Data Centre Recruitment Specialist | Data Center Talent Acquisition | Data Center Jobs

Joined September 2011

- Tweets 1,501

- Following 2,266

- Followers 739

- Likes 376

29 Photos and videos

UK poorer than every individual US state? instagram.com/p/DY3fDS0k7vg/…

7

Datacenex Recruitment retweeted

May 27

NVIDIA QUIETLY DROPPED A $249 BOX THAT REPLACES YOUR $200/MONTH OPENAI SUBSCRIPTION WITH $2 IN ELECTRICITY

it's called the jetson orin nano super. smaller than a wallet, runs at 25 watts, does 70 trillion ai operations per second. runs llama 3, mistral, gemma and deepseek locally with no api fees and no data leaving your house

a developer running automations and coding assistants pays $200 a month to openai. the same workload on this box costs $2 a month in electricity and breaks even in 10 weeks

install ollama with one command. change one line in your code. point it at localhost instead of openai. everything else works identically

7 billion parameter models handle 80% of what people use chatgpt for. summarization, drafting, coding, document q&a, automation pipelines. total monthly cost drops from $200 to $22

cloud subscriptions keep getting more expensive and rate limits keep getting tighter. the people who set this up in 2025 are going to look very smart in 2027

bookmark this and read the article below

Community note

Jetson Orin Nano Super ($249) is a Dec 2024 software update/price drop (67 TOPS) on 2022 hardware with 8GB RAM. Runs quantized ~7-8B models for basic tasks/privacy but not equivalent to frontier cloud models for complex work. nvidia.com/en-us/autonomo… developer.nvidia.com/blog/nvidia-je…

382

900

5,643

2,346,200

I'm attending Building Energy Infrastructure in a Data Center Driven Market. Join me on June 11. linkedin.com/events/building…

4

10

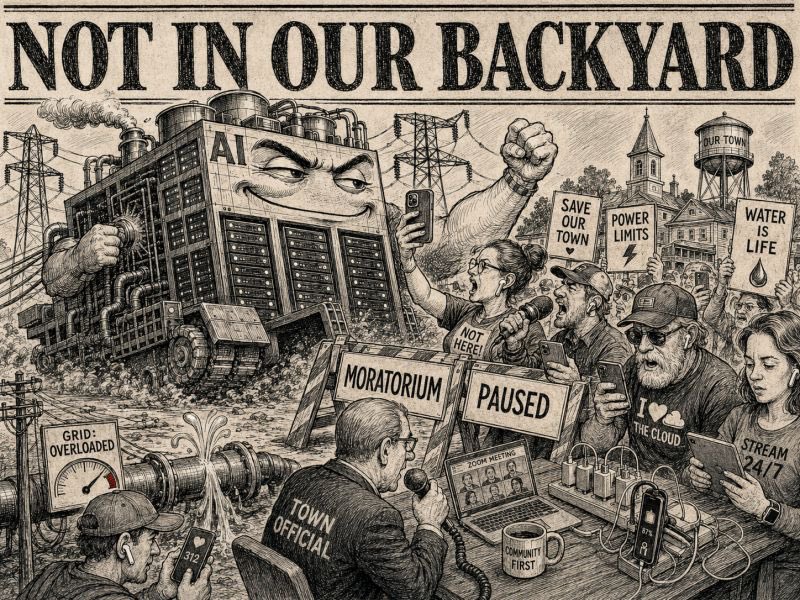

Data centers emerge as growing wedge issue in midterm races thehill.com/homenews/campaig…

10

Datacenex Recruitment retweeted

Mar 9

🚨 BREAKING: Anthropic quietly dropped a 32-page playbook on building Claude Skills.

Skills let you teach Claude your exact workflow once. It executes it every time after that. Across Claude.ai, Claude Code, and the API.

No more re-explaining. No more inconsistent output.

This is how AI goes from chatbot to custom operating system.

PDF: resources.anthropic.com/hubf…

45

346

2,294

529,945

Datacenex Recruitment retweeted

Mar 5

Striking image from the new Anthropic labor market impact report.

