I trade stonks and bryptos // Tweets are not financial advice.

Joined February 2018

- Tweets 2,392

- Following 2,163

- Followers 1,223

- Likes 603,270

283 Photos and videos

𝐑 𝐀 𝐒 𝐂 𝐀 𝐋 retweeted

7 Oct 2025

$IREN's Most Likely Partner for SW1: OpenAI

For a site as large as SW1, the fastest path to monetization would be partner and use cashflow to continue to expand it’s full owned CSP when Vera Rubins come out in 2027 on SW2 and future sites/expansions that @FransBakker9812 is finding clues for such as (2). @litigious_dulce explains the insane economics Vera Rubins and how Blackwells economics will pale in comparison (3) so it’s important for IREN to time their self-bought chips for Vera Rubins. I will explain why IREN-OpenAI makes sense for both parties.

OpenAI:

The first key fact is that a critical part of DeepSeek’s breakthrough was their direct use of PTX bypassing some CUDA functions. The second piece of the puzzle is AMD’s hardware benchmarks always look great but their interface layer, ROCm, is far inferior to CUDA for full utilization of the hardware. Now if DeepSeek is able to write custom PTX, OpenAI can modify/customize ROCm to create an optimized version for their inference. For OpenAI, this will save them a fortune over Nvidia GPUs for inference where horizontal scaling makes sense, and it’s evident why OpenAI announced to buy 6GW of Instinct GPUs starting with 1GW in H2 2026.

No power constrained neocloud $CRWV, $NBIS could take the risk to buy that many AMD GPUs and tie up all their power. $NBIS doesn’t even have close to 1GW much less 6GW. Heck even, AMD knows that OpenAI is basically the only customer in 2026 at this scale and is willing to give up to 10% of their company to AMD if the whole 6GW of their GPUs is eventually purchased. OpenAI will need a Neocloud to deploy the 1GW in H2 2026. Even if NBIS does managed some how manage to pull off 1GW from somewhere, signing it entirely away would mean giving up their PaaS aspirations. Although there are are candidates like 5C group, IREN is a front-runner due to SW1’s proximity to OpenAI’s $ORCL sites in Abilene. OpenAI’s job post show no hiring for IaaS operations and even if they did, they would in house the GB300s first. OpenAI is signing deals with Coreweave on higher margin GB300s and would in house the operations of GB300s before in housing the operations of Instinct GPUs. IREN is a perfect candidate for OpenAI to provide the GPUs and have IREN operate them.

IREN:

How would the economic look like in relation to other known deals? We know that the top-line ARR for NBIS/MSFT deal is 11.6m/MW-yr (17.4B/300MW/5yrs). However after accounting cost of GPU, switches, $CRDO cables, DataOne colocation, NBIS is looking at a profit estimate of ~4.832m/MW-yr which is still fantastic. IREN profit estimate is 7.232m/MW-yr of profit for its self owned GB300s (1). However to have the asset/cashflow leverage to quickly build out B200/B300/GB300 and eventually Vera Rubins for it’s Canadian Sites (160MW) Childress (up to 750MW) SW2 (600MW) while maximizing it’s fleet composition Vera Rubins in 2027, it makes sense to do a hybrid Colo/IaaS partnership with OpenAI. There’s not much figures for this, but a rough ball park would be 2.5m/MW-yr to 4m/MW-yr. For a 5 year deal, this would be 17.5B - 28B. Unlike $NBIS who is paying for GPUs and Colocation with DataOne, this would be mostly profit for IREN.

12

29

286

33,256

23 Sep 2025

$IREN Stargate deal a lock at this point…

23 Sep 2025

$ORCL, OPENAI & SOFTBANK JUST DROPPED A $400B BET ON AI INFRASTRUCTURE

Five new U.S. data center sites will take Project Stargate to ~7GW of planned capacity -- one of the largest utility buildouts in U.S. history.

Power is now the bottleneck.

7

1,409

4 Sep 2025

Aped some $RIVN 2027 calls today for the culture.

