AMFI Regd MF (ARN 146704)& SIF (SIF 146704) Distributor,APMI Regd PMS (APRN 05905) Distributor; AIF Distributor

Joined September 2019

- Tweets 1,881

- Following 535

- Followers 136

- Likes 1,741

411 Photos and videos

In #investing

Narratives always changes

But

Your Behaviour should not

Just stick with your #AssetAllocation; review your portfolio periodically; rebalance it, if necessary.

that' it

All Done!

4

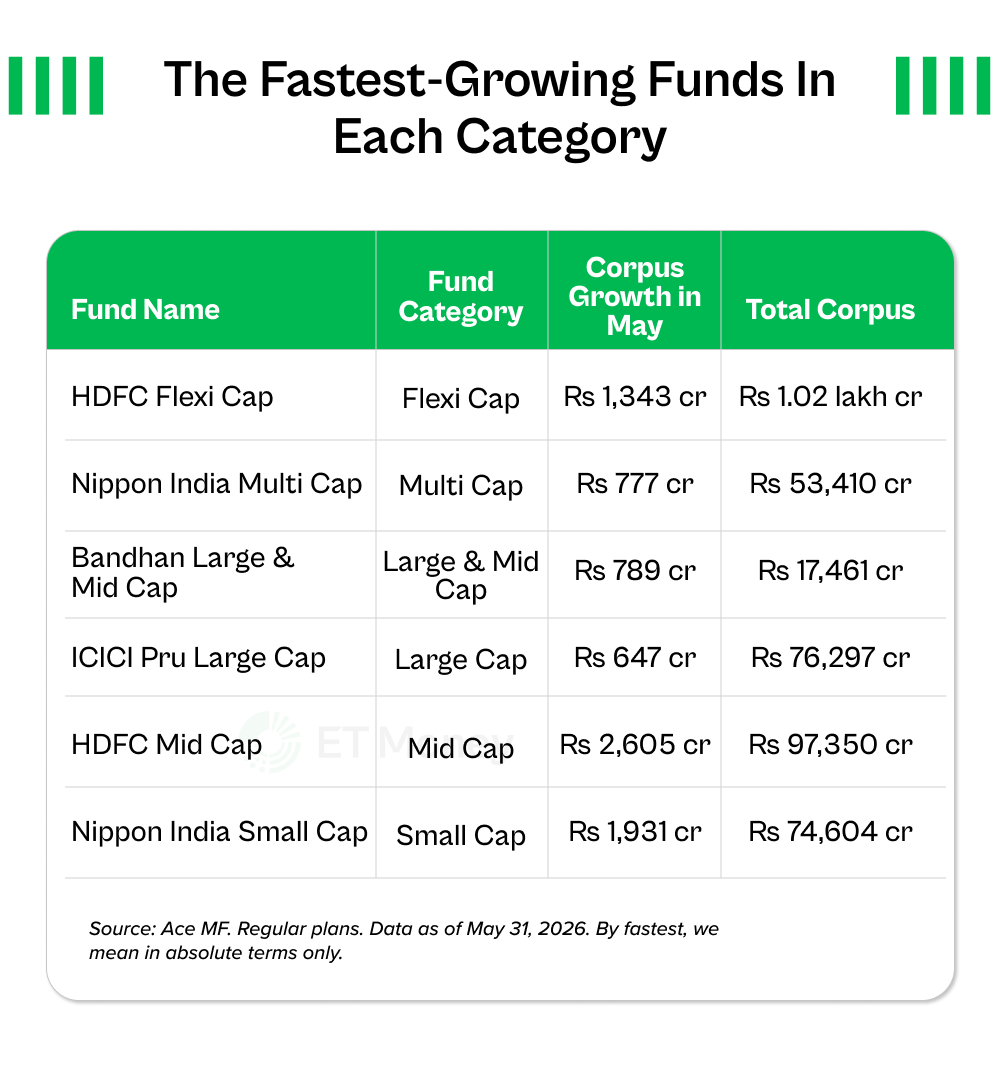

Parag Parikh is no longer India's fastest-growing flexi-cap.

