A research-driven firm dedicated to making crypto happen sooner and better than it would without us.

Joined September 2018

- Tweets 11,654

- Following 999

- Followers 681,342

- Likes 9,369

4,023 Photos and videos

Pinned Tweet

Jun 12

Introducing the Token Design Toolkit

A free tool from Delphi Consulting to model your token design before launch

Stress-test unlocks, liquidity, and demand, then simulate to compare designs

Get insight into your token economy here:

delphi.link/Tokentool

Jun 12

I’ve been building a token design tool for founders and protocol teams.

Tokenomics should not just live in a spreadsheet or deck.

Teams should be able to test how their initial design affects liquidity, price, demand, unlock pressure, staking incentives, and growth.

The tool helps reason through:

- who gets tokens and when they unlock

- whether launch liquidity is enough

- whether demand can absorb sell pressure

- whether staking rewards are sustainable

- whether users will take risk for token yield

- how the system behaves across bull/base/bear simulations

The key question is not “does this token design look good?”

It’s:

“If we launch this design, where does it break?”

I want this to become an end-to-end workspace for token design before launch.

Would love feedback from founders, investors, researchers, and token teams.

12

12

36

10,297

Kevin explains why open-source AI is becoming so crucial.

"Prior to this example, we kind of had fears of being priced out or locked out. Now we’re starting to see that becoming real... And that’s where open source comes in.”

46

3

26

5,616

Read the Hermes report for free here.

delphi.link/Hermes

4

2,889

Delphi Digital retweeted

Jun 12

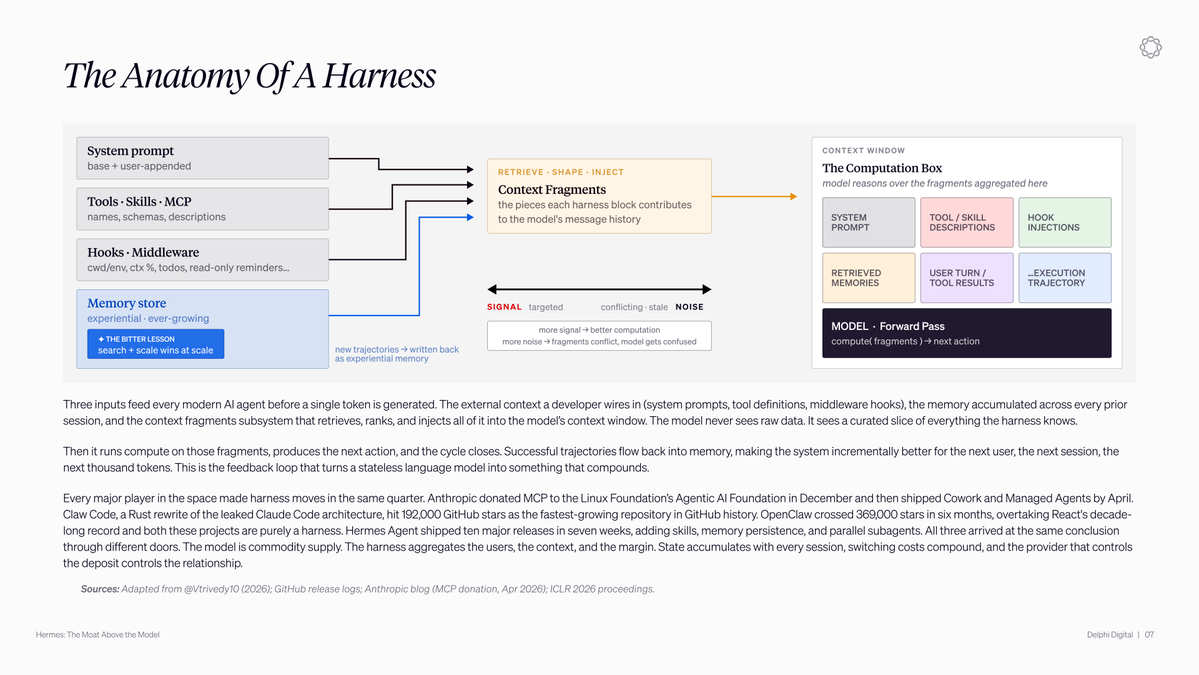

Kevin explains why agent harnesses are becoming the next operating system.

