Professor at @MITSloan working on finance, macroeconomics, international economics, economic history, and other fun stuff

Joined December 2014

- Tweets 1,708

- Following 638

- Followers 4,896

- Likes 2,930

157 Photos and videos

Pinned Tweet

Jan 28

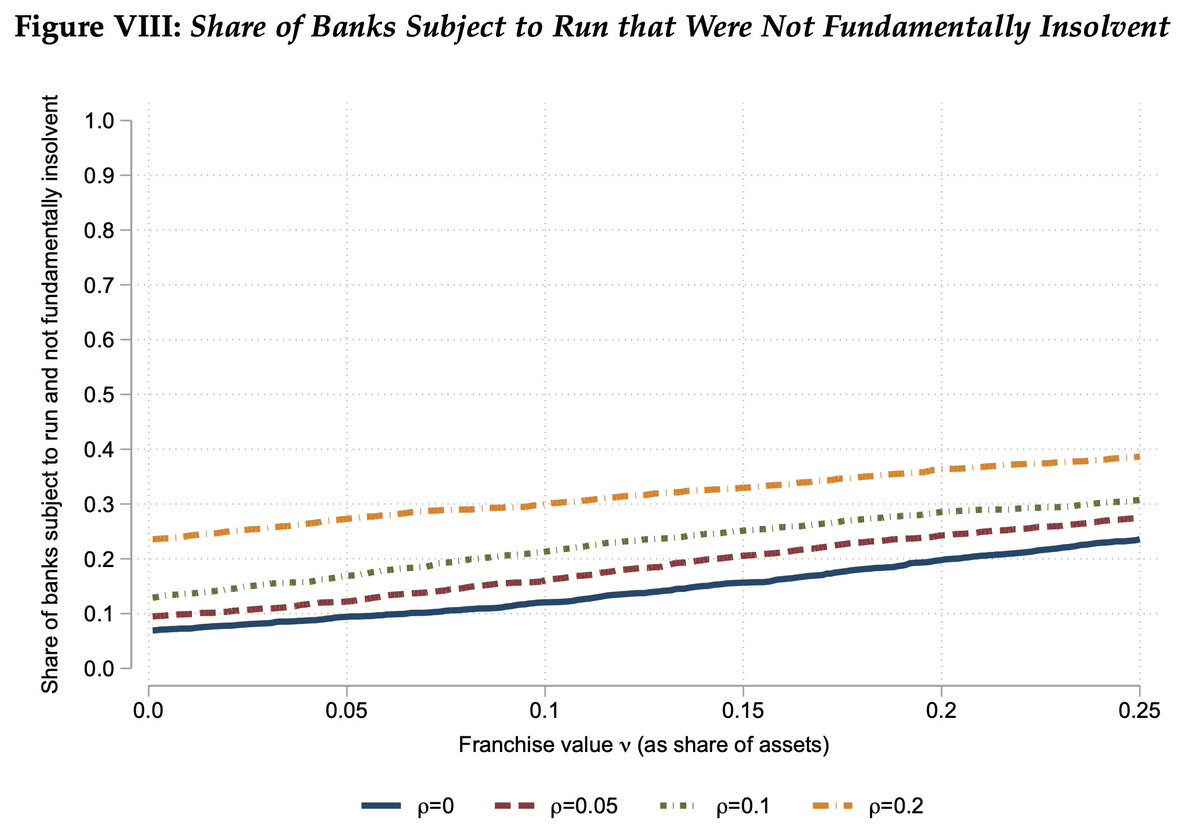

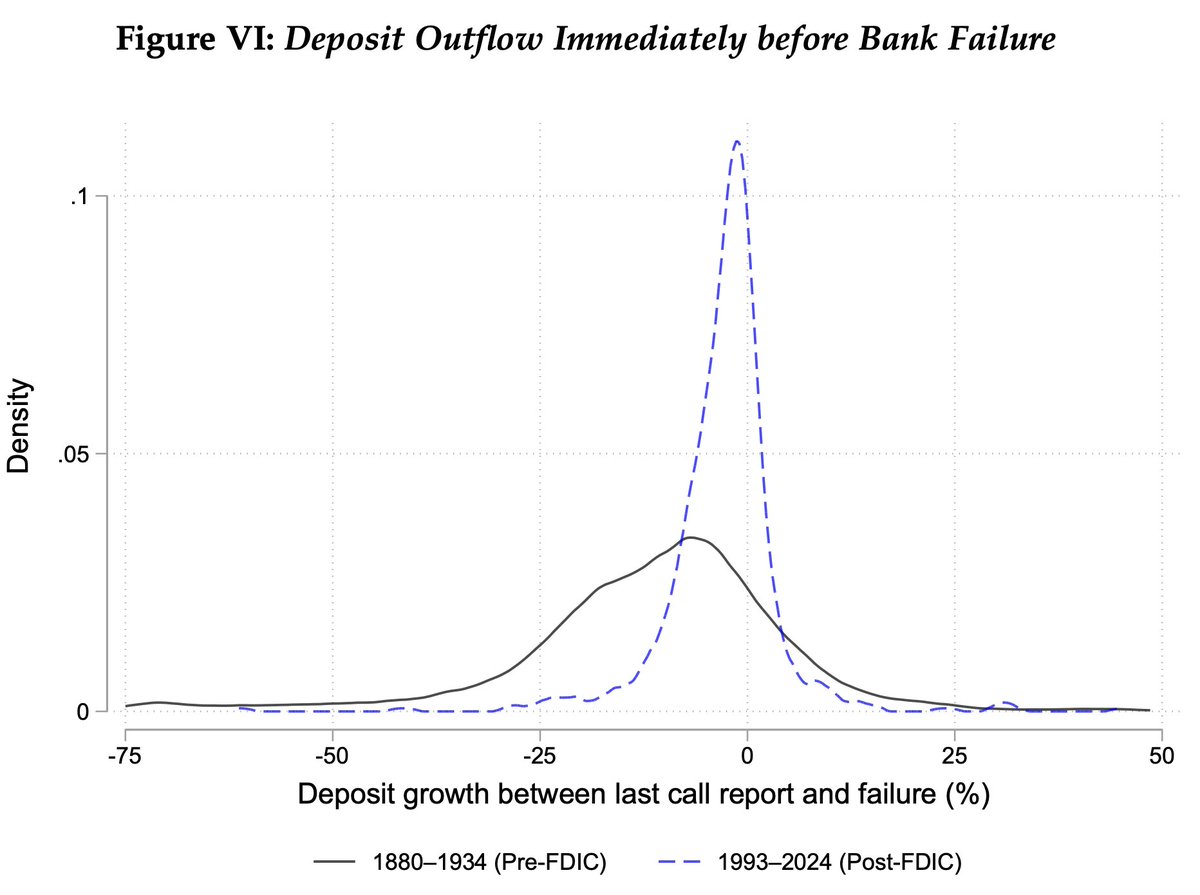

New paper on bank runs with Correia and Luck:

"Bank Runs With and Without Bank Failure"

Questions:

- What are the determinants of runs?

- When do bank runs result in bank failure?

- Can runs trigger the failure of healthy banks and amplify small shocks into large crises?

- Are runs themselves the initial cause of financial distress or are they a symptom of deeper fundamental solvency problems in the financial system?

What we do:

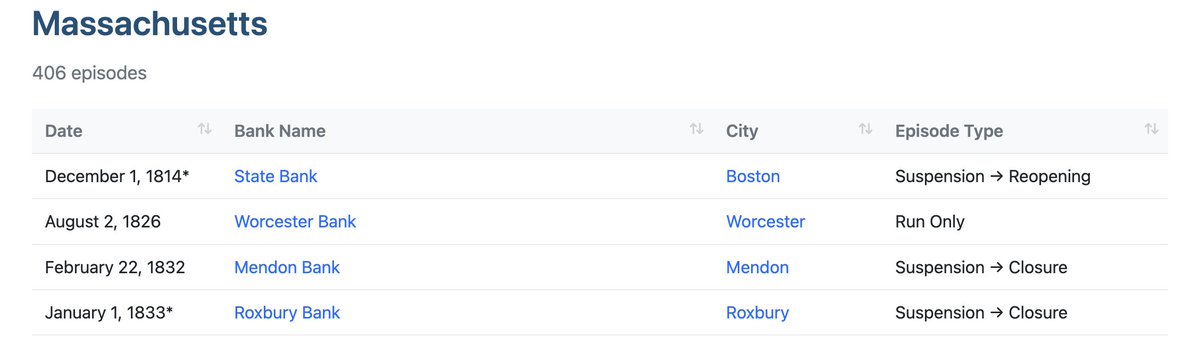

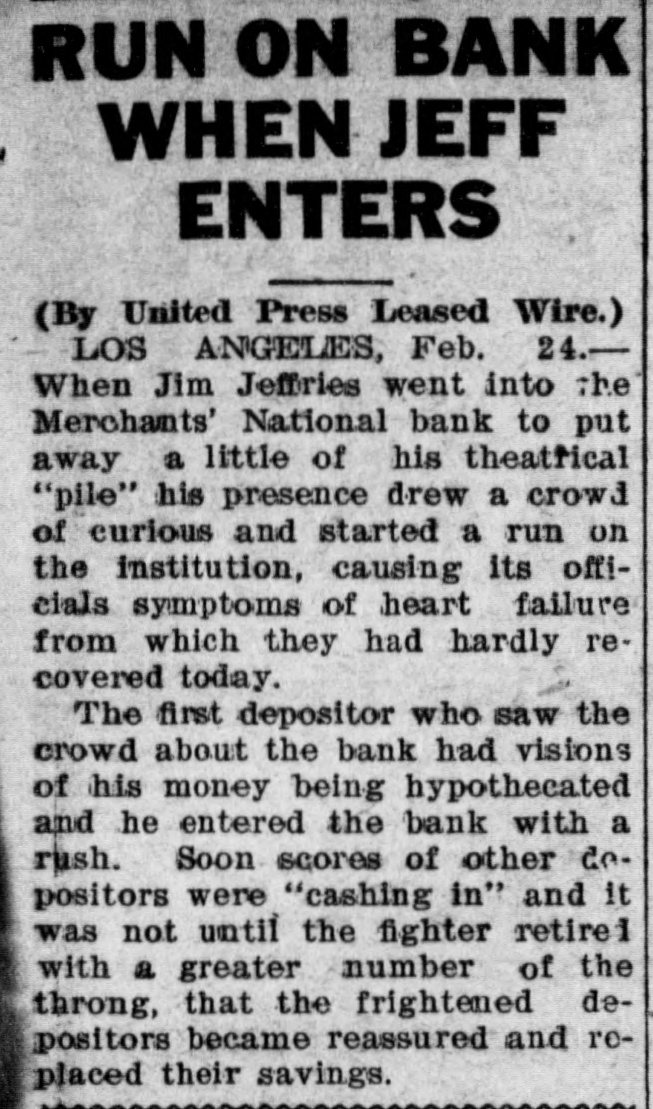

- Apply LLMs to historical newspapers to uncover over 4,000 runs on individual banks in the pre-FDIC US banking system from 1863 to 1934. Capture the most famous runs (Bank of the US

- Merge data on runs and other bank-level events discussed in newspapers (suspensions, failures) to bank-level fundamentals (harder than it sounds!)

What we find:

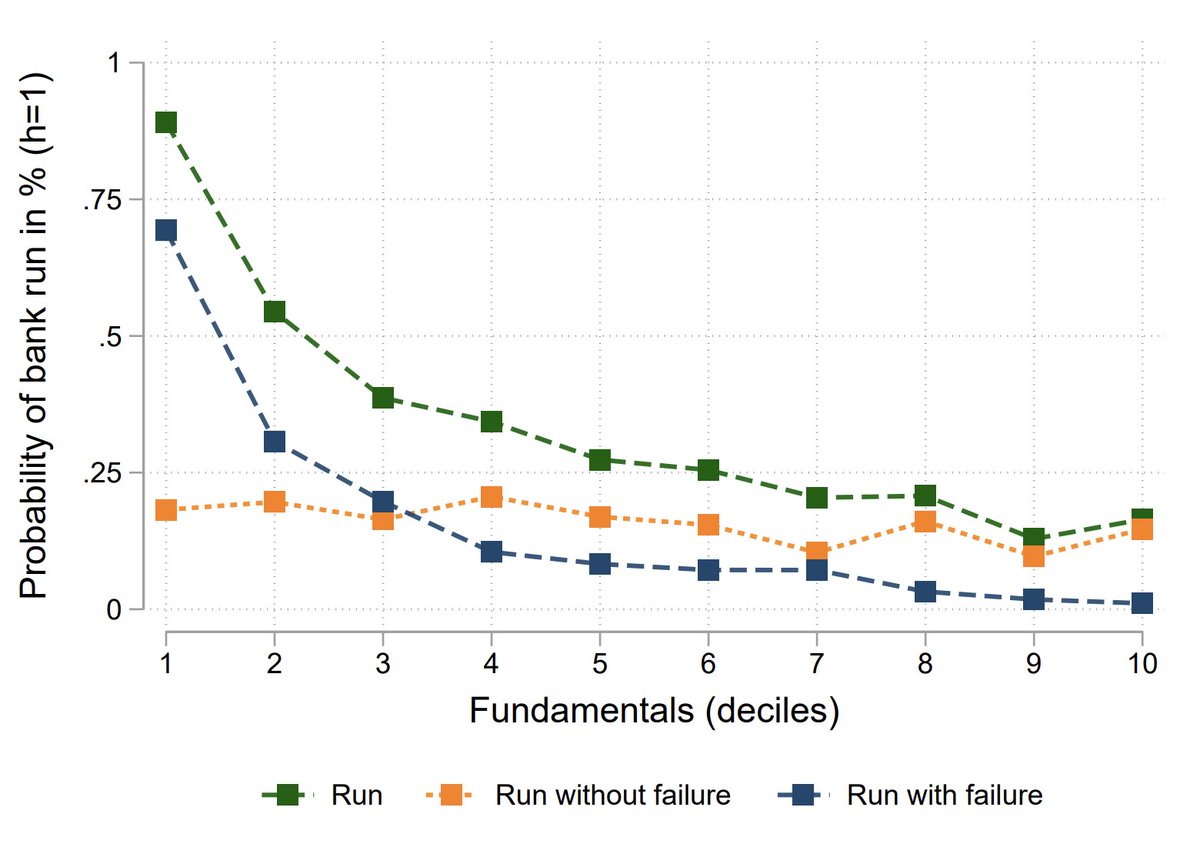

(1) Runs are considerably more likely in weak banks, but can also occur in strong banks, especially in response to negative news about the real economy or the broader banking system.

(2) However, runs typically only result in failure for banks with weak fundamentals [see figure below]. Strong banks survive runs through various mechanisms, including interbank cooperation, equity injections, public signals of strength, and suspension of convertibility

(3) At the local level, poor fundamentals necessary for runs to translate into large declines in lending. Moreover, bank failures (with and without runs) translate into substantially larger declines in deposits and lending than runs without failures.

Overall takeaways:

- Poor fundamentals are key for whether runs pass through into failure and have severe consequences for the broader economy.

- The findings temper the view that small shocks can result in large jumps to bad equilibria via runs on demandable debt.

