Joined July 2011

- Tweets 5,581

- Following 1,273

- Followers 14,294

- Likes 1,595

1,629 Photos and videos

Pinned Tweet

May 11

Registration is now open for CI Live 2026 📣

Now in its second year, CI Live returns to Glaziers Hall, London on 4 November 2026, bringing together senior leaders from across the energy sector for a full day of market-leading insight, high-level debate and networking.

For a limited time, save 20% on your ticket with code SUPEREARLY20 at checkout. This offer is available until 4 June 2026, so don't wait too long.

Secure your place and super early bird rate: web-eur.cvent.com/event/5672…

447

Jun 11

Building a long-term view in the GB power market has become increasingly challenging in recent years.

As renewable capacity grows, electrification gathers pace and flexibility takes on a greater role in system balancing, the interactions between wholesale prices, Balancing Mechanism activity and Capacity Market revenues are shifting in ways that are increasingly difficult to interpret and plan around.

Our Renewables & Power Market Forecast and Flexible Power Market Forecast services are built to cut through that complexity and give investors, lenders and developers a clear, independent view of where the market is heading.

We’re offering a complimentary overview of our latest Q1 2026 forecast, covering:

- The long-term trajectory of GB wholesale electricity prices and the forces driving them

- How new sources of demand, including data centres, heat and transport electrification, are reshaping the capacity picture

- How revenues for renewable, co-located and flexible assets may evolve as market conditions change

- The shifting balance of value across wholesale, Balancing Mechanism and Capacity Market revenue streams

Request your complimentary overview using the links below.

Renewables and Power Market Forecast: cornwall-insight.com/l/11082…

Flexible Power Market Forecast: cornwall-insight.com/l/11082…

242

Jun 10

We’re excited to announce our first guest speaker for CI Live 2026 – the founder and CEO of the UK’s largest energy supplier and a global energy and technology company.

Joining us is: Greg Jackson CBE, CEO and Founder of @OctopusEnergy

Greg has built two giants worth billions – Octopus Energy and Kraken – and in 2024 was appointed CBE and named one of TIME magazine’s 100 Most Influential Climate Leaders. Operating across 20 countries, Octopus manages an £8 billion renewables portfolio, leads thriving businesses in EV leasing, heat pumps and solar, and has attracted over $3 billion in funding from international energy companies, pension funds and global investors.

CI Live returns to Glaziers Hall, London on 4 November 2026, bringing together senior leaders from across the energy sector for a full day of market-leading insight, high-level debate and networking.

For a limited time, you can save 10% on your ticket with code CIEARLYBIRD10 at checkout.

Reserve your place today: web-eur.cvent.com/event/5672…

219

Last chance to save 20% off CI Live 2026 tickets!

Our super early bird discount ends tomorrow, so there is just one day left to secure your place with 20% off standard ticket prices.

CI Live is back for its second year at Glaziers Hall, London on 4 November. More than 250 professionals joined us last year for a full day of high-level debate, market-leading insight and networking, and at CI Live 2026 we will get into the harder questions facing the sector around the GB energy transition.

Use code SUPEREARLY20 at checkout to save 20% before 4 June 2026.

Look out for some exciting speaker and agenda announcements in the coming weeks.

Reserve your place and super early bird rate: web-eur.cvent.com/event/5672…

272

The UK REGO market is under pressure from multiple directions.

Renewable generation capacity, ongoing market reform proposals and REGO pricing trends all shape how renewable generators understand and realise value from their assets.

On Tuesday 23 June at 10:00 AM, Cornwall Insight and Renewable Exchange are co-hosting a free webinar exploring recent REGO pricing movements, PPA market commentary and the impact of wider policy developments, including the Contracts for Difference scheme, on future REGO price trajectory.

Don't miss this opportunity to stay informed and register today: cornwall-insight.com/events-…

1

1

303

May 28

In case you missed it, our recent blog by Jacob Briggs explores why business electricity and gas costs continue to rise across every part of the bill, from the impact of geopolitical events on commodity prices to rising network charges and recent policy developments.

