Professor of Law @CornellLaw | Research Member @ecgiorg | Co-Managing Editor @JFinReg

Joined April 2015

- Tweets 8,796

- Following 172

- Followers 3,970

- Likes 5,929

171 Photos and videos

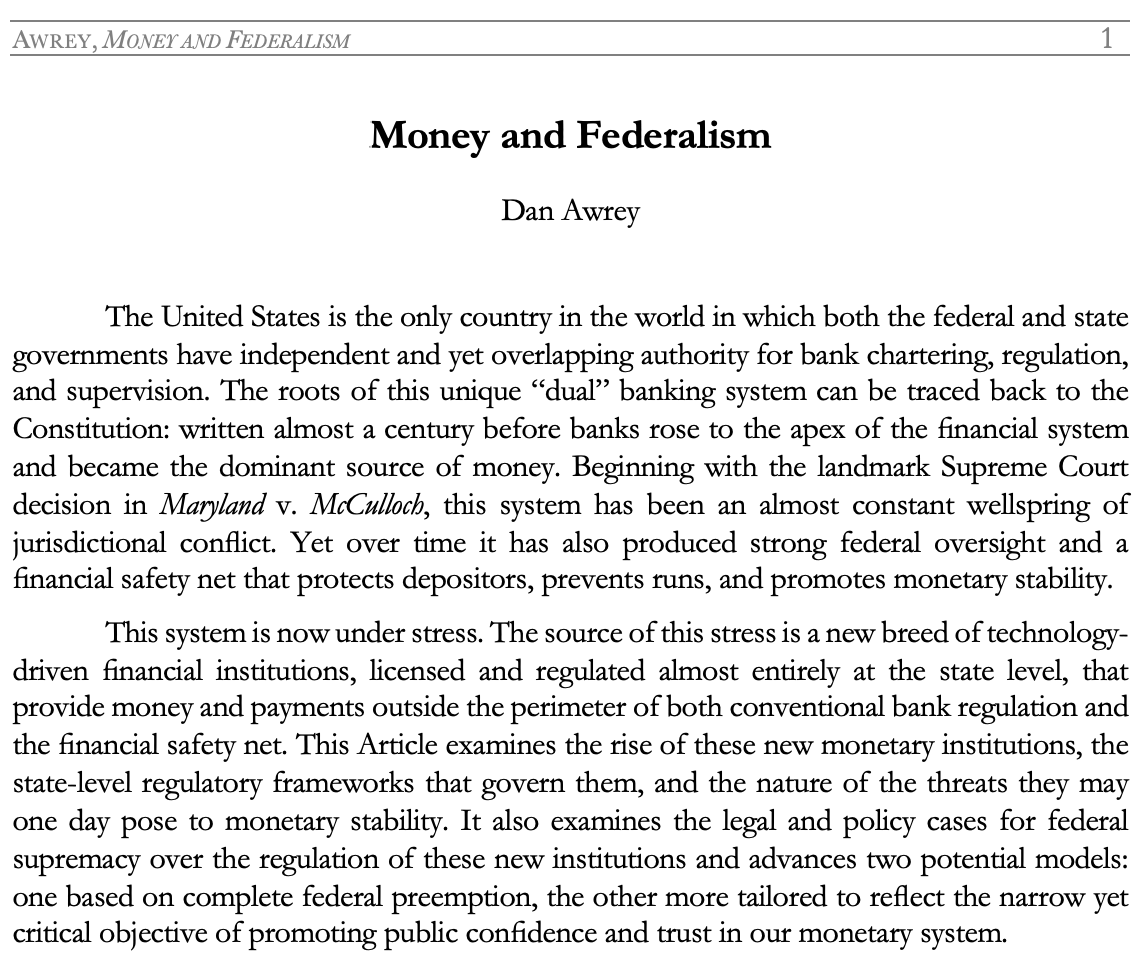

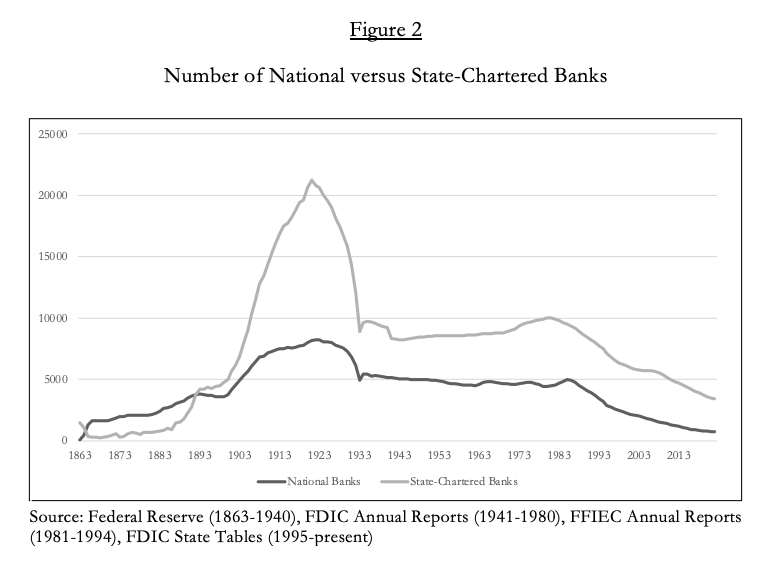

📢👷🏼🛠️ NEW WORKING PAPER exploring the impact of technological disruption on bank business models, consumer