Has been engaged in stock trading since 2015 | Daily join over 50,000 learning groups, send me a private message and get the latest investment advice for free

Joined April 2011

- Tweets 25,263

- Following 580

- Followers 634

- Likes 150

137 Photos and videos

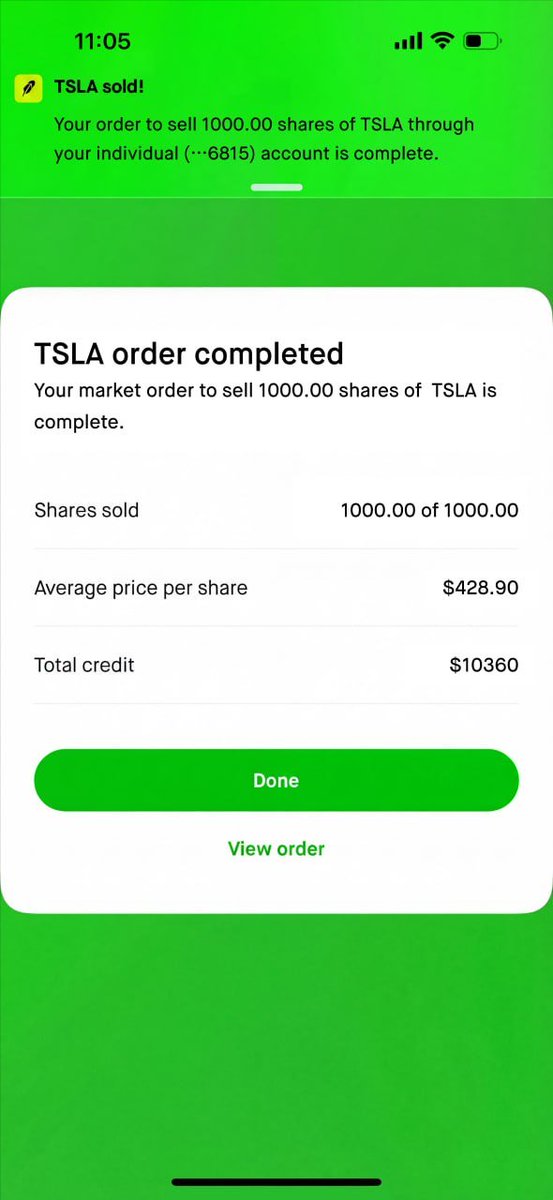

May 22

1000 shares sold.

Not luck. Not gambling.

Just strategy, discipline, and execution. 📈

51

May 20

$MSFT is rising after Microsoft unveiled new AI-focused Surface devices, but the real story isn’t hardware sales.

The market is pricing Microsoft as the “AI operating system” for enterprise tech.

Every new Surface Copilot launch strengthens:

• AI ecosystem lock-in

• enterprise AI adoption

• Windows Azure integration

• long-term Copilot monetization

Surface revenue alone won’t move a $3T company dramatically.

But these launches reinforce investor confidence that Microsoft can dominate the next decade of AI-powered productivity.

That’s why even small product events can support higher valuation multiples and continued stock price appreciation.

$MSFT remains one of the market’s safest large-cap AI compounders.

