Dentist, self employed, interested in value investing, based in Germany

Joined December 2019

- Tweets 5,275

- Following 48

- Followers 263

- Likes 27,721

3 Photos and videos

Cesar Filip retweeted

Jun 3

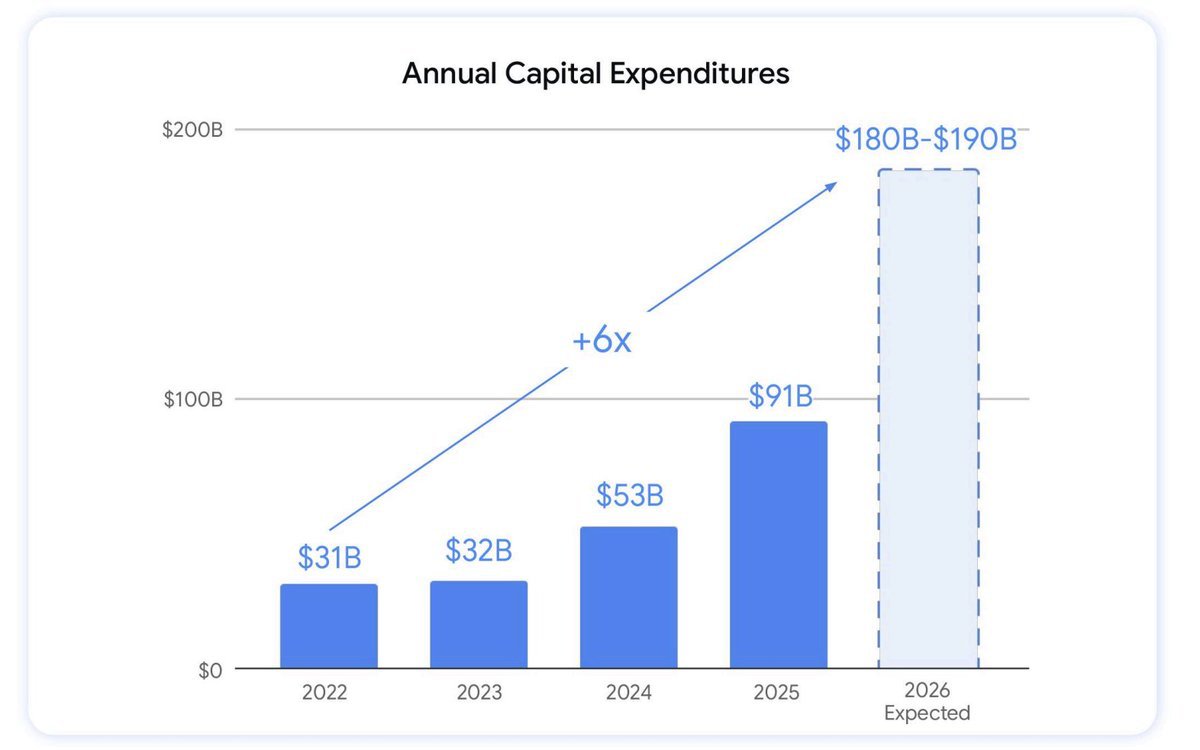

Amazon, Microsoft, Meta and Alphabet are going wild with R&D and CapEx spending.

These businesses were infamous for a few attractive attributes:

1. They were asset and capital-light (but with enormous CapEx, that is no more)

2. They had amazing return on capital and cash conversion ratios (but with enormous CapEx, that is no more)

3. They were internally financed (requiring no debt) and even had excess cash flows to return to shareholders (but with enormous CapEx, that is no more)

6

6

35

2,986

Cesar Filip retweeted

May 26

I’m in love with this sentence:

“The longer you stay on the wrong train, the more expensive it is to get home.”