CT about to send a $17B company lmao

1

2

21

3,915

𝐑 𝐀 𝐒 𝐂 𝐀 𝐋 retweeted

18 Jun 2025

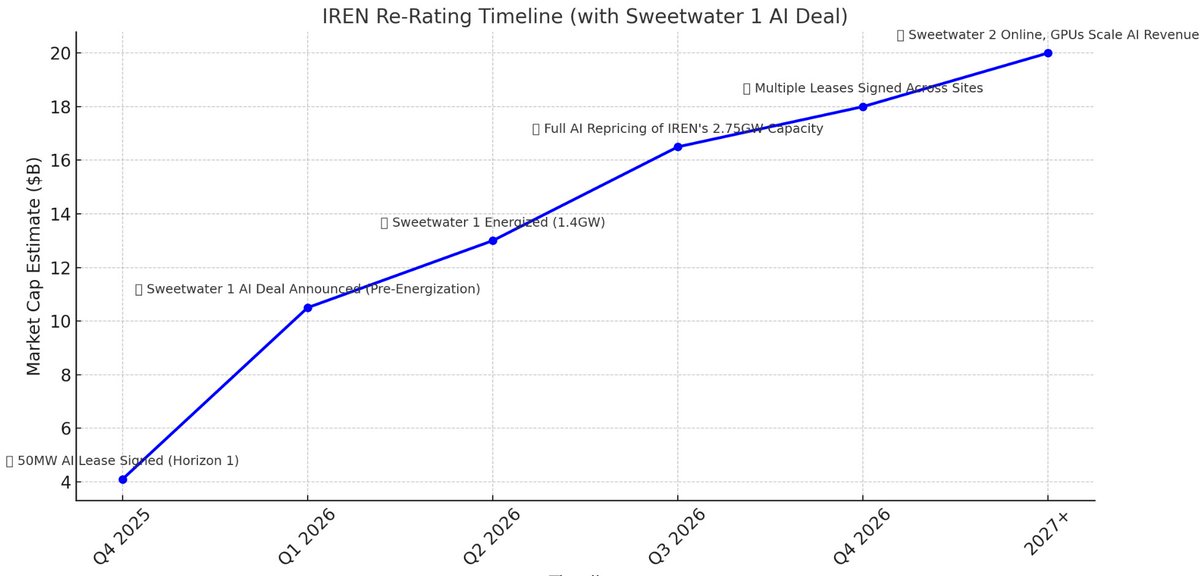

$IREN: The Most Asymmetric Play on AI Infrastructure

A single 50MW lease proves they can deliver.

A Sweetwater 1 deal (1.4GW) before energization triggers full re-rating.

This chart shows a realistic path to $100/share as 2.75GW gets monetized.

📈 $20B upside

#openAi $ORCL

12

28

236

45,448

𝐑 𝐀 𝐒 𝐂 𝐀 𝐋 retweeted

14 May 2025

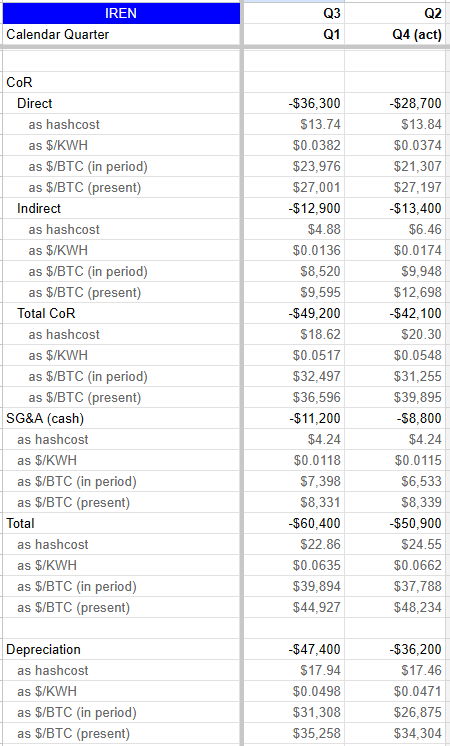

$IREN - great quarter, raking in cash as guided. Earned about $81m cash profits from mining -- far ahead of any other miner. All-in cash hashcost coming in at $22.86, which is just insanely good, and true to their guidance. Easily the best at pureplay mining right now.

Costs are clearly under control. Won't speak to HPC prospects, but those renderings look great.

