Facilitating Global Investors' access to high-quality, high-growth credit products in Emerging Markets via tokenization. CM is the next-gen RWA marketplace.

Joined June 2024

- Tweets 938

- Following 52

- Followers 230

- Likes 1,126

2 Photos and videos

Pinned Tweet

2nd place at #StableHacks 2026 among 100 projects from 59 countries! 🏆

Being recognized by institutional giants like @aminabank, @solana, and @solstice_fi validates our mission to bring Brazilian credit on-chain.

Thanks @Tenity_global! 🚀

18

4

48

3,042

List #8 of my series of projects participating in the @solana Frontier Hackathon on @colosseum has arrived

I loved this list a lot for one reason and that is that I was surprised by the number and good projects from Brazil all closely supported by @SuperteamBR it is good to see how they come together to build great things

Special mention for @NOMADZxyz, an established project led by @ivan_nomadz that I have known and used for months, they are here to take a leap to excellence

Which country should I continue with? I would like LATAM or Spain

- @riptidesim : Replayable economic stress tests for Solana programs

- @Credit_Markets : Facilitating Global Investors' access to high-quality, high-growth credit products in Emerging Markets

- @OpenDevT : OPEN | Chrome DevTools for

Solana

- @arcane_finance : Compliance-ready privacy infrastructure for on-chain finance

- @AnemoneDefi : Pure IR Swaps on Solana

- @usesendsol : The future bank for Brazilians Dollar savings instant payments.

- @hivebits_io : An RWA project onboarding bees to the blockchain via DePIN

- @vayofinance : Bring onchain yield to your product with plug-and-play infrastructure

- @encrypt_xyz : Encrypted Capital Markets FHE on Solana

- @kaxisclub : RWA platform tokenizing Brazilian credit card receivables

- @uLendMe : Get a small advance to ship real work

- @zupyoficial : Social Loyalty for the real world. While cashback and miles reward spending

- @norafinancexyz : The Brazilian Real Stablecoin ecosystem with yield and onchain fx for Neobanks

- @traded_gg : The Onchain TCG Super App

- @NOMADZxyz : Solana travel app for booking stays with crypto

- @usekixa : Your agent, your rules. Create AI agents and own the permissions on Solana

A new list of aspiring projects for the @solana Frontier Hackathon by @colosseum has arrived and it doesn't stop, nice and promising projects are here in DeFi, RWA, Cosumer App, DePin, AI, Layers this is crazy lol

In this list what is your fav one and why?

Next list mainly Spanish and LATAN projects tag here your fav one

- @edulearndotfun : Incentivized Web3 AI Study Companion

- @myStableCorp : earn onchain. bank compliantly. built for the global web3 builder

- @Protocol01_ : Privacy infrastructure for Solana.

ZK-powered stealth transfers, shielded pools, and programmable payment streams

- @archade_io : The social layer for Pumpfun. Scroll, Trade, Post, Launch

- @aifinpay : The Payment Infrastructure for Autonomous AI

- @voutcomeengine : Trust is a resource. VRE is how you earn it. On-chain proof of who won

- @Artifacte_inc : The Sotheby's of Sol, aggregated RWA's, Gachas powered by @Collector_Crypt

- @usesendsol : The future bank for Brazilians, Dollar savings instant payments

- @yoursolanabuddy : Voice first hardware assistant that speaks Solana

- @paymento_io : Empowering wallets to become your business gateway

- @KRED_info : A reputation layer where KOLs earn trust through track records

- @captur_go : A people-powered network gathering real-time geospatial and location intelligence

- @agenttech : A programmable stack where agents transact across 14 chains, prove identity, and build commercial reputation

- @DefundsFinance : On-chain asset management Work with top traders or create your own fund,secured by Solana smart contracts

- @xplaceapp : The financial OS for your digital wealth. Spend without selling your assets

- @voicehavefun : Opinion Layer of the Internet, Screw gambling. Get paid for your hot takes

17

9

45

2,073

Credit Markets retweeted

Jun 4

StableHacks 2026 brought together some of the most thoughtful builders working at the intersection of stablecoins, institutional finance, and on-chain infrastructure. 🚀

What stood out wasn't just the quality of the projects, but how many teams arrived at similar conclusions around compliance, tokenisation, and the infrastructure needed to bring digital assets into regulated financial systems.

Congratulations to the teams recognised by the jury:

🥇 @ClearstoneAI

A KYC-gated lending framework that transforms real-world assets into compliant digital tokens designed specifically for institutional and banking counterparties.

🥈 @Credit_Markets

A platform tokenising Brazilian receivables into USD-denominated yield products on Solana, demonstrating how private credit markets can become more accessible through tokenisation.

🥉 @zettacapital00

A permissioned DeFi vault architecture for regulated institutions, embedding KYC, KYT, travel rule requirements, custody, and compliance directly at the protocol layer.