94

4,252

21,550

317,265

May 23

RT @InvestingCanons: Yesterday, Warren Buffett described investor Chris Hohn's performance to the Financial Times as "Exceptional"

Hohn's…

39

Cesar Filip retweeted

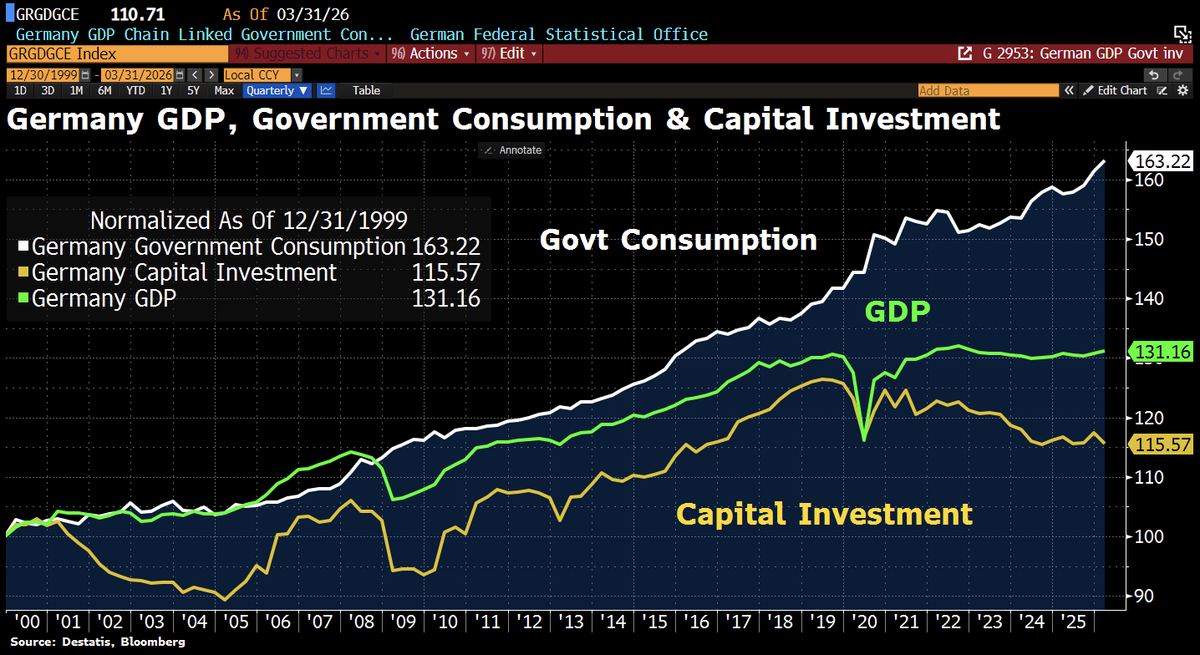

Good Morning from Germany, where the road to socialism is paved with ever-rising govt consumption. Since 1999, state consumption is up 63%, while GDP has risen only 31% and capital investment a meagre 16%. The public sector keeps expanding, but the investment base is stagnating. Germany is becoming less of a market economy and more of a state-led redistribution machine.

155

959

3,070

273,397

Cesar Filip retweeted

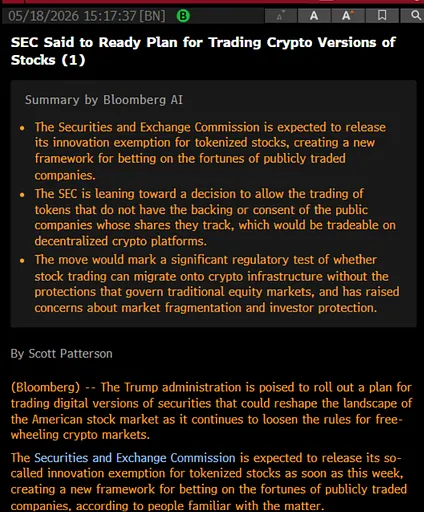

Crypto stocks. We may be headed full-on to a Snow Crash cyber-punk future with no long-term personal relationships and digital value embedded in all of us directly correlated to the value provided to a society that increasingly devalues humanity. This may be the point in time that needs to be stopped from going forward by some future being. #snowcrash

212

184

1,370

285,320

Michael Burry urged investors to scale back exposure to surging technology stocks, saying the current market environment has reached historically dangerous extremes reminiscent of prior speculative bubbles.

