Joined February 2018

- Tweets 2,709

- Following 1,843

- Followers 219

- Likes 7,671

22 Photos and videos

Pinned Tweet

25 Sep 2025

Super impressed with everything the @mintlayer team has been building over the last few years. 👏 They've been consistent and they're in it for the long term.

Mintlayer is definitely NOT vaporware. It's gud tek that the crypto industry desperately needs...

Mintlayer is the one true BTC L2 (and L3)... 🙌🤩✨🌈

Current price is not a fair reflection of the superior value that @mintlayer brings to BTCFi. It's true potential will be shown in the upcoming alt season. Mark my words: Mintlayer will fucking MELT faces in alt season... 🫠💎🙌🚀🪐

23 Sep 2025

1

1

7

417

Enigma (Viking) retweeted

Jun 13

Don’t worry about Elon becoming rich with his own money.

Worry about politicians becoming rich with your money.

2,223

36,823

158,834

1,476,022

Enigma (Viking) retweeted

Jun 14

You are given the opportunity of a lifetime to buy an asset with a 38% power law CAGR, which is currently trading at 0.45x trend.

You DO NOT opine on X that "I think its going lower".

You DO NOT let Macro analysis of Luke Groman, who has been consistently wrong the last 3 years, dissuade you.

My 10 satoshis.

73

69

1,201

53,335

Enigma (Viking) retweeted

Jun 5

YOM Mainnet is Live.

The world's first decentralized cloud gaming network is now live on @avax .

40 publishers. Sub-12ms latency. No data centers. No downloads.

YOM is live. The instant play network is real.

Contract Address: 0xb6314518b61b4864162c7aE7fdc36261e0A14C4b

Welcome to the post-cloud era. 🤝

1,207

4,191

1,572

92,568

Enigma (Viking) retweeted

Apr 19

Everyone is racing toward AGI. Most are running in the wrong direction.

The future isn't a single god-like model controlled by a handful of closed labs. It's millions of specialized agents, coordinating and evolving together, on a foundation that's open, verifiable, and owned by the people building on it.

Our executive team on what’s next. $OPG TGE April 21 👇

448

262

1,197

3,244,496

Enigma (Viking) retweeted

May 22

BREAKING: Kevin Warsh officially takes oath as new Federal Reserve Chair.

Warsh says "the real work begins now" and promises to build a Fed where "the best people can do their life’s best work."

He says the US faces major challenges, but inflation can fall, growth can stay strong, and the coming years could bring "unmatched prosperity."

59

180

974

40,017

Floki and TokenFi are launching massive new campaign with New to The Street

We are launching a new two-month national media campaign with NewToTheStreet and Fintech TV, bringing both Floki and TokenFi in front of traditional finance audiences through national TV interviews, Times Square advertising, YouTube distribution, press coverage, and social media amplification.

More specifically:

- Two executive interviews filmed at Fintech TV Studios in the NYSE.

- Airing on FOX Business and Bloomberg TV.

- More than 219 million U.S. households in combined broadcast reach.

- Times Square visibility through the Reuters 42nd Street Billboard.

- YouTube distribution through New to The Street's 4.4M subscriber channel.

- Targeted placement toward accredited investors and family offices.

The goal is simple: bring the $FLOKI and $TOKEN story to the audiences shaping the next phase of finance.

ALT Floki and TokenFi are launching massive new campaign with New to The Street

66

280

727

63,903

Enigma (Viking) retweeted

May 20

Underrated layer for AI is transaction privacy.

@Mute_swap is building the privacy layer for AI agents transacting onchain

40

40

279

21,810

Enigma (Viking) retweeted

May 20

Let’s be honest

The Fed Shouldn’t Overreact to an Oil Shock

The Federal Reserve has already made one major policy error this cycle. It shouldn’t compound it with another. The Fed should not raise rates!!

During Covid, the Fed invoked its emergency powers and effectively wrote a blank cheque for a massive fiscal expansion, absorbing a surge of government debt on its balance sheet. It did so in ways that aligned remarkably neatly with the priorities of the Biden administration, turning “independent” monetary policy into a willing partner for a de facto experiment in modern monetary theory.