The innovation on display reinforced just how quickly the infrastructure around regulated digital assets continues to evolve.

#StableHacks #Stablecoins #Tokenisation #RWA #InstitutionalFinance #DigitalAssets #DeFi #AMINA

2

2

12

388

Credit Markets retweeted

Jun 2

💎 Congratulations to the winners of StableHacks 2026! 💎

After an incredible competition showcasing the future of institutional DeFi, tokenization, and compliant on-chain finance, we're excited to celebrate our top three teams

🥇 Clearstone Fusion — KYC-gated lending that wraps real-world assets into compliant "d-tokens," built explicitly for a bank counterparty. c.c Achim Huebl

🥈 Credit Markets — tokenizes Brazilian receivables into USD-denominated yield assets on Solana, via a custom vault standard. Emerging-market private credit, repackaged as institutional-grade yield. c.c. Lucas Britto

🥉 Zetta Capital — sophisticated RWA tokenization with async settlement. A permissioned end-to-end DeFi Vault for regulated institutions - KYC, KYT, travel rule and custody enforced at the protocol layer. c.c. Neil Batchelor

We're excited to follow the journey of these winning teams and look forward to seeing their solutions scale beyond the hackathon and into the broader financial ecosystem

Special thanks to our partners and jury for helping create a platform where innovators can build solutions to real institutional challenges.

➔ Main partners: @SolanaFndn , @AMINABankGlobal , @Solstice

➔ Other Partners: @keyrock , @FireblocksHQ , @SteakhouseFi, @SuperteamDE , @softstackHQ ⧉, @SIX, @kamino

Jury: ➔ Myles Harrison (Amina), ➔ Markos Theologitis (Amina), ➔ Philipp Vonmoos (Solana), ➔ Marcus Maute (Solstice), ➔ Ramzy Ali (Solana), ➔ Andreas Iten (Tenity)

A huge thank you to all participating teams, mentors, speakers, and partners who helped make StableHacks such a success.

4

4

32

1,091

Credit Markets retweeted

Jun 2

What a way to close out StableHacks 2026 🚀

Over the course of StableHacks, we saw teams tackle some of the industry's most important challenges across stablecoin infrastructure, tokenisation, real-world assets, compliant DeFi, and institutional adoption.

Congratulations to the winning teams Clearstone Fusion, Credit Markets, and Zetta Capital. 🏆.

We're grateful to our co-hosts @tenity_global, @Solana, and @SolsticeFi and partners @Keyrock, @Fireblocks, @SteakhouseFi, @SuperteamDE, @softstackHQ, SIX, @Kamino who helped bring the initiative to life and create a platform for the next generation of builders to showcase their work.

The future of digital assets will be built through collaboration between innovators, institutions, and infrastructure providers—and StableHacks demonstrated exactly what that can look like. 💪

#StableHacks #DeFi #Tokenization #RWA #Stablecoins #InstitutionalFinance #Web3 #CryptoValley

3

10

358

2nd place at #StableHacks 2026 among 100 projects from 59 countries! 🏆

Being recognized by institutional giants like @aminabank, @solana, and @solstice_fi validates our mission to bring Brazilian credit on-chain.

Thanks @Tenity_global! 🚀

18

4

48

3,042

The correct tag is @AMINABankGlobal @solsticefi . Sorry! Too much happiness. Lol

1

2

92

Credit Markets retweeted

Jun 1

Today is Money Legos Brazil.

Together with @norafinancexyz, we’re bringing together leaders across stablecoins, neobanks, RWAs, DeFi, payments, and financial infrastructure to show how Brazil is not just adopting onchain finance, it is helping reinvent global financial infrastructure.

From Pix-native distribution to BRL stablecoins, embedded DeFi, RWAs, and the rise of neobanks, Brazil is becoming one of the most important laboratories for the next generation of financial products.

We’ll be joined by our partners:

@NexaFinance, @rivool_finance, @4payFinance, @koresolutions_, @Credit_Markets, Âmbar, and @KASTxyz.

We’ve already crossed 150 registered attendees, so we highly recommend arriving early to ensure a smooth check-in and a great experience.

See you today at Money Legos Brazil.

Where Brazil’s financial infrastructure meets the onchain future.

11

30

1,427

Credit Markets retweeted

May 29

Our trip to Switzerland was an absolute success! From high-impact meetings to diving deep into the ecosystem at the @CVConf_ @thecryptovalley, it’s been incredibly productive. 🇨🇭

✨ Big updates are coming soon—keep your eyes on @credit_markets! 🚀

4

2

17

909

May 26

This is a real Alpha!