551

2,223

13,361

7,269,891

Datacenex Recruitment retweeted

18 Oct 2025

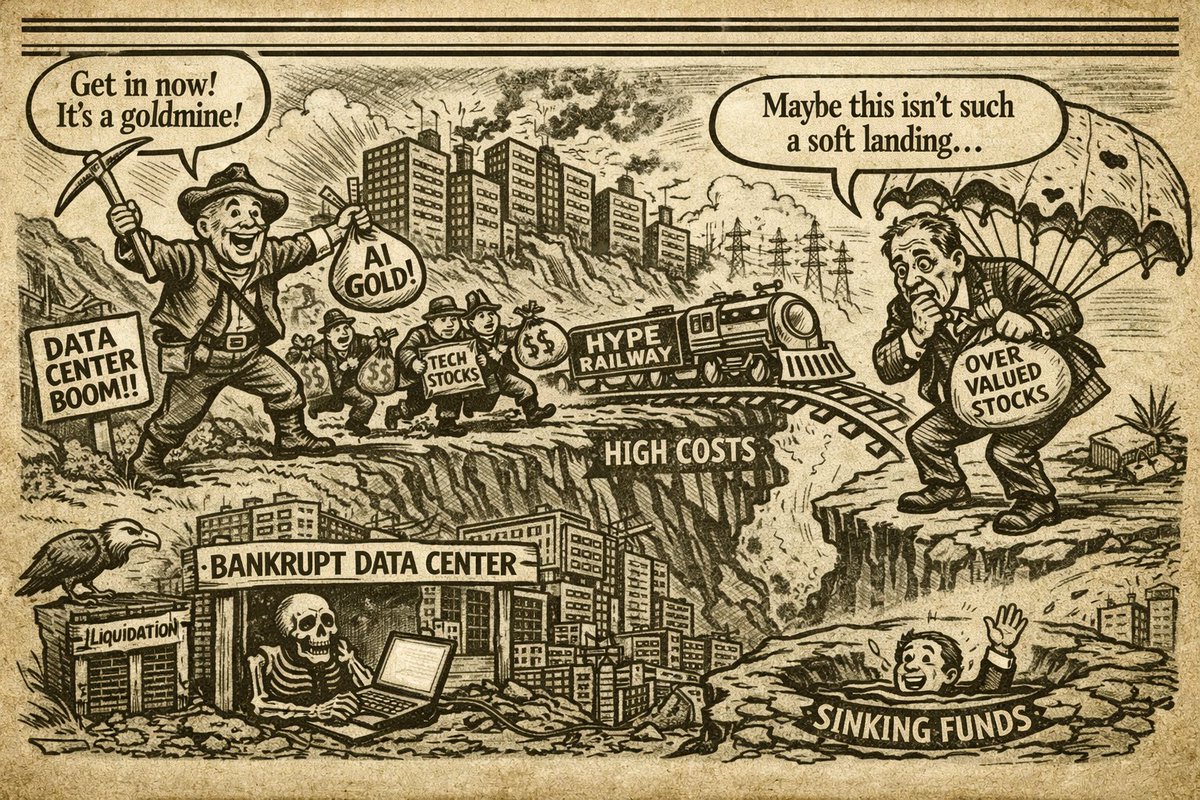