100

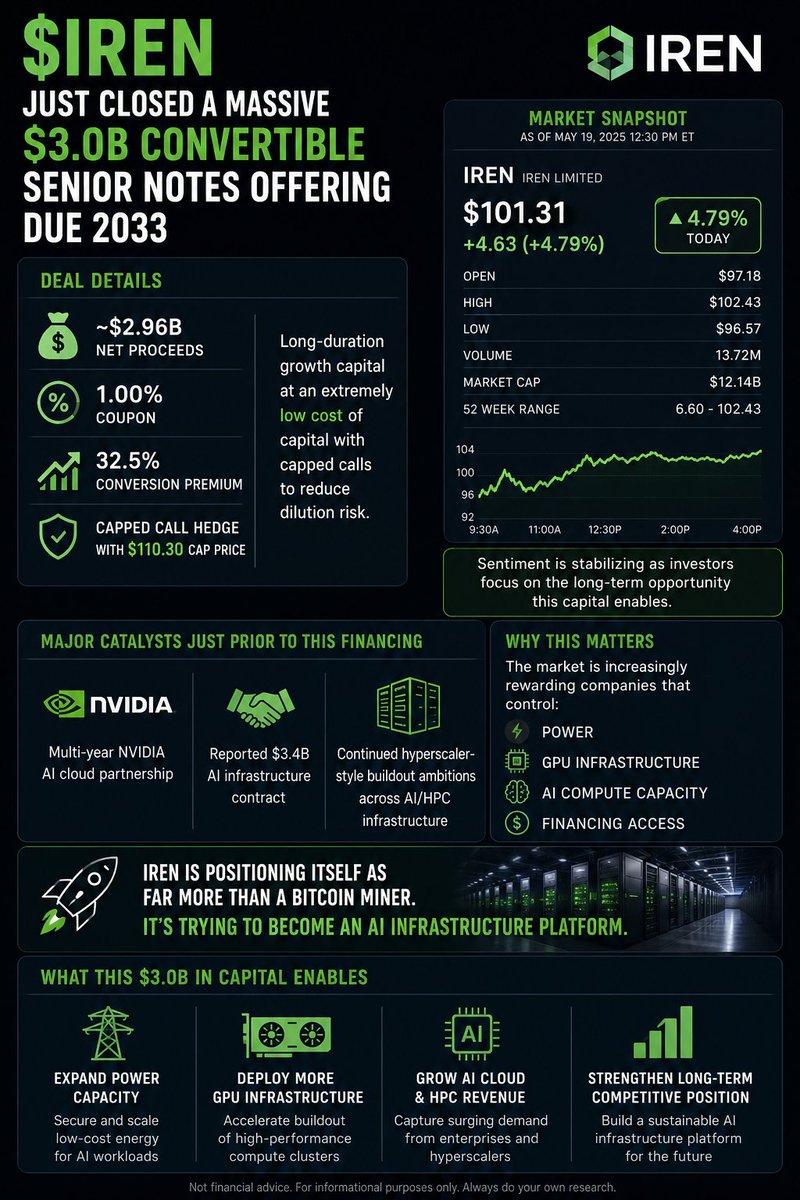

May 14

$IREN just closed a massive $3.0B convertible senior notes offering due 2033.

Key terms:

• ~$2.96B net proceeds

• 1.00% coupon

• 32.5% conversion premium

• capped call hedge with $110.30 cap price

The market initially sold the financing news on dilution fears, but sentiment is stabilizing as investors focus on what this capital enables:

massive AI infrastructure expansion. (Quiver Quantitative)

This comes right after:

• IREN’s multi-year NVIDIA AI cloud partnership

• a reported $3.4B AI infrastructure contract

• continued hyperscaler-style buildout ambitions across AI/HPC infrastructure. (Stock Titan)

The important part:

IREN just secured long-duration growth capital at an extremely low cost of capital while using capped calls to reduce dilution risk.

The market is increasingly rewarding companies that control:

power

GPU infrastructure

AI compute capacity

financing access

IREN is positioning itself as far more than a Bitcoin miner.

It’s trying to become an AI infrastructure platform.

