The DeFiTimeZ is a FREE weekly digital Magazine . download here for free defitimez.com join our telegram t.me/DeFiTimeZ

Joined May 2023

- Tweets 7,161

- Following 963

- Followers 4,166

- Likes 12,799

718 Photos and videos

Pinned Tweet

I spent the last week breaking down why the global financial system is far more fragile than we’re told.

No leaks. No opinions. No predictions.

Just what central banks, institutions, and history have already admitted — in their own words.

This is a 6-part breakdown. Share it with your friends and family

Start here 👇

Happy New Year Everyone!

THE SYSTEM SERIES — PART 1

This Is Not Stability. It’s a Financial System Being Held Together

Most people think a financial collapse looks like a sudden event.

A crash. A headline. A breaking-news moment.

That’s not how modern financial systems fail.

They weaken quietly.

Not in public panic — but in official language.

Not in screams — but in carefully chosen words like “stability,” “support,” and “temporary measures.”

For years now, the institutions responsible for global finance have been telling us — in reports, speeches, and press releases — that the system is under strain. They don’t say it plainly. They don’t need to. The message is already there if you know how to read it.

Because when a system is truly strong, it doesn’t need constant reassurance.

It doesn’t require emergency tools that never go away.

And it doesn’t survive by rolling problems forward year after year.

What we’re living inside today isn’t stability.

It’s something else entirely.

And the most unsettling part?

The people running the system have been admitting it for a long time.

The quiet language of fragility

At the center of global financial coordination sits the Bank for International Settlements, often described as the central bank for central banks.

Its role is not political.

Its language is not emotional.

And its publications are not written for the public.

Which is exactly why they matter.

Across years of BIS reports and reviews, the same phrases appear again and again:

“Heightened systemic risk”

“Persistent liquidity stress”

“Elevated financial fragility”

“Extraordinary policy measures”

This isn’t alarmism. It’s technical language. And translated into plain English, it means one thing:

The system cannot operate on its own anymore.

When “emergency” stopped meaning temporary

Before 2008, central banks treated emergency measures as last resorts.

After 2008, they became policy.

Quantitative easing was introduced as a short-term fix.

Zero interest rates were framed as exceptional.

Balance sheet expansion was described as reversible.

None of those conditions were ever restored.

Instead, emergency tools were normalised, expanded, and re-used — again and again — each time with more urgency and less resistance.

By 2020, the response wasn’t debated. It was automatic.

That tells us something important:

the system no longer absorbs shocks — it avoids them.

What “stability” really means

When central banks speak about financial stability, they are not talking about household security or long-term prosperity.

They are talking about:

banks remaining liquid

markets continuing to function

payments clearing without interruption

Stability, in this context, means preventing sudden failure — not eliminating risk.

A system that requires permanent intervention to avoid collapse is not stable in the way most people understand the word. It is managed fragility.

The media has been signalling it too

Mainstream financial media has echoed this tone for years.

Headlines regularly warn of:

banking stress

credit tightening

confidence shocks

market dislocations

The language is always conditional:

if conditions worsen

if liquidity dries up

if confidence erodes

Those aren’t hypotheticals.

They’re pressure points.

Why this matters

You don’t need secret meetings to see what’s happening.

When institutions repeatedly acknowledge fragility, dependency, and risk — while insisting everything is under control — they are telling you exactly how close to the edge the system operates.

Modern finance no longer fixes problems.

It manages them forward.

That works — until trust breaks.

What comes next

This series is not about panic or prediction.

It’s about documentation.

In the next parts, we’ll show:

how debt became the operating system

why emergency measures became permanent

who really funds the system

and where pressure begins to build when confidence shifts

Only then will we explore why alternatives — including crypto — exist at all.

Not as ideology.

As response.

Up next: Part 2 — When Emergency Measures Became the New Normal

1

6

13

601

Apr 17

Michael Saylor: Genius or Pyramid Schemer? Here's Everything You Need To Know — In Plain English

There is a man called Michael Saylor. He runs a company called Strategy, formerly known as MicroStrategy. For years he stood on stages around the world and said one thing louder than anyone else in the room. Buy Bitcoin. Never sell it. Bitcoin is the future of money. Bitcoin is digital gold.

People listened. People trusted him. And then he built something that has the entire financial world asking a very simple question.

Is this the smartest trade in the history of money? Or is it the most elegant pyramid scheme ever constructed?

We are going to explain it simply. No jargon. No complicated finance words. Just the plain truth of what is happening — and then you can decide.

First. What Does Strategy Actually Do?

Strategy is not really a tech company anymore. It is a Bitcoin buying machine.

Saylor's company currently holds over 780,000 Bitcoin. That is worth roughly $54 billion at today's prices. No other public company on earth holds anywhere near that amount.

He buys Bitcoin. He never sells it. That is the whole strategy. His bet is simple — he believes Bitcoin will one day be worth one million dollars per coin. If he is right, Strategy becomes one of the most valuable companies in history.

But here is the problem. Buying that much Bitcoin costs a lot of money. And Strategy does not make enough money from its actual business to fund it. So Saylor built a machine to pull money in from investors. Several machines, actually.

The Jar. A Simple Way To Understand STRC.

Imagine a jar sitting on a table.

Saylor says to you — put your money in this jar. Every single month, I will take some money out of the jar and pay it back to you as a reward. Right now that reward is 11.5% per year. So if you put in $1,000, you get roughly $115 a year paid back to you monthly in cash.

Sounds good. So you put your money in.

Saylor then takes most of what is in the jar and buys Bitcoin with it.

Next month he needs to pay you your reward. But the jar is mostly empty — he spent it on Bitcoin. So he goes and finds new people to put money into the jar. Their money pays your reward.

Then the month after, he needs to pay everyone again. So he finds more new people.

This product is called STRC. It is a preferred stock that trades on the Nasdaq stock exchange. It pays 11.5% annually, monthly in cash. It has already raised over $6.4 billion. Record trading volumes of $1.6 billion in a single day have been reported this week alone.

Saylor calls it his iPhone moment. The greatest capital markets product ever created.

But Wait. It Gets Bigger.

STRC is not the only jar on the table.

Saylor has built four of them. Each one pulls money in from a different type of investor. Each one promises to pay those investors a yield. All of them funded the same way.

STRK — Strike. Pays 8% per year, quarterly in cash. Has a special feature — if Strategy's common stock hits $1,000, you can convert your holding into shares. Raised $563 million.