Additionally, we found 2 giant funds bought the same stock (TVS Motors) in May. TCS, meanwhile, split opinions.

So, let’s take a deep dive into what stocks were bought and sold by prominent funds last month. 👇

2

14

137

17,753

Nilay Shah CFGP @ Edification Financial Services® retweeted

Jun 13

IF YOU DIED TOMORROW, YOUR FAMILY WOULDN'T BE ABLE TO ACCESS A SINGLE THING YOU OWN DIGITALLY.

BANK ACCOUNTS. PASSWORDS. CLOUD STORAGE. ALL OF IT PERMANENTLY LOCKED AWAY.

HERE'S HOW TO FIX IT IN 30 MINUTES:

108

935

4,217

2,014,886

Nilay Shah CFGP @ Edification Financial Services® retweeted

Jun 8

An inspiring startup story….

28

155

858

46,042

Nilay Shah CFGP @ Edification Financial Services® retweeted

Jun 5

"Why should I pay you 1% when I can just buy a direct plan myself?" Where and when does an advisor/distributor earn his fee?

The honest answer: in some fund categories, that 1% is the best money you'll spend. In others, you're being robbed.

I measured every active equity and hybrid fund in India over the last three years (direct plans, CAGR), and looked at the gap between the best and worst fund in each category.

Look at the gap, then look at the fee.

📊 Where getting the fund right is everything (gap on ₹5 lakh):

→ Flexi Cap: best compounded at 22%/yr, worst at under 1%. A ₹4 lakh gap.

→ Small Cap: 30%/yr vs 13%/yr → ₹3.7 lakh

→ Value: 26% vs 9% → ₹3.6 lakh

→ ELSS: 24% vs 6% → ₹3.5 lakh

→ Mid Cap: 28% vs 13% → ₹3.3 lakh

In these categories, even nudging a client from the wrong fund toward the right one is worth multiples of any fee. The 1% is a rounding error against the prize.

🟢 Now where that same 1% makes no sense:

• Arbitrage: the entire best-to-worst gap is ~1.2% a year. The fee is wider than the prize. There is nothing to add.

• Contra, Conservative Hybrid: barely 2–4%/yr between best and worst.

Here's the principle: the wider a fund's mandate and freedom to operate, the more the manager — and therefore the choice — matters. That's exactly where advice earns its keep. In narrow, rules-bound categories, one fund is basically the next, and you should pay for none of it. So your advisor needs to do the homework on Flexi Cap, Small Cap, Value, ELSS, Mid Cap.

One caveat: a wide gap doesn't mean today's winner keeps winning. It means the cost of choosing wrong is high — which is the whole reason to choose carefully. And the framework for choosing the fund, of course, is a whole different conversation which goes beyond performance.

So before you pay anyone 1%, ask one thing: in this category, is there even a gap worth closing?

