Joined December 2010

- Tweets 1,827

- Following 247

- Followers 4,066

- Likes 2,373

115 Photos and videos

Pinned Tweet

7 Jul 2025

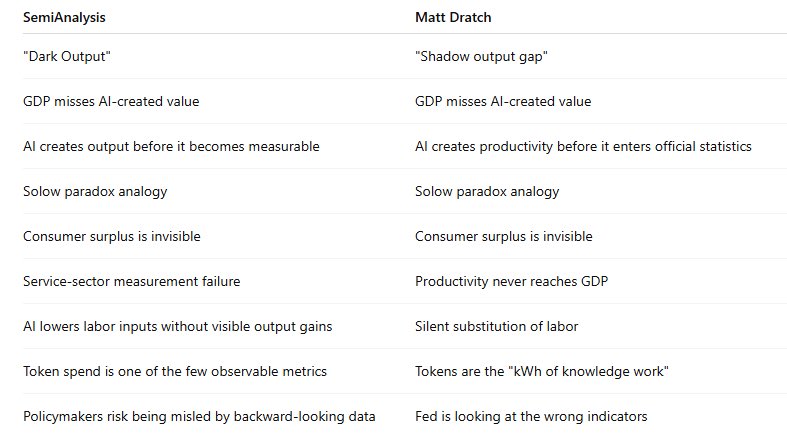

AI’s Shadow Output Gap

While Washington obsesses over debt and inflation, AI is already ushering in an age of abundance (Part 1)

⸻

The political and economic establishment can’t stop talking about deficits, debt, and the CPI. Capitol Hill hearings, FOMC minutes, and financial news all pulse to the same beat.

Yet this fixation ironically coincides with the arrival of the most powerful productivity engine in human history: generative AI. Its impact is creating a shadow output gap — an invisible but rapidly widening expansion of supply-side capacity. Policymakers, especially at the Federal Reserve, act as if the boom doesn’t exist.

The real risk is not inflation. It is a stealth supply shock that pushes prices, wages, and term premia down. Deficits may prove too small. Monetary policy may already be too tight.

⸻

Productivity Everywhere — Except in the Data

This is Solow’s Paradox, redux: “We see the computer age everywhere except in the productivity statistics.” Only this time the curve is ten-times steeper.

Previous tech waves required hardware diffusion—mainframes, PCs, smartphones. AI requires none of that; it arrives through an app. That frictionless uptake already generates latent productivity that never reaches GDP because it appears as:

•lower input costs (fewer billable hours),

•consumer surplus (time saved, spending skipped), and

•silent substitution (high-skill labor quietly displaced).

Illustrations abound:

•A patient triages symptoms with ChatGPT and skips four clinic visits.

•An analyst masters a new industry without three costly expert calls.

•A five-person start-up closes a seed round with no CFO, lawyer, or recruiter—AI fills those roles off the books.

Each case creates real value, but none is logged as “output.”

⸻

Counting the Invisible Token Economy

Tokens — the fragments of text an AI model processes — are the kilowatt-hours of knowledge work. Track them and you watch the shadow gap in real time.

•Google’s token throughput grew 50-fold year-over-year as usage soared and per-token cost collapsed.

•OpenAI’s models now sit in support desks, research departments, and legal teams worldwide.

•Rapidly falling costs are unlocking accelerating demand across every provider.

The data-center capex from Nvidia, Microsoft, and other hyperscalers is simply the physical expression of this surge.

(1/2). $NVDA $AMZN $GOOGL $MSFT $TSM $CRWV $NBIS

6

7

51

84,523

Dario ex Machina indeed

I think its a very different approach than ANT

one corner: AI IS GOING TO CAUSE A DEPRESSION AND EAT 50% OF ALL JOBS REGULATION NOW

satya: humans are going to be in the process... I call it SOAR Loops.. he is saying its mission critical which I agree with

Is it in MSFT interest? of course... he is CEO... the rubber meets the road in what they roll out. I think they/MSFT have missed in an epic manner so far (but I agree with his article thesis) ... lets see what they do, or if they are too late

2

12

8,782

“Being behind is a feature not a bug” … jokes.

But what is profound here? “Companies should use AI to create their own IP in a positive feedback loop and not live and die by one future Trojan horse model…” lol no shit.

The ecosystem matters pitch is a fine one but let’s not pretend it isn’t self serving.

1

14

7,427

There’s so much beauty in simplicity. See below.