"I could boot up straight into Hermes Desktop and everything I need to do can be done through that harness.”

26

7

27

8,140

Delphi Digital retweeted

Jun 12

Introducing the Token Design Toolkit

A free tool from Delphi Consulting to model your token design before launch

Stress-test unlocks, liquidity, and demand, then simulate to compare designs

Get insight into your token economy here:

delphi.link/Tokentool

Jun 12

I’ve been building a token design tool for founders and protocol teams.

Tokenomics should not just live in a spreadsheet or deck.

Teams should be able to test how their initial design affects liquidity, price, demand, unlock pressure, staking incentives, and growth.

The tool helps reason through:

- who gets tokens and when they unlock

- whether launch liquidity is enough

- whether demand can absorb sell pressure

- whether staking rewards are sustainable

- whether users will take risk for token yield

- how the system behaves across bull/base/bear simulations

The key question is not “does this token design look good?”

It’s:

“If we launch this design, where does it break?”

I want this to become an end-to-end workspace for token design before launch.

Would love feedback from founders, investors, researchers, and token teams.

12

12

36

10,297

Jun 12

Kevin explains why agent harnesses are becoming the next operating system.

"I could boot up straight into Hermes Desktop and everything I need to do can be done through that harness.”

26

7

27

8,140

Jun 12

Muhammad explains why AI models are commoditizing and where the new moat is.

"So the model itself is commoditized. The moat is now dependent on memory, context and data specifically."

10

2

22

5,158

Delphi Digital retweeted

Jun 12

The $SPCX IPO marks chapter one.

Sixty years of flat launch costs ended with @SpaceX.

The next 20 drive a 150x drop, from $1,500/kg to $10/kg.

Each threshold unlocks an industry that used to be science fiction.

The full cost curve, and everything it unlocks, below:

3

3

34

8,682

Jun 12

Jason explains why crypto assets need a good reason to be held in this market.

“Imagine owning ETH over the last year watching Hype or AI names, right? All of this will continue to bleed money out of crypto until Bitcoin starts to do its thing again.