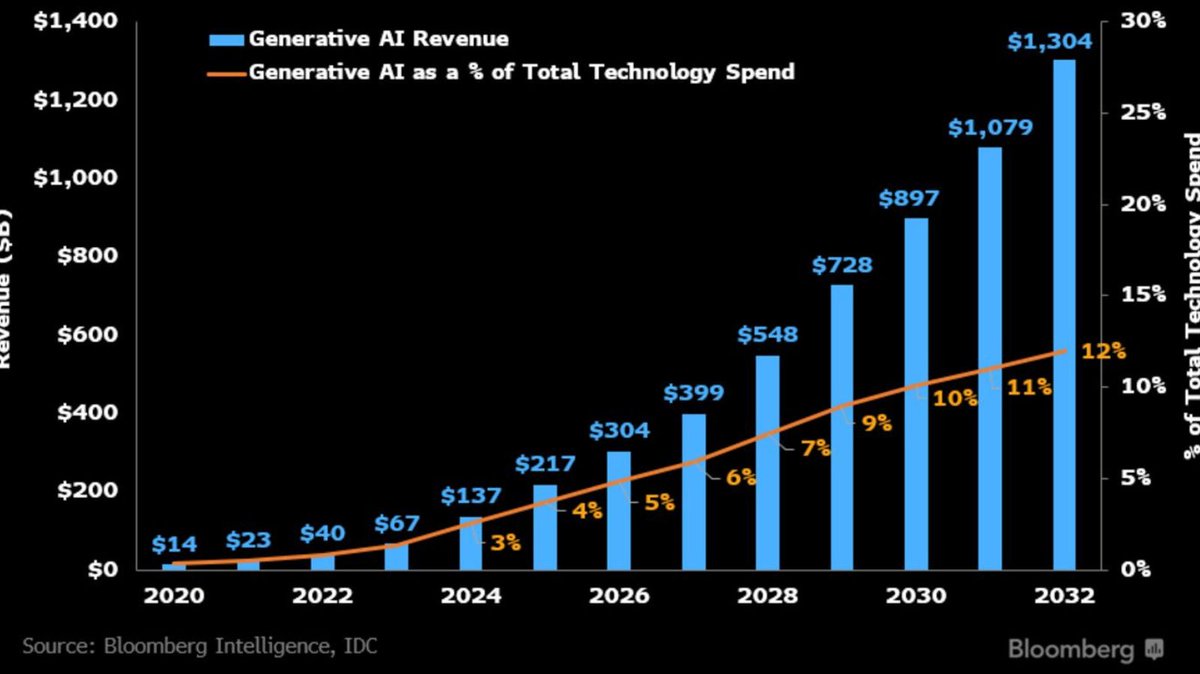

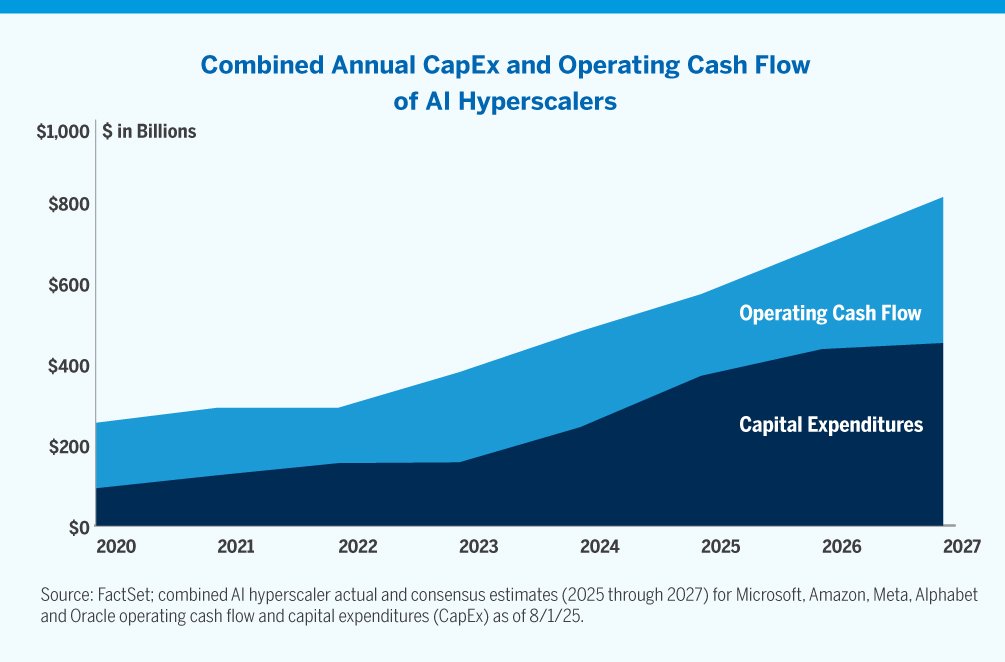

We are not in a bubble.