9h

Right now, the cheapest value stocks are:

> Samsung

> SK Hynix

> Kioxia

> Micron

> SanDisk

Right now, the highest growth stocks are:

> Samsung

> SK Hynix

> Kioxia

> Micron

> SanDisk

Don’t overthink this. Be smart and do this:

1

14

5,619

I agree the ban makes single-model dependency look sloppy. I don’t agree it makes open / sovereign inference the obvious default.

Also, “don’t build your entire infra on one model” is not some new revelation. Any serious enterprise considers vendor redundancy (including w/i the same vendor, hence opus 4.8). Most customers are already consuming lab models thru hyperscaler infra anyway, so regulation may reinforce the cloud / compliance layer more than disrupt it.

And on the frontier side, the public is using models trained months ago. Labs have internal checkpoints ahead of what we see on the path to productizing something. If govt review adds another gate, maybe the first release slips, but after that the queue resets and buyers still experience a cadence of better models, etc.

The actually surprising thing would have been if everyone believed companies could release super-magic models capable of hacking banks / critical infra w/ no oversight.

None of this is shocking, other than how many people seem unable to imagine the obvious second-order outcomes until they get hit in the face by them.

Btw, I am a LONG TIME lover of $NBIS and think Token Factory is under appreciated with an extremely bright future.

Jun 13

The Fable 5 ban made one thing clear: the intelligence layer now has a fast policy gate that hardware never had.

Hardware bottlenecks (HBM, power, advanced packaging) take years to shit but today it moved in hours.

One export directive on a closed llm = global cutoff

- frontier capability just became contingent on jurisdiction and politics (in a way it wasn’t 48 h earlier)

- clean segmentation at scale is messy.

this exposes a few layers:

1. hosted frontier model itself is no longer a neutral, always-on input. It sits behind a geopolitical choke that can be pulled for “safety” reasons with broad mkt collateral

2. the inference layer underneath becomes strategic. Who serves the model, how it’s routed, quantized, finetuned, guiardrailed, post-trained, and where the data boundary sits now carries real sovereignty weight.

3.Orchestration and redundancy stop being nice to have architecture and start looking like basic operational hygiene once any single frontier llm can be turned down faster than you can figure out alternatives

4. Europe’s demand-side sovereignty moves (Chips Act 2.0 CADA) were already tilting this way. The ban just gave them a crisp, recent case study of the exact risk they’ve been pricing in. It most likely reduces timelines on building parallel capacity and preferring alternatives in critical sectors

On the inference side this opens real space

Specialized providers that can run open weights, customized finetuned and post-trained models at scale with strong sovereignty guarantees just got more relevant.

-> Not because frontier models disappeared, but because the economics and risk profile of depending on them exclusively shifted now

You can keep frontier hosted models for the narrow slice of work where they still deliver decisive quality on long horizon or high-stakes reasoning.

But for volume, regulated workloads, domain-specific agents, or anything where you need predictable updates, data residency, or protection from foreign policy moves, running customized open models on controllable infrastructure becomes the cleaner default.

This is where players like @nebiustf sit in an interesting spot.

Access to sovereign EU compute strong inference stack ability to host and serve fine-tuned or post-trained open models gives a credible path to reduce single jurisdiction dependency without giving up performance on the workloads that matter most.

Some deeper angles worth tracking

- Token economics get more layered.

Frontier APIs stay expensive per token for a reason.

Open fine-tuned models on sovereign or managed inference can be dramatically cheaper at volume once you control the serving stack and quantization. The gap matters more when you’re already hedging policy risk.

- Agent reliability becomes an orchestration problem, not just a model problem. If the frontier tap is sometimes restricted or degraded, you need clean fallback paths and routing logic that preserve output quality where it counts. That creates demand for more sophisticated inference engineering, not just bigger context windows.

- US labs face a subtle structural pressure. The more visible the revocation risk becomes, the stronger the incentive for non-US actors to invest in parallel inference capacity and customized models.

- and over time this can slow winner-take-most dynamics at the frontier even if raw capability btween llms gaps remain.

Power and grid constraints don’t disappear.

What of they just get pulled in slightly more directions as people build hedging capacity?

Parallel sovereign or hybrid inference clusters still compete for the same scarce electrons and networking obv

The real constraint that just got sharper is this designing systems that assume any single centralized frontier hosted model can become less reliable or more expensive to access on policy grounds, not just tech ones.