Here are the numbers as I have them. Total cash hashcost ~$23, $/KWH numbers are great as well.

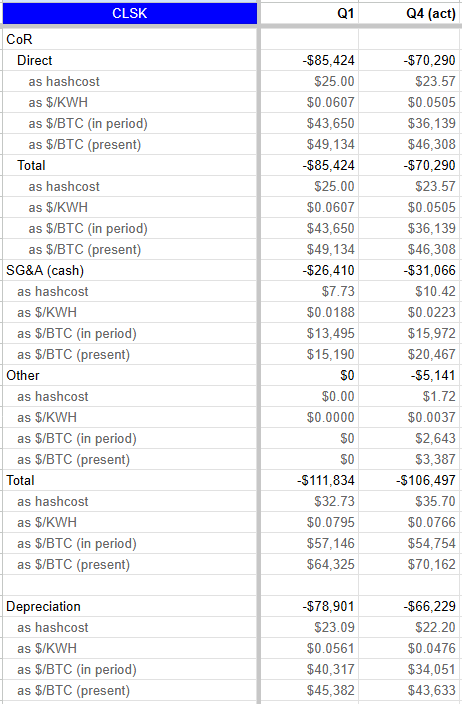

For comparison, here is $CLSK. Also a great operator, probably in 2nd place (haven't crunched all the miners' numbers yet). ~$33 hashcost -- commendable, but $IREN's lower J/TH fleet, and lower costs on a $/KWH, make $IREN the winner this Q.

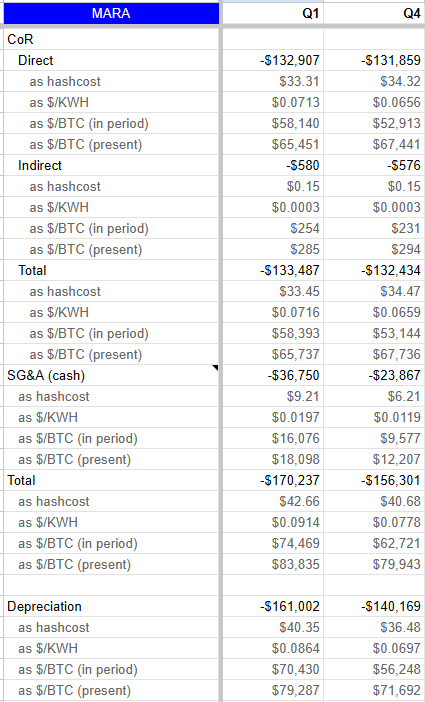

And here's what a struggling miner looks like ($43 hashcost, high $/KWHs):

Note that $MARA's "direct" cost includes hosting fees, which constitute ~45% of their BTC mining. Actual figures would be lower, but they'd presumably see an increase in SG&A as they move from hosting to O&O. So just look at "total".

If you'd like to get an idea of how all the miners would stack up if they all had the same fleet, just look at $/KWH numbers.

---

Back to $IREN, I like this nice touch where they no longer apply an "AI deduction" to guided hashcost. Thank you!

Only soft point was they sold 10m shares in Q1. Not ideal conditions to be selling, given share price at the time.

Best in class mining.. now all eyes are on HPC.

16

36

245

43,107

5 Apr 2024

Added a bunch of $TMDX this morning around ~$80, I agree with @JonahLupton's thesis here. The more I read about this company and it's growth story, the more bullish I become. $200 within 2 years? Seems like a layup.

x.com/JonahLupton/status/177…

5 Apr 2024

$TMDX up 8% today but this is just the beginning.

I think we’re going to see a lot of green days for $TMDX over the next 6-8 weeks before we get to Q1 earnings because I’ll be shocked if we don’t get a big beat & raise and investors want to be in the stock before that happens.

Not to mention all those $SWAV investors now need to find a place for that capital. Come join us on the $TMDX train to $200 within the next couple years.

1

2

11

4,862

30 Dec 2024

Frustrated that I roundtripped $TMDX, but the business has never been more solid. One bad quarter and -65%... I think it bottoms here.

Q4 should be amazing per flight data, this will be a great "January" effect stock IMO - it's now my largest position. I think $150 by EOY 2025.

