Husband - Father - Dog Dad - Full Time Investor 🏘️ - Former Pharmacist 💊

Joined October 2011

- Tweets 5,360

- Following 1,494

- Followers 1,038

- Likes 108,354

131 Photos and videos

Pinned Tweet

1 Oct 2023

Left my W2 as a pharmacist in October of 2021. Since then:

- 100 off market deals

- 29 units owned

- Attempting to build a 7 figure annual off market real estate business

2

26

2,436

Dylan retweeted

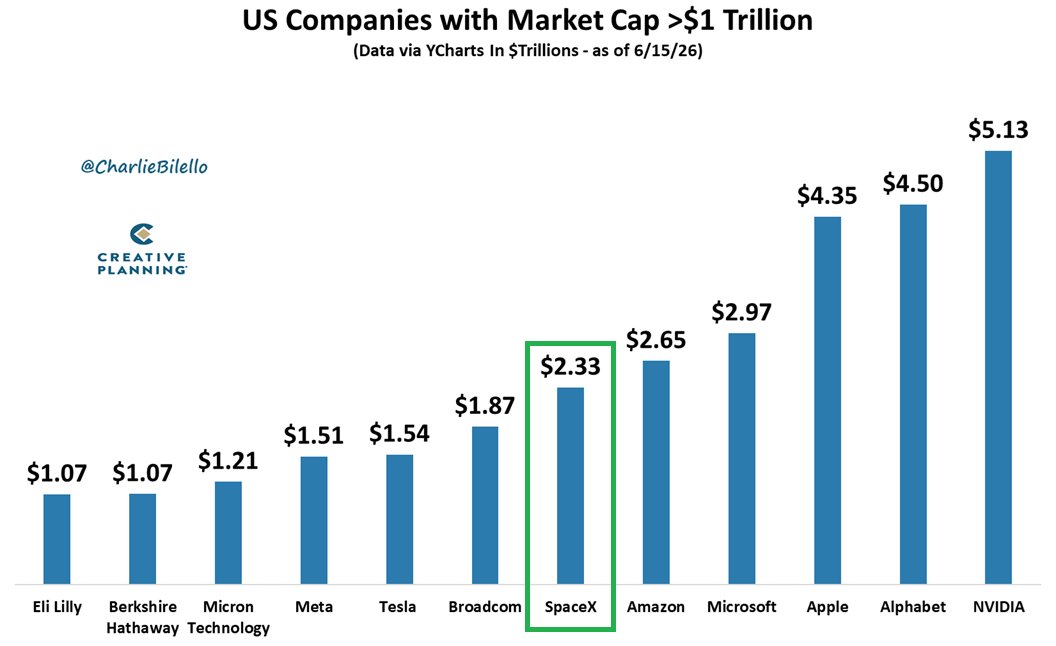

If SpaceX was in the S&P 500...

It would be the 6th largest US company in terms of market cap at $2.3 trillion.

But in terms of revenue, it would be 198th largest.

Investors are betting on exponential growth like we've never seen before. $SPCX

Video: youtube.com/watch?v=sMF_Nh5L…

33

33

216

22,216

Jun 14

They must’ve hired the Reds bullpen coach

Jun 14

Spurs led game 1 by 14 points

Spurs led game 2 by 12 points

Spurs led game 3 by 12 points

Spurs led game 4 by 29 points

Spurs led game 5 by 16 points

47

Dylan retweeted

Jun 13

The US government, citing national security authorities, has issued an export control directive to suspend all access to Fable 5 and Mythos 5 by any foreign national, whether inside or outside the United States, including foreign national Anthropic employees.

The net effect of this order is that we must abruptly disable Fable 5 and Mythos 5 for all our customers to ensure compliance.

Access to all other Claude models is not affected.

We apologize for this disruption to our customers. We believe this is a misunderstanding and are working to restore access as soon as possible.

