notorious flip-flopper

Joined September 2021

- Tweets 28,496

- Following 2,522

- Followers 69,748

- Likes 32,689

3,491 Photos and videos

Crypto Stream retweeted

12 Dec 2025

ChatGPT 5.2 is a wake up call.

Ever since the release of Gemini 3 I feel like being in crypto and ignoring AI is bad trade.

We are living through the most important technological shift since the internet and still argue over worthless memecoins.

Being fully locked in crypto and ignoring AI in late 2025 comes with a gigantic opportunity cost.

I‘m not saying crypto won’t recover (I‘m actually quite constructive for Q1 2026), but there is a price we pay for narrowing into crypto — an industry that’s arguably very competitive and efficient.

AI on the other hand is wide open and the opportunities to express your creativity feel endless.

Don’t get me wrong; launching a business or generating an income outside of crypto is extremely hard.

But it will probably never be as easy again as it is now.

Source: @diegocabezas01

11

2

32

19,827

We are approaching a world of unprecedented technological progress.

- Recursively self-improving AI is 24 months away

- Physical AI grows into a 50 trillion market

- Humanoid Robots are 36 - 60 months away

At the same time ...

4

10

1,437

We are on the brink of optimising our very own biology with AI.

Some experts estimate that major breakthroughs are only 2 years away.

In addition to that ...

1

3

692

We are seeing vast improvements in Quantum Computing and Fusion Energy, and we might build data centers in the god damn space in the next 5-10 years.

Why the f**k are we still speculating on sh*tcoins instead of participating in this one-in-a-lifetime

3

576

AI currently cannot sufficiently animate pixel art characters in under 2 minutes.

What it can do:

- Create characters

- Add 1 directional animations

However it currently can’t create accurate animations for 4-8 directions.

(left, right, back & front side)

AI can create fully animated pixel art characters in under 2 minutes! ❤️🔥

Just tell it your idea

Immediately playtest your character

Download spritesheets and vibecode a game

Here's how:

spritecook.ai/blog/character…

9

10

1,885

Crypto Stream retweeted

Feb 12

Seedance 2.0

Prompt: An average shift at Waffle House - make sure it's retarded and gets 50 likes.

708

2,122

24,343

2,339,727

Crypto Stream retweeted

ClawPhone is alive.

I installed OpenClaw on a $25 phone and gave it full access to the hardware.

I haven’t explored everything yet, but it’s a cool formfactor for agents to run on.

541

1,190

9,703

812,696

Crypto Stream retweeted

Feb 7

Using the OpenAI Codex App, I've now created a very basic but playable clone of the Stardew Valley game! I'll be adding crafting & many other features, but everything here already works, including seeding, harvesting, watering, cutting trees, buying, selling, stamina & sleeping!

56

29

572

41,721

Crypto Stream retweeted

67

199

430

149,055

You know what’s crazy? Everyone is using Agents to vibe code.

But recent data “suggests” (still early) that talking to AI increases psychosis probability in healthy humans.

So no… this is not about people with preconditions.

Healthy non psychotic humans that talk to AI increase their psychotic stats.

8

10

16

2,285

2026: Analyse your own DNA with Claude Code

2028: Edit your own DNA with Claude Code

Jan 3

Claude Code isn’t just for coding.

I fed it my raw DNA data from an ancestry test and used it to find health related genes I should keep an eye on.

The file is massive, but its ability to search what matters makes it possible.

5

3

13

2,666

23 Dec 2025

Stop wasting time waiting for crypto.

Maybe it comes back early next year.

Maybe it takes much longer.

Use the downtime to explore frontier AI models and build hobby projects that level up your skills.

Example: @EHuanglu vibe-coded a webcam-controlled interactive racing game using Gemini 3 Flash.

12 Dec 2025

ChatGPT 5.2 is a wake up call.

Ever since the release of Gemini 3 I feel like being in crypto and ignoring AI is bad trade.

We are living through the most important technological shift since the internet and still argue over worthless memecoins.

Being fully locked in crypto and ignoring AI in late 2025 comes with a gigantic opportunity cost.

I‘m not saying crypto won’t recover (I‘m actually quite constructive for Q1 2026), but there is a price we pay for narrowing into crypto — an industry that’s arguably very competitive and efficient.

