.

We have the land. We have the buildings. We have the crisis.

What we lack is the political will to make green compliance as non-negotiable as a fire NOC. But with Smt Rekha Gupta as CMA of Delhi, I am pretty confident that they will implement it.

@gupta_rekha

@LtGovDelhi @MCD_Delhi @DDADelhi @narendramodi @BJP4Delhi @PIB_India

Delhi does not need another committee on pollution.

It needs a Green Building Code with teeth.

Draft it. Enforce it. Fine those who don’t comply.

Our lungs cannot wait another winter.

🌳

@advchahat

#Delhi #GreenBuilding #VerticalGarden #TerraceGarden #DelhiPollution #DelhiHeat #AQI #MandatoryGreen #CSALegal #Environment

2

5

50