Read our full statement: anthropic.com/news/fable-myt…

12,500

25,744

87,843

89,346,055

Dylan retweeted

Jun 11

387

189

6,124

771,955

Dylan retweeted

Jun 10

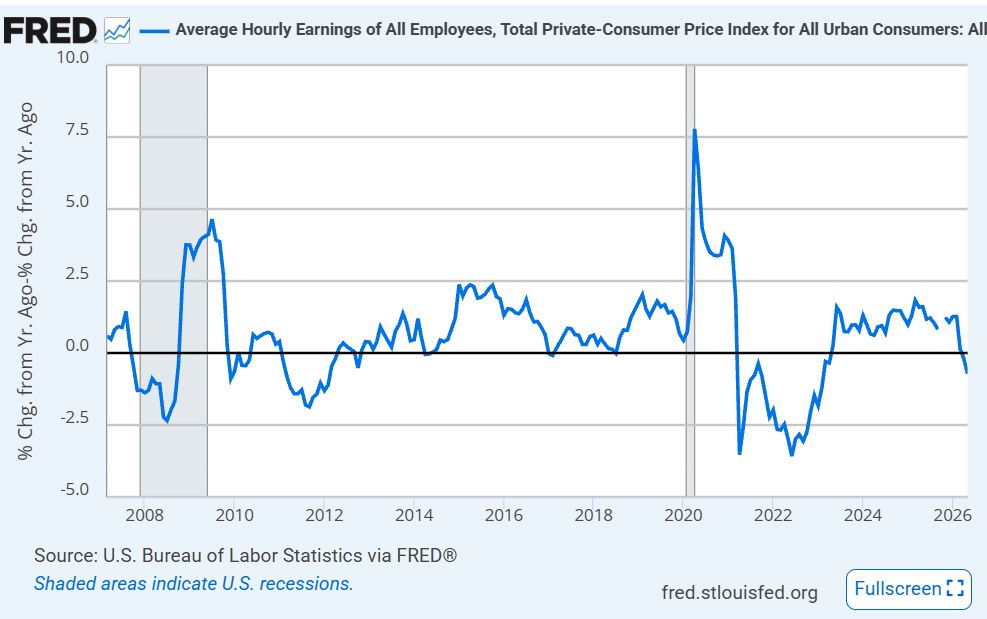

Another reminder today that real wage growth is negative.

24

73

445

41,086

Dylan retweeted

Jun 4

Caleb Hammer says the boomers had the best stock market ever yet they ended up broke

"every single boomer that's been on my show they lived it up and spend all their money to live the lifestyle the wanted"

"and they didn't even set 10% aside a month...they had the best housing market, college, jobs...they were set up for everything"

"if they just put 5-10% a month in the stock market they had they would multi-millionaires"

259

416

11,519

1,377,869

Jun 4

I mean this is great but haven’t you been AG for like 7 years? Why has it taken this long?

Jun 4

As Attorney General, my team has obtained 1,087 Medicaid Fraud convictions so far.

This morning, we announced two more indictments that combined total $42 million.