Full paper here. Comments welcome. Given the methodology and evolving AI tools, we expect to make refinements to the runs database over time. Any input is welcome.

static1.squarespace.com/stat…

3

56

188

53,304

Jun 8

Two points:

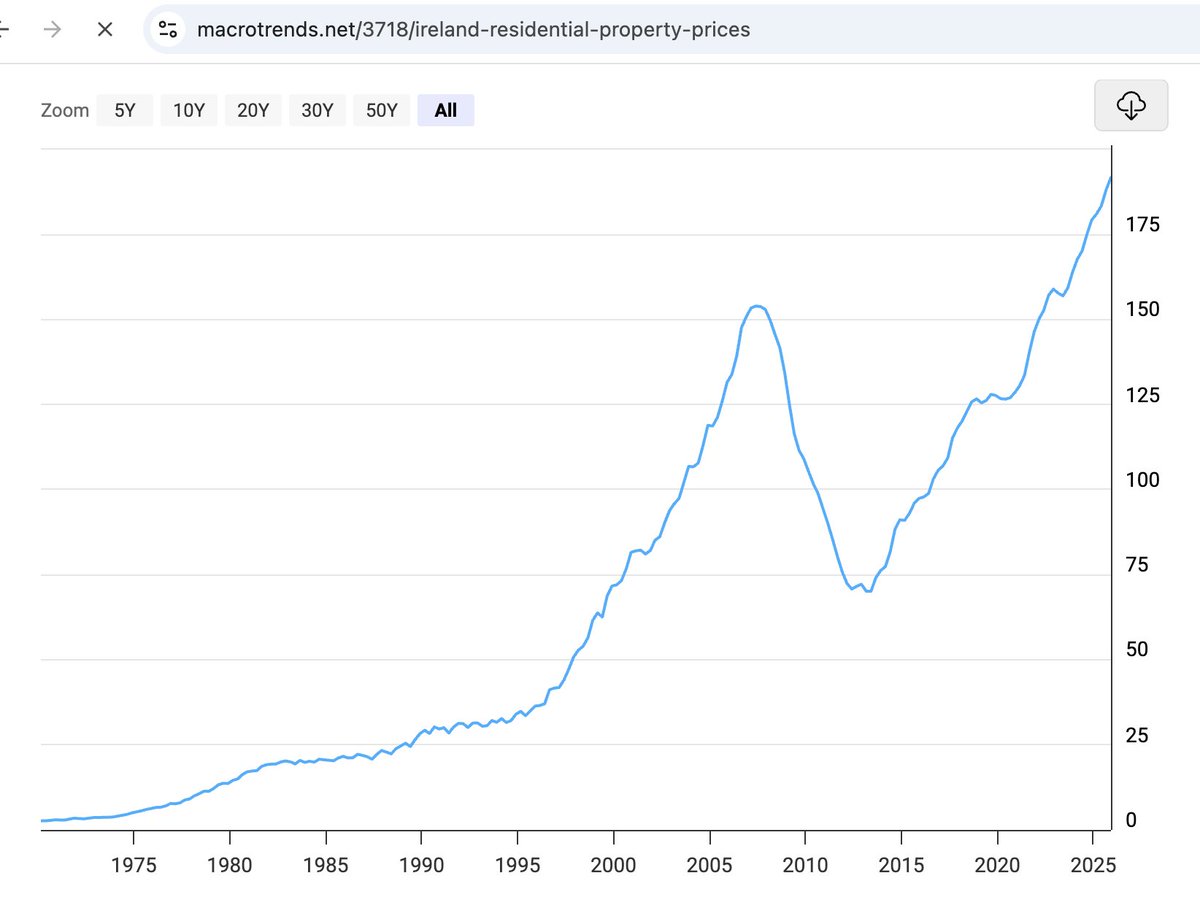

1. The boom-bust-boom was a feature of many of the housing markets in the 2000s-2020s, both across US regions and internationally.

2. The fact that there was a rebound does not disprove that valuations were extremely stretched in 2005-06. Most bubbles are based on optimism that has some fundamental kernel of truth but gets massively exaggerated (see Kindleberger...). The key issue in the 2000s boom was not just the bubble in house prices but the massive expansion in household leverage.

I'm not familiar with all those countries, but Ireland house prices recovered pretty quickly after the bust.

Was there really a "massive" bubble here at all?

2

3

19

2,967

Jun 8

On point 1, see the evidence here

x.com/EmilVerner/status/1428…

19 Aug 2021

Interesting new paper on the 2000s house price boom in the US, taking the perspective of longer-term house price dynamics from the late 1990s to today.

There are some similar patterns in international data, which I think are worth noting. 1/

4

1,107

Jun 8

Interesting speech from Governor Barr: "Deregulating in a Financial Boom: What Could Go Wrong?"

federalreserve.gov/newsevent…

7

25

2,690

Emil Verner retweeted

NEW DANISH GOVERNMENT IS (FINALLY) FORMED

- Who are they?

- What's the agenda?

- What does this mean for European politics?