With our free webinar taking place next week on Wednesday 3 June at 10:00am, there is still time to secure your place and hear from our experts on the near-term impacts of recent wholesale market shocks, what is driving sustained cost pressures, the long-term outlook for business energy costs, and see a live demonstration of our new digital forecasting platform.

Read the Blog: cornwall-insight.com/insight…

Register for the Webinar: cornwall-insight.com/events-…

1

241

May 27

Bills are confirmed to be going up in July, not good news for consumers, but the more interesting question is what comes next. Tom Goswell, our Energy Supply Lead, was on @SkyNews this morning breaking down the @ofgem announcement, what to expect this winter, and why this moment is different to the Russia-Ukraine crisis.

1

445

May 27

Ofgem has confirmed that the July price cap will rise by 13% to £1,862 a year for a typical dual‑fuel household, reflecting higher wholesale costs linked to the conflict in the Middle East.

While this increase is unwelcome for billpayers, it comes at a point in the year when energy use is generally lower due to warmer weather. The more significant concern may be what lies ahead. Our current forecast for October indicates a further 2% rise on July’s cap, coinciding with falling temperatures and increasing demand.

We are still only days into the three‑month period Ofgem uses to assess the wholesale part of the October cap, so things can, and likely will, change. That said, even if the conflict were to end tomorrow, it would be optimistic to expect prices to return rapidly to pre‑conflict levels. Damage to infrastructure, ongoing supply chain disruption and reduced market confidence are likely to take time to resolve, meaning the impact on bills could carry on longer than many expect.

Read the full release here: cornwall-insight.com/press-r…

2

2

3

612

May 21

Ireland and Northern Ireland both set a target of 80% renewable electricity by 2030, both are behind schedule.

With conflict in the Middle East keeping energy security at the top of the agenda, the gap between ambition and delivery on the island of Ireland has real consequences, for households, businesses and the long-term cost of power across the SEM.

Our latest blog looks at exactly where the transition stands right now: generation, demand, storage and interconnection. Download here: cornwall-insight.com/insight…

If you want to go deeper, we're hosting a free webinar on the progress of the SEM renewable transition on 28th May – register here: cornwall-insight.com/events-…

1

1

329

May 21

Just over a week to go until our free webinar: Rising Costs, Shifting Risks: Understanding the Outlook for Business Energy Prices, on Wednesday 3 June at 10:00am.

If your organisation is grappling with rising energy costs and increasing complexity across wholesale markets, network charges and policy costs, this is a session not to miss.

Our experts will cover the latest forecast trends, upcoming key policy developments and a live demonstration of our new digital forecasting platform, with a Q&A session at the end.

Don't miss the opportunity to hear from our energy experts and gain practical insight to support your planning and decision-making.

Secure your place today: cornwall-insight.com/events-…

259

May 20

Consumer-led flexibility is evolving fast and the opportunities for electricity customers are growing.

Our latest blog sets out how electricity customers, from households to large businesses, can engage with flexibility markets today. It covers the shift from implicit flexibility through time-of-use tariffs to direct participation in system flexibility services, new market roles like the Virtual Lead Party, and why regulators and government bodies have signalled that demand-side flexibility must grow significantly to meet 2030 and net-zero targets.

We have also launched a new course, delivered by our subject matter experts – Understanding Consumer-Led Flexibility Opportunities – for those looking to understand the full picture and the routes to market to participate in flexibility services.

Read the blog: cornwall-insight.com/insight…

1

295

May 20

CI Live is back, and we're returning to London on 4 November 2026 with some big news: Evolve Energy will be joining us as headline sponsor, extending a partnership that started at our first Annual Conference last year.

Evolve were a founding sponsor of CI Live 2025, where 250 people from across the sector spent a full day in conversation about the pressures facing Great Britain's energy system. That they're committing to CI Live for both 2026 and 2027 says something about what that day delivered.

CI Live 2026 takes place at Glaziers Hall and will get into the harder questions facing the sector, how to push towards ambitious policy goals like Clean Power 2030 without losing sight of what it costs the people paying the bills.