1

2

15

2,299

14 May 2025

$TMDX $50s ▶️ $120s. Trimmed 1/3 position today, but still holding most. Shorts are trapped and still ~25% of the float. 👀

Q2 on track for a beat after one of the best Q1 reports I've seen. $150 incoming?

1

6

1,814

14 May 2025

$PRPH looks ready... earnings next Tuesday. News about receivables or Nebula Genomics sale and this heads to >$1.

Can we get $2 this year???

1

2

8

3,513

8 Apr 2025

$COIN 😭😭

8 Apr 2025

Faced with with an unexpected tax bill? No problem.

Borrow USDC against your Bitcoin and convert it to USD instantly to pay off your bill.

4

492

𝐑 𝐀 𝐒 𝐂 𝐀 𝐋 retweeted

29 Mar 2025

$TMDX continues to have a very strong Q1 with flight volumes up 21% QoQ.

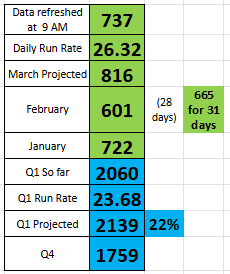

I also updated my spreadsheet today and we're at 26.0 flights per day (in March) with just 2.5 days left in the month/quarter.

This means $TMDX should do approximately 2,130 flights in Q1 which is 21% above Q4 flight volumes.

There are several other data points and variables we can't track but it certainly looks like $TMDX is headed for a monster Q1 earnings report, perhaps a 15-20% beat above current street estimates which now stand at $123.4M

Q4 revenues per flight was $69,220 and if you apply that to Q1 flight volumes it gives us $147.4M which would be a 19.5% beat above street estimates.

Unfortunately we can't track exactly what % of Q1 flights is internal (company owned planes) vs external (chartered planes) so my math above assumes that % stayed constant from Q4. Obviously if it changed in a meaningful way we won't know until they report earnings. If that % did change, I doubt it was by more than 5% in either direction.

If $TMDX does indeed report $140-150M in Q1, I would expect them to raise full year revenue guidance from 20-25% to 25-30% which means at the midpoint we're talking about $563M which means the stock is trading at 4.4x NTM EV/SALES which is simply too cheap in the medtech sector when they already have 20% EBITDA margins.

Personally I think $TMDX does at least 30-35% growth in CY2025 with EBITDA margins in the 20-22% range in which case $TMDX is trading at exactly 20x NTM EBITDA which is also too cheap for a company growing EBITDA at ~40% for the next few years as they launch OCS 2.0 and KidneyOCS plus increase efficiencies with their 21 planes.

29 Mar 2025

$TMDX had a record breaking day yesterday with 19 out of 21 planes flying all over totaling 36 flights in 24 hours!! Q1 is heading to landslide!!

24

27

235

65,448

𝐑 𝐀 𝐒 𝐂 𝐀 𝐋 retweeted

28 Mar 2025

$IREN trading at ~2x FCF (50 EH) from BTC at $80-90k. Free option on AI datacenters. Cheap enough? Ask yourself, not Mr. Market.