2

4

15

3,344

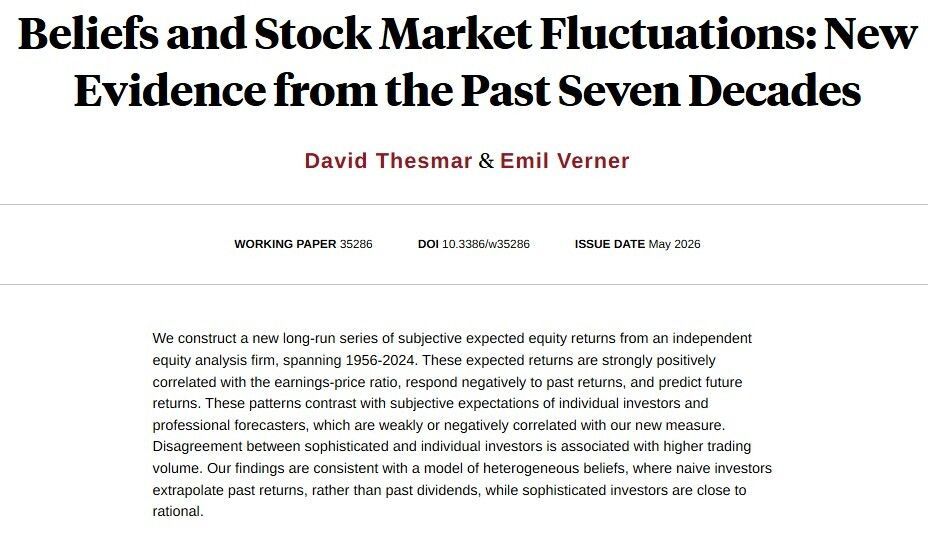

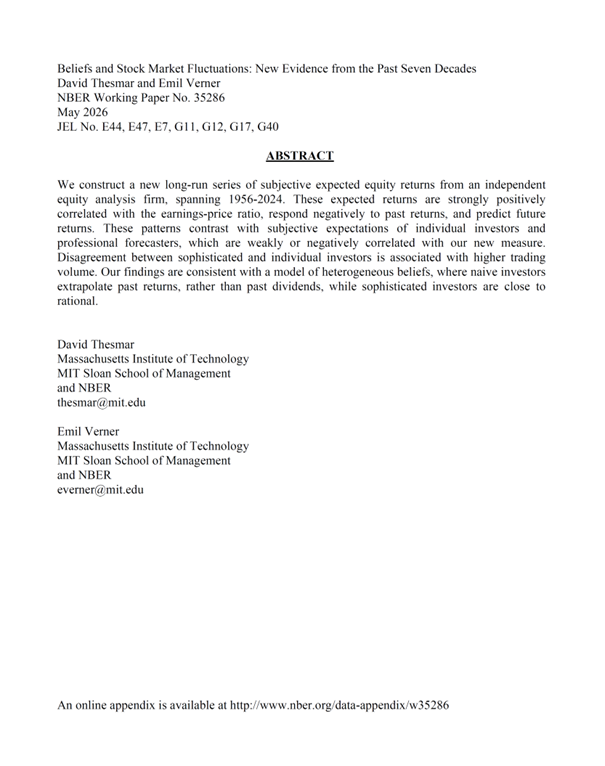

Sophisticated analysts' expected stock returns are strongly correlated with valuations, are contrarian, and predict future returns, in contrast with individual investors, from @dthesmar and @EmilVerner nber.org/papers/w35286

8

74

8,229

Jun 3

I've really been enjoying @DavidBeckworth @Macro_Musings podcast lately (we are in a golden age of econ podcasts!). A recent episode with former CEA chair Tyler Goodspeed takes on a fascinating question: Are recessions driven by random shocks (bad luck) or the product of inherently cyclical boom-bust phenomena? Goodspeed's new book argues it's the former. The episode is good fun and very interesting.

mercatus.org/macro-musings/t…

Two thoughts I wanted to share in reaction, given that this is a topic close to my heart:

1) Somewhat ironically, even though we call short-run fluctuations business *cycles*, the random shocks view is close to the mainstream approach in academic macro. A long tradition in time series macro going back to Granger's work in the 60s looks at the properties of macroeconomic time series (spectral densities!) and finds that there is not much evidence of stable, regular cycles in macro series. Modern DSGE macro models expansions/recessions as the product of relatively persistent shocks, rather than endogenous cycles. The view that business cycles are the product of endogenous boom-bust dynamics is slightly more on the periphery of macro than people might think!

2) That said, I would push back a bit on the strongest version of the random shocks view. I agree that a lot of variation at business cycle frequencies comes from random shocks. But there is quite a bit of evidence that the endogenous boom-bust story has some truth, at least during specific episodes featuring credit and financial booms preceding financial crisis recession. There is quite a bit of evidence that rapid expansions in credit, especially to certain risky sectors like real estate, coupled with booming prices of real estate and other assets, are a strong predictor of future downturns and financial crises. Financial crises are not unpredictable "bolts from the blue." While the exact timing of a crisis is very hard to predict, there are certain vulnerabilities that make financial crises and deep recessions more likely. These dynamics don't hold mechanically during every business cycle, but they do matter for understanding major downturns involving financial instability.

A few examples off the top of my head include: 2008 in the US, Spain, Ireland, etc; the Japanese financial crisis after the 1980s boom; the crises and deep recessions in the Nordic economies of late 1980s; emerging market crises like Mexico 1994 and Thailand 1997; or historical crises like Australia’s housing boom and bust in the late 1880s, the panic of 1893, and perhaps the US Great Depression.