42

Dylan retweeted

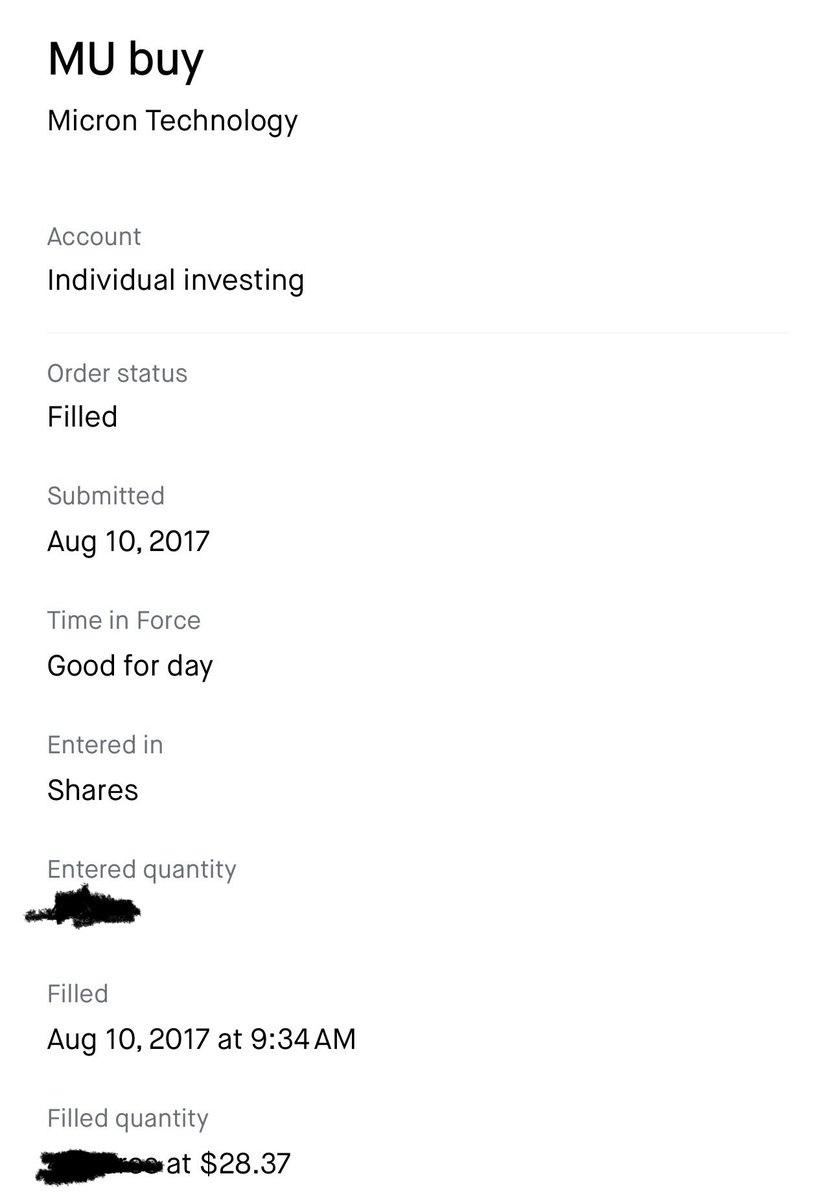

May 31

If you are having a bad day, remember that Mohnish Pabrai had 79% of his portfolio in Micron but sold the entire stake in the middle of 2023

The stock is 1400% since then

59

145

3,613

328,626

Dylan retweeted

May 29

peak euphoria: “Today will likely be the largest SPX call volume sessions of all time. Calls have made up 70% of every option traded” - Goldman

89

254

2,783

347,232

Dylan retweeted

May 28

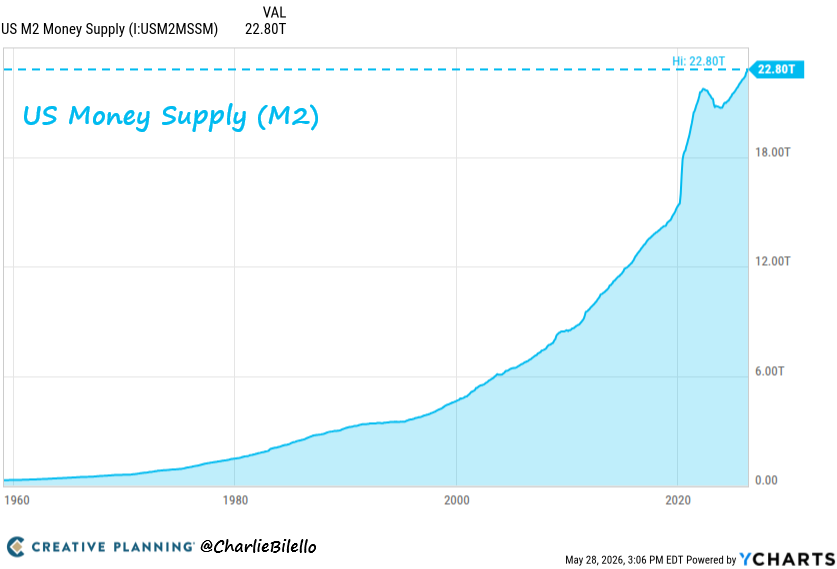

The Fed expanded the money supply by nearly $9 trillion under Powell.

Inflation has averaged >4% per year over the past 6 years.

Powell's explanation? It was nearly all due to rolling “supply shocks" over which the Fed has no control.

The truth: this inflation was made in Washington as it always is - from too much government borrowing/spending and too much government creation of money.

236

870

3,048

188,712

Dylan retweeted

May 27

JUST IN: FBI arrests senior CIA official after uncovering over $40 million in gold bars & $2 million in cash at his Virginia home.