The ban didn’t invent that assumption but defo made it ignoring it look like incomplete engineering.

22

4,725

The FUD narratives are getting hard to keep straight. Last week the bear case was that everyone would token-minimize, use cheap models / harnesses, and cut spend. Now the bear case is that restrictons at the frontier collapse diffusion and maybe the whole TAM.

These are opposite arguments coming from the same people within days. If cheap models and harnesses are enough to drive diffusion, reg at the bleeding edge matters less. If frontier reg collapses the TAM, then the frontier models are more valuable than the pple were saying last week.

Same thing with Jevons paradox. People understand it perfectly when cheaper models drive more usage, then forget it when they say cheaper memory solutions / edficiencies will crush HBM / DRAM.

I suppose when these inconsistencies / viral slop fests chill out, that will be my best tell that it’s time to rotate to the ‘End Game AI trade’… TLT

3

2

44

4,915

Jun 13

The Boy Who Cried Ban

12%

Fable back by 8am Monday

62%

Fable back by 9am Monday

25%

Fable back Sunday 5:59pm

8 votes • Final results

2

677

Jun 13

Next up, Trump “gifts” America stakes in the largest Ai companies for it’s 250th birthday. Lowering cost of capital, fueling the buildout, and killing the “IPO supply!” Bear case (sovereign anchors never sell? 🤔) all in one move. Dream a little. 😉😝

Jun 13

someone please tell me if I’m retarded but the Anthropic news is the most bullish thing that has ever happened

2

22

3,181

Jun 13

“Only WE can save YOU”. “The onus is on US”. 🤢🤮. Perhaps they’ll enshrine both at the bottom of the Tower of Compute, help ensure an unsturdy foundation so it surely crumbles. History rhymes, indeed

Perhaps this will be the Summer of Sam. @sama Great plotline for the next episode in the Simulation.

3

13

2,694

Jun 13

The regulation Dario has been dying for

Jun 13

As a result of a US government directive, we are suspending access to Claude Fable 5 for all users. You can continue to use all other Claude models.

Here’s what this means for you:

Across Claude products, new sessions will run on your selected default model or Opus 4.8, and existing Fable 5 sessions will end with an error.

On the Claude Platform, requests to Fable 5 will also return an error. Please update your integrations to other Claude models.

We know this is a disruption to your workflows; we appreciate your patience and support.

12

1,469

Jun 11

“I’m selling bc people are selling bc people are selling ahead of supply!” — Market man. Spaceballs can’t come soon enough.

17

1,481

Jun 11

Zeroedge is slop city these days. Always a FUD factory but has gotten way worse.

9

41

8,091

Jun 11

Time to level set. Since the start of June we have ~$220 billion of incremental equity capital to be spent on AI infrastructure (Anthro Series H $Googl $SPCX). That $ will ostensibly be levered 4-5x ($1T) and spent over the next 18mo. $Amzn / $meta may add to it. In that same period of time $HUT priced 15 year BBB- bonds at T 125 ish. An AI stock dip is a gift, no?

AND while Mr Warsh could eventually take down the b/s, Mr Trump may take up his! Perhaps the US gov’t will absorb some of this IPO supply fear w/ stakes in leading AI companies. I prefer **AI Easing** over quantitative easing, anyway.

2

46

7,088

Jun 10

A wonderful reminder of WHOSE WHO IN THE ZOO from the lovely Iliana Bouzali’s (MS) great note today. Plus a little wisdom. (I find it v bullish things like trump accounts w/ help of @altcap will continue this trend. QQQ > homes 😝)