Made with @MugdhaPetiwale

6

10

76

8,150

Nilay Shah CFGP @ Edification Financial Services® retweeted

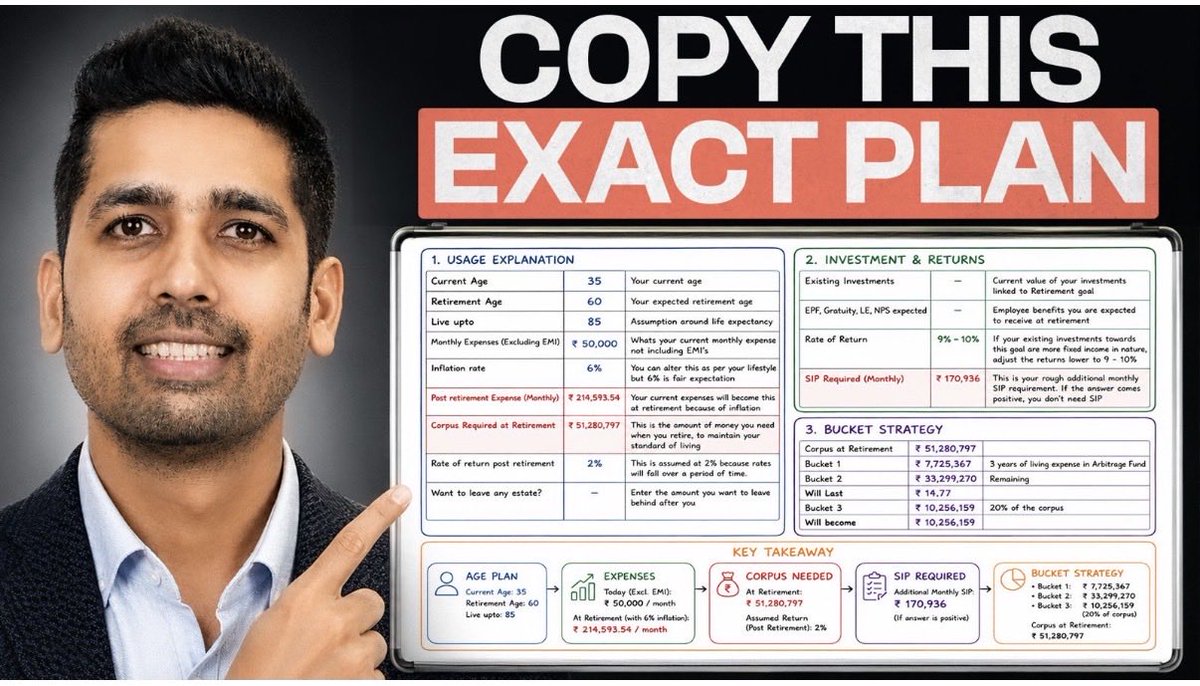

Jun 3

Just recorded a crisp yet a detailed video on retirement planning

The video covers,

- How to calculate the numbers required for your retirement

- A brilliant Investment strategy to deploy your retirement corpus

- Most importantly, the Retirement tool that you can download and personalise the plan for yourself

If you have 18 minutes, do watch the video. Link to the video in the first comment below 👇

youtu.be/ZnPV8V59in8

6

30

200

21,252

Nilay Shah CFGP @ Edification Financial Services® retweeted

May 26

Top fund managers have very different takes on Indian IT.

Rajeev Thakkar is finding value at current levels and is buying IT across funds.

Prashant Jain is neutral. His view the sector may need 2 more years for better clarity.

Kenneth Andrade has completely exited IT, citing uncertainty around the real impact of AI on the sector.

S. Naren, the contrarian, is also seeing value and continues to hold IT stocks.

Samir Arora is bearish on traditional IT, with zero allocation there, but prefers select tech and capital market plays.

Sunil Singhania has no exposure to traditional IT stocks, but is buying a product-based tech company.

It will be interesting to see who gets this right.

23

13

184

26,581

Nilay Shah CFGP @ Edification Financial Services® retweeted

May 27

I Cancelled Spotify.

I cancelled Disney .

I cancelled Apple TV .

No more paying every month.

Claude transformed my laptop into a free entertainment center.

Here are 8 prompts to create this system:

35

151

941

252,768

Nilay Shah CFGP @ Edification Financial Services® retweeted

May 28

I don't understand. Why wouldn't you buy bonds via debt or hybrid funds?