May 25

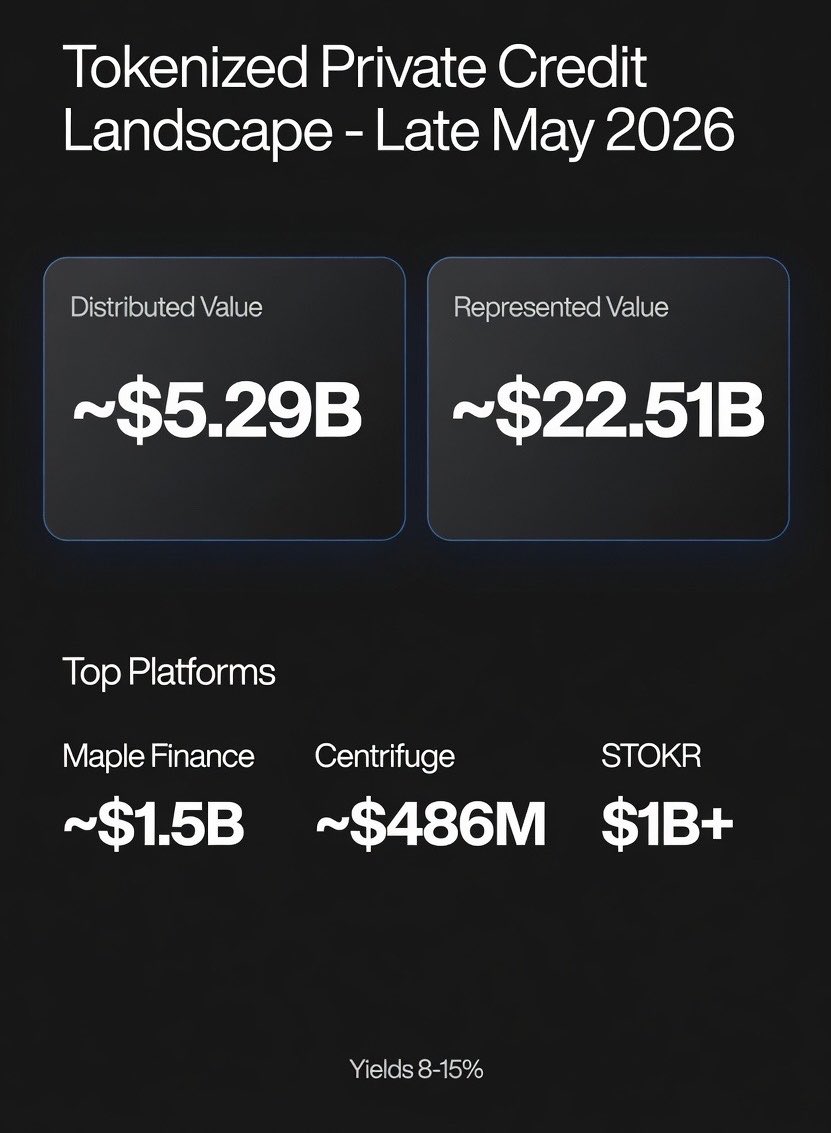

Here’s a quick snapshot of the current Tokenized Private Credit landscape as of late May 2026.

Private credit remains one of the largest and most active categories in tokenized RWAs. It brings real yield from actual loans and credit products (invoices, SME lending, trade finance, HELOCs, etc.).

Key Metrics (rwa.xyz data):

• Distributed Value: ~$5.29B

• Represented Value: ~$22.51B

• Thousands of assets and holders across the category

Top Platforms by value:

• @maplefinance Currently leading with ~$1.5B. Strong in onchain institutional credit pools (syrupUSDC & syrupUSDT)

• @STOKR Surpassed $1B in total tokenized asset volume, building capital markets infrastructure on Bitcoin’s Liquid Network

• @centrifuge ~ $486M, foundational infrastructure player

• Others active: @HastraFi (PRIME), @Securitize powered deals

Established Players:

@maplefinance continues to lead in onchain institutional credit with meaningful AUM and consistent loan originations.

@centrifuge remains core infrastructure for tokenized real world credit invoices, receivables, and structured products like the Janus Henderson Anemoy AAA CLO fund. It has strong multichain reach and a solid track record.

@goldfinch_fi also maintains presence, especially in emerging markets credit.

Emerging & Regional Builders to watch:

Several newer and regional players are bringing private credit onchain:

• @Credit_Markets — Focused on tokenized LATAM Private Credit

• @KamuiFinance — Active in tokenized private credit and institutional RWA yield strategies

• @Factorcx — Tokenized private credit

• @empower_fi — Tokenized Brazilian credit

• @Stra_protocol — Tokenized Brazilian credit

• @NusaHarvest — Indonesian agricultural lending (credit angle)

More projects are surfacing from hackathons and specific regions, especially LATAM and Southeast Asia SME-focused credit plays.