1

24

92

9,394

Jun 3

Some references for the latter view:

- Jorda-@MSchularick-Taylor's great work.

aeaweb.org/articles?id=10.12…

onlinelibrary.wiley.com/doi/…

- Beaudry-Galizia-Portier (more focused on US time series): aeaweb.org/articles?id=10.12…

- Greenwood-Hanson-Shleifer-Sorensen: onlinelibrary.wiley.com/doi/…

- My work with @AtifRMian and @profsufi on household credit booms: academic.oup.com/qje/article…

- My work with @KarstenMueIIer on real estate/non-tradable sector credit booms:

academic.oup.com/restud/arti…

1

8

31

2,472

Jun 3

Nice point. I had exactly the same thought when I read the original Krugman substack post, which indeed basically adopts the Cobb-Douglas/Cole-Obstfeld setup. In the special Cole-Obstfeld case, there is full risk-sharing through the terms of trade. The US becomes more productive, which pushes down the price of US goods, leading to the same real income and consumption in the US and EU. In the data, I think the elasticity of substitution could even be less than one... So this would strengthen the benefits for the foreign country through the ToT.

But this result is sensitive. A lot is missing from the simple model: include market power/rents, productivity externalities, AI might be partly nontradable... Maybe the Garicano side is relatively more concerned about these effects. I would be curious to know where the current international literature stands on the effects of different types of foreign productivity shocks on income/welfare.

I'm not sure, but maybe one can think about the debate between @lugaricano and @paulkrugman as follows. The US produces AI and a non-tradable. Europe produces European vacations and a non-tradable. All the productivity growth is in AI. If AI and European vacations are good substitutes, US living standards will rise relative to Europe. If they enter preferences in a Cobb-Douglas fashion, the US will have all the productivity growth, but in purchasing power terms both regions will do equally well. So I think they are arguing about whether or not Cole and Obstfeld applies.

3

2

41

8,418

Emil Verner retweeted

Super interesting!

"Beliefs and Stock Market Fluctuations: New Evidence from the Past Seven Decades" by David Thesmar and Emil Verner.

"We construct a new long-run series of subjective expected equity returns from an independent equity analysis firm, spanning 1956-2024. These expected returns are strongly positively correlated with the earnings-price ratio, respond negatively to past returns, and predict future returns. These patterns contrast with subjective expectations of individual investors and professional forecasters, which are weakly or negatively correlated with our new measure. Disagreement between sophisticated and individual investors is associated with higher trading volume. Our findings are consistent with a model of heterogeneous beliefs, where naive investors extrapolate past returns, rather than past dividends, while sophisticated investors are close to rational."