1)Funds invest in many bonds; a single NCD is a concentrated bet

2) Fund gains are deferred to redemption, bond interest taxed annually

3) Debt funds - daily NAV exit, bonds have thin secondary mkts

37

21

173

70,479

Nilay Shah CFGP @ Edification Financial Services® retweeted

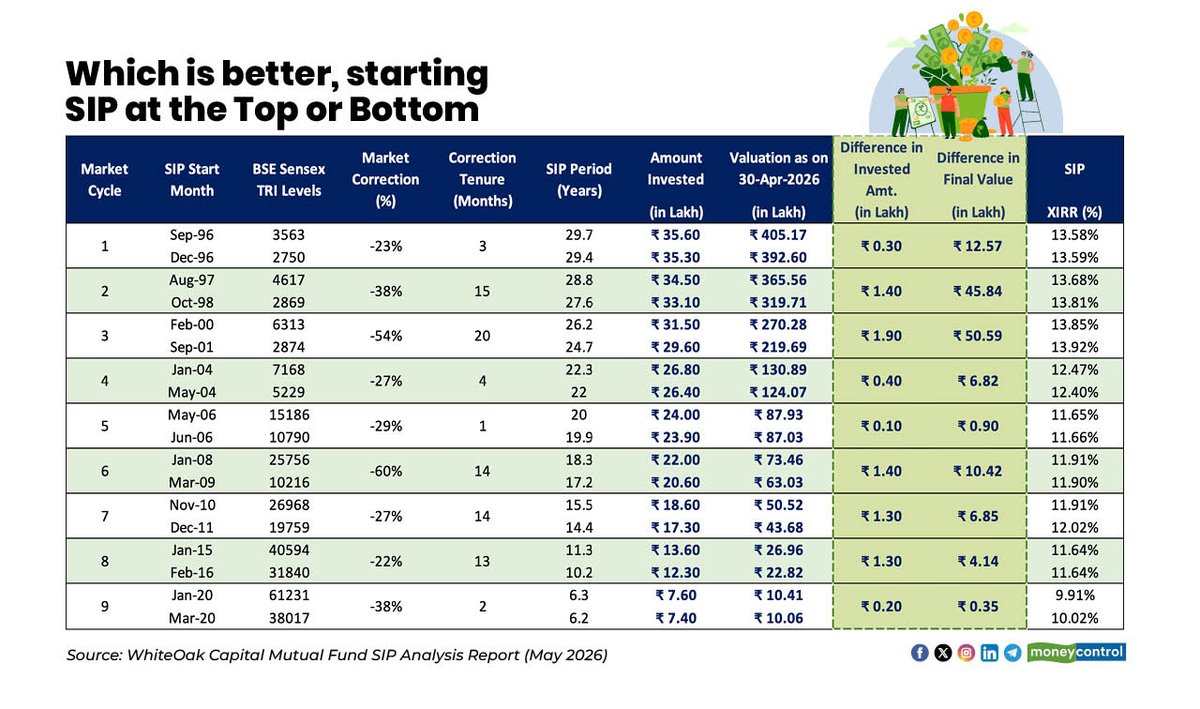

Which is better, starting SIP at the top or bottom?

SIP data of nearly 30 years from WhiteOak Capital report shows that while the % return is marginally higher for SIPs started at the bottom of the market cycle, the absolute gain in rupee term is far higher for SIPs that began at the top.

The longer an investor waits for markets to bottom out, the greater the opportunity lost in terms of wealth creation.

Data shows an SIP invested on the “luckiest” day of the month in the BSE Sensex TRI between August 1996 and April 2026 delivered an XIRR of 13.80 percent, while investing on the “unluckiest” day still generated 13.32 percent.

A disciplined SIP made on a fixed date every month, such as the 15th, delivered a comparable 13.58 percent return.

Writes @PriyadarshiniM9 :