1

9

1,881

Jun 10

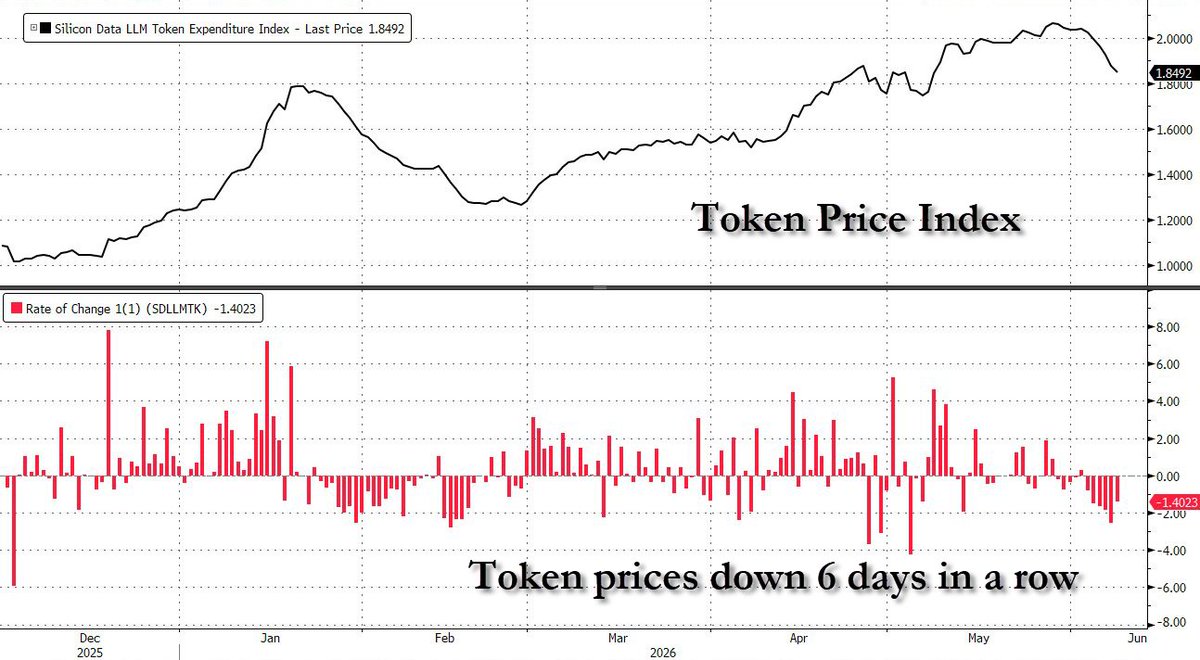

Today was a bad day so I’ve decided to rage against this index. Shockingly, people don’t know that you can’t reliably track tokens. Nobody outside the labs / hypers sees the actual token flows.

Before I even get to the flaws in the data, did anyone consider that as capability rises and cost falls, task complexity goes up? Agentic work has a long tail of simple steps for every hard one, and the easy stuff scales disproportionately. This index skews toward API middlemen running harnesses that route subtasks to the cheapest capable model (including using sonnet > opus!!). So a falling blended price may say very little about who’s using what, and a lot about total usage and task complexity going up. Now to the data.

This index in particular is a blended avg price of itself a subset of incomplete data. For ex, one big synthetic data run on a cheap open model could impact it while frontier demand remains the same.

The sample also liens on aggregators (api middlemen man). So you’re not seeing direct enterprise contracts or first party consumption (using the app). This is like looking at online retail and not having prime or Walmart.

And it has no idea what anyone actually pays. 1) All tokens are not the same, 2) list prices do not equal token prices.

On 2, important cost reduction techniques like batching / caching are offered at huge discounts (50-90%) and so mix shift here adds to the noise.

Free tokens / expanded limit promos (liek what anthro is doing right now) also show up as falling prices… so the marketing budget is bleeding into the “demand” chart.

And if you needed another reason: if the conclusion is people are using frontier models less bc the chart is rolling, how would you explain the chart also rolling at the start of the year when everyone was having an orgasm about frontier lab (Claude) ARR absolutely ripping during this period?

Which is all to say that model usage is assuredly evolving (see NBIS token factory) and that may be the right conclusion, but i would not be using this data to “track” that.

Jun 10

This data is not what people think it is.

5

6

88

30,051

Jun 10

This data is not what people think it is.

Jun 10

Token prices down 6 days in a row: longest streak since January.

"Adoption is becoming less about what frontier models can do and more about the price... the recent drop in the token index may reflect some of this shift toward cheaper models"- Citadel

5

1

45

52,500

Jun 10

What happens when everyone’s margin becomes everyone’s opportunity?