In practice, the central bank validated a fiscal programme that the White House could not have financed on such a scale without a compliant Fed. That experiment in ultra-loose policy, coupled with aggressive deficit spending, produced the inflation that politicians tried to dismiss as “transitory.” The surprise was not that prices rose, but that so many officials claimed to be surprised when they did.

Today’s inflation scare is different. The recent uptick is being driven primarily by an energy shock linked to the Iran conflict, not a new wave of stimulus or credit excess. Before that shock, core inflation was clearly trending lower, and the underlying data pointed toward steady disinflation rather than a re-acceleration. In other words, the heavy lifting was already happening beneath the headline numbers.

That is why calls for the Fed to “get ahead of inflation” with another round of rate hikes are so misguided. Treating every adverse supply shock as a demand problem leads to the same reflexive response: tighten policy, prove your toughness, hope the models validate the move after the fact. But an oil spike that will wash out over months does not require the same reaction as a broad, credit‑fuelled boom.

Kevin Warsh will likely take over the Fed with one or two more hot inflation prints still in the pipeline as the energy shock feeds through. The temptation, in markets, in politics, and inside the institution, will be to use those numbers as cover for another hike. That would be a mistake. If core disinflation resumes as expected once energy normalizes, additional tightening now would mean squeezing an economy that is already cooling on its own.

The lesson of the Covid era should not be that the Fed must always do more, earlier, and with greater drama. It should be that misdiagnosing the shock leads to the wrong tool and the wrong dose. The last cycle’s mistake was to underprice the inflationary impact of fusing fiscal expansion with emergency monetary policy, in a way that blurred the line between technocratic judgment and partisan convenience. The risk now is the mirror image: overreacting to a temporary supply shock and locking in unnecessary damage to growth.

A Warsh Fed will have an early chance to show that it can tell the difference between Powell’s political legacy and a genuinely independent central bank, and between reflex tightening and the discipline of letting a temporary shock pass.

13

37

166

9,093

May 17

AI is cool until you realise it can't be trusted. Especially for AI agent payments/transactions, trustless AI becomes crucial to see behind the black box...

*Trustless AI is the future. The future is now with OpenGradient...

May 16

OpenGradient has processed over 1M LLM inferences through x402-powered infrastructure since launch.

Inference requests are settled through batched onchain payments, enabling scalable execution for verifiable AI systems.

Verifiable AI systems are beginning to operate at meaningful scale.

1

35

May 14

It is DONE...!!! 🥳🥳🥳 Clarity is coming... ✅

May 14

The crypto market structure bill has PASSED the Senate Banking Committee with a bi-partisan vote!

Historic day for crypto and for the future of digital assets in America. Grateful for the countless hours from lawmakers and staff to strengthen this legislation. Big improvement from where we were in January on rewards, tokenization, DeFi, and CFTC authority. I'm proud we stood up for our customers in that moment, and the bill is better because of it.

Looking forward to a bipartisan law that cements the US as the world's crypto capital. Let's get CLARITY done.

15

May 13

Kevin Warsh is confirmed as the new Fed chair. Let's see if his approach of low short rates gradual QT can send markets higher for longer (less bubbly).

Today @SenateGOP, along with the Democrat who put country before political ideology, confirmed @POTUS's nominee Kevin Warsh as the next Chairman of the @FederalReserve. Chairman Warsh will usher in a new day at an institution that is in need of accountability, sound policy guidance, and the renewed sense of purpose to help guide our economy. His chairmanship opens the door and lays the groundwork for every American family to build and grow in the world's greatest economy.

39

Enigma (Viking) retweeted

May 12

This is exactly the problem we started OpenGradient to solve.

Agents are already transacting, hiring other agents, moving money.

The verification layer can't be an afterthought, it has to come first.