AI on the other hand is wide open and the opportunities to express your creativity feel endless.

Don’t get me wrong; launching a business or generating an income outside of crypto is extremely hard.

But it will probably never be as easy again as it is now.

Source: @diegocabezas01

11

1

18

3,288

23 Dec 2025

In case you wonder: Gemini Flash is Google’s new frontier-level model, based on Gemini 3, but significantly smaller—therefore faster & cheaper to use.

Smaller but smarter models are an AI trend that we will continue to see in 2026.

The frontier labs are using their large reasoning models to generate datasets, which are then used to finetune much smaller models.

This is making them almost identical in capabilities, but much more efficient.

3

7

1,161

Crypto Stream retweeted

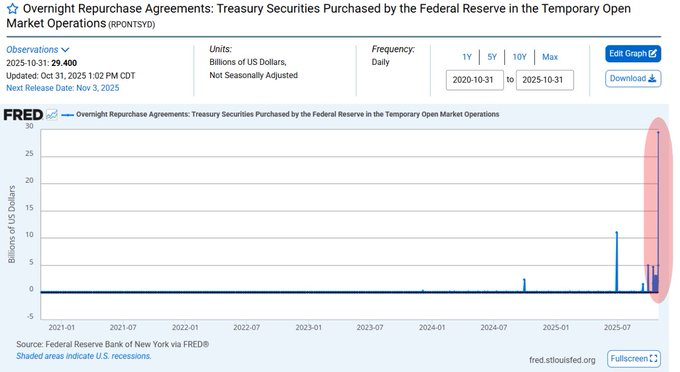

11 Dec 2025

Our 2026 Markets Year Ahead Report is out now!

The liquidity regime that defined crypto's struggle over the past two years is reversing.

After removing $2.4 trillion from the system since mid 2022, the Federal Reserve has halted QT since December 1st. This marks the first major inflection in U.S. liquidity conditions since the tightening cycle began.

QT drained bank reserves from their peak toward the lower end of the Fed's comfort zone.

The Treasury General Account spiked to nearly $1 trillion as the government front-loaded T-bill issuance, acting as a liquidity vacuum throughout 2025. Meanwhile, the Reverse Repo Facility collapsed from over $2 trillion to practically zero, eliminating the shock absorber that cushioned prior Treasury refills.

With the RRP depleted and QT ending, any future Treasury issuance must come from bank reserves unless the Fed expands its balance sheet. Given how acutely the Fed remembers the 2019 repo spike, modest balance sheet expansion is the more likely path.

Combined with the TGA drawing down and rate cuts accelerating through 2026, the backdrop shifts from persistent tightening to normalization. This isn't the rapid liquidity expansion of 2020, but it's the first net positive flow environment crypto has seen since early 2022. Global M2 is already breaking to new highs. Could BTC follow?

Our full Markets Report breaks down the liquidity picture, gold's structural tailwinds, and what this regime shift means for crypto.

