Value Investor, Stocks Analyst, Deep Company Research, Student of the game

Joined December 2017

- Tweets 14,607

- Following 519

- Followers 17,002

- Likes 29,193

1,022 Photos and videos

Pinned Tweet

Paid subscription to my newsletter gets you:

- Articles with clear reasons why stock thesis will or won't work

- Focused on insights missed by the market

- Access view to my personal outperforming portfolio

- 24/7 chat

- Q&A

Join with the link below:

substack.com/@deepicevalue?u…

1

2

2,193

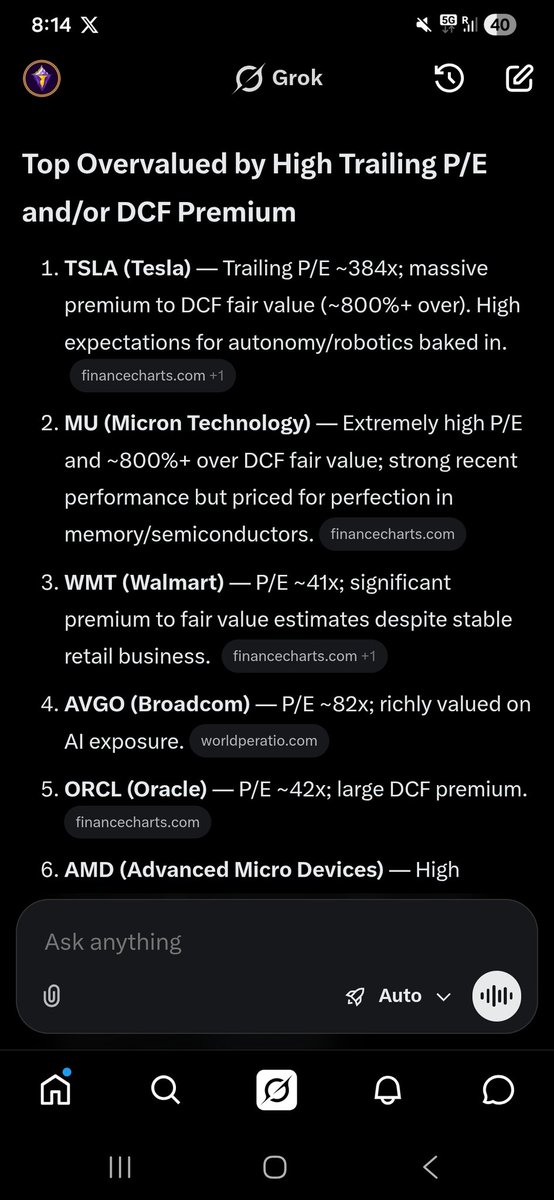

What are currently better investments than $MU?

