Joined August 2016

- Tweets 3,365

- Following 384

- Followers 3,575

- Likes 13,856

192 Photos and videos

Lightbridge ($LTBR) attended the White House meeting today to discuss the DoE's new UPRISE initiative.

This is about up-rating equipment at existing US nuclear plants as well as restarts. Lightbridge's participation shows the interest in retrofitting existing LWR plants with metal fuel, as I discussed in my recent report on the WNFM Conference. #uranium

x.com/LightbridgeCorp/status…

energy.gov/ne/articles/natio…

CEO Seth Grae attended the White House launch of UPRISE, a federal initiative to expand U.S. nuclear capacity by maximizing output from the existing reactor fleet.

Lightbridge advanced #nuclearfuel technology is designed to do just that -- enable reactors to produce more power from the same facility. Hence, it could play a major role in increasing existing U.S. nuclear plant output.

@GovNuclear

Learn more about Lightbridge Fuel here: ltbridge.com/lightbridge-fue…

1

1

13

1,530

Jun 15

World Nuclear Fuel Market Conference - 2026 (Scottsdale, AZ)

Part 1

I attended this excellent conference for the first time this year, where uranium producers and utilities met to negotiate prices and deliveries. The attendance was large with the entire nuclear fuel supply chain being well represented.

The economics for utilities have improved so much that they are installing up-rated equipment as fast as possible, even beyond what is disclosed publicly, including moving to higher fuel enrichments (6.25% and up). This is the next logical step, after conventional up-rates are done. Analysts agree the supply chain is not ready for this, let alone new builds.

New builds are now competing for many of the same components required for the up-rate projects.

The term "super up-rates" is also being used some, informally. One example is retrofitting to move to metal fuel (something like Lightbridge) for the existing LWR fleet.

Most of the growth in mining is currently ISR, but uranium milling is still seen as a weak spot. However, Energy Fuels is still running their White Mesa mill intermittently.

New investment really needs to ramp very quickly, but it's mostly private start-ups stepping into the fray at present, particularly for conversion.

The field of SMR and fuel cycle start-ups is now about 150 companies and many are expecting a major shake-out, soon.

We have 2 new start-ups that will do uranium conversion in Texas, FluxPoint Energy and Raven-Flint. This is in addition to UEC's plan and Solstice's (Converdyn) announcement they are up-sizing their expansion plans for the Metropolis plant and even considering a "Metropolis 2.0", in some central Southern state.

If this new conversion capacity gets built, the pressure will focus on the enrichment bottleneck even more.

It really makes me wonder what Cameco has been waiting for at Port Hope and Springfields? I'm also concerned about the Cameco/Silex GLE partnership, but I'm writing a separate report on that (Stay tuned).

General Matter, a very private enrichment start-up that recently won a $900 million contract from the DoE, was a hot topic.

GM claims to be ahead of their competition and will have the lowest cost SWUs. Of course, that's only really possible if their technology is somehow more efficient than centrifuges and/or lasers.

Their arrogance is amazing. While their laser enrichment peers have spent years explaining the merits of SILEX, CRISLA and QLE, GM refuses to disclose anything about their tech. "Just trust us, you don't need to know". It really does not land well with utilities, coming from a Silicon Valley start-up with no experience in this industry. But, they have a website now and "EXIM-backed financing".

GM has said their prospective customers are in the loop on their technology. But, some large fuel buyers told me they somehow missed those meetings. They seem to know less about GM than I do.

As I have written, I think GM's tech is either an updated version of gaseous diffusion or Calutrons, but that would not be more efficient. But, why would this be a secret? Why insult the intelligence of your prospects in the room? My theory is their tech was granted to them from a DoE lab, with never-to-be-disclosed requirements attached, because of nuclear proliferation concerns.

More on GM's tech:

x.com/ClayDMontgomery/status…

It's uncomfortable, but GM represents a larger trend, most of the desperately needed new investment in the US fuel supply chain is coming from private start-ups that tend to be really opaque and short on commercial scale production experience.

I also got confirmation that the secret waivers from the Canadian government for Atlantic Ro-Ro carriers that transport the Russian uranium (EUP) to the US are continuing to at least 2028. There is an annual meeting in Canada where DoE officials renegotiate this. It's still one of the best cards Canada has in trade negotiations with the US and the details of these meetings are still secret, including the waiver documents themselves.

Imported EUP Schedule:

arrcm.com/schedule.html

The lack of discussion on spent fuel reprocessing and plutonium was disappointing. There is actually a lot of this work going on behind the scenes now. This industry still does not want to talk about it. This is for the next generation of reactors that need HALEU.

The Trump Administration is currently negotiating the sale of 34 metric tons of weapons-grade plutonium to 5 SMR start-ups to substitute for HALEU.

Doing the math, that could produce about 136 metric tons of MOX to substitute for HALEU (or about 680 tons of MOX to substitute for LEU). That is over 150 years of Centrus' current production from their 16 centrifuge cascade (which produces 900 kg/year from LEU feedstock). Seems important.

How could this affect uranium miners? That 34 tons of plutonium is energy-equivalent to approximately 17 million lbs of mined U3O8. Remember when we got into the uranium sector because "there is no substitute"? Well, a lot of uranium (for HALEU at least), IS being substituted, because of the looming enrichment supply crisis.

French start-up Nuward is even using MOX substitution as a selling point for their SMRs, in Europe.