OpenGradient

38

20

119

7,564

Enigma (Viking) retweeted

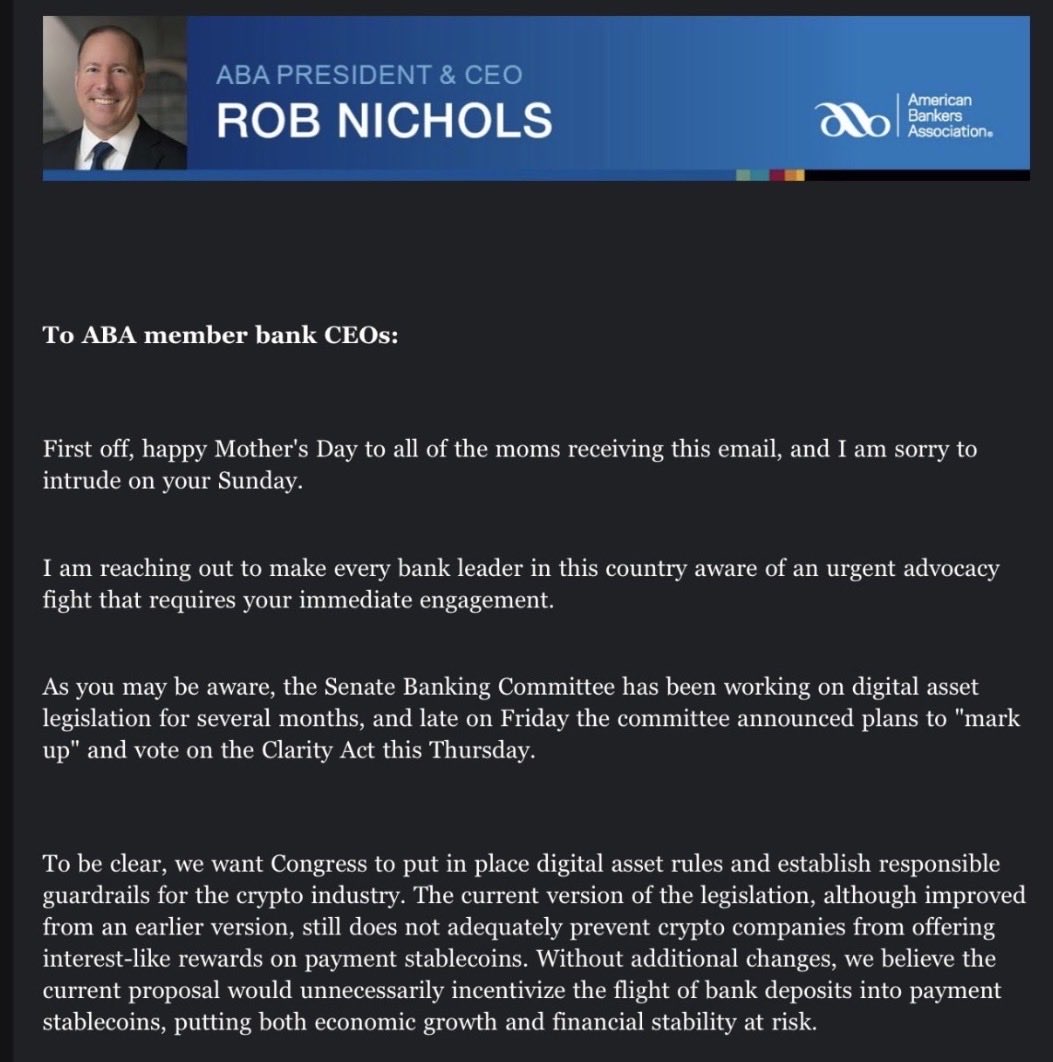

May 11

🚨 The banking cartel is in full panic mode. 🚨

While Americans were celebrating Mother’s Day with their families, the CEO of the American Bankers Association sent a frantic alert to every bank CEO in the country, demanding “immediate engagement” to lobby Senators and kill stablecoins that would finally let everyday Americans earn real yields on their own money.

This line in the letter sticks out: “we believe committee members may not be fully aware of the risks to the economy by the stablecoin loophole.” That’s both intellectually dishonest and simultaneously demeaning. First, there is no “loophole.” This entire issue was litigated during the GENIUS Act debate. @BillHagertyTN worked tirelessly on this issue and this statement is an insult to his and others work.