Yields in this space have historically ranged between 8–15%, depending on risk and region (often higher in emerging markets credit).

While many deals are still somewhat permissioned or geared toward accredited/institutional access, the infrastructure layer is clearly maturing. Recent activity also includes partnerships that aim to connect onchain yield with more regulated distribution rails.

This is the current state of tokenized private credit.

I’ll keep tracking and sharing updates as new deals, pools, and builders emerge.

1

2

104

May 25

First up: we are officially competing in the #FrontierHackathon from @colosseum

And we are very happy to see our name on this list! Tks @michael2xl !!

LFGOOOOOO!!

May 25

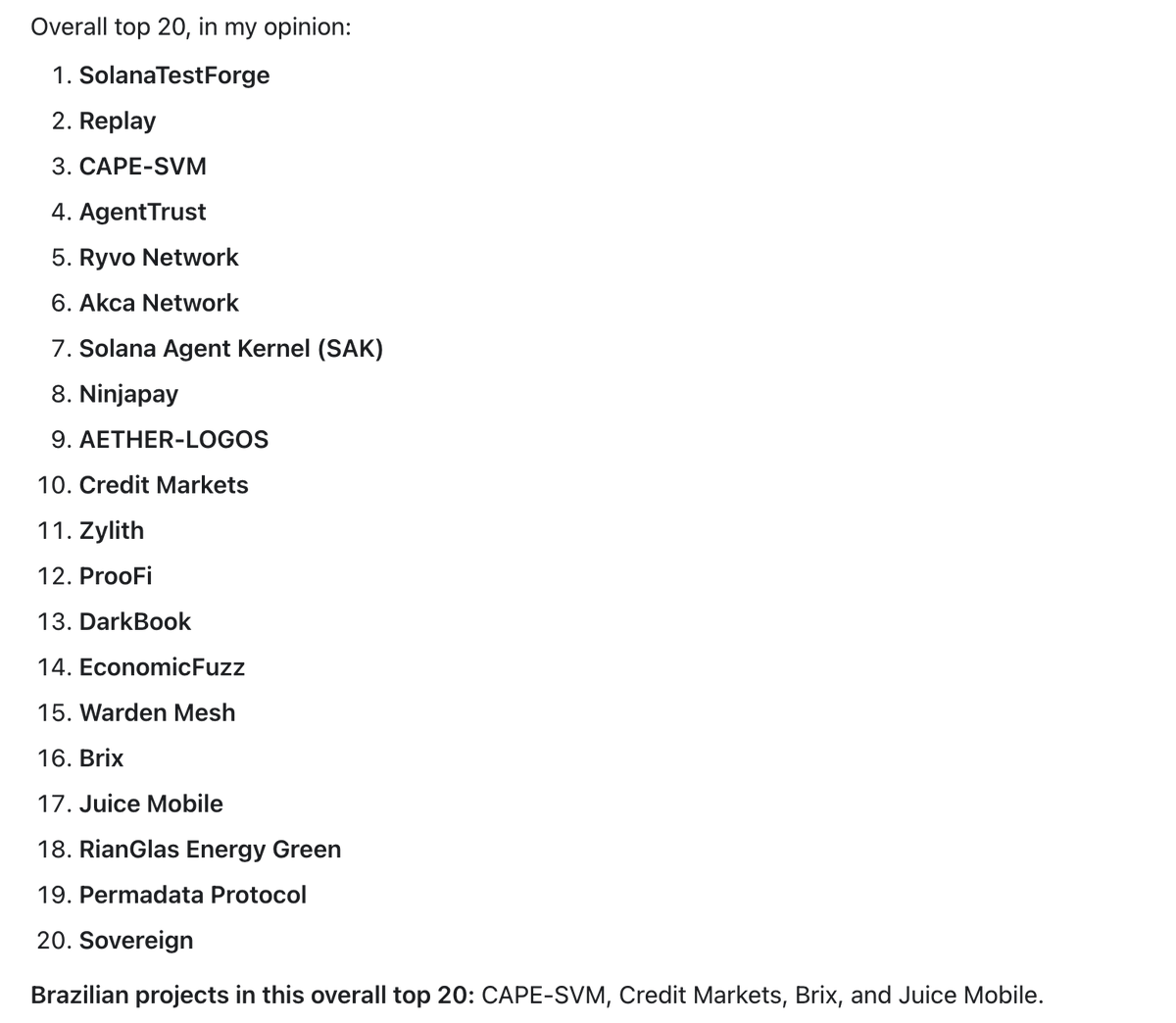

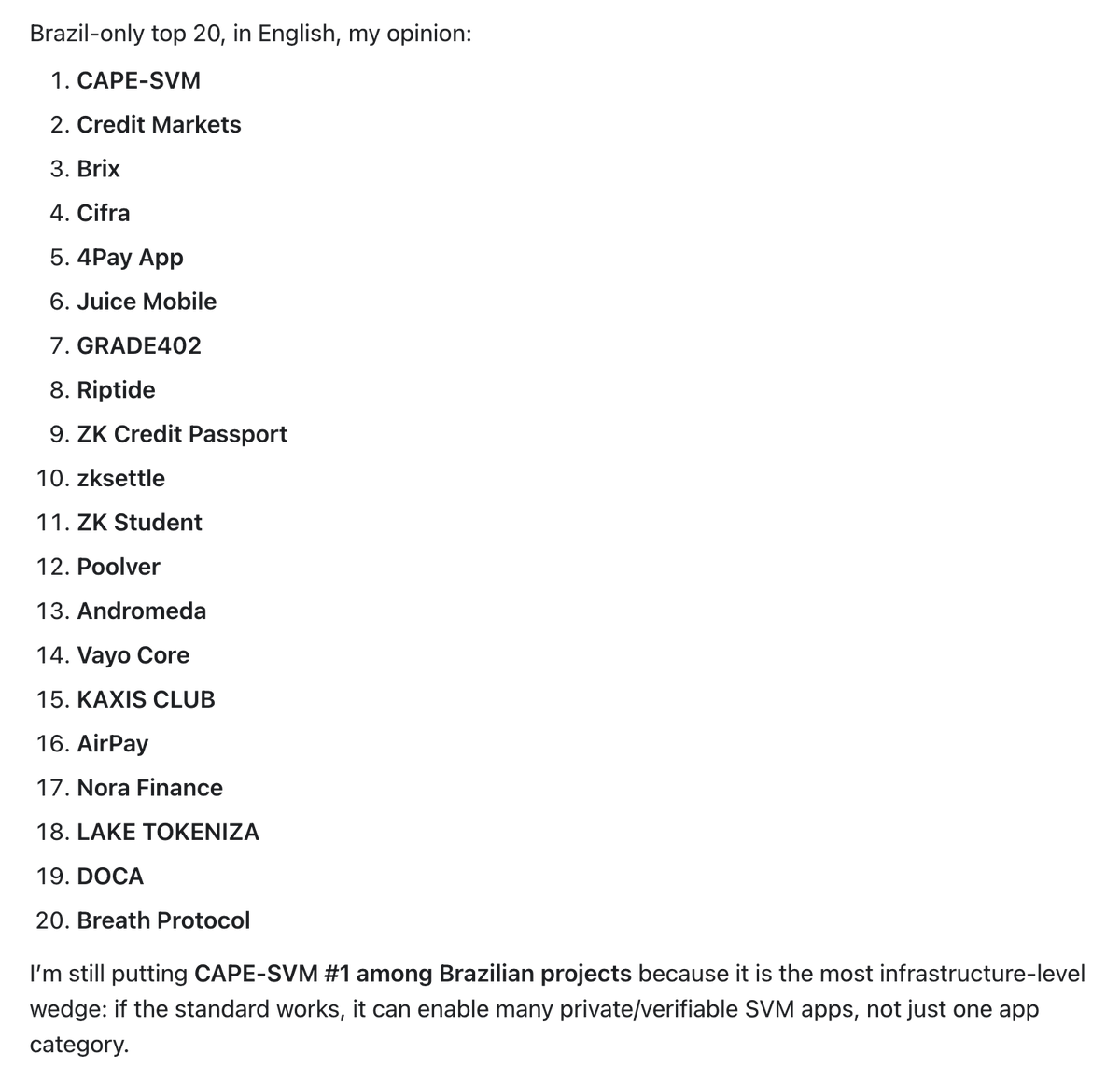

Download 2858 projects from @colosseum Frontier.

I asked the top 20 to the GPT 5.5. Funny fact, it gave the top 3 to my project globally and top 1 in Brazil.

GPT: "I’m still putting CAPE-SVM #1 among Brazilian projects because it is the most infrastructure-level wedge: if the standard works, it can enable many private/verifiable SVM apps, not just one app category".

3

215

May 25

After a few months in deep focus, we are back to share what we have been doing!!