45

1

35

19,602

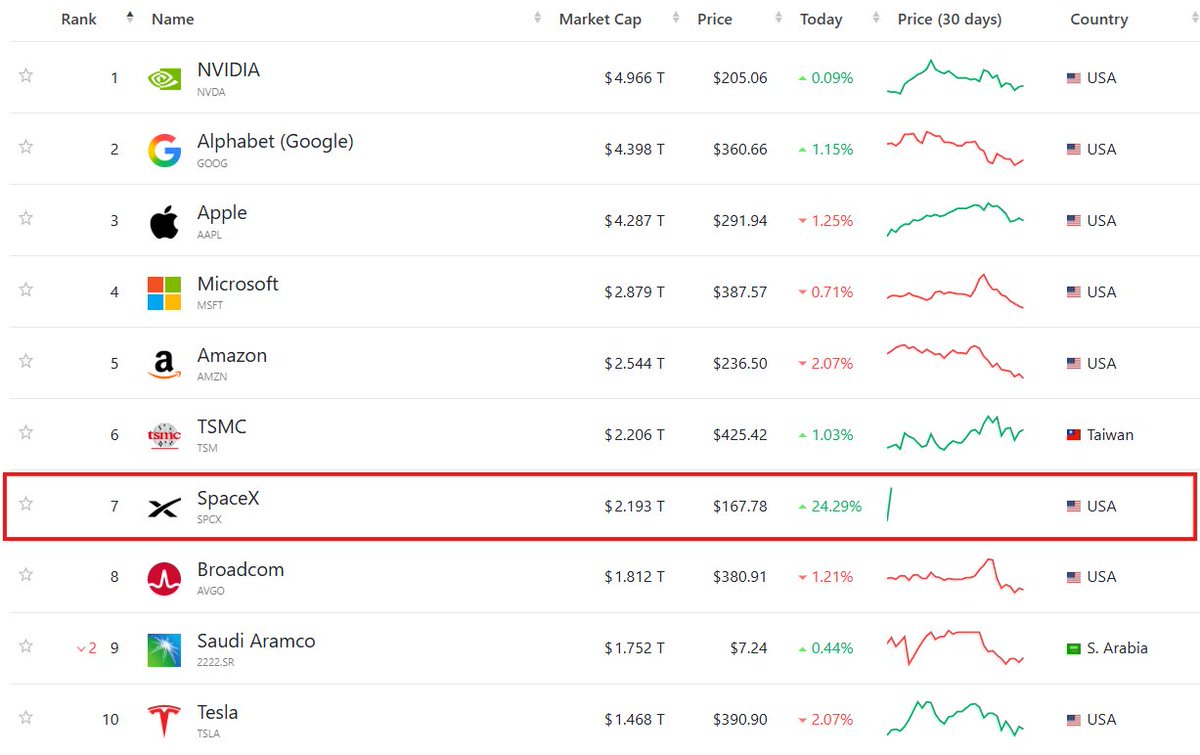

$Google owns approximately 6% of $SPCX!

Google initially acquired a roughly 10% stake in SpaceX during a $1 billion joint investment with Fidelity in 2015.

Over the years, that position has been slightly diluted by subsequent funding rounds, including a recent all-stock transaction for the acquisition of xAI..

$GOOG is up 0.28% after $SPCX IPO..

4

1

4

2,013

Good times to be 100% in stocks.. 🤑

2

5

1,424

$GLD, $NEM, $AEM, $B are flying under the radar..

I have barely heard anyone talk about gold $GLD. When gold was running, everyone had an opinion. When it pulled back, suddenly the room got quiet.

That silence is what interests me.

Gold is emotional. When it is rising, people talk about debasement, hyperinflation, central banks, currency collapse, and $10,000 targets. When it drops 15–20%, those same people often disappear.

But nothing fundamental changed in a month. The only thing that changed was the price.

And that is exactly why gold is hard.

I do think gold can go much higher over time. I would not be shocked to see $10,000 gold eventually. Currency debasement is real. Governments are not suddenly becoming fiscally disciplined.

Debt is not disappearing. Inflationary pressure is not some fantasy. Over the next 10 or 20 years, I think paper money will continue losing purchasing power.

But knowing that is not the same as having an investment strategy.

The key question for me is not, “Can gold go up?”

Of course it can.

The better question is: “Is gold the best vehicle for building wealth?”

That is where I struggle.

Gold does not produce anything. It does not pay me dividends. It does not grow earnings. It does not reinvest cash flow. If I buy one ounce of gold today, then 10 years from now I still own one ounce of gold.

That may protect purchasing power, but it does not automatically create more wealth.

A good business can compound. It can raise prices. It can grow earnings. It can pay dividends. It can buy back shares. It can turn one ounce of gold worth of capital into two ounces, three ounces, or more over time.

That is the difference.

Gold can absolutely outperform during certain periods. History shows that clearly. There are cycles where gold explodes higher and everyone who ignored it looks foolish.

But history also shows something else: after big speculative runs, gold can spend years, even decades, doing very little. During those periods, productive assets quietly keep compounding.

That matters to me.

I am not anti-gold. I understand why people own it. I understand the fear of currency destruction. I understand the argument for having real assets outside the financial system.

But my own wealth creation process is not built around sitting on metal and hoping the world gets worse.

My process is to own productive assets with a margin of safety.

For some people, gold is peace of mind. For others, it becomes a religion.

I think the dangerous part is confusing a macro thesis with a portfolio strategy.

Yes, currencies will likely lose value. Yes, gold may go much higher.

But the real question is whether I can find assets that do even better while producing cash along the way.

That is where I prefer to spend my time.

Gold may protect wealth. Great businesses can create it.

4

8

724

Guys $ADBE is currently trading below Covid lvls... 🤯🤯

- 12% revenue growth

- 18% EPS growth

- Fwd P/E 7.46

- Growing AI rev

- Raised guidance

Im buying more on monday..

5

11

1,913

$MELI is starting to look cheap.. Here is how I see it..

I’ve been spending time looking at MercadoLibre, and the more I study it, the more I see why investors often call it the Amazon of Latin America.

But honestly, that comparison may even undersell what the company is building.

This is not just an e-commerce marketplace. MercadoLibre sits at the center of a much larger digital ecosystem: marketplace, payments, logistics, merchant tools, advertising, credit, insurance, and fintech. In one company, you get pieces of Amazon, PayPal, Shopify, and a digital bank operating across a region with hundreds of millions of people and still-low digital penetration.

That opportunity is enormous.

Latin America still has plenty of room for e-commerce adoption, digital payments, formal credit, and online advertising to grow. MercadoLibre has already spent years building trust, infrastructure, and scale, which are not easy things to replicate in fragmented emerging markets.

The recent numbers still look strong to me. Revenue growth remains very high, items sold continue to rise, and engagement across the platform is improving.

The market, however, seems focused on margin pressure. That is understandable, but I don’t think it tells the full story.