expectations, and financial stability. Questions, comments, and suggestions all very welcome: papers.ssrn.com/sol3/papers.…

2

2

29

2,413

Dan Awrey retweeted

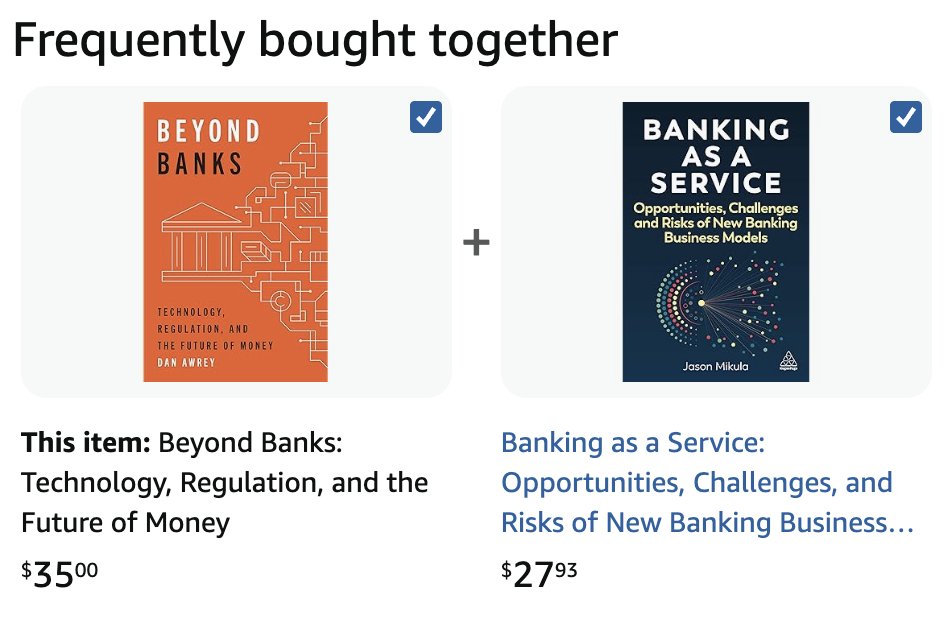

...and is available for pre-order! penguinrandomhouse.com/books…

🇺🇸 USA: 250 years old

💵 Dollar: 500 years old

Great new book by @bhgreeley that is coming soon to the podcast!