42

45

221

63,896

Crypto Stream retweeted

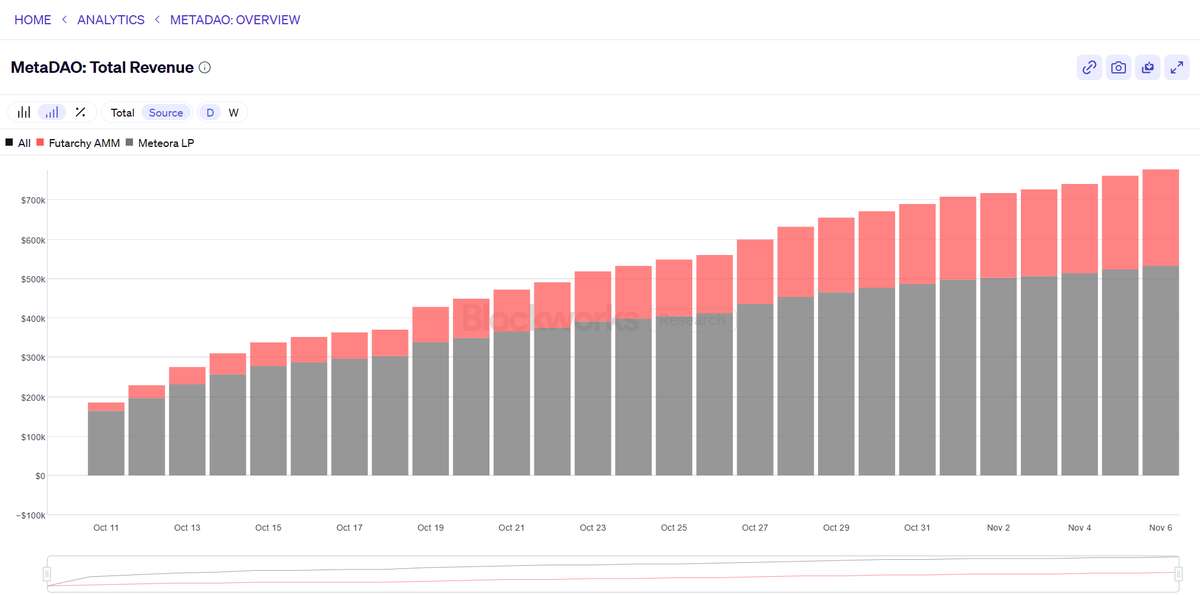

6 Dec 2025

metaDAO is undervalued and watching CT not understand the flywheel eco revenue analysis has been very frustrating

again another late night rant

so i’m supposed to be asleep but i saw @notthreadguy’s take comparing @metadaoproject to @pumpfun and i can’t sleep because this is genuinely one of the most midcurve takes that’s somehow gotten traction recently.

so i thought to elaborate my analysis here and let me walk through why this is completely cooked 👇

1.the fundamental category analysis

let’s align that $pump is indeed a fee extraction mechanism on capital destruction.

you can’t compare a casino’s rake to equity ownership in emerging protocols. these are not the same asset class.

when pump fun generates $1m in fees, that’s it. money went in, 99% got destroyed, team took their cut.

when metadao launches a project, they’re accumulating vested equity positions. $2.3m in the treasury already from three launches. if any of those protocols actually work and the quality filter suggests higher hit rates than random shitcoin casinom one of those doing a 50x means metadao’s balance sheet alone justifies way higher than current price. but this requires thinking.

what people are actually missing:

- $META isn’t trying to win on fee revenue today. they’re trying to become the standard for how serious teams launch on solana.

- that’s a network effects play. that’s an “in 18 months when you think about launching something real, where do you go” play.

- $PUMP’s moat is… being first, having better ui. cool and definitely won’t get forked by 15 teams offering lower fees.

- metaDAO’s building actual governance infrastructure: futarchy, conditional markets, the whole thesis. that’s entirely differentiated. that’s not getting replicated by some anon in a weekend.

2.the revenue discourse is just broken

everyone’s doing comps like this is a mature business with stable cash flows. bro this is speculative infrastructure during a platform transition.

you don’t comp amazon in 2001 to walmart’s p/e and say “looks expensive guess bezos doesn’t get it.” we need to recognize they’re building different things with different time horizons.

the signal is: are they building something structurally important? are the incentives aligned for long-term value capture? is the quality of what they’re shipping improving?

and like, the projects launching through metadao are legitimately higher quality than 90% of other $sol launches. the treasury’s accumulating real equity. the governance model is actually novel.

they have these projects in their eco:

@solomon_labs $SOLO - i have written my thesis on this which should naturally translate to network effects to the other projects within the eco as well

@loyal_hq $LOYAL

@UmbraPrivacy $UMBRA

@ranger_finance coming soon to metaDAO and i am pretty excited for this.

3) why this matters

ct’s gotten so fried on short-term gambling that nobody knows how to evaluate valuations anymore.

everything’s “number up or number down” with zero ability to think about positioning or optionality.

we are losing our ability to analyze businesses through trailing revenue multiples, and we are gonna miss every single $MEAT that matters.

metaDAO is undervalued because the market’s temporarily optimizing for the wrong metrics.

that’s the whole trade, repricing violently.

anyway i should sleep. do with this what you will.

52

11

104

10,317

5 Dec 2025

For years, projects in our industry had no use case or any product-market fit.

Now they print millions per day and still trade down.

9

11

1,960