STRF — Strife. Pays 10% per year, quarterly in cash. No conversion feature. Pure income product aimed at pension funds and conservative investors. The safest of the four. If Strategy misses a payment on this one, the missed amount compounds — growing at up to 18% until it is paid. Raised $711 million.

STRD — Stride. Pays 10% per year. Most junior of all — meaning in a crisis it is last in line before common shareholders. The most dangerous one to hold. If a payment is skipped, it simply disappears — it does not roll forward or compound. It is gone. Raised nearly $1 billion.

STRC — Stretch. The newest and largest. 11.5% variable rate, adjusted monthly, paid in cash. $6.4 billion market cap and growing fast.

Add it up. Over $1 billion per year being paid out across these four products to investors. Every single year. Growing.

Where Does That Money Actually Come From?

This is the most important question. And we have the answer directly from Strategy's own legal filings with the US Securities and Exchange Commission.

Strategy filed with the SEC confirming it has no earnings and no profits — and does not expect to have any for the foreseeable future. Their exact words cover a ten year horizon. Ten years.

So it is not profits paying those dividends. It is not revenue from selling products. The SEC filing uses a specific phrase — return of capital. They are paying investors back with money that came from other investors.

Here is how the machine actually works. Strategy sells shares of its common stock — ticker MSTR — to the market. Investors buy those shares at a premium because they believe Bitcoin is going to keep rising and owning MSTR gives them exposure to that. The cash from selling those shares goes into a reserve pool. That reserve pool pays the dividends across all four preferred products.

The reserve currently holds $2.25 billion. Enough to cover roughly two and a half years of payments if the whole machine stopped tomorrow.

But the machine is not stopping. It is accelerating.

The Bitcoin He Cannot Touch

Here is the part that should make you stop and think.

Saylor owns 780,000 Bitcoin. At $1 million per coin — his dream — that stack is worth $780 billion. Enough to pay every obligation he has ever created a thousand times over.

But he cannot sell it.

The moment he sells even a fraction of that Bitcoin, the price drops. The moment the price drops, investor confidence in MSTR drops. The moment MSTR drops, the premium he sells shares at shrinks. The moment that premium shrinks, the machine has less fuel to pay its investors. The moment investors stop trusting the machine, they stop putting money in the jar.

The entire structure depends on Bitcoin going up. Forever. And Saylor never selling. Ever.

The Bitcoin is the crown jewels of the empire. Everyone can see them. Nobody can spend them.

The Genius Case

Let us be completely fair here. Because there is a genuine argument that this is not a scheme at all. It is a visionary bet.

Saylor only needs Bitcoin to grow at 2.05% per year on average to cover all dividend obligations indefinitely without selling a single coin. Bitcoin's historical average annual return is many times higher than that.

BlackRock holds STRC. Fidelity holds STRC. VanEck holds STRC. These are not naive investors. They are the most sophisticated institutions on earth. They looked at the structure and decided it was worth owning.

If Bitcoin reaches $1 million per coin — and serious analysts believe it will within this decade — Strategy becomes the most powerful financial institution ever built by a private individual. Every product Saylor created looks like genius. Every investor who held on gets paid. The jar never runs out because the Bitcoin backing it is worth more than anyone ever imagined.

The Other Case

Now let us be equally fair in the other direction.

New money is paying old money. That is a fact confirmed by Strategy's own SEC filing — not speculation, not a conspiracy theory. The company itself says it has no earnings. The dividends are classified as return of capital.

The products carry no FDIC insurance. No government protection. STRC holders cannot get their money back from Strategy — they can only sell their shares to another investor. There is no redemption. If nobody wants to buy your shares on the day you need to sell them, you are stuck.

STRD holders can have their payments simply cancelled with no obligation to ever make them up. Skipped — gone — moving on. That is written into the terms.

STRF holders appear safer with the compounding penalty for missed payments — but that safety only exists if Strategy can actually find the cash to pay it. In a deep Bitcoin winter, that assumption gets tested.

The independent analyst Derin Olenik calculated that STRC obligations alone are growing at roughly 30% per month. He calculated that without selling Bitcoin, Strategy would eventually need to issue over one billion new MSTR shares to cover preferred dividends — diluting existing shareholders by nearly 400%. He called it, bluntly, Digital Kamikaze.

Popular investigator Coffeezilla took the story mainstream this week, warning that Strategy's CEO recommended STRC as a savings product for ordinary people — including those living paycheck to paycheck. Coffeezilla's response was simple. This is not fixed income. It is not insured. It is not a savings account. And the dividend is not guaranteed.

So What Is It?

Here is what we know as fact.

Michael Saylor built a machine that takes money from investors, pays them a yield of 8 to 11.5% funded by selling new shares, and uses the rest to buy Bitcoin that he will never sell — hoping that one day the value of that Bitcoin makes every obligation he ever created look like small change.

He has done this across five products simultaneously. He has persuaded BlackRock and Fidelity to participate. He has processed over $1.6 billion in trading volume in a single day. He has bought 780,000 Bitcoin — more than any company on earth.

He is either the greatest capital allocator of his generation. A man who saw Bitcoin's destiny before anyone else and engineered a machine to accumulate as much of it as humanly possible before the rest of the world caught up.

Or he is using other people's money to keep buying Bitcoin — building his company's value on a rising asset he cannot sell, paying investors with new investor money, and betting his entire empire on a number going up forever.

The products are real. The yields are real. The Bitcoin is real.

But the money to pay you comes from the person who buys in after you.

You decide.

@coffeebreak_YT @saylor

2

5

12

271

Apr 16

I'm Hearing Projects Are Losing Their Accounts — Is X Clearing The Board?

The question is coming from everywhere in the space right now. Projects tagging their own tokens, getting locked out. Accounts discussing crypto for the first time, suddenly frozen. Developer access to platforms built on engagement-based token models, terminated. People are connecting dots and drawing conclusions — @elonmusk is clearing the board before launching his own play.

Let's look at what is actually happening, because the facts tell a more nuanced story than the panic suggests.

What's Actually Happening — Two Separate Crackdowns, Not One

The confusion stems from two distinct policy moves happening in close succession, which have merged in the community's mind into a single narrative.

The first came in January 2026. @nikitabier, X's Head of Product, terminated developer access to so-called "InfoFi" projects — platforms that rewarded users with tokens for posting on X. Projects like Kaito, Cookie DAO, and Loud saw their tokens drop between 11% and 15% within thirty minutes of the announcement. Bier was direct about the reason: these systems were incentivising repetitive, low-quality content at scale. He even offered displaced developers help transitioning to Threads or Bluesky. That is not the language of someone trying to bury a competitor quietly.