moneycontrol.com/news/busine…

4

11

67

6,035

A must read for all retail #stockmarket traders

The real cost of #tradingcardsales

source : ETW 04.05.2026

1

5

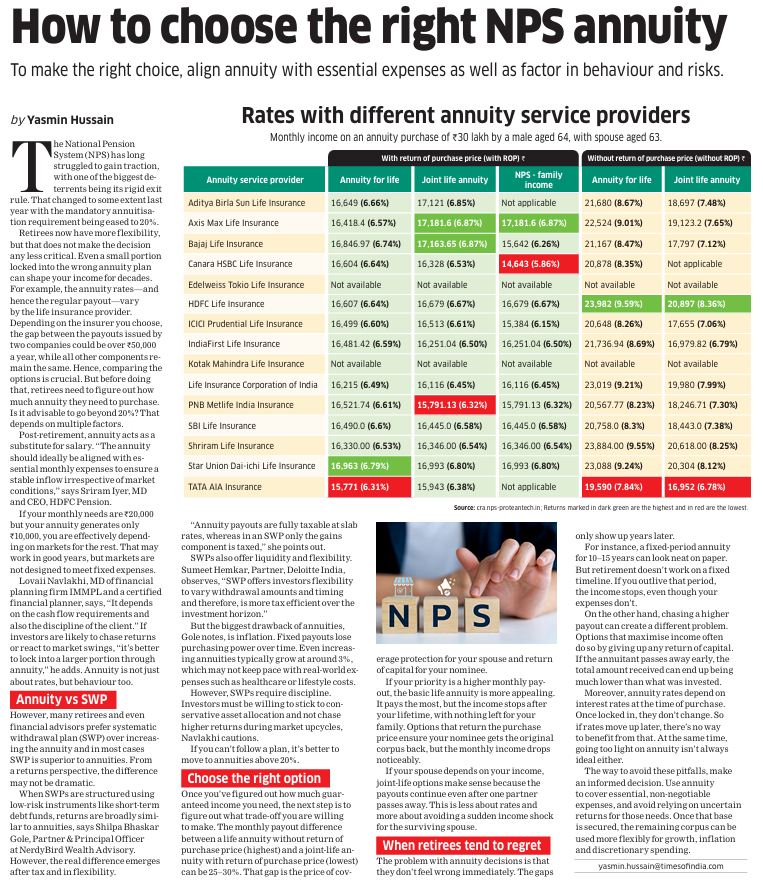

PFRDA just changed how NPS subscribers can use their retirement money.

No more being forced into annuity for your entire corpus at 60.

You can now draw a regular income from your NPS corpus while keeping it invested in the market.

Here's what changed 🧵

12

48

204

52,765

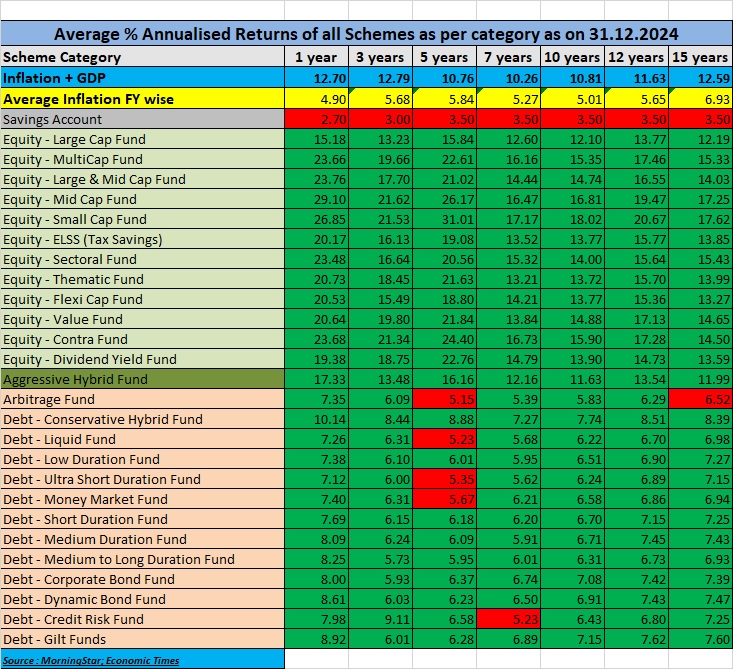

📊 Mutual Fund Returns vs. Inflation (as of 31.12.2024)

🔥 Inflation GDP: 12.70% (1Y) | 12.79% (3Y) | 10.76% (5Y)

🚀 Equity Wins! Mid Cap: 29.10% (1Y) | Small Cap: 27.85% (1Y)

