Top 5 Multi Asset Funds with Asset class wise higher exposure

📊 Not all Multi Asset Funds are built the same.

🔹 Samco leads in Equity Exposure

🔹 Edelweiss tops Debt, Gold & Silver

🔹 WhiteOak Capital dominates REITs & InvITs

🔹 Invesco India leads International Allocation

🔹 Quant holds the highest Cash position

🔹 DSP emerges as one of the most diversified portfolios, with exposure across Equity, Debt, Gold ETF, Silver ETF, REITs, International Assets, Gold, Silver and Cash.

The real differentiator in Multi Asset Funds isn't just performance it's how assets are allocated across market cycles.

#MultiAssetFunds #AssetAllocation

3

85

Most investors think gold moves for one reason.

Fear.

Peter Grant, a widely followed precious metals strategist, recently shared an insight in a Reuters report that shows why that view is incomplete.

Gold rose 1.5% to $4,861/oz and headed for a fourth straight weekly gain even as hopes of a U.S.-Iran deal improved and the Strait of Hormuz stayed open. Oil fell. The dollar weakened. Rate-cut expectations returned. Gold still held strong.

That is the real lesson:

Gold is not reacting to one headline.

It is responding to a system.

And that matters for your wealth decisions.

My investing framework is simple:

1. STOP ASKING “WHAT WILL GOLD DO?”

Ask:

- What changed in inflation expectations?

- What changed in rates?

- What changed in liquidity?

- What changed in the dollar?

- What changed in portfolio risk?

Better questions create better decisions.

2. USE GOLD AS a ROLE, NOT a BET

Gold does not need to be your whole strategy.

It can serve as:

- resilience capital

- diversification

- crisis ballast

- psychological stability in volatile periods

Assets should have jobs.

3. BUILD ALLOCATION BEFORE VOLATILITY ARRIVES

Do not decide during panic.

Decide in advance:

- maximum allocation

- rebalance rules

- when to add

- when to trim

- why you own it

That turns emotion into process.

4. WEALTH is BUILT by SYSTEMS

You do not need to predict every geopolitical event.

You need a portfolio that can function across many outcomes.

That is how long-term investors win.

Not by perfect forecasts.

By repeatable decisions.

#Investing #WealthBuilding #Gold #AssetAllocation #BehavioralFinance #LongTermInvesting #PortfolioManagement #MacroInvesting

13

Beyond Wealth | 14 มิถุนายน 2569

มหกรรมฟุตบอลโลกเริ่มเปิดฉาก ทุกทีมต่างต้องวางแผนให้สมดุล ทั้งเกมรุก เกมรับ และจังหวะการครองเกม เพราะการมีแค่กองหน้าที่เก่งอย่างเดียว อาจไม่พอให้ทีมไปถึงเป้าหมาย

“การจัดพอร์ตลงทุนก็เช่นกัน”

พอร์ตที่ดีไม่ควรมีเฉพาะสินทรัพย์ที่หวังเติบโตสูง แต่ต้องมีทั้งตัวสร้างผลตอบแทน ตัวช่วยกระจายความเสี่ยง ตัวลดความผันผวน และสินทรัพย์ป้องกันพอร์ตในวันที่ตลาดไม่เป็นใจ

ที่น่าสนใจคือ หากมองสถิติในอดีตช่วงฟุตบอลโลก ตลาดหุ้นไม่ได้มีทิศทางเดียวเสมอไป บางปีหลังจบทัวร์นาเมนต์ตลาดปรับขึ้นแรง เช่น ฟุตบอลโลกปี 1994 ที่สหรัฐฯ ตลาดบวกต่อเนื่องหลังจบงาน ขณะที่บางปี เช่น 1998, 2002 และ 2006 ตลาดกลับเผชิญแรงกดดันหลังการแข่งขัน

จากข้อมูล Bloomberg report พบว่า ผลตอบแทนค่ากลางของตลาดหุ้นในช่วงฟุตบอลโลกอยู่ที่ราว 1.0% ระหว่างการแข่งขัน และ 4.6% ในช่วง 12 เดือนหลังจบการแข่งขัน สะท้อนว่า “บอลโลกอาจสร้างสีสันให้ตลาด” แต่ไม่ได้เป็นปัจจัยชี้ขาดทิศทางการลงทุน