1

240

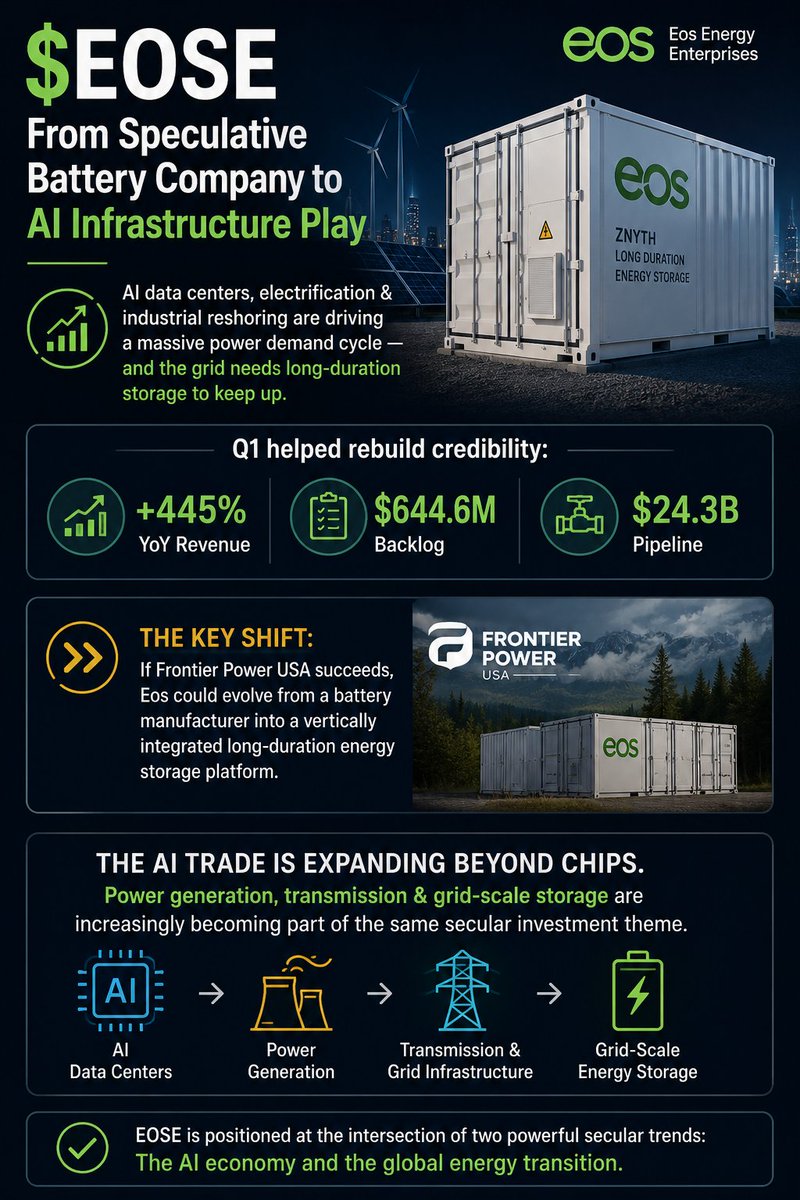

May 13

$EOSE is starting to trade less like a speculative battery company and more like a strategic AI infrastructure play.

AI data centers, electrification & industrial reshoring are driving a massive power demand cycle — and the grid needs long-duration storage to keep up.

Q1 helped rebuild credibility:

• Revenue 445% YoY

• Backlog: $644.6M

• Pipeline: $24.3B

The key shift:

If Frontier Power USA succeeds, Eos could evolve from a battery manufacturer into a vertically integrated long-duration energy storage platform.

The AI trade is expanding beyond chips.

Power generation, transmission & grid-scale storage are increasingly becoming part of the same secular investment theme.

1

245

May 11

Nvidia ( $NVDA) stock notched its third record close of the year on May 11 as investor enthusiasm over artificial intelligence (AI) and the microchip sector propelled its share price to…

Near term:

• Bull case → continued melt-up toward new highs if AI capex stays aggressive

• Base case → consolidation after this parabolic run

• Main risk → expectations getting too far ahead of execution

But as long as AI spending remains priority #1 for Big Tech, dips in NVDA will likely continue getting bought aggressively.

May 10

$NVDA no longer trades like a chip stock.

It trades like the core infrastructure layer of the AI economy.

My base case over the next 3–6 months: 10–20%.

Bull case if Blackwell demand explodes again: 40%.

Risk isn’t demand collapse.

Risk is expectations getting too far ahead of execution.

3

2

556

May 10

$NVDA no longer trades like a chip stock.

It trades like the core infrastructure layer of the AI economy.

My base case over the next 3–6 months: 10–20%.

Bull case if Blackwell demand explodes again: 40%.

Risk isn’t demand collapse.

Risk is expectations getting too far ahead of execution.

5

1

1

523

May 10

As long as AI infrastructure spending keeps accelerating, Nvidia’s long-term trend likely remains intact.

1

47

May 9

If you invested $10K in $RKLB three years ago, it’d be worth over $275K today. 🤯

The biggest winners in the market rarely look “safe” early on.