1,108

3,943

25,842

2,015,794

Dylan retweeted

May 27

I'm convinced that the single greatest challenge for any ambitious person is eliminating the guilt associated with free time and rest.

367

1,789

16,279

390,330

Dylan retweeted

May 26

The Boomers are the richest generation to ever exist. If anyone needs a property tax break, it’s the Millennials.

May 26

Our seniors should not pay property taxes.

308

144

2,732

81,248

Dylan retweeted

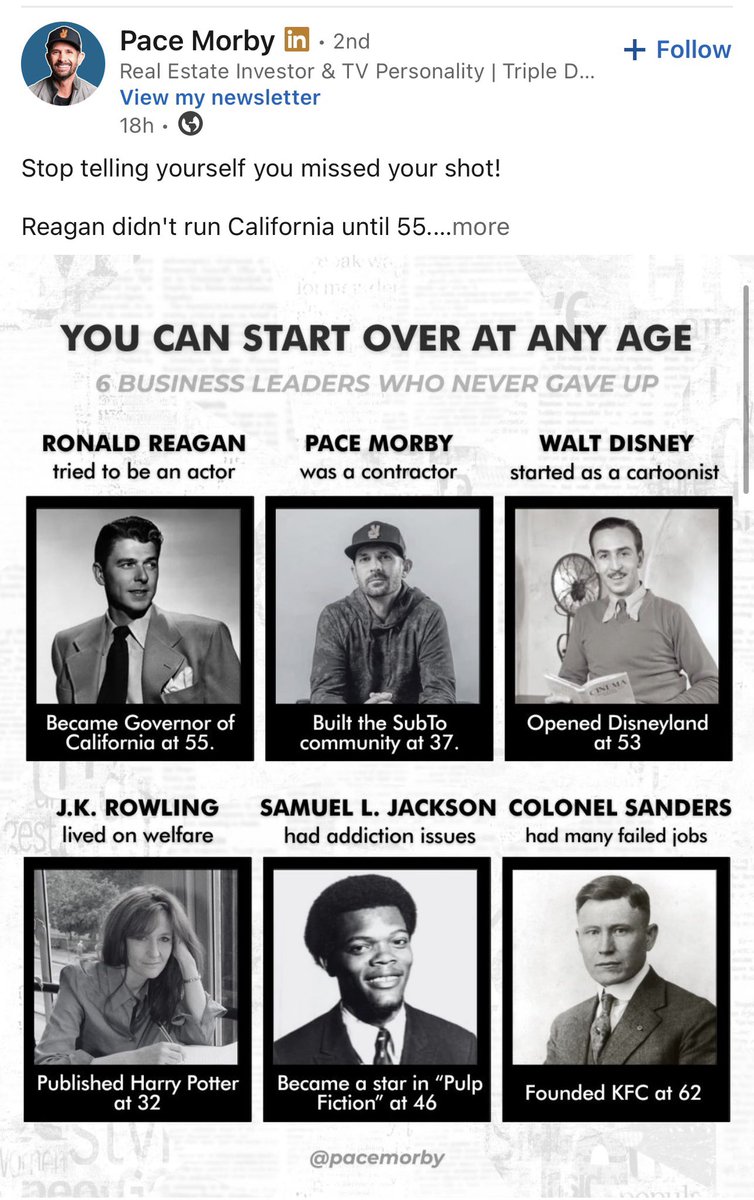

Wtf

Did Pace Morby really just put himself in this group with Ronald Reagan, Walt Disney & many other prominent well known and respected names?

This guy is a complete clown!

18

5

74

10,328

Dylan retweeted

May 24

I've got one against them on behalf of four LPs that goes to trial in October. The lack of communication and the deal going bust aren't the reasons for the lawsuit, though: they misrepresented the LTC (70% in the OM, ~82% actual), the initial DSCR (1.15 in the PPM, .95 in their internal models, and .63 actual), and told the LPs they personally guarantee every loan, but had only a limited recourse guarantee on this one.

The one that really blows my mind, though: they underwrote a 113% increase in year 1 NOI on a 1960s vintage Houston class C property that they were purchasing from a professional syndicator who had a good PM managing the property.