The second crackdown came on April 1st, 2026 — and despite the date, it was not a joke. @nikitabier announced that X would implement an automatic account lock for any account posting about cryptocurrency for the first time in its history. Those accounts would then be forced through identity verification before being allowed to post again. The trigger is first-time crypto posting only. Established accounts with a history of crypto discussion are completely unaffected.

Crypto Twitter Did This To Itself

Here is the uncomfortable truth the community does not want to hear: crypto Twitter has been drowning in its own slop for years. Engagement-farming bots, tokenised reply guys posting "gm" one thousand times a day, coordinated raids on comment sections to pump obscure tokens. Legitimate projects — the ones actually building — have been fighting for visibility in a feed polluted by incentivised noise.

X is not wrong on the InfoFi ban. Rewarding users financially for posting created a systematic incentive to generate garbage. The platform was being gamed, and the broader crypto community's credibility was suffering for it. @nikitabier called it bluntly: "Crypto Twitter is dying from suicide, not from the algorithm."

Smart Policy, Poorly Communicated

The first-post auto-lock is, when you read it carefully, a smart and targeted measure. The playbook for crypto account scams is well documented: phish a legitimate account via a fake copyright email, steal the credentials, then immediately blast the audience with fraudulent token promotions. The window between account takeover and damage is minutes. X is closing that window.

The context matters here too. In 2025, X was hit with a €120 million fine by the EU under the Digital Services Act over verification failures. Regulators were watching. Documented cases of high-profile account hacks — the Cardano Foundation account posting fake SEC lawsuits, Drake's account being used to pump a memecoin to $5 million in trading volume, the Animoca Brands co-founder's account hijacked to shill fake tokens — had made the problem impossible to ignore.

The legitimate concern is false positives. New projects, researchers, journalists entering the space for the first time will hit a verification wall. That friction is real and worth acknowledging. But the target of this policy is hijacked accounts and fresh sockpuppets — not your token project's community manager posting for the first time.

The 10K Verification Play Nobody Is Talking About

Here is something that has been largely missed in the coverage: the requirement for accounts over 10,000 followers to undergo ownership verification is not just an anti-scam measure. It is the foundation of a premium, verified crypto audience that X can sell to advertisers.

Right now, crypto advertisers on any platform are buying reach into an audience contaminated with bots, fake accounts, and engagement-farmed followers. A verified, identity-confirmed audience above 10K is a fundamentally different product. X is not destroying the crypto advertising market — it is building a cleaner, more credible version of it that commands higher rates.

For crypto media and legitimate projects, this is actually good news. Fewer bots means your real audience matters more. Verified reach commands premium value.

They're Not Evicting Crypto. They're Building A Mall.

While the community has been focused on what X is taking away, the build happening underneath has been largely ignored. Smart Cashtags — announced by @nikitabier in January 2026 — will deliver near real-time price data for any asset minted on-chain, including small-cap tokens not listed on major exchanges. Users will be able to trade stocks and crypto directly from their timeline. X Money, @elonmusk's payments platform, is in live internal testing with a public beta expected imminently.

X has obtained money transmitter licenses across multiple US states. It is partnering with Visa on its digital wallet infrastructure. @elonmusk has said plainly: "This is really intended to be the place where all the money is."

They are not clearing crypto off the platform. They are clearing the street market to build a regulated, monetised financial ecosystem on top of it.

What's In The Code Doesn't Lie

Now for the detail that adds a layer of intrigue to all of this.

A community account known as X Updates Radar, which monitors changes pushed to X's open-source code, discovered references to "x coins" and "diamonds" embedded in the platform's algorithm. The exact language found in the code: "Diamonds get accumulated by receiving coins on eligible posts. Money earned from diamonds gets added to your estimated earnings." The find was amplified publicly by @AltcoinDailyio's Aaron Arnold, who described it as "a very, very big deal."

When asked directly, @elonmusk denied that this indicated any plan to launch a native X token.

We are reporting the code finding as fact. We are reporting the denial as fact. What sits between those two facts — we leave to you.

The questions the community is asking are reasonable: Will Dogecoin, Musk's long-favoured memecoin, be integrated as the payments rail? Will "x coins" become an in-app rewards currency rather than a tradeable token? Or is the infrastructure sitting in the code waiting for a moment that hasn't arrived yet?

Verdict

Is X clearing the board for its own crypto launch? Not exactly. But it is cleaning house — removing the low-quality noise, building a verified audience, constructing the payments infrastructure, and launching financial tools that put it at the centre of crypto activity rather than the margins of it. The crackdowns are real. The build is real. And somewhere in the open-source code, "x coins" and "diamonds" are sitting quietly, waiting. The CEO says there's no token coming. The code begs to differ. Watch this space.

4

12

329

DeFiTimeZ $DFTZ $SOL retweeted

Set a reminder for my Annual Birthday Roast come and give me your best @DundiesDistrict ! x.com/i/spaces/1AxRnaRPvrVxl

3

6

13

350

DeFiTimeZ $DFTZ $SOL retweeted

Ceasefire or Rearm? What Markets Aren't Pricing

Markets celebrated Tuesday night. Oil crashed 16%, Bitcoin surged to $72,700, $595 million in shorts got liquidated, and traders who had been sitting on their hands for 40 days finally exhaled. The narrative wrote itself — dealmaker Trump, pragmatic Iran, Pakistan the unlikely hero. Risk on. Buy everything.

But what if the ceasefire was never about peace?

The story markets ignored

While diplomats were shaking hands in principle and Pakistan's PM was posting victory tweets, a different story was quietly circulating inside the Israeli Defence Forces. Reports have emerged of soldiers refusing orders, citing commanding officers who are framing the current conflict not as a geopolitical campaign but as a Biblical one. A war of prophecy. A war that isn't supposed to end with a deal in Islamabad — it's supposed to end with something far more final.

This isn't fringe noise. Religious nationalist ideology has deep roots in Netanyahu's current coalition, the most right-wing government in Israel's history. The belief that this conflict is a precondition for the Messianic age — requiring full Biblical land control and the removal of existential threats — doesn't disappear because Trump announced a ceasefire on Truth Social.

Netanyahu was the first major leader to warn Trump against the deal. Israel's official position is that the ceasefire doesn't cover Lebanon. Israeli strikes continued even as Pakistan was brokering the pause. These aren't the actions of a government that wants two weeks to negotiate. These are the actions of a government that wants two weeks to restock.