nber.org/papers/w35286

8

42

2,658

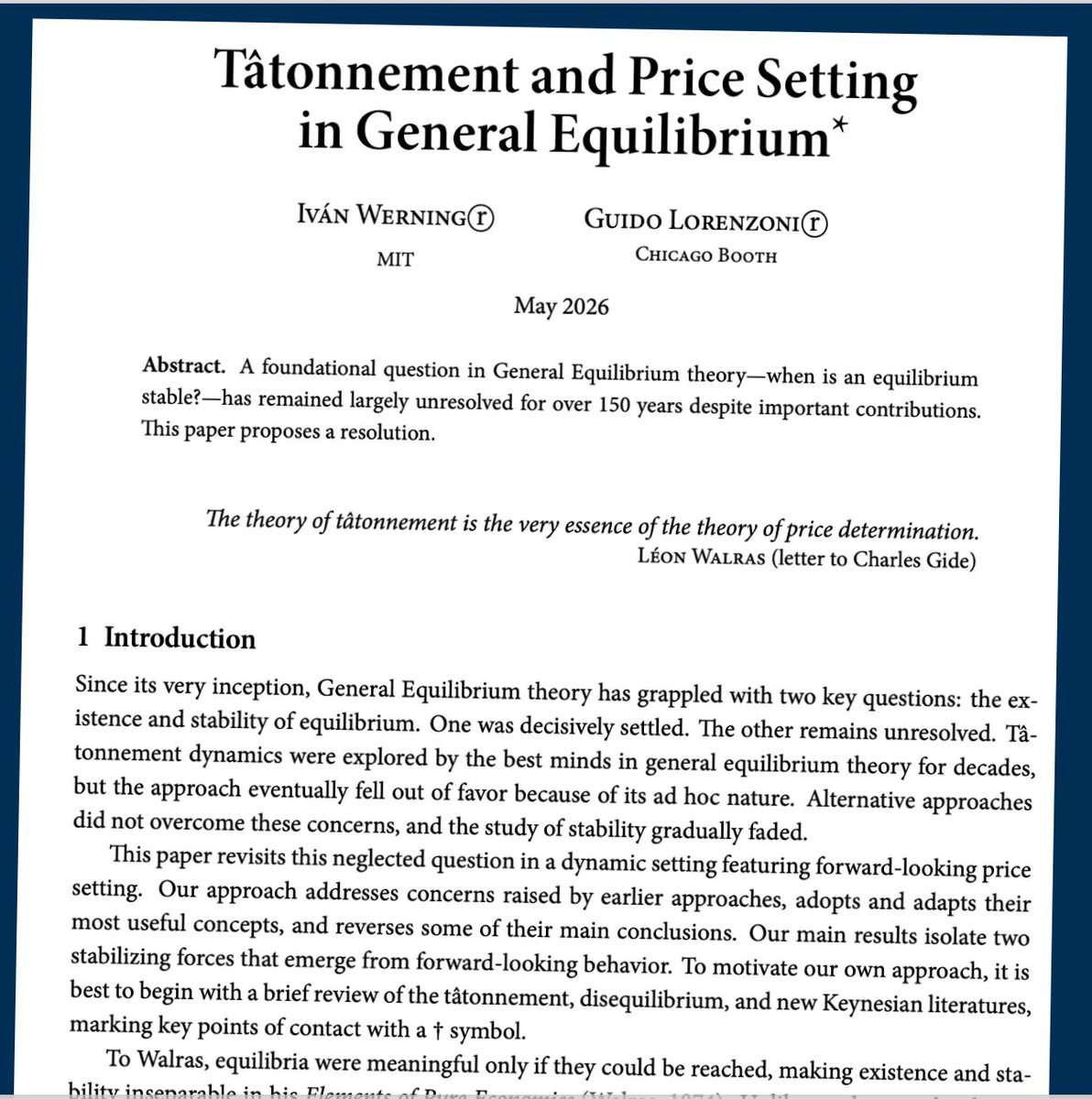

Emil Verner retweeted

May 31

Excited to FINALLY release toughest most rewarding paper I've worked on...

….we attack a 150 year old Walras question that's gone unanswered, not for lack of trying (Hicks, Samuelson, Arrow; our chances?😱)...

Q: Is the market equilibrium stable or unstable?¯\_(ツ)_/¯

🧵

51

426

1,863

1,021,376

Emil Verner retweeted

May 27

🧵Some remarks on this. First, there’s no question that entry into Canadian banking has long been limited. But during the heyday of free banking there, the entry limits weren’t as important as they became later.

3/ There are no perfect historical analogies for or against stablecoins as private money. Canada did not have crises under free banking for the same reason it had no crisis in 2008: its banking system was national, oligopolistic, and more heavily regulated than in the U.S.

2

9

25

6,872

Emil Verner retweeted

May 25

🧵I reckon myself a @greg_ip fan. But like many others he goes wrong here in claiming, on the base of antebellum U.S. experience, that competitively supplied private currencies are bound to be inefficient.

May 25

Stablecoins Are Private Money. That’s Why They’re a Risk to the Economy. Greg Ip, like most of the WSJ writers, think their readers are dumb. I am not a crypto advocate, and allocate less than 1% to crypto. wsj.com/finance/currencies/s…

3

10

43

18,985

Emil Verner retweeted

May 26

🇧🇷 The 1970 Brazil team in 4K is quite something.

67

592

5,125

250,831

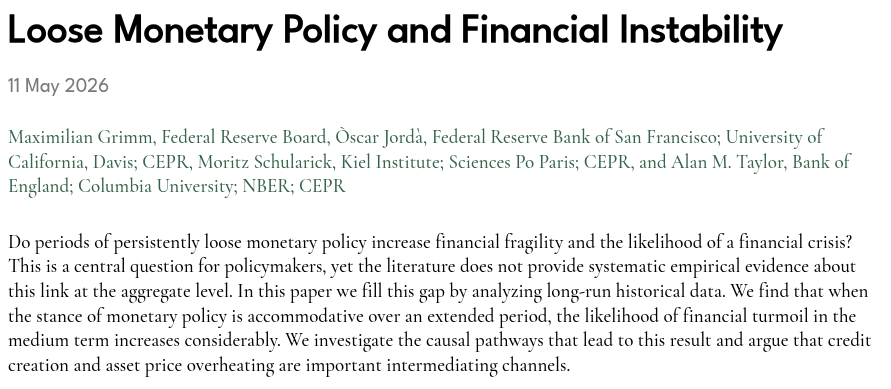

Emil Verner retweeted

New paper by Grimm, Jordà, Schularick, and Taylor

restud.com/loose-monetary-po…

#REStud

#EconX

#EconTwitter

24

81

8,028

Emil Verner retweeted

May 16

RIP Ned Phelps

Ned Phelps followed his own intellectual journey.

When Keynesians relied on a long-run tradeoff between unemployment and inflation, he showed why this was a weak reed to stand on. Thus was born the natural rate hypothesis (although the coining of the word goes to Friedman, a year after Ned’s paper).

When, later, New Keynesians were focusing on nominal rigidities, he built models of fluctuations where nominal rigidities played no role. When New Classicals were exploring the cyclical implications of competitive markets, he focused on the role of distortions in goods and labor markets, be it efficiency wages, or variable markups.

It would be fair to say that, today, the frontier macro models embody the natural rate hypothesis, and many of the distortions Ned focus on---and, what he did not like, i.e. nominal rigidities.

His style was highly idiosyncratic. He was often a poor expositor of his fundamental insights. He did not listen much to others, pursuing his agenda with focus and passion. But, to use an overused but appropriate expression, he was certainly one of the giants in the field. We often met and sometimes fought, be it on hysteresis or nominal rigidities, but I had infinite respect for him.