#Uranium #nuclear #SMR $CCJ $LEU $SOLS

Jan 20

What is the uranium enrichment technology currently being developed by General Matter?

Some of their recent statements and a big award from the DOE forced me to rethink this and I found something that changes my opinion on their viability.

GM says their technology is novel but has a high TRL (technology readiness level). "Novel" rules out centrifuges and "high TRL" rules out laser enrichment. So what else could it be? I thought it was an electrochemical process, such as Ubaryon, but there is a better candidate - Gaseous Diffusion updated with modern technology.

The old GD machines at Paducah used 50x more power per SWU than centrifuges. But, what if they were redesigned using modern tech? That 50x gap could be reduced considerably with higher quality porous membranes. Perfect membranes would require billions of precision 10 to 20 nm holes per inch. That was really hard to do in 1945. But, today it is routine in the semiconductor industry.

Modern chip fabs can make nearly perfect membranes for higher efficiency Gaseous Diffusion of UF6.

But, can silicon withstand corrosive UF6 gas? Not directly. However, aluminum metalization layers are commonly used on most chips today and Al does handle UF6 very well. It was used in the old GD machines.

General Matter has its origins in silicon valley where they know what can be made in chip fabs. I worked in the semiconductor industry for 25 years.

Remember inkjet printers? They work by squirting ink through an array of precision microscopic holes in a silicon chip.

The biggest technical obstacle for GM would probably be demonstrating that they can handle the UF6 corrosion with aluminum metalization. The remainder of GD machines are basically just gas compressors and cooling equipment. That's the sort of conservative tech that fits DOE's mandate for supplier diversity to reduce risk.

It's hard to know how far a perfect membrane could go to closing the power efficiency gap with centrifuges and laser enrichment. But, I now think General Matter could quickly become a serious competitor to GLE and Centrus Energy.

If I'm right about this, it means that new GD machines will eventually populate the same building that used to house the old GD machines (and next door to GLE) in Paducah, KY.

#Uranium #nuclear #silex $ccj $leu

10

7

47

6,144

Jun 15

Part 2 - Tour of Palo Verde Generating Station

We also toured the Palo Verde Nuclear Plant, 4 GW of very reliable power in the Sonoran desert, 20 miles SW of Phoenix.

It's a very impressive triple LWR plant which uses recovered waste water from Phoenix for cooling. Palo Verde has 9 cooling towers, but they are only about 15 feet high. They were designed specifically for the hot and dry climate.

It seems like this design could be replicated through out the Southwestern US, but they are spending $10 million just on cooling tower maintenance, each time they replace fuel. The biggest problem is removing calcium deposits from the hard water. The water is recycled up to 25 times before it evaporates.

They also share some of the water with gas-fired plants next door, which produce twice as much power.

It's impressive how self-sufficient Palo Verde is. They do almost all maintenance themselves, particularly on the cooling towers because these things are so unique. Everything is on site, dedicated security, impressive emergency vehicles, 40 years of spent fuel casks and the previous turbines that they replaced decades ago. They even pour the concrete for their dry cask storage containers on site. No thank you Orano.

Their only external dependency is their just-in-time fuel deliveries from Westinghouse and Framatome.

They don't keep a fuel inventory and they don't buy EUP from Russia!

The frequent question was "why aren't you building more reactors yet?" More water is available from a growing city and the power is certainly needed.

The answer is complex. The grid does not have any capacity to spare and the switch yard needs to be completely rebuilt. It's already one of the largest in the US.

Palo Verde is owned by a consortium of 7 utilities that are very risk-averse and building another 8 foot water pipe 20 miles to the city and a pump station, would be expensive.

This plant funds a big slice of public education in Arizona and Palo Verde really struggled in its first 15 years and very nearly failed because of technical problems. The owners are not eager to relive those years. The unspoken reason is because natural gas is still so cheap.

1

16

690

Apr 13

Remember when we used to create tutorial programs to show how new software algorithm concepts work called "Hello World" programs? The idea was simple, condense example code down to the most minimal form that still demonstrates the new concept, so that learners don't get distracted by implementation details.

One of my favorite YouTubers, Dave Plumber (who created the Task Manager for Windows 95) has created a sort of Hello World program for the foundational AI concept called "Transformers".

Maybe this is only cool for me (because I took a pdp-11 assembly programming class in 1983 and actually liked it), but implementing Transformers on a 6 MHz DEC VAX minicomputer with only 64K of RAM, brilliantly guarantees there is no superfluous complexity and the instructor stays focused.

This is not only nostalgic, but Dave gives a great and concise explanation of how Transformers actually work, with not-so-subtle reminders that these algorithms are really not so new or magical. AI still has real fundamental limitations no matter how much it is scaled up or used as an excuse for layoffs.

#aipower #AI

youtu.be/OUE3FSIk46g

3

869

Feb 16

Summary of the energy-related conferences that I plan to attend this year. I particularly recommend Enverus Evolve (oil/gas) and the TNA Summit, which are also the lowest cost.