What a fake ceasefire means for TradFi

Traditional markets have priced in de-escalation as the base case. The relief rally in equities, the collapse in oil, the drop in the 10-year yield to 4.2% — all of it assumes Islamabad on Friday produces something real.

It probably won't.

Iran's 10-point proposal and Washington's stated positions remain miles apart. There is no binding framework. There is no enforcement mechanism. There is no guarantee Israel — which is not formally party to the Pakistan-brokered deal — holds its fire for 14 days let alone beyond them.

If hostilities resume in two weeks the market reaction will be savage. Oil was at $75 before this war started. It hit $120 at peak. A ceasefire collapse doesn't take it back to $120 — it takes it higher, because the market will have learned that diplomacy doesn't work here. Energy stocks, defence contractors, and inflation hedges reprice violently. The Fed — which already priced out all 2026 rate cuts during the conflict — has no room to manoeuvre. Equity markets that just rallied hard get hit twice as hard on the reversal.

What a fake ceasefire means for DeFi

Crypto told us something important during 40 days of war. The Fear and Greed Index sat at 8. Five bearish posts for every four bullish ones. DeFi protocols contracted. Stablecoin deployment froze. On-chain activity tracked macro fear almost tick for tick.

The $180 billion in stablecoin supply sitting on Ethereum right now is dry powder — but it only deploys into risk if confidence holds. A ceasefire collapse in two weeks doesn't just reverse Tuesday's rally. It resets sentiment to levels worse than the war baseline because markets will have been caught leaning the wrong way twice.

DeFi's structural advantages — 24/7 liquidity, permissionless access, no market close — become vulnerabilities in that scenario. There is no circuit breaker on Uniswap. No trading halt on Aave. When sentiment flips at 3am on a Sunday because a missile alert sounds in Tel Aviv, on-chain positions liquidate in real time with no pause button.

The question markets should be asking

Is this a ceasefire or a resupply operation with a PR wrapper?

If commanding officers in the IDF are telling soldiers this war is Biblical, they are not telling them it ends in a negotiating room in Pakistan. They are telling them it ends on their terms, on their timeline, regardless of what any American president announces on social media.

Markets are pricing a deal. Smart money should be pricing a delay.

The next two weeks in DeFi and TradFi won't be decided in Islamabad. They'll be decided by whether the missiles stay grounded.

This is opinion. DeFiTimeZ covers the intersection of geopolitics, traditional finance, and decentralised markets. Follow us for continuing coverage.

Sound off your opinions in the comments?

2

5

11

332

DeFiTimeZ $DFTZ $SOL retweeted

That was pure market manipulation. Happy for anyone that won on that trade sorry for the people that believed that the war was over and the people of #Iran

Ceasefire or Rearm? What Markets Aren't Pricing

Markets celebrated Tuesday night. Oil crashed 16%, Bitcoin surged to $72,700, $595 million in shorts got liquidated, and traders who had been sitting on their hands for 40 days finally exhaled. The narrative wrote itself — dealmaker Trump, pragmatic Iran, Pakistan the unlikely hero. Risk on. Buy everything.

But what if the ceasefire was never about peace?

The story markets ignored

While diplomats were shaking hands in principle and Pakistan's PM was posting victory tweets, a different story was quietly circulating inside the Israeli Defence Forces. Reports have emerged of soldiers refusing orders, citing commanding officers who are framing the current conflict not as a geopolitical campaign but as a Biblical one. A war of prophecy. A war that isn't supposed to end with a deal in Islamabad — it's supposed to end with something far more final.

This isn't fringe noise. Religious nationalist ideology has deep roots in Netanyahu's current coalition, the most right-wing government in Israel's history. The belief that this conflict is a precondition for the Messianic age — requiring full Biblical land control and the removal of existential threats — doesn't disappear because Trump announced a ceasefire on Truth Social.

Netanyahu was the first major leader to warn Trump against the deal. Israel's official position is that the ceasefire doesn't cover Lebanon. Israeli strikes continued even as Pakistan was brokering the pause. These aren't the actions of a government that wants two weeks to negotiate. These are the actions of a government that wants two weeks to restock.

What a fake ceasefire means for TradFi

Traditional markets have priced in de-escalation as the base case. The relief rally in equities, the collapse in oil, the drop in the 10-year yield to 4.2% — all of it assumes Islamabad on Friday produces something real.

It probably won't.

Iran's 10-point proposal and Washington's stated positions remain miles apart. There is no binding framework. There is no enforcement mechanism. There is no guarantee Israel — which is not formally party to the Pakistan-brokered deal — holds its fire for 14 days let alone beyond them.

If hostilities resume in two weeks the market reaction will be savage. Oil was at $75 before this war started. It hit $120 at peak. A ceasefire collapse doesn't take it back to $120 — it takes it higher, because the market will have learned that diplomacy doesn't work here. Energy stocks, defence contractors, and inflation hedges reprice violently. The Fed — which already priced out all 2026 rate cuts during the conflict — has no room to manoeuvre. Equity markets that just rallied hard get hit twice as hard on the reversal.

What a fake ceasefire means for DeFi

Crypto told us something important during 40 days of war. The Fear and Greed Index sat at 8. Five bearish posts for every four bullish ones. DeFi protocols contracted. Stablecoin deployment froze. On-chain activity tracked macro fear almost tick for tick.

The $180 billion in stablecoin supply sitting on Ethereum right now is dry powder — but it only deploys into risk if confidence holds. A ceasefire collapse in two weeks doesn't just reverse Tuesday's rally. It resets sentiment to levels worse than the war baseline because markets will have been caught leaning the wrong way twice.

DeFi's structural advantages — 24/7 liquidity, permissionless access, no market close — become vulnerabilities in that scenario. There is no circuit breaker on Uniswap. No trading halt on Aave. When sentiment flips at 3am on a Sunday because a missile alert sounds in Tel Aviv, on-chain positions liquidate in real time with no pause button.

The question markets should be asking

Is this a ceasefire or a resupply operation with a PR wrapper?

If commanding officers in the IDF are telling soldiers this war is Biblical, they are not telling them it ends in a negotiating room in Pakistan. They are telling them it ends on their terms, on their timeline, regardless of what any American president announces on social media.

Markets are pricing a deal. Smart money should be pricing a delay.

The next two weeks in DeFi and TradFi won't be decided in Islamabad. They'll be decided by whether the missiles stay grounded.

This is opinion. DeFiTimeZ covers the intersection of geopolitics, traditional finance, and decentralised markets. Follow us for continuing coverage.

Sound off your opinions in the comments?