13

12

176

30,875

𝐑 𝐀 𝐒 𝐂 𝐀 𝐋 retweeted

11 Mar 2025

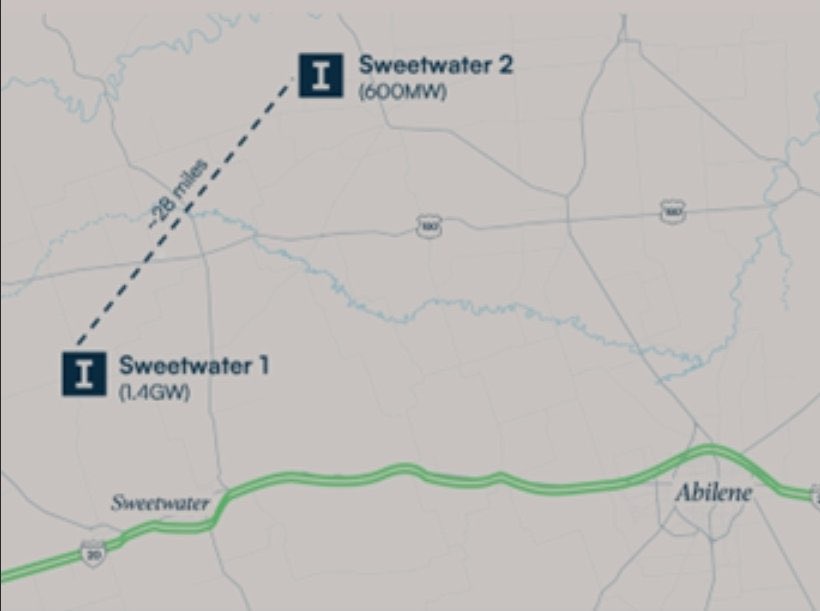

West Texas is quickly becoming the new data center capital of the world, and $IREN is growing with it.

We're set to deliver a 75MW liquid-cooled AI data center in the coming months, while the 2GW Sweetwater Data Center Hub, near the Stargate project in Abilene, is progressing well - with the first 1.4GW coming online in April next year.

datacenterdynamics.com/en/ne…

@OpenAI @sama @Oracle @larryellison @SoftBank

74

62

465

74,678

𝐑 𝐀 𝐒 𝐂 𝐀 𝐋 retweeted

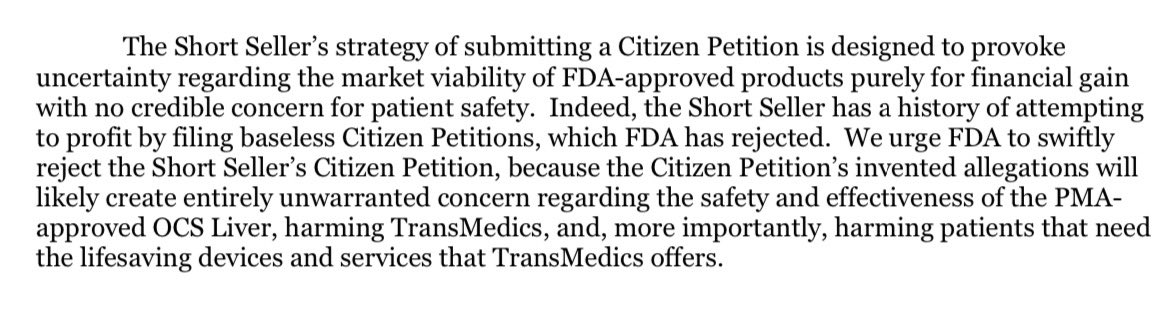

26 Feb 2025

Excerpt from $TMDX legal team’s response to Scorpion short seller citizen petition against the company.

3

25

4,202

8 Feb 2025

$IREN 👇🏾

7 Feb 2025

I think I found a Picasso at a garage sale.

But not the kind you’d think…

Lately I’ve been thinking about how to capture some of the upside of this AI boom in my stock portfolio.

But it’s hard. I’m a value investor.

The idea of paying 30x earnings for NVIDIA almost physically pains me.

Here are a few of the trade ideas I’ve sketched out:

Self-driving vehicles: self-driving is already here, it's just not evenly distributed. I use it 90% of the time in my Tesla and it's phenomenal. Between their robotaxis are coming later this year and Waymo rolling out to more cities, it seems like an obvious assumption that in the next ten years most cars will be self-driving. Trades I've considered: Long Tesla for robotaxi and Optimus upside, short Uber/Lyft as their networks become obsolete. Risk: rollout could take longer than anticipated due to huge capital costs and regulation, Uber/Lyft could pivot.

Compute and inference: The obvious plays - buy NVIDIA, ASML, and TSMC. Great companies but expensive multiples and premiums. Years of excess demand. Risk: geopolitical conflict in Taiwan, moat erosion as China and other competitors innovate.

Frontier models: You can buy secondary in Anthropic, x.AI or OpenAI, but the valuations are huge, positions are difficult to come by, and you're also betting on a winner (this is notoriously hard to predict). Risk: the value doesn’t end up accruing to any of them/models become commoditized.

Google: Another play is simply to buy Google, which owns DeepMind/Gemini and has a massive data moat. Risk: the innovator's dilemma, bungled AI rollout, ads/search business gets decimated by ChatGPT.