January 20-22 PowerGen - San Antonio, TX

powergen.com/

May 4-6 Enverus Evolve - Houston, TX

enverus.com/evolve-2026/

May 11-12 Reuters SMR & Advanced Reactors - Austin, TX

events.reutersevents.com/nuc…

May 31-2 World Nuclear Fuel Market - Scottsdale, AZ

wnfm.com/meetings/wnfm-52st-…

August 4-5 Nuclear Opportunities Workshop - Knoxville, TN

eteconline.org/now/

August 24–27 NEI/ANS NECX - Dallas, TX

nuclearenergyconference.org/

September ? Texas Nuclear Alliance Summit - Austin, TX

nucleartexas.com/

October 18-21 NEI Uranium Fuel Seminar - Houston, TX

nei.org/conferences/

November 9-11 Fertilizer Institute Market & Logistics - Atlanta, GA

tfi.org/event/market-and-log…

2

890

Feb 15

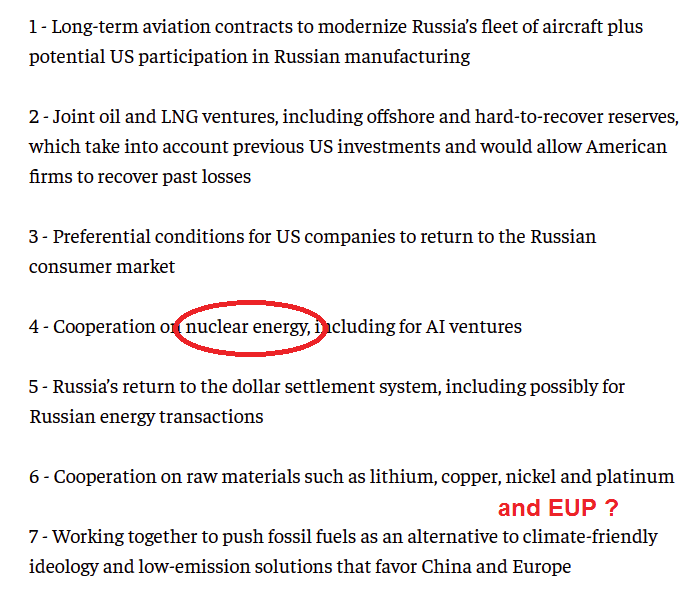

According to Bloomberg and India Times, a high-level memo has been leaked from an internal Russian document which details 7 points where Russian and US economic interests could converge following a deal to end the war in Ukraine. The memo mentions nuclear energy and raw materials, specifically.

This memo could be bad news for uranium stocks this week, if Wall Street takes notice. Even though the word "uranium" is not there yet, I think that will soon become apparent.

Pressure from nuclear utilities is increasing to re-normalize relations, to continue the pre-Ukraine war "good ole days" of $30/lb uranium, given the current circumstances of a looming ban on imports and very little progress in rebuilding US domestic fuel infrastructure.

The headline at the moment is Russia re-embracing the US dollar again as part of a wide-ranging economic partnership with the Trump administration.

The Kremlin wrote this memo, not Trump! If it's real, anything is possible.

Also, the Atlantic Council will release a new report this week titled, "Negotiating with Putin’s Russia", which might provide more info.

#uranium $CCJ $LEU $UEC

economictimes.indiatimes.com…

Areas Where Kremlin Memo Sees US and Russian Economic Interests Converge:

7

1

18

3,412

Jan 20

What is the uranium enrichment technology currently being developed by General Matter?

Some of their recent statements and a big award from the DOE forced me to rethink this and I found something that changes my opinion on their viability.

GM says their technology is novel but has a high TRL (technology readiness level). "Novel" rules out centrifuges and "high TRL" rules out laser enrichment. So what else could it be? I thought it was an electrochemical process, such as Ubaryon, but there is a better candidate - Gaseous Diffusion updated with modern technology.

The old GD machines at Paducah used 50x more power per SWU than centrifuges. But, what if they were redesigned using modern tech? That 50x gap could be reduced considerably with higher quality porous membranes. Perfect membranes would require billions of precision 10 to 20 nm holes per inch. That was really hard to do in 1945. But, today it is routine in the semiconductor industry.

Modern chip fabs can make nearly perfect membranes for higher efficiency Gaseous Diffusion of UF6.

But, can silicon withstand corrosive UF6 gas? Not directly. However, aluminum metalization layers are commonly used on most chips today and Al does handle UF6 very well. It was used in the old GD machines.

General Matter has its origins in silicon valley where they know what can be made in chip fabs. I worked in the semiconductor industry for 25 years.

Remember inkjet printers? They work by squirting ink through an array of precision microscopic holes in a silicon chip.

The biggest technical obstacle for GM would probably be demonstrating that they can handle the UF6 corrosion with aluminum metalization. The remainder of GD machines are basically just gas compressors and cooling equipment. That's the sort of conservative tech that fits DOE's mandate for supplier diversity to reduce risk.

It's hard to know how far a perfect membrane could go to closing the power efficiency gap with centrifuges and laser enrichment. But, I now think General Matter could quickly become a serious competitor to GLE and Centrus Energy.

If I'm right about this, it means that new GD machines will eventually populate the same building that used to house the old GD machines (and next door to GLE) in Paducah, KY.

#Uranium #nuclear #silex $ccj $leu

14

4

60

7,967

19 Nov 2025

NEI International Uranium Forum - Charleston, SC

Part 1

This was my 4th year at NEI's International Uranium Forum and I know a lot of these people by name now.

The mood was optimistic and exciting because of all the recent news and announcements. But, apprehension and trepidation still plague this industry that knows they are not ready for the fuel demand that is coming.