A company growing this fast often has a choice: maximize short-term profits or reinvest aggressively to expand the moat.

MercadoLibre appears to be choosing reinvestment. Logistics, credit, fintech, and customer acquisition are expensive today, but they can create a much stronger business tomorrow.

That said, valuation matters.

I don’t want to justify any price just because the business is excellent. For a conservative valuation, I prefer to assume growth slows over time and use a reasonable terminal multiple.

Under cautious assumptions, the stock may not look obviously cheap. Under stronger growth assumptions, it can still produce attractive long-term returns from here.

That is the challenge with MercadoLibre. Small changes in growth expectations can create huge differences in valuation.

I also have to respect the risks. Latin America is cyclical. Currencies can move sharply. Political and economic instability can hurt sentiment. Competition from Amazon, Temu, Shein, local players, and fintech challengers is real.

The credit business adds another layer of risk if underwriting gets too aggressive.

So for me, this is not a “back up the truck at any price” situation. It is a high-quality compounder that deserves a place on the watchlist and possibly a modest portfolio position if the price and expected return make sense.

If I owned it, I would size it carefully, probably start small, and be prepared for volatility.

A 40% or 60% drawdown would not shock me in a business like this, especially if growth stocks or Latin American markets fall out of favor.

My takeaway: MercadoLibre is one of the most interesting growth platforms in the world. I just want to own it with discipline, not excitement alone.

7

12

1,769

5

3

1,316

Can $MSFT survive this AI revolution?!

When a giant falls hard, my first instinct is not “how much can it bounce?”

It is: what am I actually buying, and what has to go right for me to earn a good return?

A return to old highs can look exciting on paper. But that is not investing logic by itself. That is just anchoring to a previous price.

For me, the real debate is Microsoft’s future cash generation versus the amount of capital it now has to pour back into the business.

AI, cloud infrastructure, data centers, OpenAI exposure, competitive pressure from Google, Amazon, and others,all of that may create enormous value. But it may also require enormous spending just to defend the moat.

That is the key distinction.

If the capex produces durable, high-return growth, Microsoft could still be attractive even at a premium valuation.

If the spending is mostly the new cost of staying relevant, then the shareholder return profile is less exciting than the brand name suggests.

I also do not look at buybacks blindly. Buybacks only matter if they meaningfully reduce share count after stock-based compensation.

Otherwise, a big headline repurchase number can overstate the actual benefit to owners.

Same with dividends. A small dividend is nice, but it does not change the thesis. I need to see owner earnings, reinvestment returns, and a realistic path to compounding.

So my view is this: Microsoft is still a phenomenal business, but a phenomenal business is not automatically a phenomenal investment at any price.

The upside case is clear: AI works, Azure keeps compounding, margins hold, and the market rewards the stock with a higher multiple again.

The downside case is also clear: growth slows, capex keeps rising, competition intensifies, and investors realize the free cash flow yield is not enough compensation for the risk.

I would not call it a simple bargain. I would call it a high-quality company with a very important question attached:

Are these investments expanding the moat, or are they the price of defending it?

That answer matters more to me than whether the stock is down from its high.

5

1

9

1,435

$ADBE discount has already started, it may become even better after the earnings 🤞🤞

7

7

1,477

My thoughts on SpaceX $SPCX IPO..

I’m watching the SpaceX IPO hype and I keep coming back to one basic question: are we investing, or are we just buying a story?

Don’t get me wrong, the story is powerful. Mars, Starlink, AI infrastructure, space-based energy, making humanity multi-planetary.

It is exactly the kind of vision people want to believe in. And Elon Musk is probably one of the best people alive at turning a big narrative into momentum.

But as an investor, I can’t ignore the numbers. If a company is valued at extreme multiples while still burning huge amounts of capital, then the burden of proof is enormous.

Growth is great, but growth funded by losses is not the same as durable value creation. Anyone can grow quickly if they spend aggressively enough. The hard part is turning that growth into real profits and cash flow.

What concerns me even more is that a lot of this demand may not be coming from people risking their own money.

Pension funds, institutions, and passive investors could end up providing liquidity for a deal priced on dreams rather than fundamentals. That’s not automatically wrong, but it changes the risk profile completely.

I also don’t love the control structure. If one person keeps overwhelming voting power, then shareholders are not really buying influence.

They are buying exposure to that person’s future capital allocation decisions. Maybe that works brilliantly. Maybe it doesn’t. But investors should be honest about what they’re signing up for.

SpaceX may achieve incredible things. I genuinely hope it does. But a great company, a great mission, and a great investment are not always the same thing.

For me, profits still matter. Valuation still matters. Cash flow still matters. I’d rather be called boring and stick to accounting than chase a rocket just because everyone else is excited about the ride to Mars.

2

1

7

964

Going to sleep, wake me up when $AMZN breaks $320.. 🫡

5

5

1,346

3

1

796

5

3

2,291