The amount of money going into AI infrastructure right now is huge, but it’s being financed in a fundamentally different way from a classic market bubble. Instead of being built on easy credit and hype, it’s being funded mostly by real cash flow from large, profitable companies.

The biggest spenders are the major cloud platforms such as “the hyperscalers". These companies already generate massive amounts of operating cash every year. They are paying for rising AI capex directly from their own balance sheets, not from borrowing on a risky scale.

According to Goldman Sachs, hyperscalers now make up a very large share of total S&P 500 capital spending. By 2026, total S&P 500 cash spending is expected to reach roughly $4.4 trillion, with most of that growth coming from investment in equipment, infrastructure, and R&D. In other words, corporate spending is shifting toward long-term, productive investments rather than short-term financial engineering like buybacks.

When Jensen Huang talks about $3–4 trillion of AI infrastructure by 2030, that’s not a random, hyped-up number. Major banks like JPMorgan Chase are running detailed models to figure out how that investment could realistically be financed. Their analysis shows that while it’s a big number, it can be covered through a mix of internal cash flow growth, rising private capital investment, and moderate use of debt.

What makes this build-out credible is that AI investment is already producing measurable productivity gains. Independent studies, including work by McKinsey & Company, estimate that AI could create trillions of dollars in value annually across industries. Companies deploying AI are reporting clear time savings per worker, better output per dollar spent, and faster production cycles. That means a portion of today’s capex is directly buying future earnings potential.

Another important difference from past bubbles is who’s putting up the money. A lot of the financing is coming from private markets and infrastructure investors. This capital is mostly being directed at real, income-producing assets. Things like data centers, power generation, fiber networks, and chips. These are tangible investments with collateral and long-term contracts. This matters because in a true bubble, prices float far above any underlying income or asset value. Here, the investments are anchored to physical infrastructure and real returns.

During the Dot-com bubble of the late 1990s and early 2000s, huge sums of money poured into internet companies that had no revenue, no profits, and no real plan to ever make money. A lot of that funding came from speculative capital and debt. When the hype broke, there was nothing solid underneath to support valuations and the market collapsed.

Today looks very different. The macroeconomic and policy backdrop supports productive investment. Tax incentives make equipment and R&D cheaper. Large corporations have strong cash positions and can shift money from buybacks to capex without relying on risky borrowing. That kind of investment raises future output which is the opposite of the 1990s, when many companies were burning cash on unproven ad-driven models that never scaled profitably.

This doesn’t mean there’s no risk. There are concentrated exposures among a few very large companies, plus challenges around power supply, grid constraints, and high valuations in some smaller or early-stage AI names. These can create sharp corrections in specific parts of the market. But the key ingredients of a system-wide bubble, excessive speculative credit, leverage spread across many sectors, and massive investment in assets with no economic value are largely missing from the AI capex core.

What’s happening instead looks more like the early phase of a structural shift in how companies spend their money. Moving from financial engineering (buybacks) toward building real assets that raise productivity and earnings.

88

162

970

113,524

Datacenex Recruitment retweeted

15 Jan 2025

Energy limitations in the US are a bigger bottleneck for AI advancement than the availability of GPUs. Decentralized distributed training is the answer.

This fact is not priced in.

benzinga.com/markets/cryptoc…

2

14

112

3,628

Datacenex Recruitment retweeted

15 Jan 2025

Big Breaking News!

Reliance Jio and Polygon Labs Join hands together to explore Web3 technologies.

This is a significant development, considering Jio has 450 million users and is the largest telecom player in the world.

Congratulations, team @0xPolygon. This is huge!