We're still trying to understand the problem. Uranium is finally trading in $90/lbs range that miners have said they need to explore and build new mines, but it's still not happening. Why? Because, utilities have stepped back from long-term contracting. The larger ones have substantial inventories of EUP (enriched uranium product) in the US. It's the smaller players and newcomers that are scrambling to find alternative sources of supply. Many of them have big tech money behind them. What we're still not seeing is big tech financing uranium mines or conversion and enrichment plants, which continue to be the actual bottleneck.

There was an honest shift in the presentation titles this year, acknowledging the looming shortages. All the new builds that are planned are finally forcing this issue to the fore:

Onshoring Nuclear Fuel - Can the US Govt Deliver?

Bridging the Uranium Supply Gap

What Keeps You Up at Night? - Perspectives Across the Nuclear Fuel Cycle

I'm not a lone voice crying wolf anymore. Everyone is discussing EUP supply problems (and HALEU) out loud now. But, it's a bifurcated problem, the large utilities have EUP inventories. It's the new players that are being forced to pursue recycling spent fuel and/or plutonium.

Jonathan Hinze (UxC) gave us the annual update on the global uranium market from UxC. He emphasized how much uncertainty there is now with US government involvement plus the new demand from start-ups and non-utility customers (SPUT). His advice for fuel buyers is to be nimble, flexible and prepare for the unexpected. New uranium mines are notoriously difficult to start. LEU is now available from Urenco, which will create more demand and physical uranium holdings by financial players (SPUT) have become really large.

He also said, "the emergence of advanced fuel cycles will greatly alter supply and demand dynamics" and "fuel recycling also seems likely to accelerate soon." I agree, but he won't talk about imports from China or the bifurcation of entrenched players with EUP and the newcomer have-nots.

Dr. Kaajal Desai (WNA) presented the latest WNA World Nuclear Fuel Report. She said that although there is enough uranium for global needs now, new mines are not being built fast enough to meet demand in the next decade. They have long held that there is sufficient conversion and enrichment capacity, globally. But this year, they were compelled to finally segment the report into different geopolitical regions, which shows that Western countries are still way too dependent on Russian supply.

WNA has reclassified how they account for secondary supplies of EUP due to major shifts in political alliances since the Ukraine war. It's about time.

WNA now forecasts that conversion will remain under-supplied in the West, until 2040 and "there is significant risk of supply disruption". WNA has good data, but they're behind the curve in recognizing the importance of geopolitics.

In the Bridging the Uranium Supply Gap panel, Lisa Aitken (Cameco) explained that uranium mining is still the long lead time item and they project a structural supply gap from 2030. New mines are needed. But, "long-term contracting is fairly anemic at 45 million lbs (for 2025)" and Cameco is still waiting for utilities to step-up contracting before they invest in new mines. It used to be that $45 was the price needed to incentivize new mines, then it was $60. But, now we are at $90, and the large miners are still waiting. There is still the collective memory of large assets being shut down and an expectation that trade polices are likely to shift again.

Imports of EUP from China was still the elephant in the room that could not be discussed aloud, even though it was the hot topic last year, in Kansas City.

So, I asked Paul Goranson about it. He has spent many hours trying to reconcile uranium import numbers from US customs data with what the EIA and China report. The US customs data alone shows that EUP imports from China continue to accelerate (more was imported in the first half of 2025 than for all of 2024). But, it is probably only the large utilities doing that.

China imports significant quantities of EUP from Russia, about as much as US utilities imported from China, according to US customs data for 2024. Since China has enough indigenous capacity for their own needs, it appears US utilities are continuing to use China as a brokerage for Russian EUP. Utilities claim the data is flawed. Paul agrees there are errors, but has learned how to correct and interpret the EIA data.

One example, is how EIA and utilities report purchasing Australian uranium, while none is shown in US customs reporting. This is because utilities take delivery outside of the US and change its origin designation to the country where it's converted and enriched, usually France. This is illegal for Russian EUP above the section 232 limits, but so easy to hide.

Why is this important? Because Russia does not buy uranium from the Americas. They have lower-cost sources from their neighbors, which they then convert and enrich and sell as EUP to the US and Europe. What they don't sell directly to Western utilities now goes through China. The end result is that American uranium miners continue to be screwed.

Moreover, inventories of EUP at larger US utilities is bigger than what is declared publicly. So, even though global production is still less than demand and Russian imports are "banned" by Canadian maritime sanctions, many Western utilities have still managed to accelerate EUP shipments from Russia/China and therefore still have significant inventories!

A special Thank You to Paul Goranson for sharing his import data! Paul does not necessarily endorse all of my opinions on uranium.

Drew DeWalt (General Matter) made some comments in a panel that reinforced my suspicion that they use the Ubaryon electrochemical enrichment process. Their parent company (OKAPI) is working on uranium mines in the US and Canada and General Matter is probably something like Silex's GLE subsidiary in the US. But, Ubaryon will never be a major competitor to laser enrichment technology. If it worked well, heavy water would not be so expensive.

I also discussed the current situation with Dustin Garrow (Deep Yellow). Dustin is also still pessimistic about the continuing lack of investment in uranium mining, "Building new mines is the really huge problem long-term."