9

6

28

4,478

Delphi Digital retweeted

Jun 10

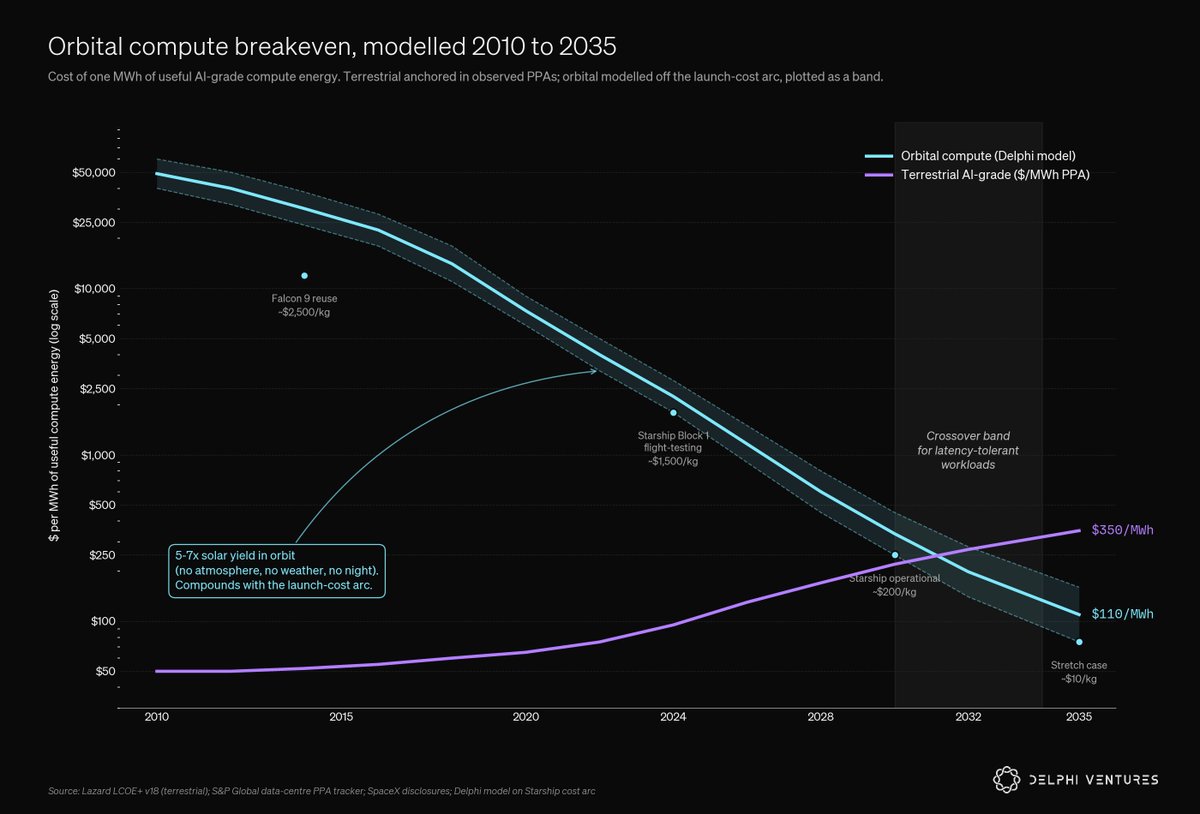

Everyone's watching the SpaceX IPO.

The bigger story is the multi-trillion-dollar economy it's unlocking.

The price of leaving Earth is about to undergo its most aggressive compression in history. Launch costs barely moved for sixty years, then SpaceX arrived and drove them down by an order of magnitude.

This report from @pierskicks anticipates another 60x drop by 2045.

Every drop in price makes previously impossible businesses viable. Each threshold unlocks an entire industry:

• $1,500/kg gave us megaconstellations and Earth observation.

• $500/kg opens orbital compute and commercial stations.

• $200/kg opens microgravity manufacturing.

• $50/kg unlocks a lunar economy.

• $10/kg underpins the Mars supply chain.

Starlink already carries capacity equivalent to as much as 20% of the world's real-time internet traffic. Orbital data centres sounded like science fiction in 2019 and are now funded in response to terrestrial power constraints. Anthropic and Google have signed deals paying SpaceX ~$26B a year for access to Colossus here on the ground.

The most interesting founders in the sector are already building for launch costs that don't exist yet.

15

11

37

14,249

Jun 11

Jason explains why it’s still worth staying active in crypto.

"If you just stick around in crypto, it guarantees you to see something early. Whether or not you buy it is a different question, but it guarantees you the opportunity to be early to things."