I don't think it's okay to represent to LPs that you are an experienced, knowledgeable RE investor when you don't realize that underwriting a 113% NOI increase in a highly competitive market that would still only get you to .95 DSCR means the deal is doomed from the start. And of course they used a floating rate 3 1 1 bridge w/ no rate cap.

1

1

10

500

Dylan retweeted

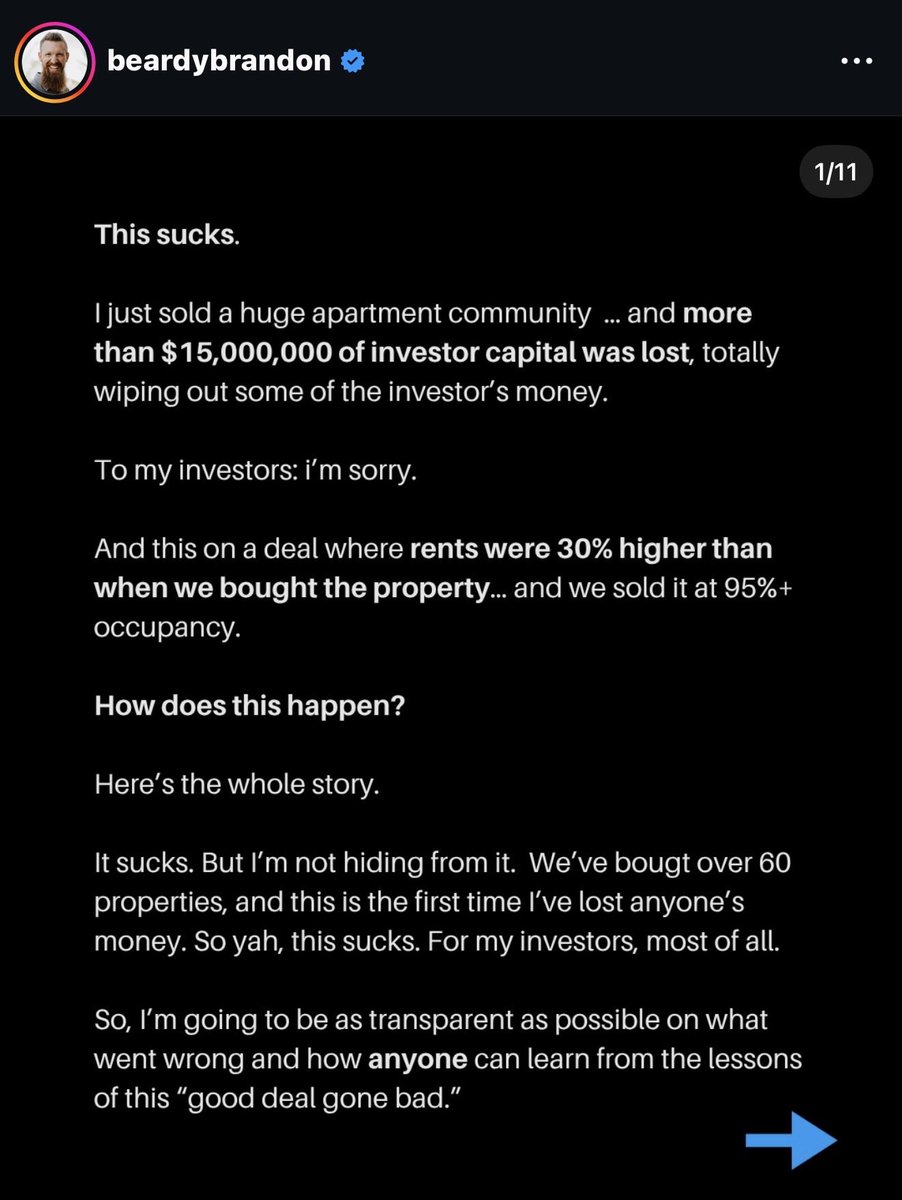

May 24

I’d like to give Brandon Turner sincere credit for this post on IG.

He fully owned up to the loss of LP capital publicly.

Explained his responsibility, which is the most important, along with the market factors the affected the downfall of this deal.

This is exactly how a sponsor should transparently communicate when something like this happens.

It doesn’t make the loss of capital easier, but I have true respect for people that take ownership.

The guru class has butchered the handling of their errors over the past 5 years.

Brandon is the first one I’ve seen to step forward and address it.