ดังนั้น สิ่งที่สำคัญกว่าการลุ้นจังหวะสั้น ๆ คือการมีพอร์ตที่จัดโครงสร้างดีพอสำหรับหลายสภาวะตลาด

Beyond Wealth จึงจัดทีมกองทุนในแผน 4-3-3 เพื่อให้เห็นบทบาทของแต่ละกองทุนในพอร์ตอย่างชัดเจน

กองหน้า คือกลุ่มที่เน้นสร้างโอกาสเติบโต เพิ่มศักยภาพผลตอบแทนเชิงรุกให้พอร์ต

นำโดย MEGA10AI, SCBKEQTG และ LHCOPPER

กองกลาง คือกลุ่มที่ช่วยกระจายความเสี่ยง คุมจังหวะพอร์ต และลดการพึ่งพาตลาดใดตลาดหนึ่งมากเกินไป

ประกอบด้วย K-VIETNAM, ES-EG และ ASP-NGF

กองหลัง คือกลุ่มที่เน้นลดความผันผวน เสริมความมั่นคงให้พอร์ตในช่วงตลาดแกว่ง

ได้แก่ KKP-INCOME, UGIS, KT-CSBOND และ MAUTOCALL

ส่วน ผู้รักษาประตู อย่าง SCBGOLD ทำหน้าที่เป็นสินทรัพย์ป้องกันความเสี่ยง ช่วยรับมือกับความไม่แน่นอน ทั้งจากดอกเบี้ย ค่าเงิน ภูมิรัฐศาสตร์ และความผันผวนของตลาดโลก

📌 มุมมอง Beyond Wealth

สถิติในอดีตบอกเราว่า ช่วงฟุตบอลโลกอาจไม่ได้ทำให้ตลาดหุ้นขึ้นหรือลงแบบตายตัว เพราะผลลัพธ์หลังการแข่งขันขึ้นอยู่กับปัจจัยใหญ่กว่า ทั้งวัฏจักรเศรษฐกิจ เงินเฟ้อ ดอกเบี้ย กำไรบริษัทจดทะเบียน และความเสี่ยงภูมิรัฐศาสตร์

พอร์ตที่ดีจึงไม่จำเป็นต้องบุกหนักตลอดเวลา แต่ควรเป็นพอร์ตที่ “ยืนระยะได้” ในหลายสภาวะตลาด

ช่วงตลาดเปิดเกมรุก กองหน้าต้องเป็นตัวเร่งผลตอบแทน แต่ในวันที่ตลาดผันผวน กองกลาง กองหลัง และผู้รักษาประตูจะเป็นส่วนสำคัญที่ช่วยให้พอร์ตไม่เสียสมดุล

หัวใจของการลงทุนไม่ใช่การเลือกกองทุนที่ดูเด่นเพียงตัวเดียว แต่คือการจัดบทบาทของแต่ละกองทุนให้เหมาะกับเป้าหมาย ระยะเวลาลงทุน และระดับความเสี่ยงที่รับได้

เพราะสุดท้ายแล้ว ทั้งฟุตบอลและการลงทุนไม่ได้ชนะด้วยการบุกอย่างเดียว แต่ชนะด้วย “ทีมที่สมดุล” และแผนการเล่นที่เหมาะกับทุกจังหวะ