1

3

3

2,089

Dan Awrey retweeted

21 Aug 2025

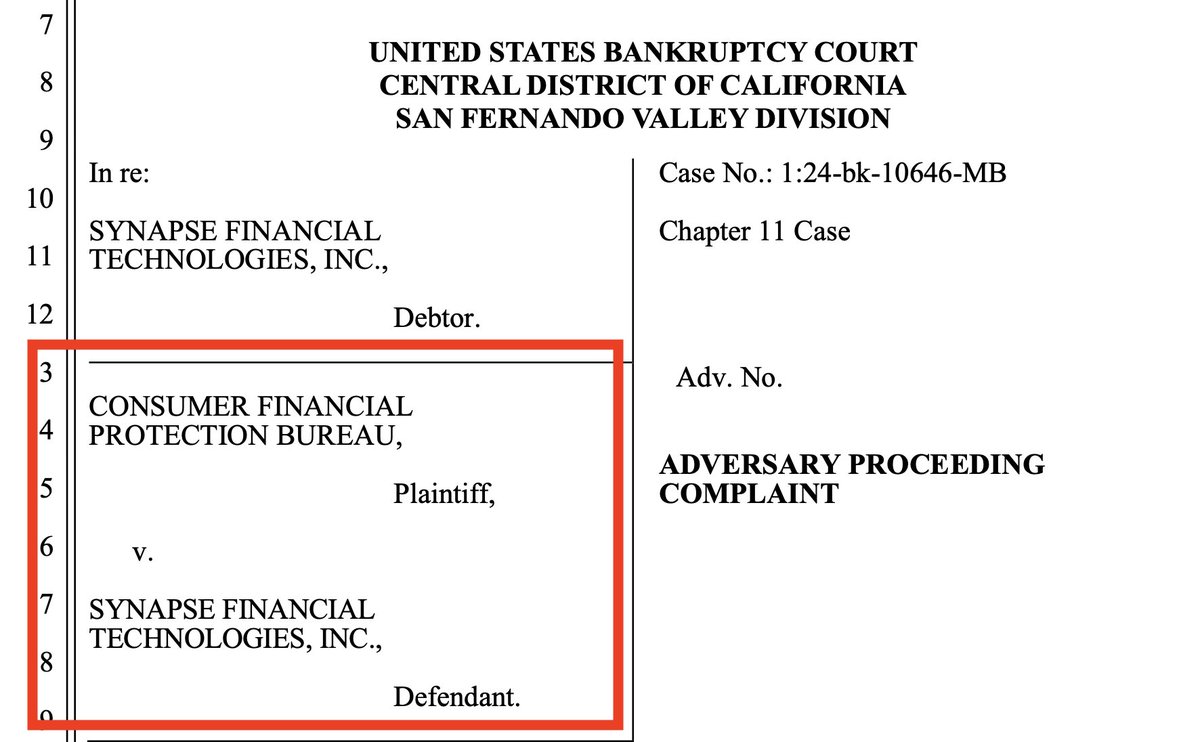

🚨 BREAKING: CFPB says that by Sept'23 "both Evolve and Synapse were aware that there was a deficit of tens of millions of dollars in funds that Evolve was holding for End Users" in just-released complaint:

The CFPB complaint alleging Synapse violated the Consumer Financial Protection Act by engaging in "unfair" acts or practices by failing to maintain adequate records was filed as part of the bankruptcy case today, August 21st, I believe I'm the first to report.

While the complaint largely rehashes already disclosed information, it's now being alleged by a government agency. A couple interesting items worth noting:

-The CFPB alleges that "[c]onsumers did not have control over how Synapse moved or tracked funds across different Partner Banks that were holding their funds and processing their debit card, ACH, and wire transactions."

-and that "[c]onsumers were substantially injured because Synapse’s records did not match the records of its Partner Banks."

These are important as they're necessary elements to prove Synapse acted "unfairly."

The CFPB's complaint notes that not all fintech programs "migrated" to the Brokerage/cash management structure, meaning those programs' end users’ funds should have remained with Evolve.

The complaint notes (as was already known) that even for end users who were moved to the cash management program, "Evolve continued to act as a Partner Bank by providing access to certain banking products and services, including by continuing to sponsor debit cards. Evolve also continued to act as the receiving bank for ACH transfers for which consumers had previously been using Evolve’s routing number, such as direct deposit. Evolve continued to maintain accounts on behalf of these End Users to provide these services. Synapse would sweep funds from those accounts to Synapse Brokerage."

The complaint seeks to enjoin Synapse from further violations of the CFPA (a non-issue, as it's bankrupt), additional injunctive relief (also largely irrelevant), award relief the court finds necessary to redress injury to consumers (this theoretically could be a significant monetary amount, though the chance of recovering any money seems very low), and a civil money penalty (necessary to enable CFPB to tap victim relief fund).

It's worth noting that Synapse was a third-party service provider to Evolve. While the CFPB isn't making an accusation that Evolve engaged in "unfair" acts or practices, that doesn't preclude Evolve's regulators, the St. Louis Federal Reserve and the Arkansas State Bank Department, from potentially pursuing an enforcement action against Evolve for "unfair" practices conducted by Synapse on the bank's behalf (though I wouldn't hold your breath.)

Many states offer consumers a *private* right of action for a business' "unfair" conduct, potentially offering victims an avenue to file civil suits against Evolve stemming from Synapse's "unfair" conduct.