There’s a version of the next few years that no one is positioned for, let’s call it the “modified @Citrini bear case”. AI works but mostly deflates. As the price of intelligence collapses, so does everything intelligence touches. You know the obvious ones, but the big one is on the come per leather jacket Jensen: robots, etc. (Note, his track on what’s next is good enough to save you some time 😉)

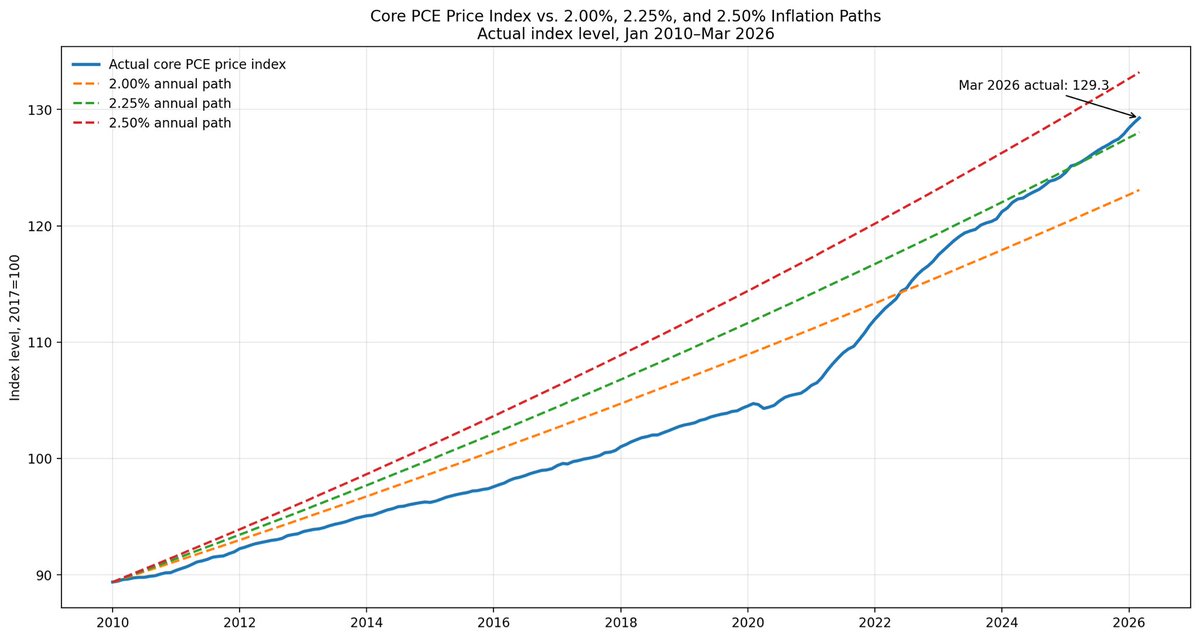

But this is not likely to be the ‘doomer outcome’; instead, it looks a lot like 2010-2019. Decent growth, meh wage pressures, supply compounding faster than demand, and official productivity stats that miss the real world (the same stats that said the mobile internet decade had no productivity… LOL). Which is to say, perhaps the more things change the more they stay the same.

The COVID inflation regime was anomalous IMHO, and we may be reverting to trend. You don’t see it discussed a lot but the 15yr PCE CAGR is actually around ~2.3% ish. The recent ‘hot period’ simply made up for last decade’s undershooting, ironically.

Today’s AI capex boom may be a similar head fake because the buildout is inflationary but the deployment is deflationary… and the latter compounds. In other words, in the race between atoms and bits, I’d bet on the bits being faster than people think. You can read that as adoption / ‘goodput’ reflexively picking up.

To me, this makes optionalized duration extremely interesting as a hedge… and it may just work anyway. For example, betting the 20yr bond returns to its 2010s avg pays anywhere from 25-35:1 over 18-20 months. So, 3-4% odds that we go back to the pre-covid regime? Seems low. I know, no one agrees, rates and inflation higher blah blah… but that’s why you get to buy long term rate vol at 7yr lows. At least in this case it pays to THINK DIFFERENTLY. $TLT

5

41

4,675

Jun 9

Some observations… Generally illogical price action. 🤦🏻♂️

Jun 8

Some observations…. Generally ‘logical’ price action. 1) AI stuff people want to own is up, 2) The Meh 7 has a supply / space problem short term, 3) ‘other’ stocks have a CPI / Warsh problem (the former may help de-risk the latter). Some vol control selling today, as well. A couple days of digestion is normal. And ‘bend but don’t break’ is a bullish signal.

1

1

11

5,063

Jun 8

Someone tell Trump about this right away 👀👀👀

President Lee said Korean equities remain undervalued - proposed “anti stock suppression law” would tax inheritance/gifts for listed companies with PBR <0.8 based on asset/earnings fair value rather than depressed market price.

$mu $hynix

2

11

4,527