1

2

123

Iran-US Ceasefire: What It Means for Finance and DeFi

Forty days of war, a closed Strait of Hormuz, and markets on a knife edge. Then, just before Trump's 8pm Tuesday deadline, Pakistan brokered a two-week ceasefire — and global markets moved instantly and violently.

The immediate numbers

Oil plunged 16% to around $95 a barrel as the Strait reopened. Bitcoin surged to $72,700, up 5% in 24 hours. The move triggered $595 million in total crypto liquidations across 118,489 traders, with short positions accounting for around $427 million — the most aggressive short squeeze since early March.

Crypto-linked equities followed suit, with Strategy, Galaxy Digital, Coinbase and Circle all posting healthy gains. The 10-year bond yield fell to 4.2%, signalling reduced macro stress across the board.

What it means for traditional finance

WTI crude had surged 69% since hostilities began on February 28, while European natural gas prices rallied 61%, reflecting the combined effect of the Strait closure and strikes on power facilities across the region. The ceasefire removes that war premium — at least temporarily.

But analysts are cautioning against reading this as an all-clear. Ras Laffan, the world's largest LNG export complex, had 17% of Qatar's export capacity knocked offline, with repairs expected to take three to five years. Infrastructure damage doesn't heal with a ceasefire announcement.

Iran's 10-point proposal — which Trump described as a workable basis for negotiation — reportedly includes the withdrawal of US combat forces from the region, the lifting of sanctions, and continued Iranian control over the Strait. The gap between both sides remains wide heading into Islamabad talks on Friday.

What it means for DeFi

The war exposed something important about crypto's relationship with geopolitical risk. The Fear and Greed Index sat at 8 throughout the entire conflict, with five bearish social media posts for every four bullish ones. DeFi protocols, stablecoins, and on-chain activity compressed alongside traditional risk assets. Decentralised finance is not yet decoupled from geopolitical fear.

The rally also highlighted DeFi's speed advantage. On-chain positions were liquidated and rebuilt within hours. Ethereum's stablecoin supply had already reached a record $180 billion — capital sitting ready to deploy the moment sentiment shifted.

The bottom line

This is a two-week pause, not a peace deal. The Islamabad talks on April 10 will determine whether this becomes a genuine de-escalation or another false dawn. Whether Bitcoin breaks its $65,000 to $73,000 war range depends entirely on what those two weeks become.

For DeFi specifically, the lesson from 40 days of conflict is clear: liquidity retreats fast when fear spikes, and returns faster when it lifts. That dynamic is only going to intensify as the sector grows.

1

3

5

126

Set a reminder for War Money and Oil what’s the real story? Who has it and who needs it?! x.com/i/spaces/1yKAPMkmPpDxb

1

5

10

139

I've just launched a Free Tarot Bot in the DeFiTimeZ Telegram group t.me/DeFiTimeZ go and check it out get a Celtic Cross reading by typing /reading give it a try and let us know what you think? #Tarot #CelticCross #TarotReading

4

6

339

Mar 31

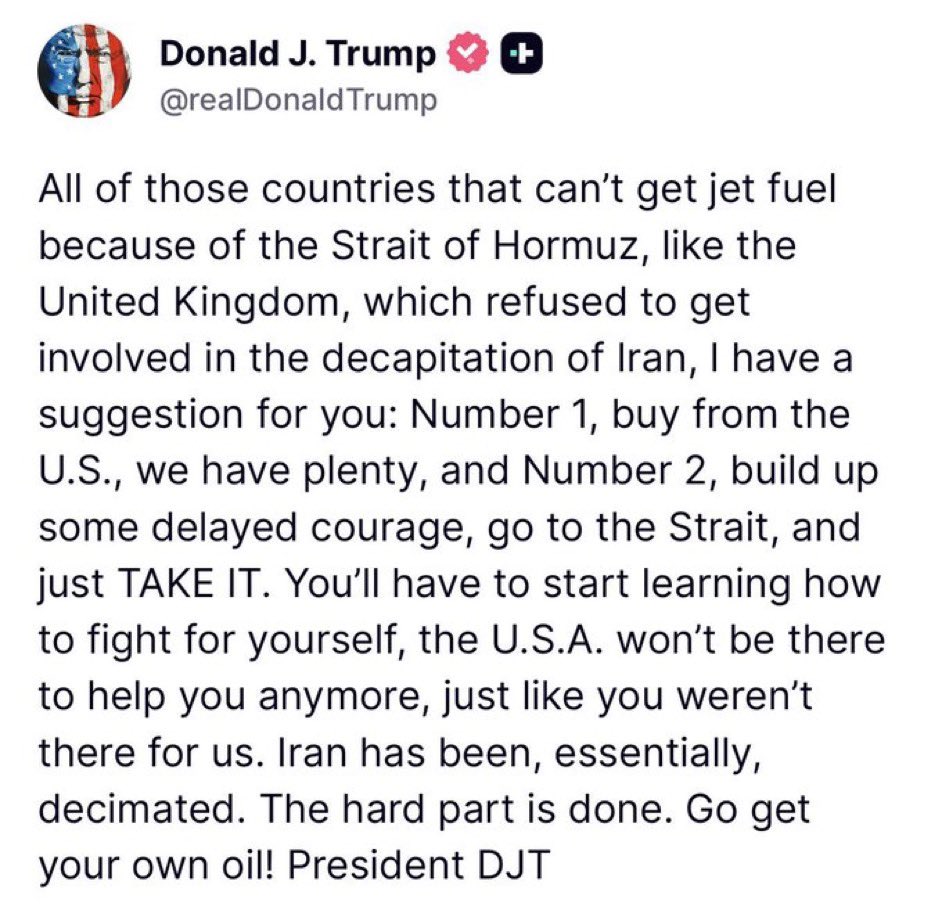

I think someone needs to tell the Donald that the UK has followed America into all of their dumb wars but we took on Argentina on our own and won! The UK doesn’t need your help Bruh

1

1

1

58

DeFiTimeZ $DFTZ $SOL retweeted

Mar 31

Set a reminder for HipHop Spotlight Kick Push to Conscious King The Lupe Fiasco Legacy! x.com/i/spaces/1XxygmQbboPGM

1

7

9

140

DeFiTimeZ $DFTZ $SOL retweeted

Mar 29

🚨 ON THIS DAY IN HIP HOP HISTORY 🚨

March 29, 1988 —

🎤 DJ Jazzy Jeff & The Fresh Prince dropped He’s the DJ, I’m the Rapper.