The famed investor, best known for predicting the 2008 housing collapse, said investors should “reject greed” as enthusiasm around artificial intelligence and momentum-driven trades pushes valuations sharply higher.

Read more: cnb.cx/4npOw8v

103

128

465

82,500

Cesar Filip retweeted

May 8

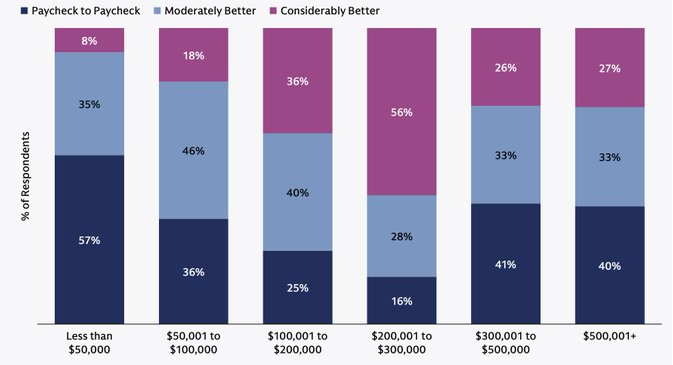

Insane stat: 40% of $500K earners say they are living paycheck to paycheck.

That's not an income problem - it's a lifestyle problem.

If your spending scales with your income, you’ll always feel broke.

46

52

368

40,196

Apr 18

👏👏👏👏

As Carl Jung put it, "Man needs difficulties. They are necessary for health." Yet most people instinctually avoid pain. This is true whether we are talking about building the body (e.g., weight lifting) or the mind (e.g., frustration, mental struggle, embarrassment, shame)--and especially true when people confront the harsh reality of their own imperfections. #principleoftheday

10

Mar 22

RT @InvestingCanons: “Price fluctuations have only one significant meaning for the true investor:

They provide an opportunity to buy wisel…

26

Mar 19

👏👏👏

Mar 19

Peter Lynch: If you can't explain to an 11-year-old in a minute or less why you own a particular stock, you shouldn't own it and should just buy a fund instead.

20

Cesar Filip retweeted

"Society is being destroyed by schools and college teachers. Your children are indocrinated by people who are doing what they are doing because of their limited intellect and practical skills. And the costs TO YOU of such indocrination are ballooning." - Nassim Nicholas Taleb

6

34

295

9,741

Cesar Filip retweeted

Feb 27

Is reading one page so difficult? No, it’s easy. But do you know why people don’t read? Because they think about finishing the whole book instead of just reading the next page. And how do you finish a book quickly? By reading for hours consistently. And who reads for hours? The one who has been reading consistently for years. How did they build that habit?They started with one page.

45

217

1,303

37,460

Cesar Filip retweeted

Feb 19

Remember this scene in The Big Short?

Jamie Shipley and Charlie Geller have bet everything against the housing market.

They've been bleeding for months, wondering if they're wrong.

Then they flip on CNN and see it: New Century Financial - the second-largest subprime lender in America - has filed for bankruptcy.

"It's starting."

That was April 2, 2007. New Century wasn't the crisis. It was 1% of the problem. But it was the first domino.

4 months later, BNP Paribas froze 3 funds citing "complete evaporation of liquidity." 18 months after that, Lehman was dead.

I'd encourage you to watch that scene today. Because we JUST got our New Century moment in private credit:

Blue Owl Capital - $307 billion in assets under management - just permanently halted investor redemptions at its retail private credit fund, OBDC II.

Investors will NEVER AGAIN redeem shares from this fund.

On January 25th, I wrote that private credit was showing cracks at the exact moment Wall Street wanted to open it up to your 401(k).

3 weeks later, here we are.