1

3

52

Credit Markets retweeted

May 14

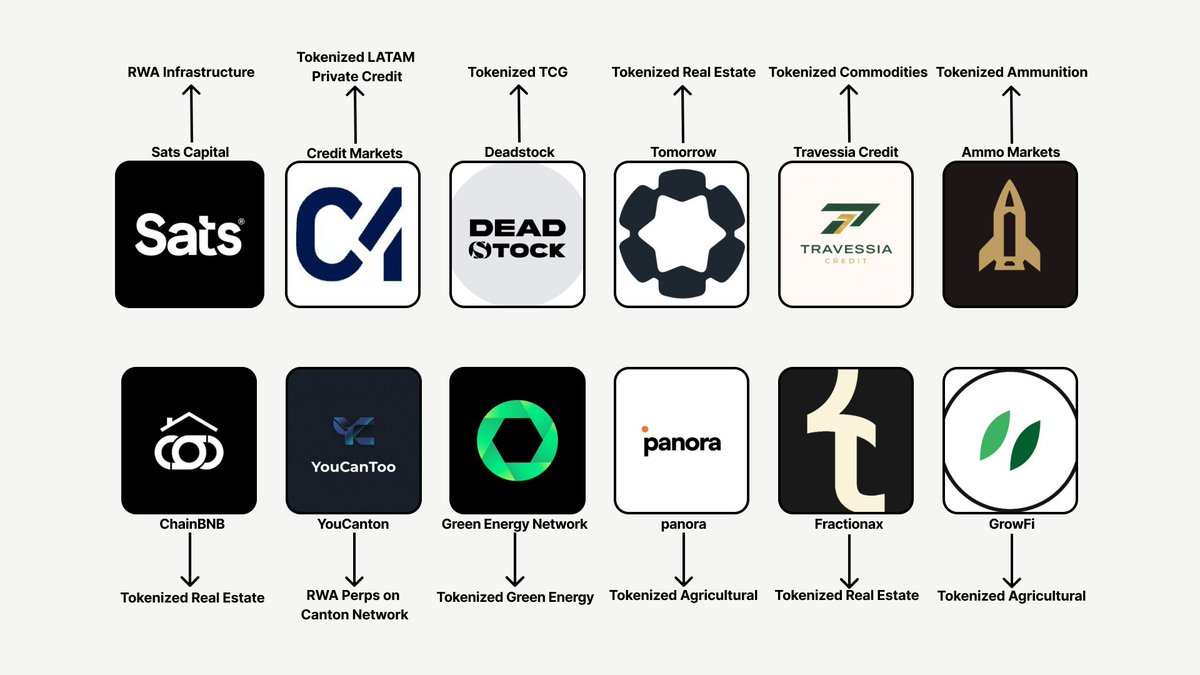

I found early RWA projects weekly so you don’t have to PT.17

@Credit_Markets - Tokenized LATAM Private Credit

@higrowfi - Tokenized Agricultural

@fractionaxapp - Tokenized Real Estate

@officialpanora - Tokenized Agricultural

@you_canton - RWA Perps on Canton Network

@ChainBNBapp - Tokenized Real Estate

@ammomarkets - Tokenized Ammunition

@TravessiaCredit - Tokenized Commodities

@satscapital_ - RWA Infrastructure

@GENPowered - Tokenized Green Energy

@deadstock_app - Tokenized TCG

@OnchainEstate - Tokenized Real Estate

[ Bookmark for later read🔖 ]