20

7

28

7,599

Jun 11

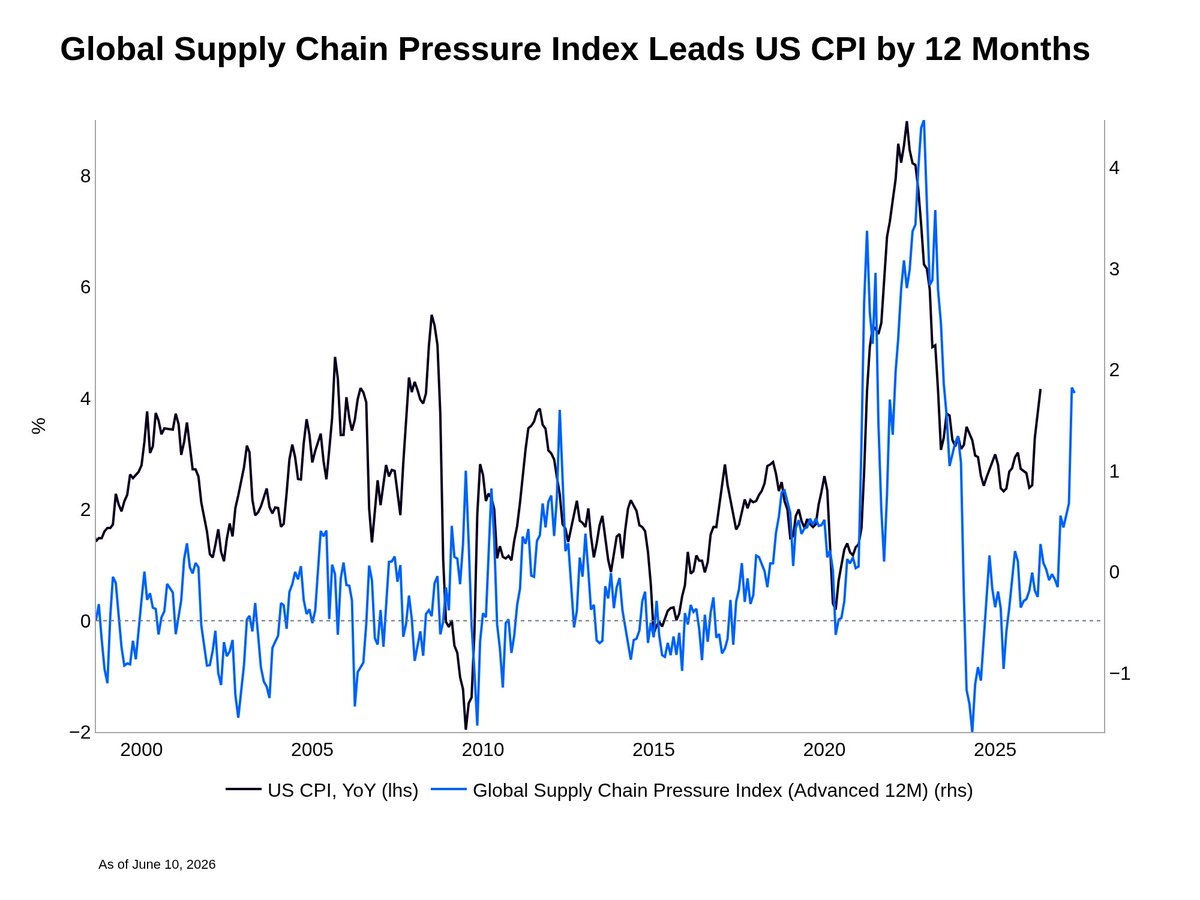

The disinflation story is under pressure.

Our markets team has been flagging this for three months, and this week's CPI print is the confirmation. That's a meaningful shift from the pre-war outlook and removes one of the reasons 2026 looked more resilient than 2022.

The oil shock from the Iran conflict is showing up in headline CPI. Core leading indicators are moving in the same direction. Prices paid remain elevated across manufacturing and services, and import prices ex-petroleum are picking up.

Wages are what's giving the Fed cover. Wages aren't yet accelerating enough to force the Fed's hand, but last Friday's reaction to a strong jobs print is a preview of how quickly that changes if labor data runs hot.

Against that backdrop, Warsh's first FOMC meeting lands next week. The market has a habit of testing incoming Fed Chairs (Greenspan in 1987, Bernanke in 2006). Consensus expects him to anchor on Dallas Fed Trimmed Mean PCE since it remains subdued.

But as a reminder, headline CPI leads it by six months.

8

4

19

6,693

Jun 11

Going live in 10 minutes!

Our report on @NousResearch Hermes Agent is now free and open source.

Hermes Agent is now the most popular agent harness.