#BeyondWealth #BeyondSecurities #AssetAllocation #WorldCup2026

23

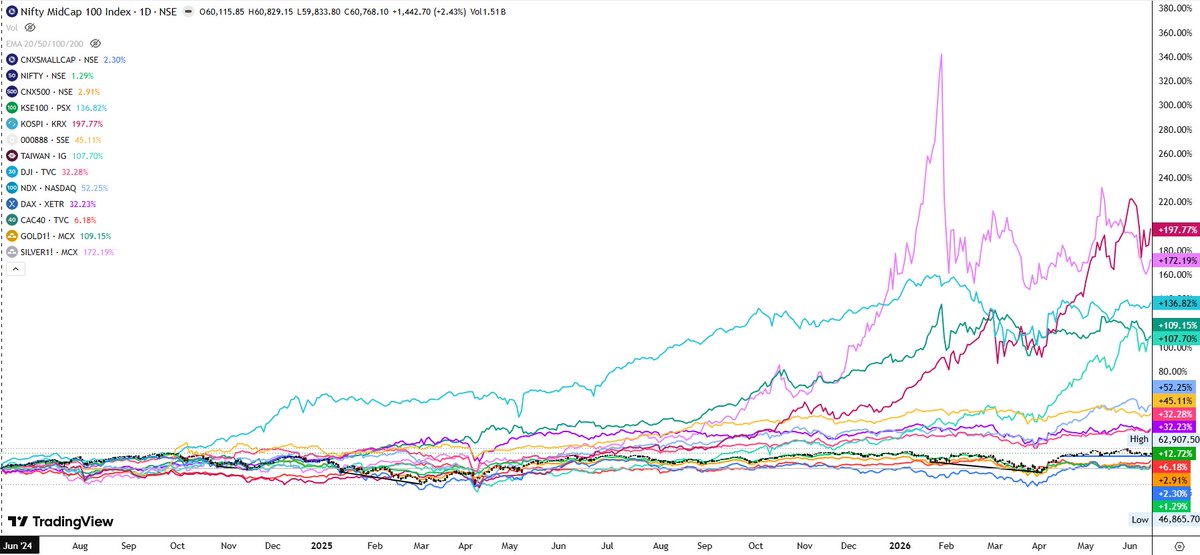

#Investing #Investment #Bullish #Nifty #Midcap #StockMarketIndia #Investing #TechnicalAnalysis #Nifty500 #Gold #Silver #Nifty50 #Investing #Commodities #AssetAllocation #MacroEconomics

🧵 Asset Class Performance: Equities Stall, While Gold & Silver Explode into a Mega Bull Run! 🪙🚀

If you are still only tracking equity returns, you are missing out on the real kings of the last 24 months. Between June 2024 and June 2026, precious metals have completely stolen the show while domestic equities remained locked in a tight consolidation.

The multi-asset leaderboard tells a fascinating macro story: 👇

1️⃣ The New Global Performance Leaderboard

🟣 KOSPI (South Korea Equity): 🚀 197.77% (Leading global tech/hardware)

🌸 SILVER (MCX): 🥈 172.19% (Outsized gains — Commodity Super-Cycle)

🟢 KSE 100 (Pakistan): 📈 136.82%

🟢 GOLD (MCX): 🥇 109.15% (Wealth protection turning into a multi-bagger)

🟢 TAIWAN (Taiwan Tech): 💻 107.70%

🔵 NASDAQ (US Tech): 🇺🇸 52.25%

🇮🇳 Indian Equities (Nifty/Nifty 500): 📊 1% to 3% (Completely flatlined).

@DAmmannaya

@drprashantmish6

@DRCHETANLALSETA

@VijayThk

@ADX_Learner

@AmitabhJha3

@TraderHarneet

@garwasanjay

@Rishikesh_ADX

@Investor_Mohit

@jitu_stock

2

2

116

You don’t need a crystal ball or a stock tip.

You need a clean asset allocation and a way to keep it in line.

Enrich lets you:

• Connect all your accounts in one place.

• Set goal‑based target allocations for each bucket in your life.

• Track drift and get step‑by‑step rebalance instructions when it’s time to act.

You stay in control of every trade. Flat subscription, no AUM.

#assetallocation #diyinvesting #goalbasedinvesting #taxawareinvesting #indexinvesting #longterminvesting #enrichfinance #personalfinance #investing

8

(3/8)

• The right asset allocation.

• Patience during volatility.

• Risk managed, not ignored.

• A long-term strategy that wasn't abandoned.

#assetallocation

1

35

💰 ₹𝟏 𝐂𝐫 𝐁𝐚𝐥𝐚𝐧𝐜𝐞𝐝 𝐏𝐨𝐫𝐭𝐟𝐨𝐥𝐢𝐨 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭 💰

How to split ₹1 Cr for Growth Stability Security:

𝐆𝐫𝐨𝐰𝐭𝐡: 𝟔𝟐%

Equity Mid/Small Cap: 30% → ₹30L

Equity Large/Flexi Cap: 20% → ₹20L

US Equity: 12% → ₹12L

𝐒𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲: 𝟐𝟔%

Gold ETF: 10% → ₹10L

REITs/InvITs: 8% → ₹8L

Debt Short Duration: 8% → ₹8L

𝐒𝐚𝐟𝐞𝐭𝐲: 𝟏𝟐%

NPS/PPF: 7% → ₹7L

Liquid/Emergency: 5% → ₹5L

Diversified across asset classes geographies = Peace of mind.