They usually share the same traits:

• massive TAM

• founder-led vision

• years of skepticism

• brutal volatility

• then exponential execution

The market is increasingly rewarding long-duration themes:

AI infrastructure, defense tech, robotics, energy, and space.

$RKLB wasn’t just a stock move — it was a reminder that asymmetric returns come from identifying paradigm shifts before Wall Street fully prices them in.

The hardest part isn’t buying early.

It’s holding through the chaos.

May 7

$RKLB just signed the largest launch contract in company history with a confidential customer.

The agreement includes:

• 5 Neutron launches

• 3 Electron launches

• Missions scheduled through 2029 across LC-1 and LC-3

This is a major signal for Rocket Lab’s long-term positioning.

Why it matters:

🚀 Neutron demand is becoming real before full operational scale.

📦 Multi-launch agreements create revenue visibility and strengthen backlog quality.

🛰️ Customers are increasingly looking for alternatives to SpaceX for dedicated launch capacity.

The market is starting to realize:

$RKLB is evolving from a small launch company into a vertically integrated space infrastructure platform.

Still early.

But this is exactly the type of contract that helps re-rate the long-term thesis.

1

831

May 6

Palantir isn’t just growing — it’s accelerating.

133% commercial

84% government

Guidance raised

Most people are still underestimating this story.

Explained why on Fox Business Network — $PLTR remains one of my highest-conviction bets.

7

10

5,209

May 8

If you'd like, I can share my live trading plan with you for free. 👍I believe this will be helpful. Let me know in the comments below or via private message.

23

May 8

$ASTS is moving from “prototype mode” to industrial-scale execution.

The company is expanding Texas manufacturing capacity to mass-produce next-gen Micron satellites featuring the largest commercial phased arrays ever deployed in LEO.

Why this matters:

• Faster constellation deployment

• Lower long-term production costs

• Better direct-to-phone connectivity

• Stronger competitive moat in space-based cellular

This is no longer just a speculative space story — it’s becoming a real infrastructure buildout.

Bull case: if ASTS successfully scales direct-to-device satellite broadband, the upside could be enormous.

Bear case: execution risk, cash burn, and manufacturing complexity remain very high.

High risk. High reward. Pure asymmetric bet.

2

2,147

May 7

$RKLB just signed the largest launch contract in company history with a confidential customer.

The agreement includes:

• 5 Neutron launches

• 3 Electron launches

• Missions scheduled through 2029 across LC-1 and LC-3

This is a major signal for Rocket Lab’s long-term positioning.

Why it matters:

🚀 Neutron demand is becoming real before full operational scale.

📦 Multi-launch agreements create revenue visibility and strengthen backlog quality.

🛰️ Customers are increasingly looking for alternatives to SpaceX for dedicated launch capacity.

The market is starting to realize:

$RKLB is evolving from a small launch company into a vertically integrated space infrastructure platform.

Still early.

But this is exactly the type of contract that helps re-rate the long-term thesis.

2

2

9

3,634

May 7

"NY Fed's Williams: Hard labor data shows stabilization, soft data hints at gradual softening → rising slack, but policy remains 'well-positioned.' Elevated inflation resilient economy = Fed on hold through much of '26.

Stocks get stability from soft landing hopes, but delayed rate cuts keep pressure on valuations & growth names. Volatility ahead on data & geopolitics. Higher-for-longer bias intact. #Fed #Markets"

1

106

May 7

Not that long ago, U.S. payroll growth of less than 100,000 or so a month meant the labor market was sinking and signaling a potential recession. No more, though, as that kind of number is pretty much all that is needed to keep unemployment steady and the Federal Reserve at bay.

1

1

36

May 7

$AMD ’s stock has now skyrocketed roughly 320% over the last 12 months as the shift toward agentic artificial intelligence boosts demand for its central processing units.

The market still thinks AI = GPUs.

But inference is changing the game.

As AI scales globally, CPUs, memory, networking, and power efficiency become critical bottlenecks too.

That’s why $AMD ’s positioning matters so much here.

Not just an AI chip company — a full-stack compute player.

4

1

1,734

May 7

$AMD ’s climb in yesterday’s session propelled the Nasdaq Composite to another all-time high and the S&P 500 to its first close above 7,300.