Dustin thinks that the traditional nuclear utilities are going to be left behind because of their unwillingness to invest in the fuel supply chain. Big, behind the meter data center projects are being built around the utilities by tech companies with very different cultures and appetites for risk. Dustin attends some conferences that I miss, like the World Fuel Market. He quoted Malcolm Critchley (CEO at ConverDyn), who recently stated, "Still nothing much is really happening."

Honeywell just completed the spin-out of ConverDyn as Solstice ($SOLS). It's interesting that UF6 is not even listed as a product on their new website, even though it is about 12% of revenues and hopefully they are going to expand Metropolis Works soon? Any announcement on that will be bullish for the miners.

#Uranium $CCJ $SLX.AX $SOLS @GoransonPaul

21

19

114

26,990

26 Oct 2025

TNA Summit 2025 - Part 1

The Texas Nuclear Alliance Summit was twice the size this year at 700 attendees in Austin. I talked to so many people and ate the best BBQ in the world all week!

We started with a tour of the test reactor at the University of Texas Pickle Research Center, where I got my first blue pulse experience while standing over the reactor core water!

4 control rods moved out slowly, then Bamm! The fifth rod popped out and back in a second via a solenoid.

No dosimeter, boots, PPEs, radios, body scanners or cameras. Just full-on, Cherenkov radiation baby!

It looked similar to this reactor:

x.com/GovNuclear/status/1935…

It's hard to appreciate fuel rods until you've seen the energy they contain up-close and personal.

Take your Comanche Peak and stick it, Vistra!

Robert Bryce (Energy Writer) and Ray Rothrock (a long-time Venture Investor and board member at Centrus) gave a great but sobering presentation about the huge SMR opportunity and the huger obstacles. It was a rarely expressed but needed perspective that voiced many of my concerns. Ray said, "this always happens". An obvious opportunity attracts a lot of money and too many players. The main innovations are financial to mitigate risk, not the technologies. Ray is invested in 14 SMR vendors and expects a big "winnowing out", soon.

Robert explained the enrichment bottleneck and fuel shortage problems. Ray mentioned how hard it is for Centrus to find EUP for their customers every quarter, even for 2-3 years out. And he said it will take 5 years to build the centrifuge cascade (once they actually start). He did not define how many centrifuges that would be. Ray talks to many SMR vendors and the biggest worry they have is fuel supply. I pieced this together some time ago, but it was great to finally hear it explained on a stage.

Robert also explained how nuclear control rods require the same rare-earth metals used for magnets. Uranium and rare-earth mining are closely linked in many ways. The supply chain challenges go way beyond uranium and copper.

They said the STP is now the cheapest power source in South Texas. Vogtle is already the cheapest power in Georgia and between Vogtle 3 and 4, their power cost dropped about 30%. This mirrors the huge drop in costs in the 1970's due to "industrial learning".

But, building SMRs is not going to move the needle. We need bigger scale, like AP-1000s, but no one wants to go first, they explained.

Singing the Reddy Kilowatt song was a great way to close!

Paul Goranson is a mining consultant now and will speak at the NEI Fuel Forum in Charleston, next week.

He said uranium mining projects are accelerating due to easier permitting now in the US, but it might not last.

It's surprising that Springfields (UK) is still not being expanded, but Cameco's priority is their domestic conversion plants in Canada.

Several important IPO's are likely to happen soon, including Holtec, X-Energy and Honeywell's spin-out of Converdyn. The latter should finally drive investments to expand the Metropolis Works conversion capacity.

#Uranium #nuclear @pwrhungry @GoransonPaul $CCJ

WATCH: It's not every day you get to see a test reactor pulse!

7

8

69

13,437

26 Oct 2025

TNA Summit 2025 - Part 2

We had a lot more participation this year from uranium miners, such as UEC, EnCore and Laramide. Amir Adnani got an extensive interview.

Judge Merrifield (a former NRC Commissioner), patiently answered my questions about the mounting challenges to the regulatory monopoly of the NRC. He says some attorneys do believe the military can/should bypass NRC regulation to deploy SMRs on military bases, assuming that they never sell the produced power, commercially. There is also the new multi-state suit against the NRC that alleges federal agencies do not have jurisdiction over micro-reactors. Everyone wants to preserve the NRC's "gold standard" reputation and trust, but the situation is changing fast and NRC staff are not even at their desks during the current federal government shutdown.

John Borland, (Director of Widelity and former USSOCOM Innovation Chief), provided some guidance on the panel discussing national security. He said, "Whether this will become Pele 2.0 or Janus, I highly encourage everyone to watch that closely" because there is a lot of momentum around re-looking at the regulatory bodies. US military bases are too dependent on diesel supply. It cost lives in the Gulf War.

Aalo Atomics, another SMR start-up in Austin, recently shifted their fuel type to 5% LEU (supplied by Urenco), instead of HALEU (UZrH), which was their original plan. Their design is a modular sodium-cooled micro-reactor. The field of HALEU designs keeps getting smaller while the total number of start-ups is still growing.

Another major trend is "Nuclear-Ready". Build a gas-fired power plant that can be upgraded to nuclear sometime later by "just dropping in the nuclear island". I'm skeptical but that's the plan for several start-ups. I think this is how Oklo plans to meet their 2027/28/29 completion date promise - with a "Nuclear-Ready" gas-fired power plant. SMRs are supposed to be modular, right?

Jake Jurewicz (Blue Energy) detailed how the Nuclear Ready approach enabled financial support earlier for them, following the Venture Global model, instead of relying on tax or rate payers.