Save this for your next portfolio review 📌

Message Mutual funds/ Bonds / Insurance/ Unlisted-pre ipo/ PMS / AIF on WhatsApp. wa.me/919908550341

📩 DM for details

#PersonalFinance #Portfolio #AssetAllocation #MutualFunds #Equity #Gold #REITs #InvestingIndia #FinancialPlanning

#IPOAlert

1

134

Gold நல்லது...

ஆனா Wealth Create பண்ண அதுவே போதாது. 📈

சரியான Asset Allocation Long-Term Planning தான் பெரிய செல்வத்தை உருவாக்கும்.

#InvestmentSolutions #GoldInvestment #WealthCreation #FinancialPlanning #SmartInvesting #InvestmentSolutions #GoldInvestment #AssetAllocation #WealthCreation #FinancialPlanning #SmartInvesting #LongTermInvesting #PersonalFinance #WealthManagement #FinancialFreedom #GrowYourMoney #InvestmentStrategy #MoneyManagement #Anithamohan #Anithamohaninvestmentsolution

1

23h

I've received many similar questions from investors lately.

The Nikkei index has hit a new high.

Why do many people find the market increasingly difficult to understand?

I'm also continuously compiling my observations.

#JapanInvestment #AssetAllocation #MarketObservation

4

Jun 13

Rule of Thumb:

Equity Allocation = 100 − Your Age

So, if you’re 33, your ideal equity exposure is around 67%.

A simple way to balance growth and risk as you get older.

Do you follow this rule?

#Investing #PersonalFinance #AssetAllocation 📈

Jun 13

Investing by Age

✅Under 30

- Stocks - 70%

✅30 to 45

- Stocks - 65%

✅45 to 60

- Stocks : 45%

✅Above 60

- Stocks: 30%

What do you think?

1

5

364

Jun 13

A policy suggestion mentioned is Universal pre-distributive capital accounts. These are seeded at birth, expanding to workers most exposed to AI, which can be funded directly by equity in AI companies. #AssetAllocation #Equities #spacexstockprice

6

Are Gold ETF outflows a warning sign or a healthy market reset?

#GoldETF #AssetAllocation #PortfolioDiversification #WealthManagement #InvestmentManagement #CapitalMarkets #MarketVolatility #InvestorBehavior #FinancialPlanning #MutualFundIndustry

bfsi.economictimes.indiatime…

1

1

24

Jun 13

KS: Asset Allocation กลยุทธ์จัดพอร์ตกองทุนรวม เดือนมิถุนายน 2026 📊🌍

ไม่ว่าตลาดจะอยู่ในช่วงผันผวนหรือขาขึ้น การจัดสัดส่วนการลงทุน (Asset Allocation) ยังคงเป็นหัวใจสำคัญของการสร้างผลตอบแทนระยะยาวและบริหารความเสี่ยงของพอร์ต

🛍️ KS Mutual Fund แนะนำ 3 รูปแบบพอร์ตตามระดับความเสี่ยงที่รับได้

✅ Conservative (หุ้น 30 / ตราสารหนี้ 70)

เหมาะสำหรับผู้ที่ต้องการรักษาเงินต้นและลดความผันผวนของพอร์ต

Global Equity 21%

Global Fixed Income 49%

Cash 15%

Satellite Portfolio 15%

✅ Balance (หุ้น 60 / ตราสารหนี้ 40)

เหมาะสำหรับผู้ที่ต้องการสมดุลระหว่างการเติบโตและการบริหารความเสี่ยง

Global Equity 42%

Global Fixed Income 28%

Cash 4%

Satellite Portfolio 26%

✅ Aggressive (หุ้น 70 / ตราสารหนี้ 30)

เหมาะสำหรับผู้ที่มุ่งเน้นการเติบโตระยะยาวและรับความผันผวนได้สูง

Global Equity 49%

Global Fixed Income 21%

Satellite Portfolio 30%

📌 Product Highlight

KKP GNP : Global Equity

K-GDBONDUH : Global Fixed Income

K-CASH : เงินสด

A-GRID : หุ้น Global Infrastructure

KKP TECH-UH : หุ้นเทคโนโลยีสหรัฐฯ

ASP-NGF : หุ้นญี่ปุ่น

MINDIA : หุ้นอินเดีย

SCBKEQTG : หุ้นเกาหลีใต้

🎲 KS Smart Fund Tips:

Asset Allocation ที่ดีไม่ใช่การเลือกสินทรัพย์ที่ให้ผลตอบแทนสูงที่สุด แต่คือการจัดสัดส่วนให้เหมาะกับเป้าหมายการลงทุน ระยะเวลาลงทุน และระดับความเสี่ยงที่ยอมรับได้ เพื่อให้พอร์ตสามารถเติบโตได้อย่างยั่งยืนในทุกสภาวะตลาด

📊เปิดพอร์ตลงทุนกองทุนรวมกับ KS ลงทุนได้หลากหลาย บลจ. >> ksecurities.co/Open-Account_…

⛳Follow us :

📲 LINE : ksecurities.co/KS-LineOA

📲 Facebook: ksecurities.co/KS-Facebook

📲 Instagram: ksecurities.co/KS-Instagram

📲 Twitter: ksecurities.co/KS-Twitter

📲 YouTube: ksecurities.co/KS-Youtube

📲 Threads: ksecurities.co/KS-Threads

#KS #KSecurities #หลักทรัพย์กสิกรไทย #AssetAllocation #MutualFund #GlobalInvesting #PortfolioManagement #ลงทุนกองทุนรวม

คำเตือน : กรุณาทำความเข้าใจลักษณะสินค้า เงื่อนไขผลตอบแทน และความเสี่ยงก่อนตัดสินใจลงทุน

7

9

663

Jun 12

Research has shown that asset allocation is one of the most important drivers of portfolio return variability over time.

Portfolio construction isn't just about what you own.

It's also about how everything works together.

Find out more about Rareview Capital's goals-based investment approach at rareviewcapital.com.

#AssetAllocation #PortfolioConstruction #Investing

1

3

5

167

Jun 12

🚨 L’or recule de près de 30 % depuis son record historique. Faut-il y voir un signal d’alerte ? Pas forcément. Pour Pierre Sabatier @Pierre_Sabatier, président de PrimeView et de l’AUREP, l’or ne doit pas être analysé comme une action ou une obligation. C’est avant tout un « actif patrimonial » dont la fonction première est la préservation du patrimoine et la protection contre la perte de valeur des monnaies.

📉 L’once est revenue autour de 4 200 $, contre plus de 5 600 $ lors de son point haut.

À première vue, certains y voient un signal baissier.

En réalité, cette correction doit être replacée dans une tendance beaucoup plus vaste.

➡️ Au début des années 2000, l’or valait moins de 300 $ l’once.

➡️ Sa moyenne sur 30 ans est d’environ 1 168 $.

➡️ Sa moyenne sur 10 ans avoisine 2 000 $.

Autrement dit, même après sa récente baisse, le métal jaune évolue encore à des niveaux historiquement élevés.

💡 Ce que rappelle Pierre Sabatier est essentiel :

L’or n’est pas un actif spéculatif.

L’or est un actif patrimonial.

Sa vocation première n’est pas de générer de la performance mais de protéger le pouvoir d’achat accumulé au fil du temps.

Et c’est précisément là que le débat devient passionnant.

🌍 Les déficits publics explosent.

💸 Les dettes souveraines atteignent des records.

🏦 Les banques centrales ont profondément transformé les règles monétaires depuis deux décennies.

📈 Les créations monétaires massives ont alimenté une interrogation grandissante sur la valeur future des devises.

Selon Pierre Sabatier, la hausse structurelle de l’or depuis plus de 30 ans reflète avant tout une perte progressive de confiance dans la capacité des États à préserver durablement la valeur de leur monnaie.

⚠️ Aujourd’hui, le recul du métal jaune s’explique principalement par la remontée des rendements obligataires.

Quand les obligations souveraines rapportent davantage, elles deviennent temporairement plus attractives face à un actif qui ne verse aucun coupon.

Mais ce phénomène est-il durable ?

Rien n’est moins sûr.

Car derrière les discours rassurants, les fondamentaux restent inchangés :

🔹 Déficits publics massifs

🔹 Croissance économique fragile

🔹 Endettement historique

🔹 Consommation américaine qui ralentit

🔹 Risques géopolitiques persistants

📊 Et si les banques centrales devaient finalement revenir à des politiques plus accommodantes pour soutenir l’économie ?

Le débat est ouvert.

Une chose est certaine :

Pierre Sabatier rappelle qu’une assurance ne s’achète pas parce qu’elle monte ou parce qu’elle baisse.