For decades, these banks have treated your deposits like their personal piggy bank, paying you next to nothing while lending YOUR money out for massive profits and executive bonuses.

During the Biden era, these same banks worked hand-in-glove with @SenWarren and her allies to debank Americans, including President Trump’s own family. They shut down accounts of conservatives, patriots, and anyone who dared challenge the regime, all while regulators applied pressure under schemes like Operation Choke Point 2.0. It wasn’t about risk. It was about political control.

Now that innovative stablecoins threaten to break their monopoly and give you actual financial freedom? They’re running to Congress again, screaming about “threats to economic growth and financial stability.”

Translation: Protect the racket at all costs.

The Senate Banking Committee votes on landmark crypto legislation this Thursday.

As a member of that committee, my message is clear:

Hands off the people’s money. Let Americans choose real competition and better returns. No more shielding Wall Street from the future. The banking elite’s days of rigging the system and debanking their political enemies are over. Innovation, freedom, and the American people will win.

I’m voting to break the cartel.

454

2,453

8,548

931,801

Enigma (Viking) retweeted

May 1

AI is cool… until you can’t verify it.

That’s the problem OpenGradient (OPG) is fixing.

Verifiable on-chain AI inference infrastructure.

@OpenGradient

Learn More:htx.com/en-us/views/feed/det…

14

12

68

7,824

Enigma (Viking) retweeted

Apr 21

Most AI runs in black boxes. You can query a model, but you can't verify what actually ran.

OpenGradient changes that.

4,000 models hosted

2M verifiable AI inferences

500K proofs and attestations

All onchain. All provable. Join us in accelerating on-chain AI.

1

3

33

9,301

Enigma (Viking) retweeted

Apr 21

OpenGradient is now live on Virtuals Protocol.

Every Virtuals agent can now run on verifiable AI compute. Models onchain, inference cryptographically proven, payments settled through x402. The intelligence behind agent decisions is no longer a black box.