I think many players recognize that the US should be doubling the number of large reactors at existing sites, but those owners are not stepping up, so this has enabled a lot of creative risk mitigation strategies with SMRs designs. But, what they missed are the fuel supply problems because smaller reactors generally require higher-enriched fuels.

The high point of the conference was probably Rick Perry discussing Fermi America. It was big on attitude, but small on the details.

They claim they will build four (4) AP-1000s, simultaneously, along with a lot of gas-fired and solar, also! "All of the above" and at record breaking speed for nuclear builds, about the speed at which the Hoover Dam was built in the 1930s.

The local, state and federal support for Fermi is impressive and suggests maybe this lines up. But, they don't seem to know that they should already be ordering the turbines, transformers and nuclear fuel, yesterday. What they did do first, is get a public listing - $FRMI.

Recent comments from Chris Wright imply data centers will also be built simultaneously, next door.

Locating Fermi beside the Pantex plant seems brilliant. Perry says it's all there - land, water, fiber trunk cables, grid, airport, rail, local support, military security and plutonium. He says it's about national security and implies the military will be their first customer.

Can Amarillo, a city with a population of 250K, really become the epicenter of 4 GW of new nuclear power, with accompanying data center and AI talent in 6 years?

This will be exciting to watch, practically from my backyard. I see Fermi as a race between the states and an outright war between big nuclear and SMRs. If Fermi proceeds on schedule, it will make many SMR designs look unnecessary, at least in the US heartland.

The AI boom and SMRs have interesting, circular dependencies. SMRs are needed to provide credibility that AI's power needs will be met, and SMR vendors need the big premiums big tech is paying to bootstrap the capital investments needed for clean power.

Maybe this can develop into a synergy of industries given enough time. But, the Fermi project suggests the opportunity window for some small reactor designs is closing. Once the next few domestic AP-1000s get financed, some small reactor vendors are likely to get shaken-out and left with niche applications like military bases and industrial process heat.

5

4

50

5,805

8 Oct 2025

I've got my travel plans set for the remainder of 2025:

Texas Nuclear Summit - Austin 10/16

NEI Uranium Fuel Seminar - Charleston 10/28

The Fertilizer Institute - Charlotte 11/11

USNIC - New Nuclear Capital - NYC 12/2 (online)

CG - Global Uranium Equity Summit - NYC 12/9

Maybe too much focus on #nuclear and #uranium? Perhaps, but it feels necessary right now.

3

14

1,820

29 Sep 2025

I attended the DataCloud conference in Austin last week. This was primarily the folks who build data centers and fiber cable installations. Business is great, of course, and it was crowded.

This is one of the few industry conference sectors seeing excellent attendance and many copy-cat conferences are popping up across the US.

The huge topic is their power grid constraints. So, I assumed everyone would want to hear about the return of nuclear power and the TNA Summit, which is next month, just 2 blocks down Cesar Chavez Street?

Well, not so much.

Anytime I take a step away from nuclear industry people, it's still hard to find interest in nuclear, even in a technical and engineering crowd that really, really needs the power!

I didn't want to believe I was getting the same old questions about nuclear waste and proliferation. So, you know Oklo's plan is to build lots of small reactors that run on spent nuclear "waste". Right? "Oh! Really?"

DataCloud reinforced my view that the big tech investments into nuclear projects are largely an extension of solar and wind virtue-signalling, while bigger money is going to build gas-fired power and much of it behind the meter (like what Elon Musk already did in Nashville). With this plan, it makes sense to start with announcements of projects with names like "The Crane Clean Energy Center".

Big Tech has gambled that the public will accept new nuclear (because it takes so long to build), but they also have to look credible to investors expecting AI growth which wind and solar can not handle.

It seems like walking a tight-rope, but the open question of new nuclear build times provides them cover, for now.

#Nuclear #Uranium #SMR

1

2

21

3,979

28 Sep 2025

I sold 2/3 of my large stake in Silex Systems, last week.

I've been a champion of Silex and GLE since 2021, when I started accumulating the shares and writing how the EUP bottleneck restrains the uranium miners.

This is the first time I have sold Silex. I'm still bullish long term, but macro events have convinced me to move more to cash.

Silex is up because of rumors of possible DoE grants and equity stakes in uranium enrichment companies that are likely coming soon. I hope so. But, such funding will be divided amongst Centrus, BWXT and others.

It's unfortunate, but I don't expect an Australian company can ever get the level of infatuation from the market that Centrus, Lightbridge, BWXT, UEC and UUUU enjoy. But, the DoE rumors provide a good exit and I hope to be back in 2026.

It is gratifying to hear @DoombergT and others talking now about the conversion and enrichment bottleneck and Secretary Wright's determination to fix the domestic fuel supply chain. But, as Wall Street learns how long it will take to build this infrastructure, I'm looking for impatience to return.

#Uranium $SILXF $SILXY $LEU $CCJ $LTBR $BWXT

12

2

52

5,964

14 Jul 2025

An important power struggle for the future of US nuclear is becoming public. President Trump's executive orders precipitated a meeting that detractors are characterizing as a "hostile takeover" of the NRC. Anonymous sources claim they are demanding the NRC now "rubber stamp" applications already reviewed by the DoD or DoE.

And Trump fired Christopher Hanson, an NRC Commissioner with no explanation. Can he do that? Was Hanson an anti-nuke? Yes, and Hanson was appointed by anti-nuke bureaucrats in sheep's clothing.