Elle s’achète parce qu’on en a besoin.

Et c’est probablement la meilleure définition de l’or que l’on puisse donner.

🟡 Dans un monde où les certitudes économiques disparaissent les unes après les autres, le métal jaune continue de jouer son rôle historique : celui d’une protection contre les excès du système monétaire.

La volatilité est temporaire.

La préservation du patrimoine est permanente.

#Or #Gold #Investissement #Patrimoine #Epargne #Inflation #BanquesCentrales #PierreSabatier #PrimeView #AUREP #MarchesFinanciers #Finance #Economie #ValeurRefuge #GestionDePatrimoine #Investir #MacroEconomie #DettePublique #AssetAllocation #WealthManagement

1

1

12

789

Jun 12

Multi Asset Allocation Funds: Performance vs Portfolio Changes (May 2026 vs April 2026)

Fund managers are taking very different allocation calls despite operating in the same category.

The latest portfolio disclosures reveal meaningful shifts across Equity, Debt, Gold ETFs, and Silver ETFs, reflecting evolving market views and risk management strategies.

📊 Key Observations:

✅ Some funds increased equity exposure aggressively, while others reduced equity allocation by more than 10%.

✅ Debt allocations witnessed significant changes, indicating selective positioning towards stability and income generation.

✅ Gold and Silver allocations continue to be actively used for diversification and portfolio hedging.

✅ 1-Year returns range from low single digits to high double digits, highlighting the importance of asset allocation decisions over time.

A Multi Asset Allocation Fund is not just about past returns—understanding where the fund manager is allocating capital today may provide valuable insights into future strategy.

Which Multi Asset Allocation Fund's portfolio positioning looks most interesting to you?

⚠️ Disclaimer: Educational content only. Portfolio allocations are based on monthly disclosures as of May 2026 and may change without notice. Past performance and current positioning do not guarantee future returns.

#MultiAssetAllocation #MultiAssetFunds #MutualFunds #AssetAllocation #InvestmentResearch #MF360

Prepared by: Ankush Prajapati.

1

1

19

902

Jun 12

Think 60/40 is dead? Modern allocations use risk parity, factor mixes and alternatives - practical ETF steps to update your portfolio now.

Read more: stockalpha.ai/alpha-learning…

#Investing #AssetAllocation

1

It's Friday, your weekly dose of unbiased, clear, and focused financial wisdom will be LIVE today! #fridayinvestmentsatsang

Your Questions Answered: A dedicated, in-depth live Q&A where Parimal & Gaurav answer viewer questions about their portfolios, asset allocation, and market uncertainties with @ParimalAde & @gjyadnya

🔔 Set the reminder and follow @investyadnya for more such content so you don't miss future market insights!

#FinancialWisdom #InvestmentStrategies #MarketInsights #LiveQA #AssetAllocation

ALT It's Friday, your weekly dose of unbiased, clear, and focused financial wisdom! #investmentsatsang Your Questions Answered: A dedicated, in-depth live Q&A where Parimal & Gaurav answer viewer questions about their portfolios, asset allocation, and market uncertainties with @ParimalAde & @gjyadnya 🔔 Set the reminder and follow @investyadnya for more such content so you don't miss future market insights!