Tickets are on sale now. Use code SUPEREARLY20 at checkout to save 20% before 4 June 2026: cornwall-insight.com/events-…

Read the full announcement here: cornwall-insight.com/insight…

249

May 19

Our final price cap forecast for July to September 2026 predicts the cap will rise by £209 to £1,850 a year for a typical household. That’s around a 13% rise from the current cap.

❓ Why are prices going up?

The main driver for the increase in our forecast is rising wholesale prices, which climbed sharply in February and March after US and Israeli missile strikes on Iran, and the subsequent retaliatory attacks, saw damage to Gulf energy infrastructure and the closure of the Strait of Hormuz, a shipping route for around 20% of global oil and gas.

A temporary ceasefire brought some calm to markets, but prices remained elevated throughout the observation window.

❓ What about prices heading into the winter?

While households will be understandably frustrated by a rise during the summer, the impact will be reduced as household energy usage typical falls during the hotter months. The bigger concern is October, when demand picks up again and current forecasts point to a similar cap level as July.

While the October cap will depend on how the Middle East conflict unfolds, even if the conflict were to end tomorrow, the physical damage to infrastructure, and lingering effect of disrupted supply, means a fall back to April’s price cap levels in the autumn looks unlikely.

❓ What is a "typical household" and how might this be changing?

To give people an idea of what an average household may be paying under the price cap @ofgem has devised Typical Domestic Consumption Values (TDCVs) for gas and electricity. Ofgem is consulting on a change to its TDCVs, to reflect the fact that average household energy use has fallen.

Cornwall Insight has therefore published two forecasts. If Ofgem adopts the lower consumption figures, the headline “average bill” could appear to rise by less - to £1,667. However, as the cap controls unit rates and standing charges, rather than the total bill itself, what households actually pay will depend on how much energy they use and will not be impacted by Ofgem’s “average bill” figure.

Read the full release here: cornwall-insight.com/press-r…

4

3

599

May 18

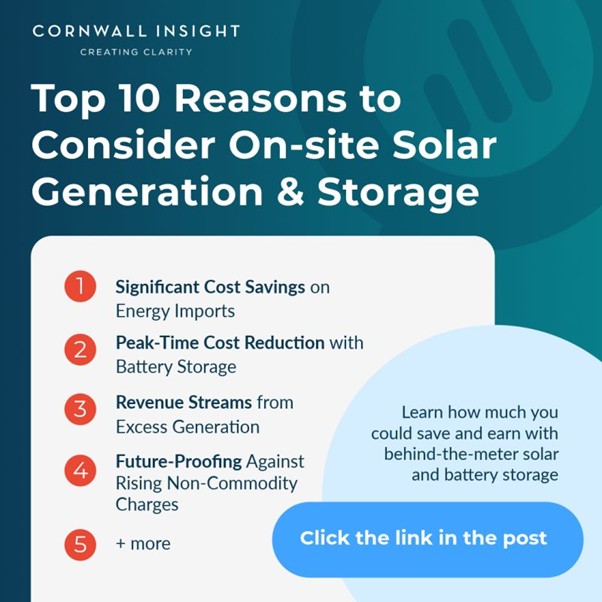

Energy bills are one of the biggest costs your board can't ignore right now, and on-site generation could be a way to achieve significant energy cost savings.

Policy charges and stubbornly high wholesale costs are rewriting the economics of on-site solar and battery storage faster than most finance teams have had time to model. We've pulled together 10 business cases for going on-site, plus the actual numbers on what a high-energy business could realistically save and earn.

The data is available to request directly through the blog.

Read the full blog here: cornwall-insight.com/insight…

Want the broader picture on where business energy prices are heading? We're running a free webinar on exactly that, register here: cornwall-insight.com/events-…

333

May 14

Business energy costs are becoming increasingly complex to navigate.

With wholesale market volatility driven by global events, alongside rising network charges and evolving policy costs, organisations are facing growing challenges when it comes to planning and budgeting with confidence.

Join us for our free webinar ’Rising Costs, Shifting Risks: Understanding the Outlook for Business Energy Prices’, on Wednesday 3 June at 10:00am.