The timeline follows a pattern anyone who's been around markets long enough recognizes:

Through the first 9 months of 2025, OBDC II investors withdrew $150 million - up 20% year over year.

Meanwhile, Blue Owl execs publicly assured investors there was "no meaningful pressure" on their asset base.

But there was. And they're now facing a federal class-action lawsuit for saying otherwise.

In November, they attempted a merger that would have forced OBDC II investors into a publicly traded fund trading at a 20% discount to NAV. Effectively confiscating a fifth of their capital.

Blue Owl's own CFO conceded investors "could take a potential haircut." The stock dropped 11% in 8 days. They killed the deal.

Now they've abandoned the pretense entirely. PERMANENT halt. Fire-selling $1.4 billion in loans across three funds.

Investors get roughly 30% of NAV back through quarterly distributions - on Blue Owl's schedule, not theirs.

One delightful detail:

Blue Owl's co-CEOs have pledged $1.9 billion of their OWN company shares as collateral for personal loans - proceeds used, in part, to acquire the Tampa Bay Lightning.

The stock is down 33% this year. That collateral has literally shed $260 million since January.

Founders leveraging company stock for hockey teams while retail investors queue up for their own money. Wall Street's version of noblesse oblige.

But here's what matters:

This isn't about Blue Owl.

Blue Owl is a symptom.

The disease is a $3.4 TRILLION private credit industry built on opacity, conflicts of interest, and the polite fiction that illiquid assets can offer liquid redemptions.

Morningstar DBRS reports the trailing default rate has risen to 4%, up from 2.8% a year ago.

Downgrades outpacing upgrades. Outlook negative. UBS warns defaults could reach 13% if AI disrupts the software companies making up 17% of BDC loan portfolios.

Payment-in-kind loans (where borrowers can't pay cash interest and simply pile it onto the debt) have surged past 11% of BDC income.

When your borrowers are paying you with IOUs, the word "income" deserves quotation marks.

And the government's response?

Open YOUR 401(k) to private credit.

Trump's executive order directed regulators to do exactly that.

They want to "democratize" an asset class whose flagship retail product just permanently locked investors out.

The KKRs. The Blackstones. The Apollos. Everyone loaded up on private credit is exposed.

When the tide goes out, you find out who's swimming naked.

In April 2007, New Century went bankrupt.

Most of the financial world shrugged. 17 months later, Lehman made the point impossible to ignore.

And Blue Owl permanently halted redemptions TODAY.

AVOID PRIVATE CREDIT

AVOID PRIVATE EQUITY

Because it's starting...

Jan 28

In August, President Trump signed an executive order titled "Democratizing Access to Alternative Assets for 401(k) Investors."

The order directs regulators to make it easier for your retirement savings to flow into private credit, private equity, and other "alternative" assets.

The Department of Labor quickly rescinded Biden-era guidance that had discouraged these investments in retirement plans.

Apollo. Blackstone. Goldman Sachs. State Street.

They're all racing to launch private credit products for your 401(k).

But here's the problem:

Private credit is showing cracks at the exact moment they want to open it up to retail investors.

Just this week, BlackRock TCP Capital - one of the largest publicly traded private credit funds - plunged 17% after disclosing a 19% writedown on its net asset value.

The biggest drop in almost six years.

This is BlackRock. The world's largest asset manager. $14T in assets.

If they're taking hits like this, what chance does your 401k have?

Let me walk you through what's actually happening in this market...

Private credit has ballooned to over $2T in assets.

For years, it was the domain of sophisticated institutional investors - pension funds, endowments, insurance companies.

These investors have teams of analysts, lawyers, and risk managers to evaluate complex deals.

Your average 401k participant doesn't have any of that.

And the timing couldn't be worse.

The IMF's 2025 Financial Stability Report found that 40% of private credit borrowers now have NEGATIVE free cash flow.

That's up from 25% in 2021.

Goldman Sachs data shows 15% of borrowers can no longer generate enough cash to fully cover their interest payments.