SoftBank: The final idea I've considered is buying Softbank. It holds some OpenAI and other AI businesses, is investing in data centers via Stargate, owns 90% of ARM (whose chip designs are a small part of many critical AI components and GPUs), and is trading for roughly ⅓ of NAV. Risk: volatility/debt, as Masayoshi Son is known for wild bets.

While these are all interesting potential options, I recently found an investment that offers a particularly interesting risk/reward...

Last month, I got a call from my friend @kashramki, a value investor based in Toronto.

We had gotten to know one another over a decade ago, when he worked at BCI, a large pension fund in my hometown. Since then, he had gone on to lead dozens of multi-hundred-million and even billion-dollar investments into infrastructure deals (mostly pipelines, datacenters, and renewable energy).

He told me he was doing something radical:

"I'm selling my entire personal portfolio and putting it all into one stock."

When a smart investor says that, I lean in.

I was surprised. Kash is a highly conservative and thoughtful guy and I'd never seen him be so "all in" on something.

Usually I was the one telling him about my latest hare-brained investment while he crossed his arms and scratched his head, telling me about the litany of ways it could go wrong.

He went on to tell me about a company called IREN.

Public market investors have boxes in their minds. When they look at a company, they sort it into a box labeled "Good," for later research, or "Bad," which they discard immediately.

Like expert poker players dispassionately folding hands, they have trained themselves to instantly dismiss any stock that comes with certain toxic labels - red flags that trigger an immediate 'pass'.

Words like:

- IPO

- Cannabis

- Biotech

- and the dreaded Bitcoin

IREN is one of these stocks.

And when he explained it, I realized that Kash had found the public market equivalent of a Picasso at a garage sale.

Here’s the backstory he gave me:

In 2018, @danroberts0101 and his brother Will, both infrastructure bankers from Australia, started IREN ($IREN). Their thesis was simple: demand for energy and compute would grow significantly in the coming decades.

They acquired a series of large, high power datacenter sites located near renewable energy plants.

Their first few were in British Columbia, and they went on to acquire two massive sites in Texas, which are coming online in the next year or so.

To date, they've been using the BC-based datacenters to mine Bitcoin. But they are far from Bitcoin bulls.

Every Bitcoin they mine is immediately sold for a profit. They hold near zero Bitcoin long term and are simply doing arbitrage, making hundreds of millions of dollars from Bitcoin sales each year.

The stock is currently trading at a market cap of around $2.3 billion with no debt. That is an illustrative adjusted 2024 run-rate EBITDA multiple of ~4.6x based on disclosures from the company (from page 16 of management's November 2024 presentation: illustrative 2024 EBITDA at ~$435m at $90k/Bitcoin).

As of today, Bitcoin is at $99,480, so we can assume that number is a little higher.

Their growth plans for this year, if executed as planned, could result in an even lower forward multiple. In the range of ~2.5-4x.

Ok, so it's a potentially cheap stock (CC: @dirtcheapstocks). But how does this relate to AI?

Two key things fuel AI: energy and compute.

Both are in limited supply. We've all seen nuclear, semiconductor, and datacenter stocks go parabolic over the last year. That is because AI will require an almost unimaginable amount of energy and computation.

Training AI models requires huge clusters of chips, typically Nvidia GPUs, and generally requires them to be in one location.

These huge datacenters are already in thin supply and take time to build and permit. They are heavily regulated.

IREN's new Texas facilities are significantly larger than industry averages in both land size and power capacity. For context, their Childress facility alone (750MW) is nearly four times larger than what is considered a normal modern data center (200MW), and their Sweetwater Texas site is almost double that at 1.4GW.

I believe that IREN trades at a low multiple for two reasons:

1. They are investing massive amounts of capex in building out their two huge Texas datacenters (coming online in 2025/26) and those earnings haven't hit the P&L yet.

2. They are dismissed and miscategorized as a Bitcoin miner. Others are starting to wake up to this (see: Softbank/Cipher).

If we simply value IREN as a traditional datacenter business and compare it to similar companies, we'd expect this business to generate datacenter free cash flow of ~$2 billion a year from their Sweetwater, TX 1.4GW site that is primed for AI compute starting April 2026.

That is ~$2 billion per year from this one additional site.