8

12

47

6,762

Dan Awrey retweeted

17 Aug 2025

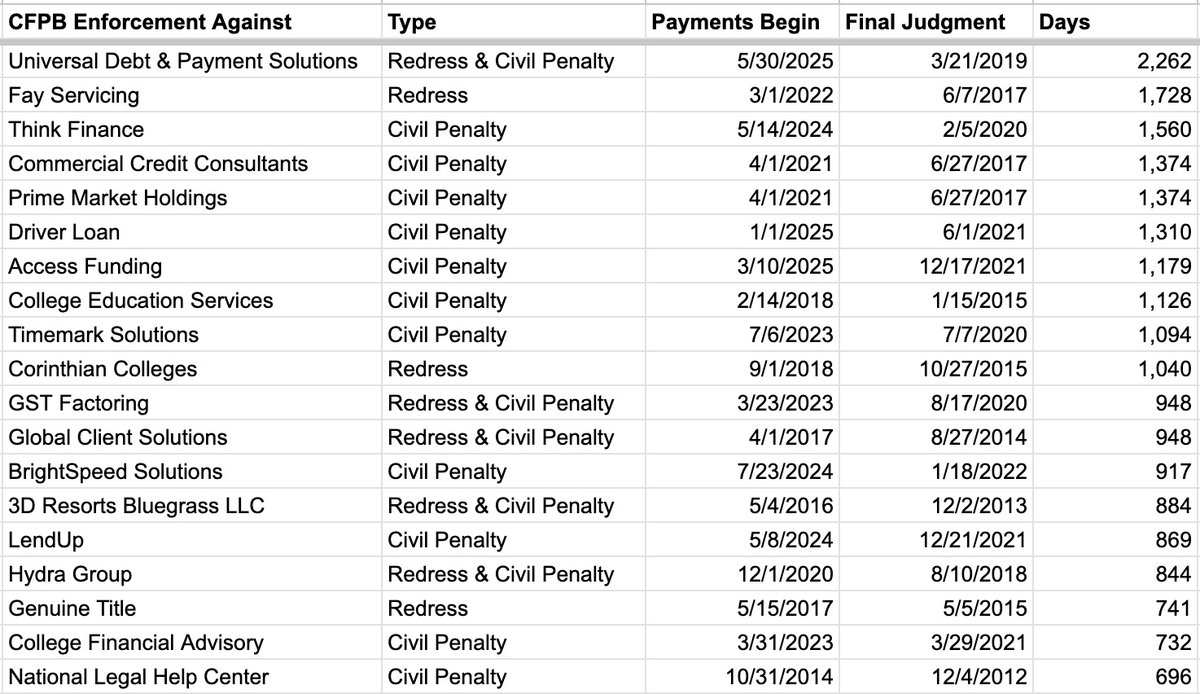

Fintech Biz Weekly just dropped:

Synapse-Evolve victims could end up waiting YEARS to get a CFPB bail out payment, new analysis of Bureau records suggests.

CFPB's average time from a final order to starting payments to victims? A whopping *682 days*

You know where to find it.