It won the first Grammy EVER for Best Rap Performance. Will Smith was just getting started. The culture got its first official Grammy recognition. 🏆

1

3

5

125

Mar 25

🚨 So 4 Private Ambulances were burned in London this week?

And those Ambulances were insured?

And a GoFundMe has already raised over £1,000,000 from the public?

So @wesstreeting — you've pledged to replace ALL 4 Ambulances with taxpayer money AND loan them 4 working Ambulances to use RIGHT NOW?

Just so we're clear…

The same government that can't fix NHS ambulance response times — where if YOU have a heart attack tonight, you're looking at a 1 hour 30 minute wait for an ambulance that may never come in time…

That same government found the budget for this. Immediately. No debate. No waiting list.

50,000 people died last year from long A&E waits in England.

Did they get replacement ambulances?

Up to 2 in 5 NHS ambulances are currently off the road due to age and disrepair.

Did those trusts get an immediate government pledge?

I'm just asking questions. 🤷🏾♂️

Because the people of Britain deserve the same urgency, the same speed, the same political will that was shown this week — every single day.

Not just when the cameras are rolling.

Not just when it's politically convenient.

Every. Single. Day.

Thank The Lord for #SatoshiNakamoto for giving us Blockchain and @VitalikButerin for giving us DeFi — at least we can make our money decentralised even if our government clearly isn't working for all of us equally.

SMH 🤦🏾♂️

#NHS #London #Hatzola #DeFi #Web3 #DFTZ

2

3

7

88

DeFiTimeZ $DFTZ $SOL retweeted

Mar 23

Set a reminder for HipHop Spotlight Still Not a Player to Latin Legend The Big Pun Legacy! x.com/i/spaces/1yxBeMzykEoJN

7

13

154

Mar 14

THE INVISIBLE BAILOUT: How the Rot from 2008 Is Surfacing in 2026

The 2008 financial crisis wasn't solved. It was papered over. The toxic debt didn't vanish — it migrated. It moved from the balance sheets of the Too Big to Fail banks into two new homes: the Federal Reserve, which absorbed trillions in bad assets through quantitative easing, and the unregulated shadow world of Private Credit and Private Equity, which expanded fivefold in the years that followed.

Now, in March 2026, the walls are closing in. What we are watching is not a routine market correction. It is the first full stress test of a $2 trillion private credit industry that was built in the era of near-zero interest rates, has never been through a real downturn, and whose participants have been selling everyday investors a promise of liquidity they cannot keep.

The public — already struggling with a cost-of-living crisis driven by years of inflation — is about to find out that the bill from 2008 was never really paid. It was deferred. And as history shows, when the reckoning finally comes, it is always ordinary people left holding it.

THE GATES ARE SLAMMING SHUT

The word the industry uses is "gating." In plain English: the doors are locked. You put your money in, you want it back, and you're told — not right now, and not all of it. In early 2026, gating is happening across multiple major funds simultaneously. The first time at this scale since the post-2008 era began.

BLUE OWL — February 2026

Before BlackRock and Blackstone made headlines, Blue Owl Capital became the early warning signal. In February 2026, Blue Owl permanently closed redemptions on its Blue Owl Capital Corporation II fund — a $1.6 billion retail vehicle that had promised investors quarterly access to their money. Withdrawal requests had surged over 200%. Rather than continue to gate, the fund shifted into an orderly liquidation — returning capital at a rate of its own choosing, not the investor's.

Blue Owl had tried to merge this fund with a publicly traded vehicle to give investors a clean exit. The deal collapsed when investors realised it would crystallise losses of roughly 20% on their holdings. Blue Owl's stock subsequently entered an 11-day losing streak, erasing approximately 60% of its value from its late-2024 highs. The retail investors who had been sold this fund as a "semi-liquid alternative" discovered that semi-liquid, when stress arrives, means illiquid.

BLACKROCK — March 6, 2026

BlackRock's $26 billion HPS Corporate Lending Fund received withdrawal requests equivalent to 9.3% of its net asset value in Q1 2026 — approximately $1.2 billion. The fund's structural quarterly cap is 5%, meaning BlackRock could only pay out around $620 million — roughly half of what investors requested. This was the first time this fund had ever breached its quarterly threshold since launch.

It is important to be precise here: the 5% cap is not a legal limit imposed by regulators. It is a contractual limit built into the fund's own structure — one that investors, many of them ordinary wealth-management clients, were told protected them. It does protect them from a forced fire sale of illiquid assets. But it also means that when stress hits, the fund is protected first. The investor waits.

BlackRock's share price fell nearly 7% on the day of the announcement. Contagion spread immediately to KKR, Carlyle, Apollo, and Ares — all down 5–6%. The market understood what the headlines were trying to soften.

BLACKSTONE — March 3, 2026

Blackstone's flagship $82 billion Blackstone Private Credit Fund (BCRED) faced $3.7 billion in withdrawal requests in Q1 2026 — equivalent to 7.9% of its net asset value, well above its standard 5% cap. Blackstone's response was different from BlackRock's: they raised the repurchase cap to 7% and injected $400 million of their own firm and employee capital to honour 100% of requests.

This is being presented as a show of strength. Look at it more carefully. When an $82 billion fund requires a $400 million emergency capital injection from its own executives just to process one quarter's withdrawal requests — that is not a sign of health. JPMorgan analysts described it as the first ever quarterly outflow in BCRED's history and "a significant expression of souring investor sentiment on direct lending." The spin is strong. The underlying signal is not.

MORGAN STANLEY — March 2026

Morgan Stanley's North Haven Private Income Fund capped redemptions, meeting only 45.8% of investor requests in Q1 2026. This is now industry-wide. BlackRock, Blackstone, Blue Owl, Morgan Stanley — these are not four isolated incidents. This is a pattern.

THE ZOMBIE COMPANIES HIDDEN INSIDE THE FUNDS

To understand why the gates are closing, you have to understand what is actually inside these funds — and why it cannot be easily sold.

Private credit funds lend directly to mid-sized companies, typically those too risky or too small to access traditional bank lending or public bond markets. In the era of cheap money between 2010 and 2021, these loans were made at floating rates and generous terms. When rates were near zero, borrowers could service their debt easily. When rates rose sharply from 2022 onwards, many of those same borrowers began to drown.