41

164

1,012

41,585

Datacenex Recruitment retweeted

15 Oct 2024

Ex-Google CEO Eric Schmidt tells UK PM Keir Starmer that building more AI data centers and investing in the energy infrastructure to power them will paradoxically solve energy issues much quicker

32

116

680

61,252

Datacenex Recruitment retweeted

3 Dec 2024

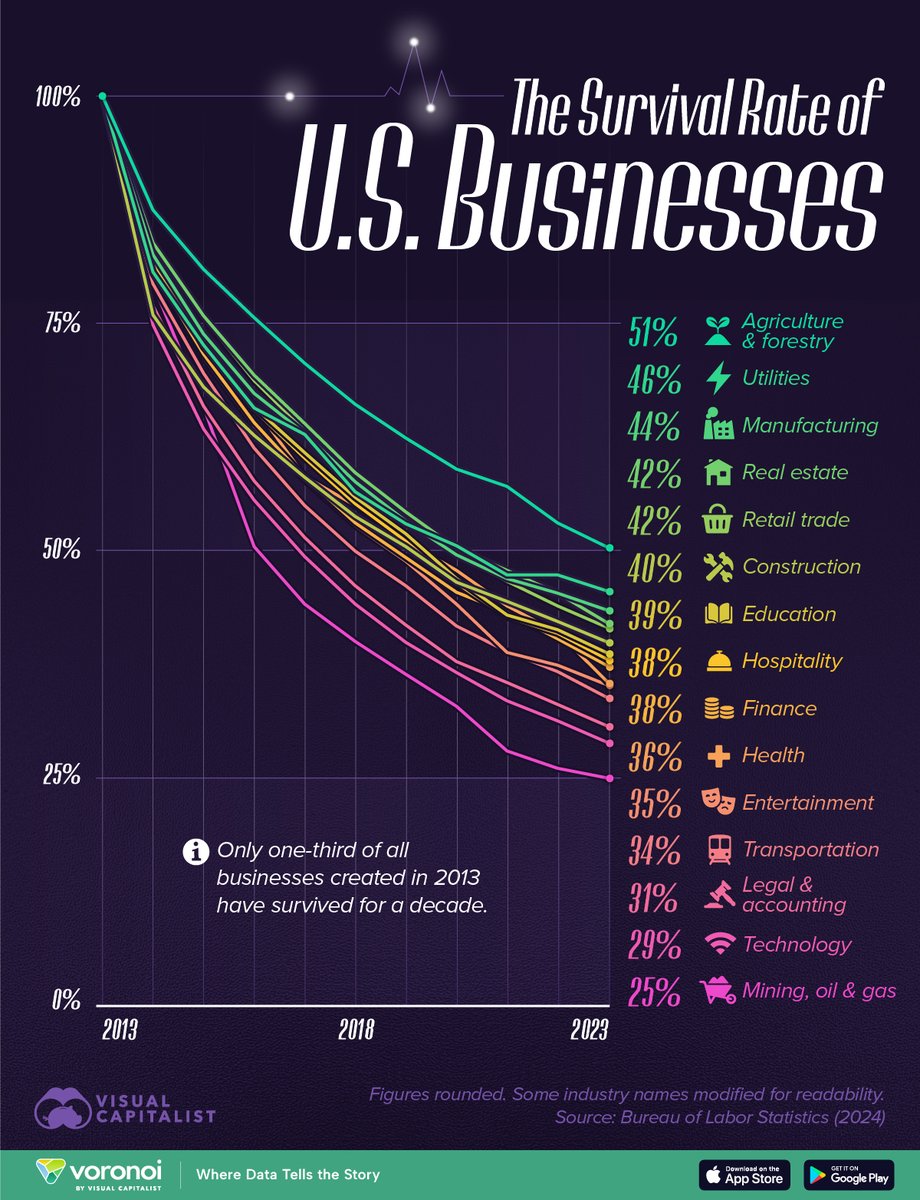

Charted: The Survival Rate of U.S. Businesses (2013-2023) 💼

🔍Discover more visual insights daily on the @VoronoiApp.

voronoiapp.com/business/This…

4

54

204

22,102

Datacenex Recruitment retweeted

21 Oct 2024

Obama: With Bitcoin, everyone is walking around with a Swiss bank account in their pocket.

698

689

4,332

659,541