Credit where credit is due.

Bravo.

84

7

321

353,636

Dylan retweeted

May 21

JUST IN: Minneapolis day care owner featured in Nick Shirley’s viral fraud video federally charged in an alleged $4.6 million fraud scheme.

308

1,926

34,463

3,059,411

Dylan retweeted

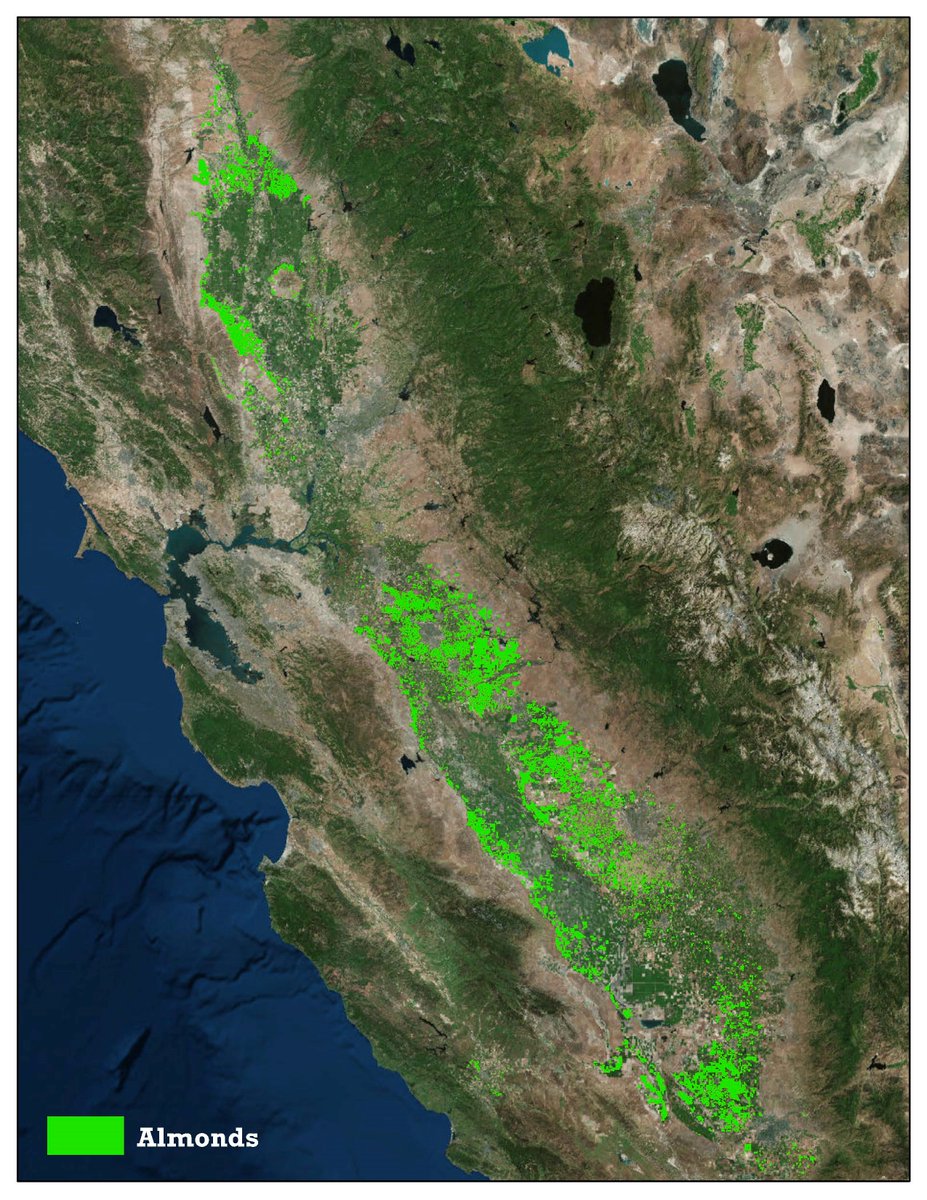

May 20

Insane stat of the day: California almonds use roughly 3–5.5 million acre-feet of water per year, depending on methodology.

That's ~4-7x more water than all data centers in North America used combined in 2025.

1,085

1,123

6,274

3,123,524