196

Jun 12

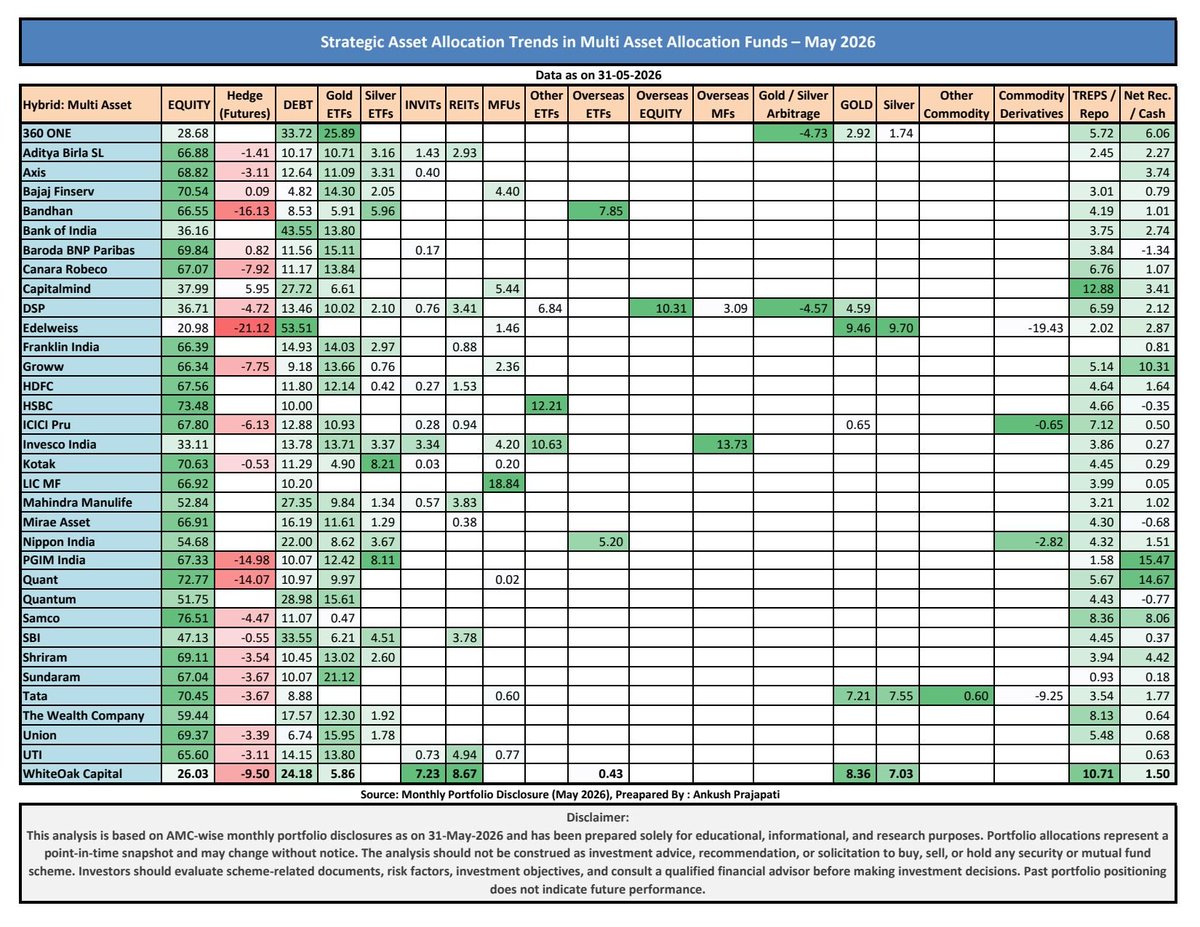

Multi Asset Allocation Funds: Strategic Asset Allocation Trends (May 2026)

Not all Multi Asset Allocation Funds are allocated the same way.

A detailed AMC-wise analysis of portfolio disclosures reveals significant differences in:

✔️ Equity Exposure

✔️ Debt Allocation

✔️ Gold & Silver Holdings

✔️ REITs & InvITs Exposure

✔️ Overseas Investments

✔️ Cash & Arbitrage Positions

Understanding these allocation decisions is critical because asset allocation often drives long-term investment outcomes more than security selection.

Source: AMC Monthly Portfolio Disclosures (Data as on 31-May-2026)

#MultiAssetFunds #MutualFunds #AssetAllocation

3

25

1,826

𝗛𝗼𝘄 𝗴𝗹𝗼𝗯𝗮𝗹 𝗳𝗮𝗺𝗶𝗹𝘆 𝗼𝗳𝗳𝗶𝗰𝗲𝘀 𝗮𝗿𝗲 𝗿𝗲𝘀𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗶𝗻𝗴 𝘁𝗵𝗲𝗶𝗿 𝗽𝗼𝗿𝘁𝗳𝗼𝗹𝗶𝗼𝘀

UBS’s Global Family Office Report 2026 shows that headline allocations look familiar, but risk is now being taken very differently inside portfolios.

For the first time in the report’s history, 60% of family offices globally plan to change their strategic asset allocation in the next 12 months - the highest reading UBS has recorded.