💡 Debt Struggles! Some categories failed to beat inflation

#MutualFunds #InvestWisely

1

141

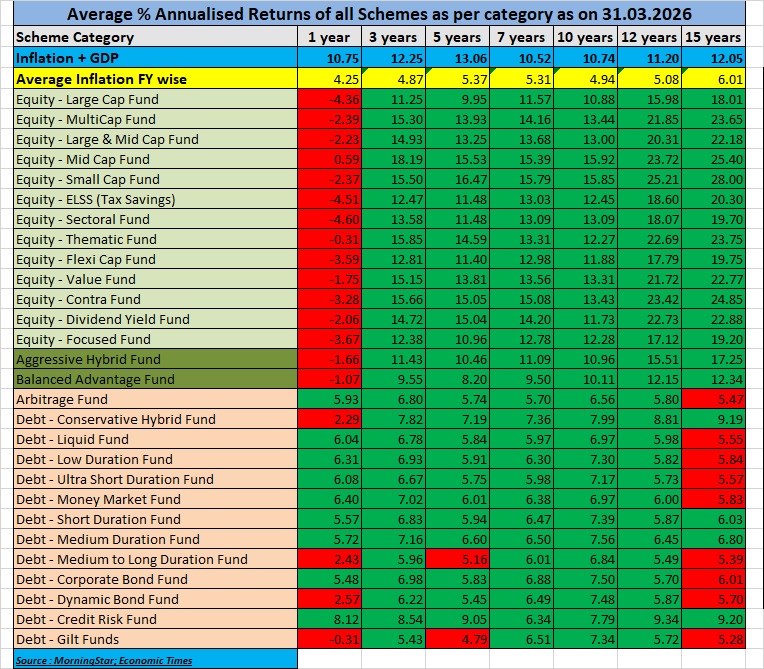

📊 MF Returns 31.03.2026

🔻 1-Year under pressure – Most Equity categories in red (Large, Flexi, ELSS, Sectoral)

🟢 Long-term intact – 10Y–15Y returns across Equity still strong (18–25% in many categories)