Trade (OPG): app.virtuals.io/virtuals/720…

38

43

342

29,934

Enigma (Viking) retweeted

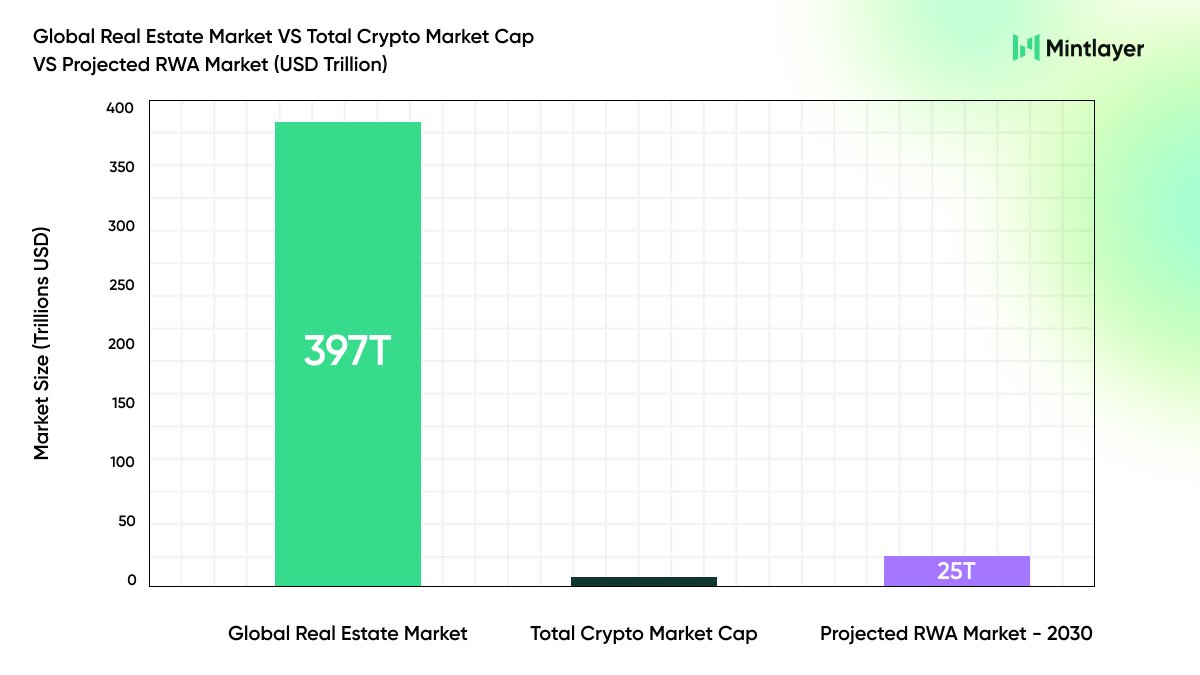

Apr 15

When you step back and look at the scale of global markets, the imbalance becomes clear. Real estate alone exceeds $397 trillion, while crypto represents only a fraction of that, barely one percent of a single asset class, highlighting just how early we still are.

Hundreds of trillions across real estate, bonds, commodities, and private credit remain off-chain. This isn’t a limitation, it’s one of the LARGEST opportunities in finance today.

Tokenization is the bridge, unlocking accessibility, liquidity, and interoperability in ways traditional systems haven’t achieved.

With RWA adoption up over 260% in early 2025 and institutions like BlackRock and Goldman Sachs already building in this space, even a small shift on-chain could redefine markets.

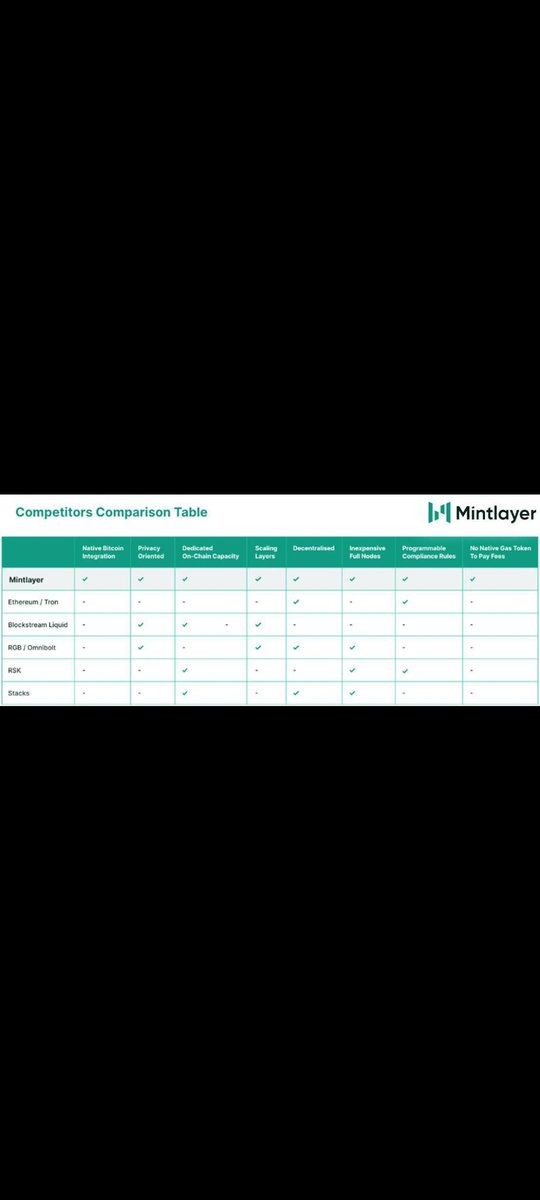

Mintlayer.com has built the infrastructure to support that transition bringing real-world value onto $BTC's most secure settlement layer.

And this is only the beginning. 🥂

12

23

78

2,448

Enigma (Viking) retweeted

Apr 12

The last administration drove away the digital asset industry. It’s time to welcome them home with clear rules of the road.

Pass the Clarity Act.

630

1,163

8,898

506,219