1

1

132

May 6

AI isn’t just GPUs anymore — CPUs are the new bottleneck as inference explodes.

$AMD is perfectly positioned: leading high-performance CPUs, strong heterogeneous architectures, and rising AI revenue mix (targeting ~$12B in 2026).

This isn’t hype. Hyperscalers need full-stack solutions. $AMD delivers.

Building core position on dips. Long-term winner in the AI infrastructure shift.

2

4

1,485

May 6

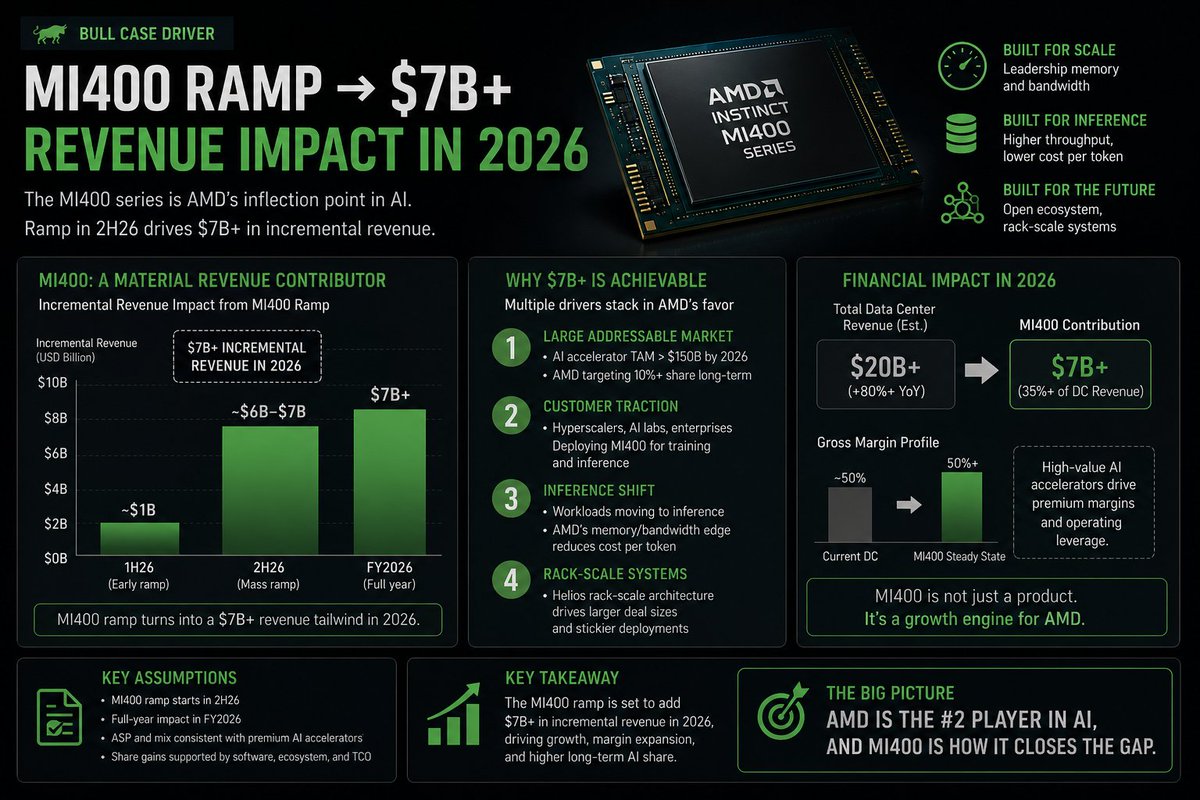

$AMD AI chip positioning is one of the most interesting setups in the market right now.

Strong #2 player Memory & inference edge Chasing NVIDIA with MI400/Helios But the gap is still huge.

Execution beats: 15-20% Solid but lags: flat to -5% Software/competition miss: -15% This isn’t just about hardware anymore.

It’s about closing the CUDA moat.Explore AMD AI chip positioning — long the alternative or still too early?

2

2

1,102

May 6

Palantir isn’t just a growth story anymore.

It’s becoming critical infrastructure for the AI era.

Most people are still treating it like a “story stock.”

That’s the opportunity. $PLTR

1

6

188