We are going live this Thursday 11AM ET with @KSimback, @Shaughnessy119, and @yusufxzy to discuss Hermes agent, harness moats, and where AI goes from here.

4

4

4,140

Jun 11

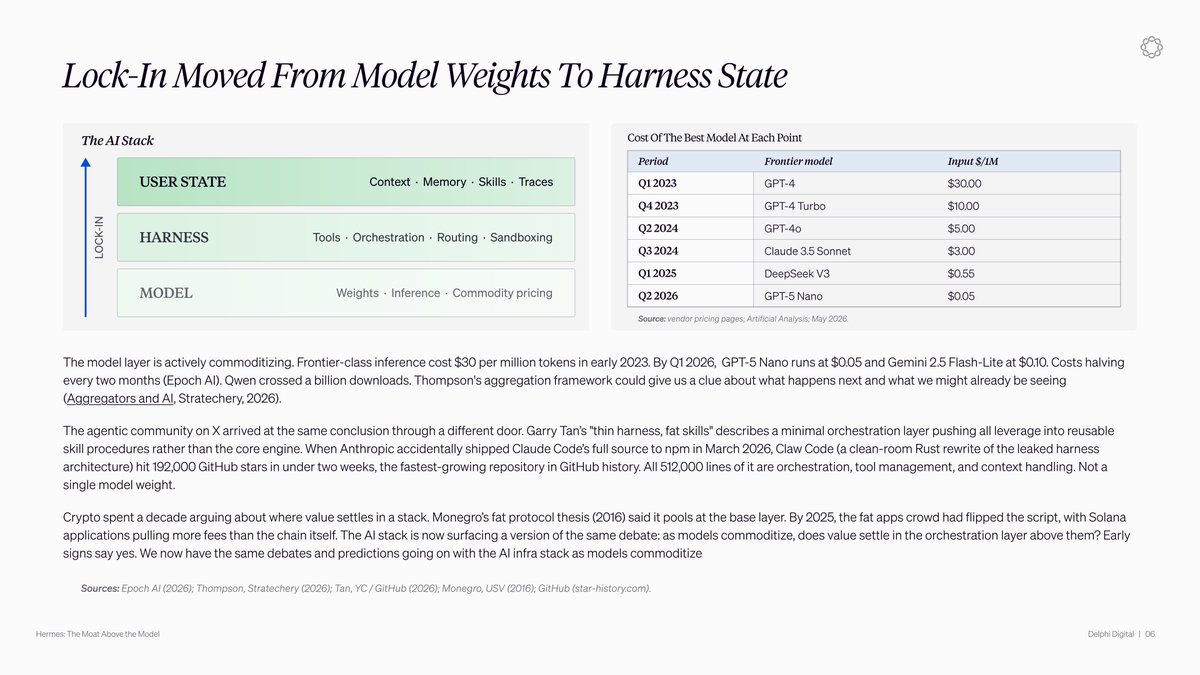

Harnesses could be the new moat in AI.

On SWE-bench Pro, running the same model through different scaffolds swings the resolve rate by 22 points. Swapping between the six best frontier models inside the same scaffold moves it by less than one.

Meta and Harvard paired Sonnet 4.5 with a custom harness and scored 52.7%, beating Anthropic's own scaffold running the more expensive Opus at 52.0%. The cheaper model won because its harness was better.

@NousResearch built Hermes Agent around that same thesis. Every session writes its state to your machine. Conversation history goes into a local SQLite database with full-text search, and project context and personal preferences sit in markdown files the agent loads at startup. Complex tasks get saved as reusable skill files, and Honcho keeps a structured profile of how you work.

The model underneath is interchangeable. Closed agents keep your context with them, and leaving means rebuilding from scratch. Hermes lets you take your context to whichever model you want.

Closed labs hold an edge in long sessions because they fine-tune against thousands of hours of degraded runs, and open source providers haven't had the session data to match.

Hermes routed 3.2 trillion tokens in one week on OpenRouter which gives Nous a path to closing that gap.

9

1

23

5,298