9

12

48

11,906

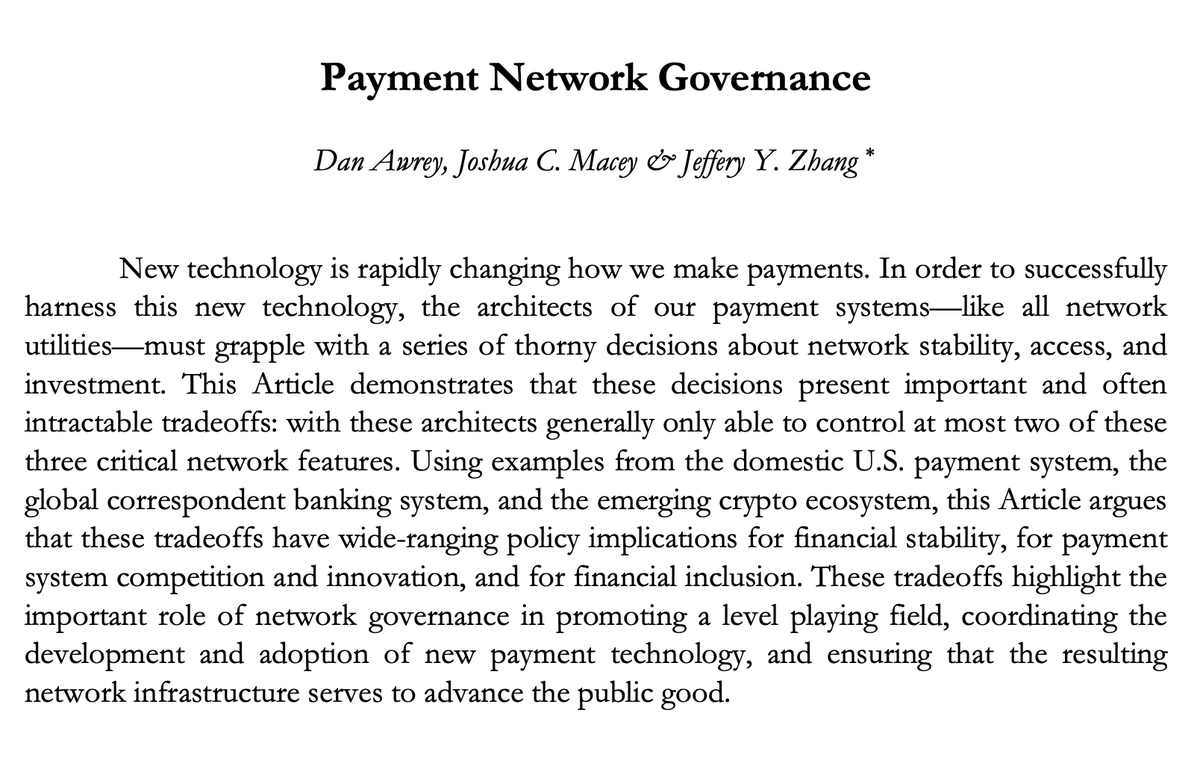

This is a very thoughtful piece by William Buiter on @ProSyn. But like many reviews of #beyondbanks it ascribes to me a position that I don't hold: namely, that we should separate all money and payments from financial intermediation 1/4 prosyn.org/ZiTEUWr

1

4

619

This is also why, to Buiter's lament, I ignore CBDCs. Central banks rarely have an advantage over private firms in conducting technological experiments with new payment tech, let alone the infrastructure we might build on top of it. This makes retail CBDCs a fool's errand 3/4

1

2

425

Dan Awrey retweeted

28 May 2025

As stablecoins grow, so does their impact on the markets they invest in. They already influence short-term Treasury yields, with implications for monetary policy and financial stability bit.ly/4kABGBl

#Stablecoins #Treasuries #FinancialStability

9

66

171

38,398

This may take the prize for the most timely law review note in history harvardlawreview.org/print/v…

2

1

10

1,086

A safe, sound and fair fintech business model has a place in today’s federal banking system. Read more at occ.gov/news-issuances/news-…

ALT OCC Conditionally Approves Fintech Business Model for a National Bank

1

6

15

11,288

Dan Awrey retweeted

15 Mar 2025

The CDFI Fund is one of the most successful programs at getting affordable capital to small businesses and parts of our economy not well served by the existing financial system, like Indian Country. A colossal mistake to shut it down.

15 Mar 2025

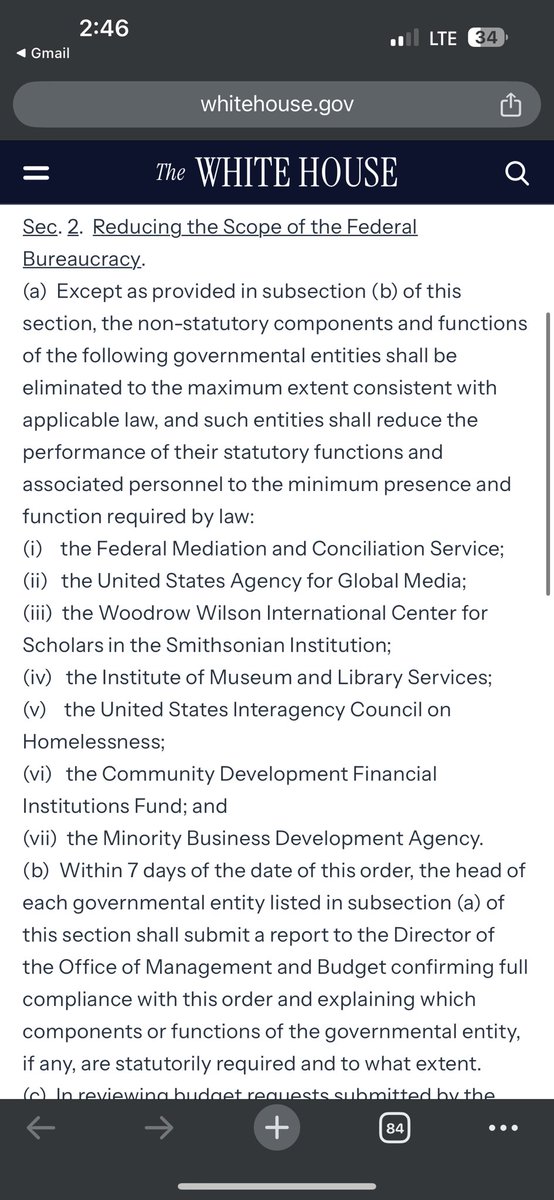

This White House EO dated yesterday appears to gut the Community Development Financial Institutions Fund.