⚖️ Hybrids cushioning volatility better than pure equity

#MutualFunds

1

22

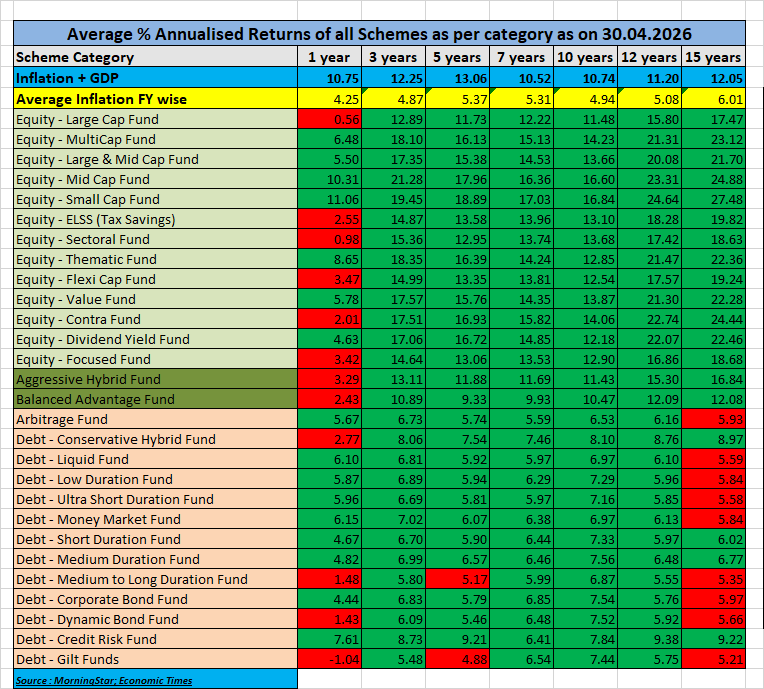

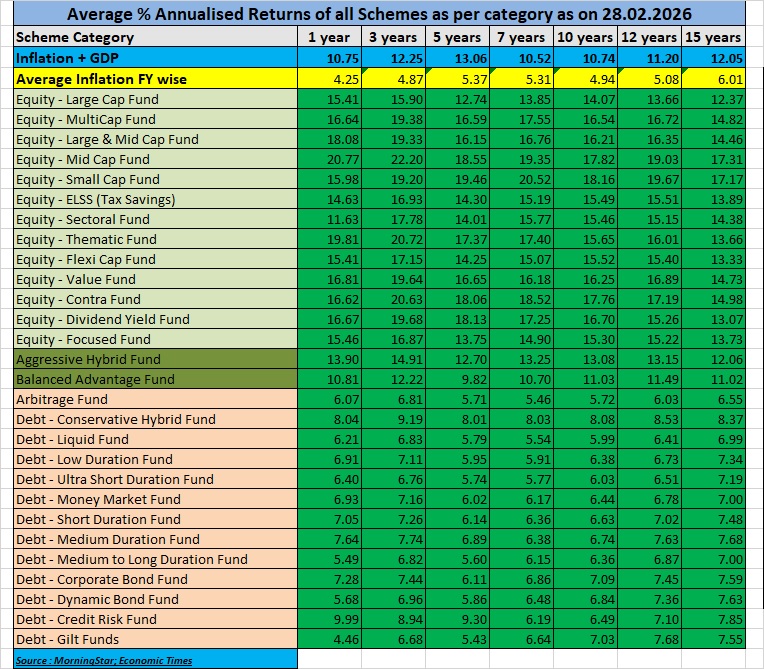

📊 MF Returns 30.04.2026

🟢 Equity bounce-back visible — Mid & Small Funds back in double-digit 1Y returns

⚖️ Hybrid funds continue to offer stability during volatile phases

🔻 Some Debt categories & Gilt Funds still struggling to beat inflation over long periods