Added to its existing earnings, that's more than what the entire company is worth today.

If we apply industry multiples to their long-term projected earnings (once the Texas sites come online), the math becomes almost laughably compelling.

Using typical free cash flow multiples in the datacenter space, that gets you an enterprise value of ~$20-40 billion. 10 to 20 times where the company is currently trading. And that’s without valuing their Bitcoin business, which could be worth several billion on its own.

And yes, I just heard you yell “BUT WHAT ABOUT DEEPSEEK???” through a mouthful of potato chips.

Many point to DeepSeek's claimed $6M model training costs as evidence that compute demands might be cooling.

While they've achieved big efficiency gains, this isn't the paradigm shift some claim it to be. As Anthropic's CEO Dario Amodei explained in a recent blog post, we've historically seen a ~4x per year decrease in AI training costs.

DeepSeek's improvements are roughly on this expected curve, not dramatically below it.

But more importantly, these efficiency gains don't reduce total compute demand—they get immediately reinvested into training even more sophisticated models. The path to AGI and ASI will still require massive amounts of compute, both for training increasingly complex models and handling the explosion in inference demands as AI applications proliferate.

There’s a reason that Microsoft, Meta, and Google recently (post DeepSeek) announced they would collectively spend $220 BILLION on capital expenditures this year. The large majority of which will be spent on AI infrastructure.

Back to IREN…

So, we have a well-run company with no debt, ample cash flow generation, in an industry with huge excess demand, and a dirt cheap valuation.

This is my kind of garage sale Picasso!

As my friend @mohnishpabrai describes his favorite type of investment:

“Heads I win, tails I don’t lose much."

This feels like one of those.

Even if I’m completely wrong, and AI compute isn’t the hot commodity I’m anticipating, the underlying datacenters should still be valuable. Even before AI came onto the scene, the US datacenter market was expected to grow at 9-10% CAGR through 2030.

But, if AI does play out in a big way, those same datacenters could become Crown Jewels that could spit off huge amounts of cash from training and inference compute. Toll roads en route to the AI revolution.

So, all this is to say, I bought the stock.

A relatively small position for me. A few % of my portfolio mixed with a few other bets on frontier models, Google, and semiconductors.

Of course, like all investments, this has risk.

Here are a few of the best arguments for why IREN doesn’t pan out as I’m anticipating:

• They could dilute shareholders excessively.

• They could fail to capture the AI datacenter opportunities by favouring their past strategy of bitcoin mining, all in the hopes that bitcoin goes to the moon. With an 18-month payback period on their bitcoin hardware, the case for growing their bitcoin operations is very compelling, but it is only as sound a strategy as the price of bitcoin itself. And who knows what it will do tomorrow?

• Will they find a highly creditworthy counterparty for their mega-site in Texas? They could fail to demonstrate to the hyperscaler community that they have sufficient construction or operating experience to build and manage a large AI datacenter, especially in the middle-of-nowhere-Texas, where highly skilled datacenter operators are scarce.

• Bitcoin prices could drop to the point where mining is no longer profitable (around $30,000)—although I would argue the datacenters themselves are still valuable in this scenario. If you wanted to get clever, you could buy puts on a Bitcoin ETF to cover this scenario.

But overall, I think it offers a good risk/reward. I believe the underlying datacenter assets are valuable even if AI plays out very differently than expected.

I welcome any thoughts and critiques :-)

Is this a Picasso or a cheap reproduction? Roast me!

Important Disclaimers:

IREN stock is volatile. It swings around a lot, so if you buy, buckle up and be ready to hold for a few years. The value here depends on management delivering on their planned expansion.

I'm just a guy on the internet sharing thoughts. Not a financial advisor, and this definitely isn't investment advice. Yes, I have met with IREN's IR team, but everything I've shared comes from public sources - SEC filings, presentations, and public statements. Reality might look very different from the scenarios discussed.

Datacenters and crypto are wild markets with plenty that could go wrong - competitive pressures, regulations, market swings, geopolitics, you name it.

I own IREN shares and some of the other stuff mentioned here. Might trade them anytime. Could make me biased.

Do your own research, talk to actual financial advisors, and don't bet the farm. Past performance doesn't predict the future.

1

663