May 7

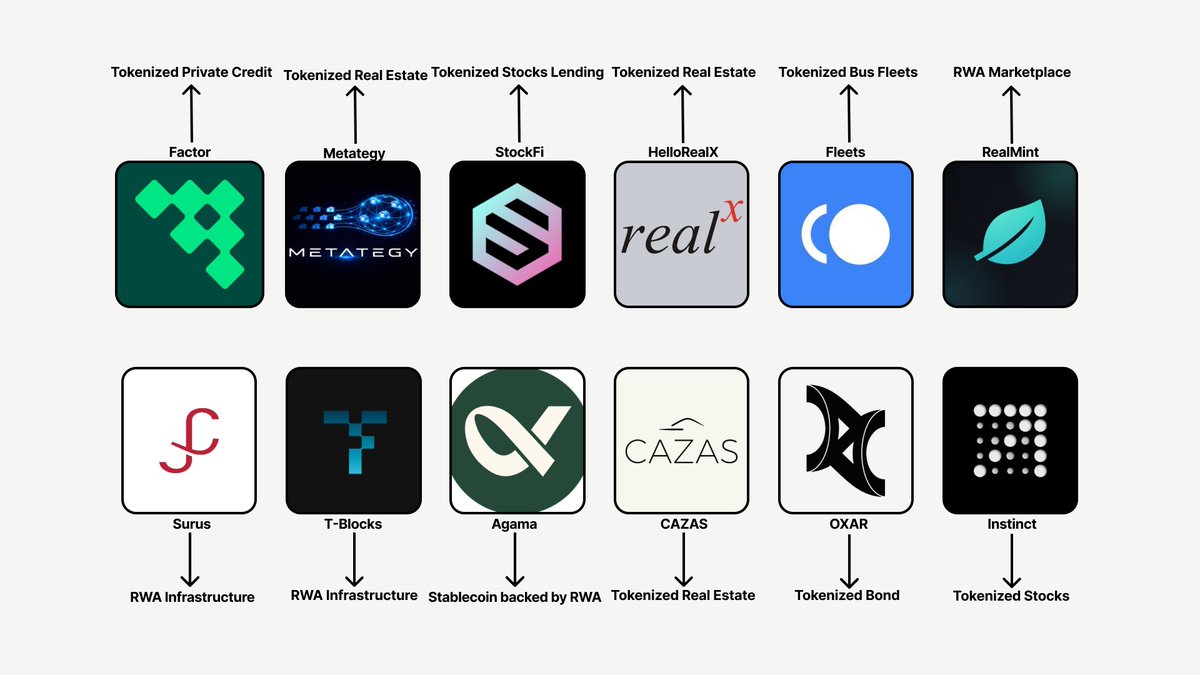

I found early RWA projects weekly so you don’t have to PT.16

@Surus_io - RWA Infrastructure

@tblocks_io - RWA Infrastructure

@agamafinance - Stablecoin backed by RWA

@CazasHQ - Tokenized Real Estate

@the_oxar - Tokenized Bond

@instinctxyz - Tokenized Stock

@realmintio - RWA Marketplace

@usefleets - Tokenized Bus Fleets

@Metategy - Tokenized Real Estate

@Factorcx - Tokenized Private Credit

@hellorealx - Tokenized Real Estate

@stock_fi - Tokenized Stock Lending

@Metategy - Tokenized Real Estate

@Factorcx - Tokenized Private Credit

[ Bookmark for later read🔖 ]

27

14

119

13,929

18 Dec 2025

Institutional capital needs more than apps.

It needs liquidity layers built for scale.

Keel emerges as a key onchain capital allocator and catalyst for RWAs, stablecoin liquidity, and credit, hand in hand with Credit Markets. 🌱

18 Dec 2025

Institutional money is sitting on the sidelines waiting for the first movers.

Cian Breathnach (@crocdundalk) of @keel_fi explains why on-chain balance sheets may be what finally kicks off large-scale tokenization & what is on the horizon.

Watch here 👇

youtu.be/XX-_5KvMF04

6

592

16 Dec 2025

Onchain local currencies are foundational for real credit markets in LATAM.

Our CSO helps you understand why BRL, MXN, and COP stablecoin flows are key to building lending, settlement, and FX rails that actually match how the region operates.

See the full report 👇

16 Dec 2025

We’ve just released a new report on Latin America local stablecoins 🇧🇷🇨🇴🇲🇽

The report analyzes stablecoins pegged to BRL, COP, and MXN, covering supply, transaction volumes, DeFi activity, and on-chain usage.

All on-chain data was built using @Dune.

Full report 👇

iporesearch.ventures/

8

300

14 Dec 2025

Tokenization going from future plans to infrastructure.

Collateral, settlement, and compliance are finding their ways onchain, enabling entirely new credit markets to become possible, especially in regions where capital is scarce and spreads are high.

14 Dec 2025

Big institutions are embracing tokenization.

This week brought new regulatory progress and real-world adoption as the world’s largest companies begin to move onchain.

Here’s what you need to know 👇

1️⃣ CFTC pilot allows for tokenized assets to be used as collateral in derivatives markets.

The first-of-its-kind U.S. program allows BTC and ETH, along with USDC and other payment stablecoins, to be used as collateral in derivatives markets.

coindesk.com/policy/2025/12/…

2️⃣ Ondo Finance to invest $200M in State Street Investment Management’s tokenized fund

Ondo Finance joins with State Street Investment Management and Galaxy Asset Management in plans for a new private tokenized liquidity fund bringing traditional cash management onchain.

thestreet.com/crypto/investi…

3️⃣ BMW uses JPMorgan blockchain system for automated FX transfers

JPMorgan Chase & Co's Kinexys platform automatically transfers euros from BMW's Frankfurt accounts when dollar balances in New York drop below a certain threshold.

bloomberg.com/news/articles/…

4️⃣ The SEC formally closed a confidential Biden-era investigation into Ondo

Regulators are shifting from enforcement-first approaches toward frameworks that support modernized market infrastructure. The path is now clearer for tokenized Treasuries and tokenized equities to become core components of U.S. capital markets.

ondo.finance/blog/tokenized-…

5️⃣ SEC approves DTCC to support tokenized equities

The SEC granted permission to the DTCC to custody and recognize tokenized equities and other real-world assets onchain. DTCC can now offer tokenization services on pre-approved blockchains for three years.

bloomberg.com/news/articles/…

4

203

11 Dec 2025

Tokenization is inevitable.

11 Dec 2025

Every major institution is rapidly embracing tokenization.