The session will include:

- How recent wholesale market shocks are shaping near-term business energy costs

- The drivers behind sustained cost pressures beyond wholesale prices, including network charges and policy costs

- What upcoming policy developments could mean for your organisation’s energy strategy

- A live demonstration of our new digital forecasting platform

Register your place today to ensure your organisation has the insight it needs to manage energy costs with confidence: cornwall-insight.com/events-…

275

May 13

Our Head of Training Ed Reed joined @BusinessGreen and @SchneiderElec o dig into how businesses can build clean energy strategies in what is, frankly, one of the most complicated environments companies have had to navigate on energy costs.

Energy bills go well beyond the headline wholesale prices, as network charges, carbon reporting obligations, and procurement decisions are all adding up for businesses, download the webinar here: businessgreen.com/sponsored/…

If you’re interested in hearing more from Cornwall Insight, we're hosting our own webinar on 3 June looking at the outlook for business energy prices: from wholesale market shocks and incoming policy changes to what it all means for planning and budgeting. Register for the webinar here: cornwall-insight.com/events-…

1

299

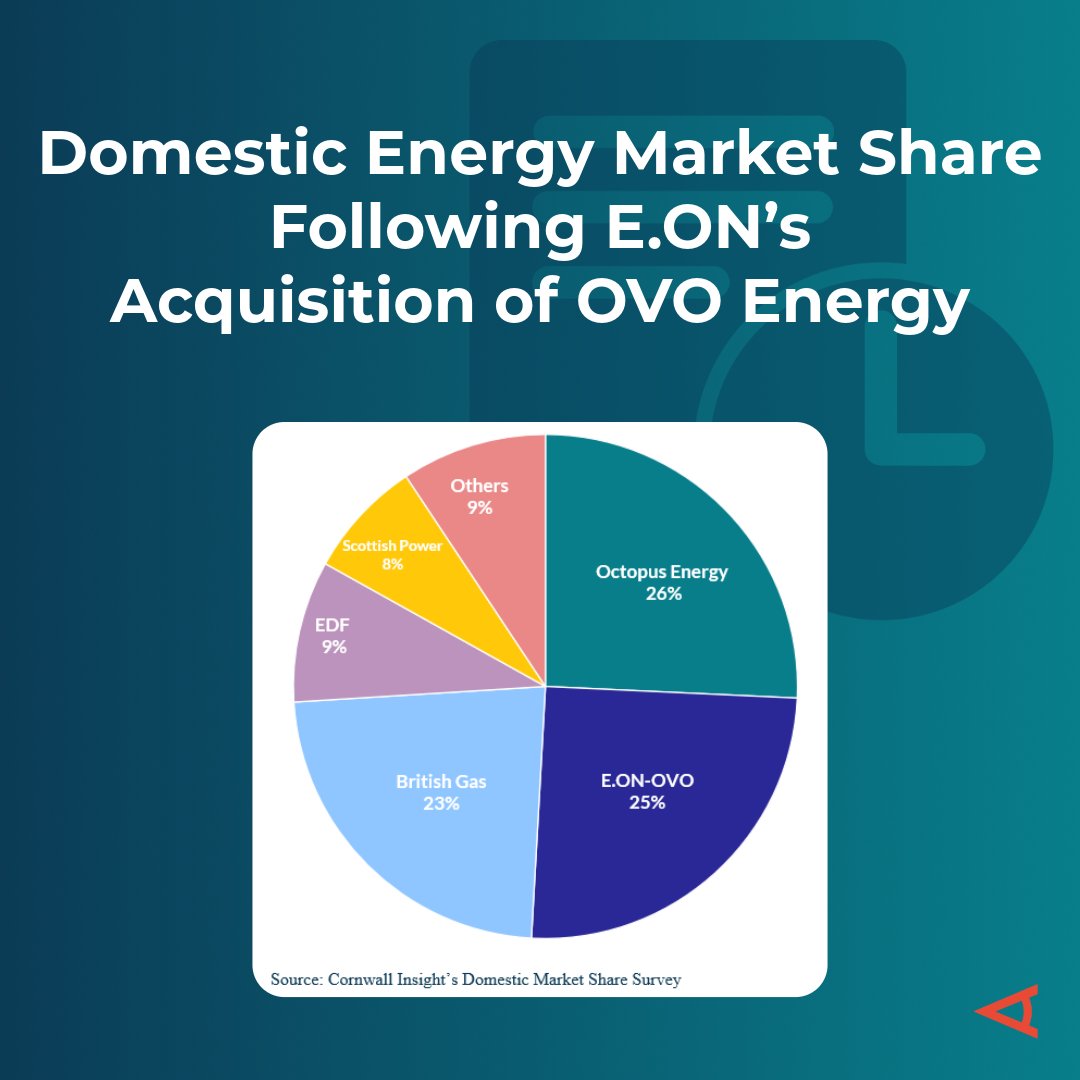

May 12

If E.ON's acquisition of OVO Energy gets the green light, Britain's household energy market will look quite different. We’ve crunched the numbers to show what that could look like:

🔷 How would market share change?

Our Domestic Market Share Survey puts the combined E.ON/OVO entity at around 25% of the market, which would make it the second largest domestic supplier in Great Britain, just behind Octopus at 26% - it’s very tight at the top of the market.

🔷 What share would the ‘Big Five’ control?

Six energy companies currently hold over 90% of the household energy market, this will fall to five if the deal completes, with the top three together accounting for close to three quarters of all supply.

🔷 Why do market share figures differ?

You might have seen different figures to ours on the E.ON/OVO deal. There's a reason for that.

Domestic market share can be measured in different ways. Cornwall Insight measures market share by the total number of electricity and gas accounts a supplier has on live supply, this means dual fuel households who receive both gas and electricity are counted as two accounts. By contrast, much of the coverage is using customer accounts, here a dual fuel customer is only counted once, regardless of how many fuels are supplied. Supplier rankings may differ depending on the metric being used.