#MutualFunds

6

Nilay Shah CFGP @ Edification Financial Services® retweeted

May 19

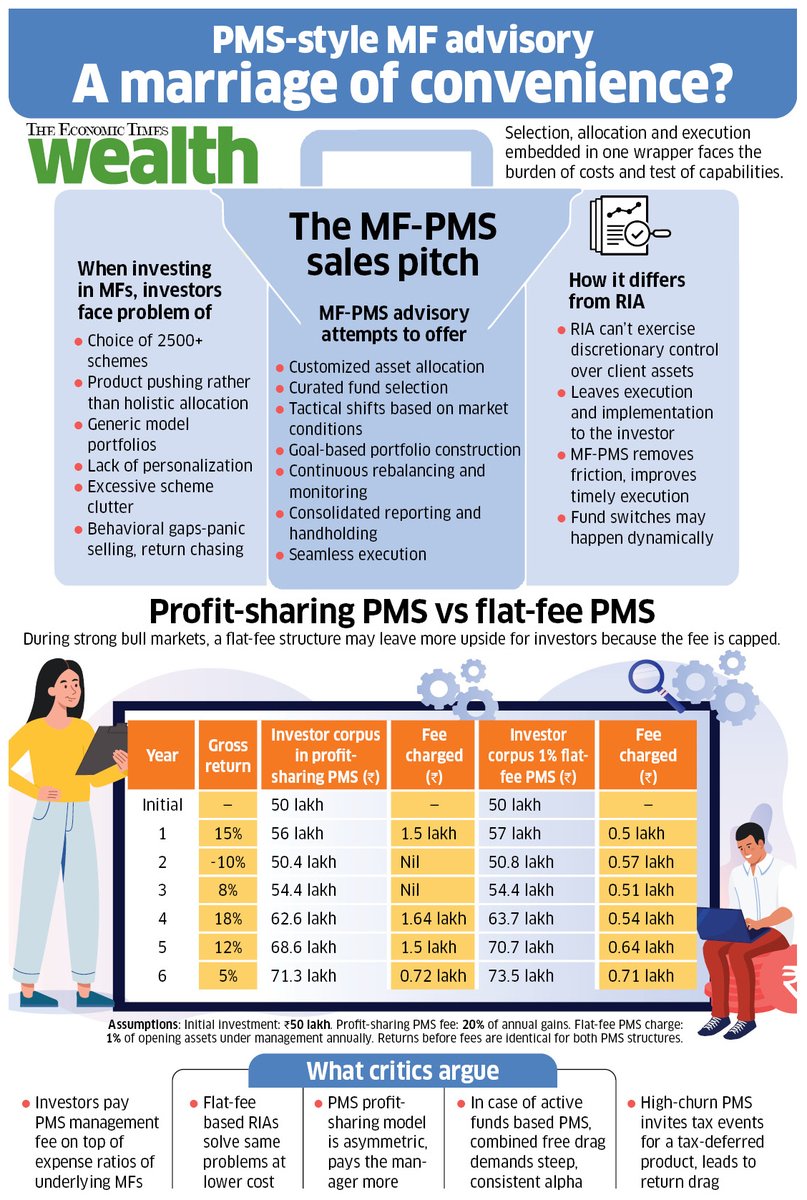

MF-PMS is the new pitch doing the rounds; they're curated funds, active allocation, seamless execution, all in one wrapper.

But does the advisory layer justify the added costs?

@SanketD_ET digs in. In this week's @ET_Wealth

3

9

34

7,535

Nilay Shah CFGP @ Edification Financial Services® retweeted

May 14

UPDATE: If you’re not using Claude in your work yet, you’re already late.

Copy these 8 prompts:

48

149

1,273

478,111

Nilay Shah CFGP @ Edification Financial Services® retweeted

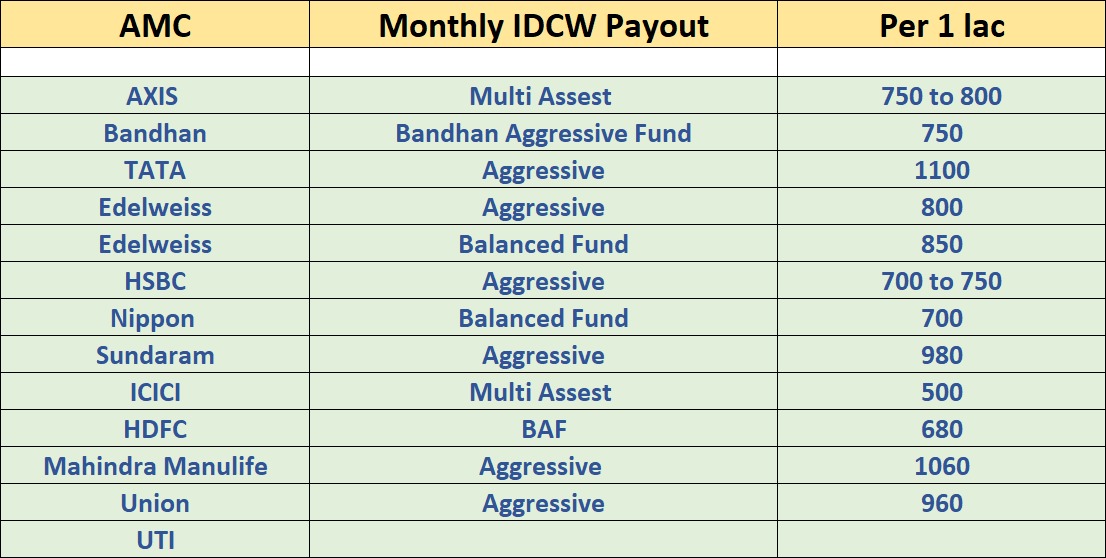

May 14

If you're looking for regular monthly income from mutual funds, IDCW plans could be a good option. Here's a quick snapshot of what different AMCs are paying out per Rs.1 lakh:

3

6

194

Nilay Shah CFGP @ Edification Financial Services® retweeted

May 14

This is what you should ideally track: Your net worth. Your financial assets. Your liabilities. Your asset allocation. Your income. Your expenses.

These are the things that actually matter in money management. Everything else is secondary.

Don’t reduce money management to chasing returns. Returns over the long term are largely an outcome of managing risk well, staying disciplined, managing liquidity, and following a sensible process.

People obsessed with returns often end up hurting their portfolio returns owing to impatience, overreaction, and constant changes.

9

90

4,691