3

127

Credit Markets retweeted

11 Dec 2025

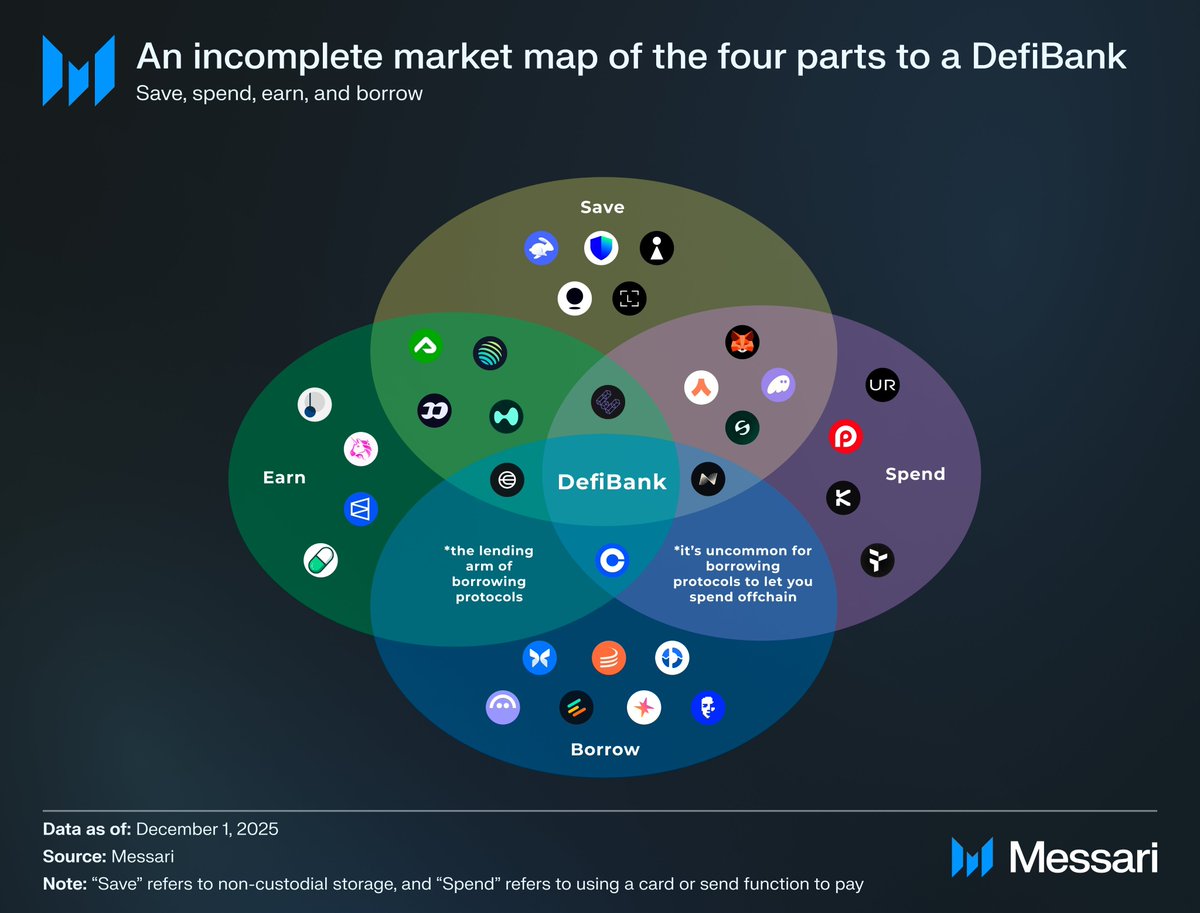

We’ve largely solved save and spend.

Earn still has a long road ahead. And borrow, especially unsecured barely exists.

At @Credit_Markets, we’re building the rails for diversified, safer RWA yield.

9 Dec 2025

spent a ton of time brainstorming with @0xCryptoSam these past few weeks on what crypto neobanks will look like. so excited to see his piece come to fruition!

fundamentally, crypto neobanks like fintech neobanks before them transform our 4 fundamental relationships with money - how we save, spend, earn, and borrow money.

but whereas fintech neobanks innovated the frontend while keeping the trad banking backend (via fdic partner banks), crypto neobanks change that backend itself, by putting it onchain and on stablecoin rails, while keeping the slick mobile UI from fintech neobanks.

this is perhaps the key difference between "DeFi Banks" and fintech neobanks or even centralized exchanges.

i also really really loved this diagram - one of the neatest market maps that i've seen that captures how different crypto neobanks are moving from their initial wedges across the entire stack, esp. in a vertical where everyone converges to the same functionalities.

will also share my full neobank piece soon... 👀

2

2

5

315

9 Dec 2025

DeFi doesn’t need more synthetic yield. It needs real cash flows from real businesses.

By bringing LatAm receivables (assets that are proven, scalable, and impactful) onchain, Credit Markets allows for better yields for lenders and better financing for providers.

Everyone wins.

5

86