This Treasury program is one of the most bipartisan out there. There's a two-year-old CDFI congressional caucus led by Sens. Mark Warner and Finance Chair Mike Crapo

1

3

16

2,293

Dan Awrey retweeted

12 Feb 2025

I like to think that my forthcoming book, King Dollar, is pretty good, but it would have been lots better if I had been able to incorporate the superb wisdom and insights from @DanAwrey’s book, which came out just as mine was already in galleys and impossible to change.

The book is real! And in only two more weeks you too can line your bookshelves with dozens of copies!

It's available for pre-order now: press.princeton.edu/books/ha…

You will also be able to find it at Barnes & Noble, Target, Audible, Apple Books, and other fine establishments.

2

2

5

836

Dan Awrey retweeted

5 Jan 2025

#Book Review: “good money” vs “good payment”

“Beyond Banks” by @DanAwrey Technology, Regulation, and the Future of Money, @PrincetonUPress 07 Jan 2025, UK.

acemaxxanalytics.substack.co…

3

7

1,898

Dan Awrey retweeted

29 Dec 2024

Santa did great this year. High information/page-count ratio, and @DanAwrey is incredibly lucid.

What he calls Gresham's New Law—but I suggest we call Awrey's Law—that we value "good payments" in financial peacetime, but "good money" in crisis-time, is essential policy insight.

2

8

48

2,448

Dan Awrey retweeted

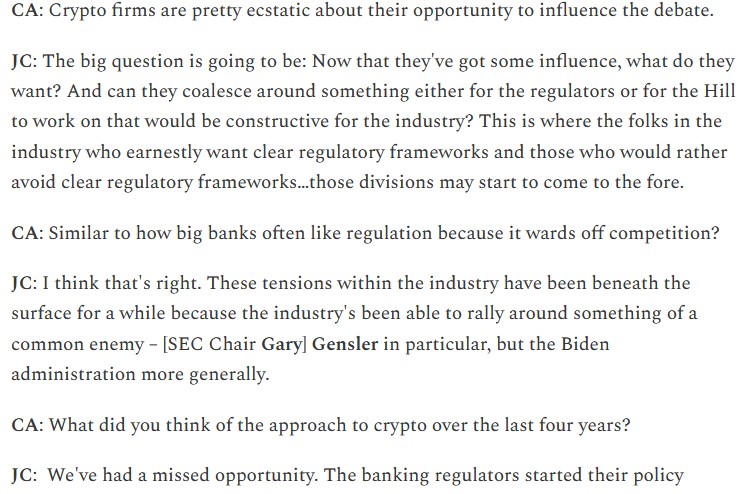

18 Nov 2024

“The tensions within the [crypto] industry have been beneath the surface for a while” thanks to a common enemy. Now, divisions could start to emerge. -@JonahCrane

18 Nov 2024

Our Weekend Q&A this week was with @JonahCrane , a DC vet who offered great perspective on FinReg changes in store. Here's one of his many interesting points: capitolaccountdc.com/p/a-fin…

1

2

7

1,788

Dan Awrey retweeted

28 Oct 2024

Under what legal authority can the @federalreserve refuse to tell Congress how much money has gone through #FedNow?

Or is the Fed so scared of the truth that it would rather break the law...

fetterman.senate.gov/wp-cont…

3

7

2,877

Dan Awrey retweeted

23 Oct 2024

In Beyond Banks, @DanAwrey explains how new technology is rapidly changing the nature of money and the way we pay.

Out now. Learn more about this pathbreaking book: hubs.ly/Q02TSscC0 #Banking #EconTwitter

ALT Beyond Banks: Technology, Regulation, and the Future of Money by Dan Awrey

4

16

1,385

Dan Awrey retweeted

12 Oct 2024

In Beyond Banks, @DanAwrey sheds critical light on the important but too often dysfunctional relationship among technology, regulation, and money.

Out October 22. Learn more: hubs.ly/Q02QY6cM0 #Banking #EconTwitter

ALT How new technology is rapidly changing the nature of money and the way we pay

3

13

1,975