The International Monetary Fund's 2025 Financial Stability Report found that approximately 40% of private credit borrowers — up from 25% in 2021 — now have negative free cash flow. They are not generating enough money from their operations to cover their interest payments. To stay alive, many are using a mechanism called Payment-in-Kind (PIK): they pay their interest not in cash, but in additional debt. They are borrowing more money to pay the interest on the money they already borrowed. Public BDCs are now receiving nearly 8% of their income in PIK form — a figure analysts describe as a precursor to eventual default, not a sign of financial health.

These are zombie companies. Kept alive on paper. Valued at prices their underlying businesses cannot justify. Hidden inside funds marketed to retail investors as "diversified," "resilient," and "semi-liquid."

The software sector sits at the epicentre. Approximately 40% of all sponsor-backed private credit loans are concentrated in software companies. These businesses, valued on aggressive growth assumptions during the low-rate boom, are now facing two simultaneous pressures: higher borrowing costs and the genuine threat that artificial intelligence will disrupt or outright replace their products. It is a sector in distress that forms the backbone of a $2 trillion market.

JP MORGAN SOUNDS THE ALARM — March 11, 2026

On March 11, 2026, the Financial Times reported that JP Morgan had begun marking down the value of loans it holds as collateral on behalf of private credit firms — specifically those tied to software companies. JP Morgan acts as a bank to private credit funds, lending them money using their loan portfolios as collateral. By reducing the assessed value of that collateral, JP Morgan is shrinking how much these funds can borrow, heaping further pressure on an industry already grappling with mass redemption requests.

This is the "mark to model" problem made concrete. Private credit loans are not traded on open markets. There is no public price. Funds decide what their loans are worth using internal models. For years, those models kept valuations artificially stable. JP Morgan's decision to apply its own, lower valuations is a direct signal that the biggest bank in America no longer trusts the numbers these funds are producing.

JP Morgan's CEO Jamie Dimon had previously warned of "cockroaches" hiding in private credit and drawn explicit comparisons to the lead-up to 2008. His bank is now acting on that concern. When the largest bank in the United States starts pulling back — that is not noise. That is information.

THE DEBT THAT NEVER WENT AWAY

This private credit crisis does not exist in isolation. It sits on top of a national balance sheet that never truly recovered from the decisions made after 2008.

As of March 4, 2026, the total US gross national debt stands at $38.86 trillion. It is growing at an average of $7.23 billion per day. The Congressional Budget Office projects a fiscal year 2026 deficit of $1.9 trillion. Interest payments on the national debt are projected to exceed $1 trillion this year — more than the US spends on national defence or Medicaid. Interest is now the second-largest spending category in the entire federal budget, behind only Social Security.

That $1 trillion annual interest bill is the delayed invoice from years of money printing designed primarily to keep asset prices elevated and financial institutions solvent after 2008. The people who benefited most from that monetary expansion were asset owners. The people paying the cost — through inflation, higher taxes, and reduced public services — are everyone else.

The Federal Reserve's balance sheet currently sits at approximately $6.6 trillion — roughly five times its pre-2008 level of around $900 billion. That expansion represents the accumulated cost of buying toxic assets and government bonds to keep interest rates artificially low and financial markets artificially elevated. The Fed does not currently have an active emergency facility absorbing private credit loans. But the architecture for intervention already exists — and history is very clear about how policymakers use it, and in whose interests.

THE COMMERCIAL REAL ESTATE WALL

Layered beneath the private credit crisis is a separate but related detonator. According to the Mortgage Bankers Association, approximately $875 billion in commercial and multifamily mortgage debt is scheduled to mature in 2026. Much of it was originated in the low-rate era at terms that simply cannot be replicated today.

Office vacancy rates remain elevated. Refinancing conditions are significantly tighter. Some estimates put total CRE maturities across 2025–2026 as high as $1.5 to $1.8 trillion when loan extensions are factored in.

The strategy employed by lenders for the past two years has been "extend and pretend" — rolling over loans rather than forcing defaults and fire sales. That road is now running out. 2026 is being called the "sorting year," when lenders must finally begin distinguishing between assets that can be refinanced and those that cannot. The commercial real estate reckoning, like the private credit reckoning, is not a future risk. It is arriving now.

THE HIDDEN INFRASTRUCTURE OF BAILOUT

The word "bailout" conjures images of Congress voting on emergency legislation — a TARP moment, visible and debated. That is not how it works in 2026. The mechanisms are quieter, more technical, and harder to see.

The Federal Reserve Bank of Boston published research confirming that the growth of private credit has been funded largely by bank loans, and that banks have become a primary source of liquidity for private credit lenders — meaning banks retain indirect exposure to the credit risk of private credit loans even though they did not originate them. Moody's estimated that Wall Street banks had provided approximately $300 billion in financing to private credit funds as of mid-2025. JP Morgan alone carried $22.2 billion of direct exposure.

The Bank of Canada's Governor, speaking at the Global Risk Institute in March 2026, said plainly: "After the 2008–09 global financial crisis, we strengthened the regulation of banks, which made the system safer. As a result, riskier activities migrated to non-bank financial intermediaries. Risks have not disappeared — they have migrated. And our global surveillance and regulatory frameworks have not kept pace."

The Federal Reserve and the Financial Stability Oversight Council have now formed a "Market Resilience Working Group" to monitor the links between private credit and the traditional banking system. The fact that this body needed to be created in March 2026 tells you everything about how prepared regulators were for what is now unfolding.

YOUR PENSION AS THE EXIT RAMP

Private equity and credit firms have, in recent years, aggressively marketed "evergreen funds" to retail investors and pension savers. Non-traded BDCs — the exact vehicles now gating withdrawals — grew from essentially zero to over $200 billion in assets since 2021. The US recently gave regulatory approval for private credit managers to sell into the roughly $13 trillion defined contribution pension market.

The mechanism is straightforward. Wealthy and institutional investors who got into private credit early want to exit. The vehicle for that exit is the retail investor — the ordinary person whose financial adviser recommended a private credit fund as a yield-enhancing alternative. When the institutional money leaves and the gates close, it is the retail investor who discovers that the liquidity they were promised was always conditional on conditions that no longer exist.

INFLATION AS THE SILENT TAX

Every dollar printed to sustain asset prices — through quantitative easing, emergency facilities, or indirect support for the financial system — reduces the purchasing power of the currency held by ordinary people. The inflation of 2022–2025 did not come from nowhere. It was the delayed consequence of years of monetary expansion designed primarily to keep financial asset prices elevated. The people who benefited most from that expansion — asset owners — were insulated from its costs. The people who suffered most — wage earners and savers — had no such protection and no say in the decision.