Surprise! Trump is following through with another item he said he would do, fix the NRC.

What many forget is that the NRC was hijacked by anti-nukes for decades. They weren't blatant about it because the OBidens claimed to be pro-nuclear. But, the NRC was the gatekeeper that blocked all domestic builds, which also crippled advanced nuclear globally.

There is also a multi-state lawsuit progressing which claims the atomic energy act of 1954 never gave the feds authority to regulate SMRs, because they are small.

Trump may yet save the US nuclear industry, despite itself, but it won't be pretty and it won't be reported truthfully. Most writers today are still in denial about the 12 profoundly wasted years and they don't know history.

#uranium #nuclear #SMR

eenews.net/articles/doge-tol…

6

6

51

3,719

11 Jul 2025

Don't miss this excellent #Uranium update from Bloor Street Capital. The conversion and enrichment problem is mentioned a few times, plus the EUP imports from China continue.

x.com/BloorStreetCap/status/…

7 Jul 2025

Join host @JamesConnor1999 along with Guy Keller, Scott Melbye and Per Jander for our #Uranium Strategy Session and if you can't make it Live, no prob, check it out 24/7 on our @YouTube channel. Register bit.ly/4lEfRS7

5

26

2,503

12 Jun 2025

Steffan (@UnoMasReactor) has been hosting a great new series of recordings on Spaces about #uranium miners and the whole fuel supply chain for #nuclear power. His perspective is on retail traders and investors in this space and it should not be missed by anyone holding these stocks!

x.com/UnoMasReactor/status/1…

10 Jun 2025

4

3

30

2,714

12 Jun 2025

$OKLO shares jumped 29% yesterday! Why?

Was it the "news" of another Notice of Intent to Award (NOITA) from the Eielson Air Force Base, in Alaska? It seems so, but a 29% jump on old news? This deal was announced 2 years ago and the NOITA is really just being re-issued and it's still not actually a done deal, either. The 2 year delay was because they discovered military contracting regulations that require competitive post-bidding negotiations. They didn't know about that?

Was the jump because of President Trump's new executive orders? Maybe. The executive orders are great. But, they are not specific to Oklo. Oklo doesn't even build the sort of large reactors that are described by the orders. The orders will cut through some of the bureaucracy to build new nuclear on federal land, such as an Air Force Base. But, no one was protesting the Eielson AFB build site.

Oklo's actual problems are they still need their first license from the NRC for their Aurora reactor and fuel designs and a HALEU fuel supply.

Maybe the jump was because of a new (paywalled) article in Barron's yesterday, titled "Oklo Stock Is Upgraded to Buy. It’s About Nuclear Fuel, Says Analyst"

It's about Seaport Research Partners' thesis on Oklo, which says their plan to recycle spent fuel is an advantage worthy of an upgrade to "Buy" with a $71 target price:

"Oklo has the ability to “self-source its nuclear fuel given sufficient capital, regulatory approval, and access to SNF"

Well, perhaps in 5 years. Oklo does plan to build their own fuel foundry to initially down-blend and then later recycle spent fuel as an eventual substitute for HALEU.

But, there are several other (still private) ventures that actually have more advanced designs for recycling spent fuel, like Curio, Moltex, Metatomics and SHINE Technologies. Orano has been doing it for decades.

This is a very nascent industry in the US, but some of these companies will eventually be selling recycled fuel to Oklo's competitors, or they could be acquired for a lot less than Oklo's $9 billion market cap.

Oklo was granted the nuclear fuel for their first reactor at the INL (from down-blending) and fuel for the AFB will come from the DoD's stockpile. But, the third and fourth Auroras will be a problem.

And Oklo just announced another $400 million in share dilution this morning!

Perpetual dilution is also part of their plan. Oklo will need a lot of that because this amazing little company (120 people) will do everything themselves. They don't need banks, utility customers or fuel suppliers. Just perpetual Wall Street money. Oklo will become the Rosatom of Silicon Valley. Guaranteed to succeed by executive orders!

x.com/ClayDMontgomery/status…

10 Feb 2025

$OKLO achieved "Meme Stock" status last week with a $5.8 Billion valuation. It's reminiscent of Tesla, with a market capitalization higher than all of it's peers, some of which actually have experience building nuclear reactors, unlike Oklo. What's so special about Oklo?

Oklo is unique in so many ways it's difficult to compare. Like X-Energy, Oklo won't sell reactors. They plan to finance, build and operate all of their nuclear plants themselves. Except, Oklo is financed with perpetual dilution of publicly-traded stock. Oklo is open about their plan to continually issue more shares. But, the risks are compounded by their very unique reactor and fuel designs. It's an understatement to call their plan bold. It's a Mars-Shot, funded through public shares.

Oklo was the company that impressed with their early application to the NRC in 2020. But, it was rejected because they hadn't quite understood the details of the process. It took 2 years to find that their application was incomplete. So, what did they do next? Go public with a reverse merger!

As I've written many times, SMR start-ups have two major problems, HALEU supply and the NRC. Oklo's choices of such a novel reactor design (Aurora), plus using recycled and HALEU fuel, will multiply their problems. The new DoE Secretary, Chris Wright (who was on Oklo's board along with Sam Altman), can't help much because the DoE does not control the NRC and has only very limited HALEU supply.