-----------------------

𝟭. 𝗣𝗿𝗶𝘃𝗮𝘁𝗲 𝗺𝗮𝗿𝗸𝗲𝘁𝘀 𝗿𝗲𝗯𝘂𝗶𝗹𝗱𝗶𝗻𝗴 𝗳𝗿𝗼𝗺 𝘁𝗵𝗲 𝗶𝗻𝘀𝗶𝗱𝗲

• 𝗥𝗲𝗮𝗹 𝗲𝘀𝘁𝗮𝘁𝗲: Down from 14% to a planned 8% - a sustained, deliberate cut to what once anchored most alternatives sleeves.

• 𝗣𝗿𝗶𝘃𝗮𝘁𝗲 𝗲𝗾𝘂𝗶𝘁𝘆: Peaked at 22% in 2023, pulled back to about 17%, and is expected to hold near that level through 2026 as liquidity and valuations are treated more cautiously.

• 𝗣𝗿𝗶𝘃𝗮𝘁𝗲 𝗱𝗲𝗯𝘁 & 𝗶𝗻𝗳𝗿𝗮: Private debt has risen from 2% to 3%, while infrastructure is building towards 2% from almost zero pre‑2023, driven by power and energy demand from the AI build‑out.

• 𝗢𝘃𝗲𝗿𝗮𝗹𝗹 𝗺𝗶𝘅: The headline 56:44 traditional‑to‑alternatives split is intact, but the alternatives sleeve has shifted from “property PE” to a broader mix of PE, private debt, infra and gold.

-----------------------

𝟮. 𝗙𝗮𝗺𝗶𝗹𝘆 𝗼𝗳𝗳𝗶𝗰𝗲𝘀 𝗿𝗲𝘁𝗵𝗶𝗻𝗸𝗶𝗻𝗴 𝘁𝗵𝗲𝗶𝗿 𝗱𝗼𝗹𝗹𝗮𝗿 𝗲𝘅𝗽𝗼𝘀𝘂𝗿𝗲

• 𝗣𝗲𝗿𝗰𝗲𝗶𝘃𝗲𝗱 𝗿𝗶𝘀𝗸: 47% of family offices say they are over‑exposed to the US dollar - unique among major currencies.

• 𝗢𝘂𝘁𝗹𝗼𝗼𝗸: 65% expect confidence in the dollar’s reserve‑currency role to weaken.

• 𝗥𝗲𝘀𝗽𝗼𝗻𝘀𝗲: 29% have reduced, or are considering reducing, USD assets, and 30% are diversifying into other currencies, with the Swiss franc and euro preferred.

• 𝗛𝗲𝗱𝗴𝗲: Gold is planned at about 3% of portfolios in 2026 as a compact hedge against currency and geopolitical risk.

-----------------------

𝟯. 𝗔𝗜: 𝗰𝗼𝗻𝘃𝗶𝗰𝘁𝗶𝗼𝗻 𝗿𝘂𝗻𝗻𝗶𝗻𝗴 𝘄𝗲𝗹𝗹 𝗯𝗲𝘆𝗼𝗻𝗱 𝗹𝗶𝘀𝘁𝗲𝗱 𝘁𝗲𝗰𝗵

• 𝗜𝗻𝘁𝗲𝗻𝘁: In 2024, 78% of family offices said AI was likely to be an area of investment within 2–3 years.

• 𝗜𝗺𝗽𝗹𝗲𝗺𝗲𝗻𝘁𝗮𝘁𝗶𝗼𝗻: By 2026, 65% are already invested across semiconductors, data centres, software platforms and healthcare, with more planning to add.

• 𝗕𝗿𝗲𝗮𝗱𝘁𝗵: ~37% now allocate to power and resources and infrastructure, and about a third to AI‑enabled healthcare - AI exposure has shifted from a few tech names to a spread across chips, power, data centres and healthcare.

-----------------------

𝗖𝗹𝗼𝘀𝗶𝗻𝗴 𝘁𝗵𝗼𝘂𝗴𝗵𝘁:

Taken together, these trends show how little the headline mix has changed, and how much the underlying exposures have - most of the action is now happening inside the sleeves rather than in the top‑line split.

💡 The chart below goes 𝗱𝗲𝗲𝗽𝗲𝗿 and compares global strategic asset allocation in 𝟮𝟬𝟭𝟵 𝘃𝘀 𝘁𝗵𝗲 𝟮𝟬𝟮𝟲 𝗽𝗹𝗮𝗻, highlighting how much of this rewiring has happened within a familiar top‑line mix. 👇🏼

#FamilyOffice #AssetAllocation #Investing #MProfit

4

6

1,307