🔷 Energy accounts or customer accounts - which matters more?

Neither approach is wrong, however, energy accounts are generally considered a more meaningful measure of domestic supplier scale. because they better reflect the number of supply points being served and the overall size of a supplier’s retail portfolio.

🔷 Where can I keep up to date with the energy supply market?

If you want to stay across how the supply market is shifting, our Energy Supply intelligence service has you covered, from proprietary market share data to pricing analysis and financial information – find out more and book a demo: cornwall-insight.com/product…

1

444

Is the island of Ireland's energy transition on track, and what does it mean for future prices and revenues?

With geopolitical tensions disrupting global commodity markets and the Single Electricity Market (SEM) reliant on imported fossil fuels, uncertainty around future energy prices is growing. Against this backdrop, the strategic importance of indigenous renewable energy is coming into sharper focus and the drive to accelerate renewable deployment is gaining momentum.

Join our free webinar on Thursday 28 May at 11:00am, where our independent experts will explore:

- Current status: The critical role of grid development and system flexibility in enabling progress towards our 2030 renewable energy targets

- Where prices are going: The long-term direction of SEM wholesale electricity prices

- Key drivers: Gas prices, demand growth and future generation build-out

- As well as an introduction to our enhanced SEM Power Market Forecast and SEM Flexibility Power Market Forecast

Don't miss this opportunity to hear directly from our experts and put your questions to the team.

Register Today: cornwall-insight.com/events-…

341

Apr 27

"Why is gas setting the price of electricity?" has gone from a niche industry debate to a question people are genuinely asking around kitchen tables, and with good reason.

Since gas prices spiked following the conflict in the Middle East, the pressure on electricity bills has been hard to ignore. The government has now put forward plans which aim to reduce how much gas can pull the whole market up with it.

Our analyst Alex Livingston has taken a closer look at the policies: how they are designed to work, and where the challenges are likely to be.

🔷 Read the blog here: cornwall-insight.com/thought…

For deeper analysis, Industry Essentials customers can access 'State versus Market: A Turning Point in GB Energy Policy' on CATALYST, examining the implications of this and Reformed National Pricing: catalyst.cornwall-insight.co…

Not yet a customer? A 14-day free trial gets you access to this piece and more, plus daily market updates: solutions.cornwall-insight.c…

443