Because Oklo's reactor (Aurora) uses fast neutrons, they can get more power output with less fuel. It can also destroy long-lived actinides in spent fuel and convert more of the fertile uranium into fissile U235.

That could help bypass the conversion and enrichment bottleneck that plagues the industry. That sounds great. But, there are reasons breeder reactors have not been commercialized before, at least in the US. And it's not entirely Jimmy Carter's fault, BTW. Although, it's hard to excuse such shortsightedness from a graduate of the US Navy's nuclear program.

Oklo's reactor and fuel designs are very novel or FOAK (first of a kind). Aurora is a compact, sodium-cooled fast reactor that uses uranium-zirconium metal fuel enriched to almost 20% (HALEU), supercritical CO2 power conversion and underground containment. This design builds on the Experimental Breeder Reactor-II and space reactor legacy military programs from the 1960s. The engineering concepts are solid, even admirable. But, the NRC did not exist then and there are many parts of Aurora's design that the NRC has little experience with. NRC's advanced reactor team is currently about 10 people and there are at least 20 SMR vendors currently vying for their time. So, the NRC will have to staff-up and learn how to work on Oklo's applications.

To say the NRC is the problem is an over-simplification. Their new commissioners will help, but Congress will have to help too, and quickly. There is bipartisan support for nuclear, but will they fund growing the NRC rapidly to enable so many new reactor and fuel designs? And will that support include fast-breeder reactors, like Aurora? There are dozens of new designs and start-ups vying for the attention of NRC's very limited staff. I think the more novel SMR designs have distinct regulatory disadvantages and Oklo's Aurora is perhaps the best example of that.

Oklo's projections assume no delays and HALEU costs of about 1/4 of current market pricing. They assume that either Centrus Energy will get 12,000 new centrifuges built quickly, or they can purchase HALEU from ASPI in South Africa or Tenex in Russia. Transporting 20% enriched uranium requires Category 2 security, an expensive step from Category 3, used for LEU today. I suspect they would have to hire the US Navy to do that, but the legal framework for that does not exist.

So, will Centrus get those centrifuges built and running in time for Oklo's plans? They don't even have a construction start date, because Congress has not funded that, yet. Each 15 MW Aurora requires an initial fuel load of 4,750 Kg of HALEU. Centrus is currently producing about 900 Kg of HALEU per year, which the DoE allocates to various SMR start-ups, not just Oklo.

Oklo received a site use permit for the first Aurora to be built in Idaho and an allocation of 5 metric tons of HALEU, enough to start this first 15 megawatt SMR.

They claim it will begin operating in 2027, yet they have not even submitted the COLA (combined license application) to start construction, yet. Oklo seems to assume they understand how the major reforms at the NRC will proceed better than anyone and that they will be accommodated quickly.

Assuming their first COLA is approved, they also need a separate fuel license. For that, Oklo must qualify their recycled, metal HALEU fuel, a type that has never been used before in the US, commercially.

It gets worse, fuel qualification could require changes to Aurora's design, which would mean repeating the COLA application. Oklo also intends to submit subsequent COLAs for additional reactors by early 2026, even before their first COLA is likely to be approved. They assume these will be approved in just 7 months, because of a new rule that promises to allow that.

Oklo's plan to make new fuel by recycling spent fuel and adding some HALEU is admirable. It's a contrarian plan that flies in the face of the decades-old narrative that spent fuel is an insurmountable problem. This could also help work-around the conversion and enrichment bottleneck problem that has most of their competitors stymied.

To this end, Oklo just announced a partnership with Lightbridge to fabricate their fuel and this partnership is propelling both company's stock higher. But, Lightbridge has a tiny market capitalisation and much more conservative management than Oklo. I have recommended Lightbridge stock repeatedly over the past year because it will be an acquisition target.

Lightbridge has expertise and patents for making metal fuel, but recycling spent fuel was not previously part of their plan. Aurora is designed specifically for metal fuel, so this alliance makes sense, technically. It's also seems to give Oklo some credibility and shows how undervalued Lightbridge is.

But, I suspect that the money crowding into this trade does not understand that Lightbridge does not have any supply of HALEU to sell to Oklo. And they certainly don't understand the delays that will come from the NRC process.

I am short $OKLO and long $LTBR and $SLX.AX.

#Uranium #Nuclear #SMR $LEU $CCJ

10

1

42

11,101

28 May 2025

Controversy is swirling around the DoE's Loan Programs Office. They shoved a record $93 Billion of public money out the door in the last 76 days of the Biden administration, after the election. That's twice the amount of the previous 15 years!

Due diligence was not done on many loans to start-ups that didn't even have a real business or a plan or a viable technology, according to Chris Wright, who testified on Capital Hill about reevaluating many loans, last week.

Jigar Shah, the man that oversaw the loan office, doesn't see a problem. He's still bragging about it on podcasts. They were actively encouraging anyone with a half-baked idea to get in on the theft. The only requirement was reducing carbon. If you didn't have a company and an idea, the DoE's ARPA-E would give you one, to get your loan application moving.

I've noticed how abandoned projects (like the Ivanpah solar collector in California), that received Billions in loan guarantees, quietly disappear off the DoE's website that allegedly tracks them:

energy.gov/lpo/portfolio-pro…

x.com/JigarShahDC/status/192…

youtube.com/watch?v=yC4goW2t…

2

1

20

2,191