UBS forecasts that private credit defaults could climb by 3 percentage points in 2026 - outpacing leveraged loans and high-yield bonds.

Meanwhile, payment-in-kind loans - where struggling borrowers defer interest by adding it to their debt balance - have surged from 7.4% in 2021 to over 11% today.

When a company can't pay interest in cash, that's not a sign of health.

It's a sign of stress being disguised.

Then came September's wake-up call:

Auto parts maker First Brands collapsed with $8B in off-balance-sheet financing that wasn't properly disclosed to lenders.

Subprime auto lender Tricolor imploded amid allegations it pledged the same loans as collateral to multiple creditors.

Both received clean audits shortly before they cratered.

First Brands' term loans went from 90 cents on the dollar to under 15 cents in weeks.

JPMorgan's Jamie Dimon put it bluntly: "When you see one cockroach, there are probably more."

Here's what makes this dangerous:

Private credit is lightly regulated, less transparent, and difficult to value accurately.

The managers making the loans are often the same ones valuing them.

They have every incentive to delay recognizing problems.

The DOJ has already issued warnings about "creative" marks and questionable valuation practices.

Banks aren't insulated either. They've lent over $2.2T to non-bank financial institutions.

When problems surface in private credit, banks feel it too.

And now they want to put this in YOUR retirement account.

The pitch is that private credit offers "higher returns" and "diversification."

But the data doesn't support the sales pitch:

Recent research shows pension funds increasing exposure to private markets have actually seen depressed returns compared to simple stock and bond portfolios.

The 50 largest US pension funds averaged just 7.4% returns over the past decade.

A basic 60/40 portfolio beat many of them.

The real beneficiaries are fund managers charging 2% fees on assets that can't be easily valued or sold.

My view really hasn't changed:

AVOID PRIVATE CREDIT

When sophisticated institutional investors start pulling back - and they are - the last thing you want to do is rush in.

Stay in liquid, transparent, low-cost investments for your retirement.

Don't be the exit liquidity.

210

894

4,404

1,528,329

People lie more than most people imagine. I learned that by being in the position of being responsible for everyone in the company. While we have an exceptionally ethical group of people, in all organizations there are dishonest people who have to be dealt with in practical ways. For example, don't believe most people who are caught being dishonest when they say that they've seen the light and will never do it again because chances are they will. Dishonest people are dangerous, so keeping them around isn't smart. #principleoftheday

90

185

1,511

115,562

Is it harder to start today? 📉

The truth is, the environment has changed. You need more resources for compliance and regulation than I did when I started. But the core principle remains: Money follows talent.

If you have the ideas and can demonstrate the logic behind them, the capital will find you. That’s how I went from playing the markets as a kid to managing an account for the World Bank.

Are you focused on the money, or are you focused on the talent? Let me know in the comments. 👇

68

70

625

89,973

Cesar Filip retweeted

“The best people possess a feeling for beauty, the courage to take risks, the discipline to tell the truth, the capacity for sacrifice.”

―Ernest Hemingway

21

389

1,875

59,879

Cesar Filip retweeted

"Je quitterai ce monde sans tristesse. La vie ne m’attire plus. J’ai tout vu, tout expérimenté. Je hais l’époque actuelle, elle m’épuise ! Partout, je ne vois que des créatures détestables. Tout est faux, tout est remplacé. Chacun rit de l’autre sans jamais se regarder lui-même !

Il n’y a même plus de respect pour la parole donnée. Seul l’argent compte. Chaque jour, nous sommes inondés de récits de crimes.

Je sais que je quitterai ce monde sans regret, sans tristesse pour ce qu’il est devenu."

Alain Delon (1935-2024)

372

1,920

8,324

321,753

Cesar Filip retweeted

Charlie Munger:

“The secret to life is easy because it's so simple:

You don’t have a lot of envy or resentment. You don’t overspend your income. You stay cheerful in spite of your troubles. You deal with reliable people and you do what you’re supposed to do.”

27

574

4,393

287,967