WHAT 2008 ACTUALLY TAUGHT US

The 2008 financial crisis produced the largest peacetime government intervention in economic history. Banks were recapitalised. Asset managers were protected. Bonuses continued. And the fundamental dynamic that caused the crisis — the privatisation of gains and the socialisation of losses — was left entirely intact.

Private credit is, in many respects, a direct product of 2008. Tighter bank regulation pushed riskier lending activity out of regulated institutions and into unregulated shadow entities. Those entities grew fivefold over fifteen years, operating with less transparency, less oversight, and with ordinary investors' money increasingly at stake. The risk did not go away. It was reorganised, rebranded, and sold back to the public as an opportunity.

Now the cycle is completing. The entities that absorbed the risk from 2008's fallout are themselves under stress. And the question of who absorbs their losses — whether through formal bailout, quiet central bank intervention, or the slower mechanism of inflation silently eroding savings — will be answered in the months and years ahead.

History offers a consistent answer to that question. In 2008, it was not the traders or the executives who bore the cost of the crisis. It was the people who lost their homes, their jobs, and their savings. The billionaires who built and sold these private credit funds have already been paid. The question now is only how much of the bill gets passed to everyone else — and through which mechanism it arrives.

THE VERDICT

The crisis unfolding in March 2026 is real, documented, and significant. BlackRock has gated a $26 billion fund. Blue Owl has permanently closed a retail vehicle. Blackstone injected $400 million of its own capital to honour withdrawals. Morgan Stanley capped redemptions at 45.8%. JP Morgan is marking down collateral. The IMF has confirmed that 40% of private credit borrowers have negative free cash flow. The commercial real estate maturity wall is arriving. The national debt is growing at $7.23 billion a day. Interest payments have crossed $1 trillion per year.

This does not mean the system collapses tomorrow. Some institutions are better capitalised than in 2008. Regulators are watching, even if belatedly. But the pattern is familiar. Complexity obscuring risk. Retail investors sold promises of liquidity that the underlying assets cannot support. Institutions too interconnected to be allowed to fail. A government and a central bank whose tools for intervention are unlimited — and whose track record of using those tools to protect financial assets rather than the people who depend on them is well established.

The music has not fully stopped. But it is slowing.

And when it does, the same question asked in 2008 will be asked again: when the music stops, who is left without a chair?

The answer, as it has always been, is not the people who built the system.

Key facts: ▪ US national debt: $38.86 trillion (March 4, 2026) ▪ Debt growing at $7.23 billion per day ▪ Fed balance sheet: ~$6.6 trillion ▪ Annual interest on debt: projected to exceed $1 trillion in 2026 ▪ Private credit market size: ~$2 trillion ▪ 40% of private credit borrowers have negative free cash flow (IMF) ▪ BlackRock: $1.2B requested, $620M paid out ▪ Blackstone: $3.7B requested, honoured in full via $400M capital injection ▪ Blue Owl: redemptions permanently closed ▪ CRE debt maturing in 2026: ~$875 billion (MBA)

#PrivateCredit #Finance #Economy #2026 #WallStreet #TheInvisibleBailout @GeorgeGammon @LynAldenContact

1

1

2

283

DeFiTimeZ $DFTZ $SOL retweeted

Mar 12

🚨 ON THIS DAY IN HIP HOP HISTORY 🚨

March 12, 2007 —

🔥 Grandmaster Flash and The Furious Five made history

They became the first-ever hip hop group inducted into the Rock & Roll Hall of Fame. A legendary moment that proved the culture couldn't be ignored. 🎤

#OnThisDay

6

3

15

462

Mar 12

THE DIGITAL STICK OF GUM: Why GPK on WAX is the Ultimate NFT On-Ramp

Remember the smell of that brittle, pink rectangle of bubblegum at the bottom of a Garbage Pail Kids pack? It was hard as a rock and lost its flavor in thirty seconds, but it was a sacred ritual. You’d rip open the wax paper, toss the gum in your mouth, and pray to find an "Adam Bomb" to trade at recess.

Today, the playground has moved to the WAX blockchain. While the digital packs are missing that physical piece of gum, they’ve managed to do something even more impressive: they’ve bottled the lightning of 1985 and turned it into a high-tech "on-ramp" for the rest of the world.

Nostalgia is the Ultimate Utility

While the crypto world often gets bogged down in complex charts, the GPK NFT collection succeeds because it speaks a language we already know: The Joy of the Pull. When a "normie" enters the space, they aren't looking for a smart contract; they’re looking for that same dopamine hit they got forty years ago.

Topps and WAX have delivered this by creating digital cards that feel "alive":

The "Gum" Borders: In a brilliant nod to the missing snack, rare cards feature animated, drippy bubble-gum borders.

The Evolution of Art: "Sketch" cards animate the transition from a rough pencil drawing to a finished masterpiece.

Retro Visuals: The "VHS" rarity adds a layer of static and jitter that feels like a Saturday morning cartoon on a fuzzy tube TV.

A "No-Fear" Entrance to Web3

The real magic isn't just the gross-out humor—it’s the accessibility. For someone who has never touched a crypto wallet, the WAX Cloud Wallet feels more like a video game inventory than a bank account.

Proof of Ownership: Just like the unique code on the back of a physical card, every GPK NFT has a blockchain-verified history.

Community Trading: Platforms like AtomicHub have replaced the school cafeteria, allowing fans to trade "Slime" animated backgrounds and "Prism" sheens globally.

Inclusive Collecting: With various price points, it maintains the inclusive spirit of the original 1980s hobby.

The Future is Bright (and a little Gross)

The Garbage Pail Kids on WAX prove that the best way to move forward is by looking back. By focusing on the positive, fun, and nostalgic elements of collecting, Topps has created a blueprint for how legacy brands can thrive in Web3.

The physical gum might be gone, but the spirit of the 80s is more alive than ever. Whether you're a hardcore collector or a curious newcomer, opening a digital pack of GPK is a reminder that the blockchain can be a place of pure, unadulterated fun.

The gum might be missing, but the nostalgia is 100% authentic.

#DeFiTimeZ #GPK #WAX #NFTs #Web3 #Nostalgia @ToppsNFTs @Topps

2

2

3

180

DeFiTimeZ $DFTZ $SOL retweeted

🚨 ON THIS DAY IN HIP HOP HISTORY 🚨

March 8, 2003 —

🎯 50 Cent’s “In Da Club” hit #1 on the Billboard Hot 100.

It stayed there 9 weeks. Shot was fired. The 2000s belonged to Fif. 🔥

#OnThisDay #50Cent #HipHopHistory

1

4

6

168