5

168

502

111,747

Emil Verner retweeted

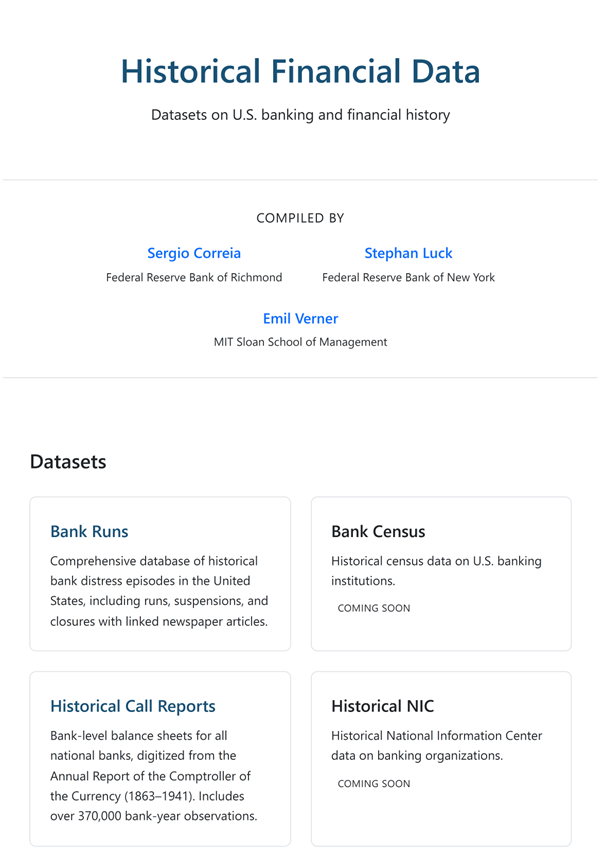

Really cool!

"Historical Financial Data: Datasets on U.S. banking and financial history" by Sergio Correia, Stephan Luck, and Emil Verner.

finhist.com/

43

161

7,464

Emil Verner retweeted

Amazing resource! What a public good!!

May 14

For researchers interested in U.S. banking and finance, we are sharing a new data resource!

It contains information on bank balance sheets, bank runs, and bank failures from the 19th century to the present:

1

4

29

5,367

May 14

For researchers interested in U.S. banking and finance, we are sharing a new data resource!

It contains information on bank balance sheets, bank runs, and bank failures from the 19th century to the present:

2

145

612

61,862

May 14

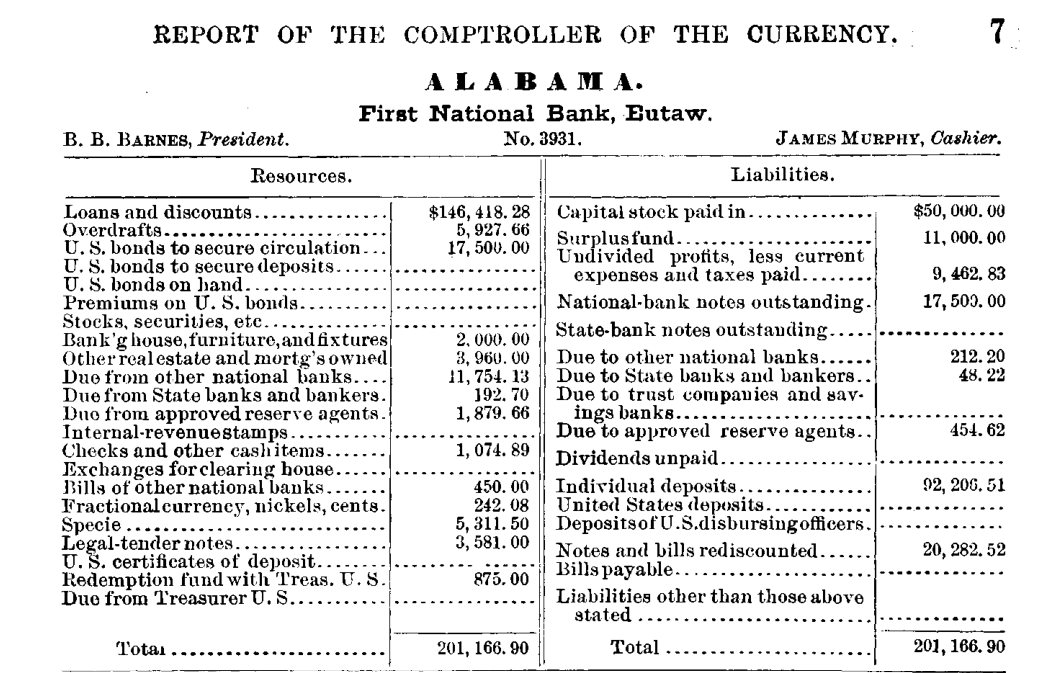

Dataset #2: Historical Call Reports.

Provides bank-level balance sheets for all national banks from 1863 to 1941, digitized from the Annual Report of the Comptroller of the Currency. Includes over 370,000 bank-year observations for over 14,000 banks.

finhist.com/historical-call/…

1

2

7

864

May 14

Dataset #3: Modern Call Reports, 1959-2025.

Contemporary reports on the condition of income for U.S. commercial banks from 1959 to the present.

More information in this thread:

x.com/EmilVerner/status/2003…

/end

22 Dec 2025

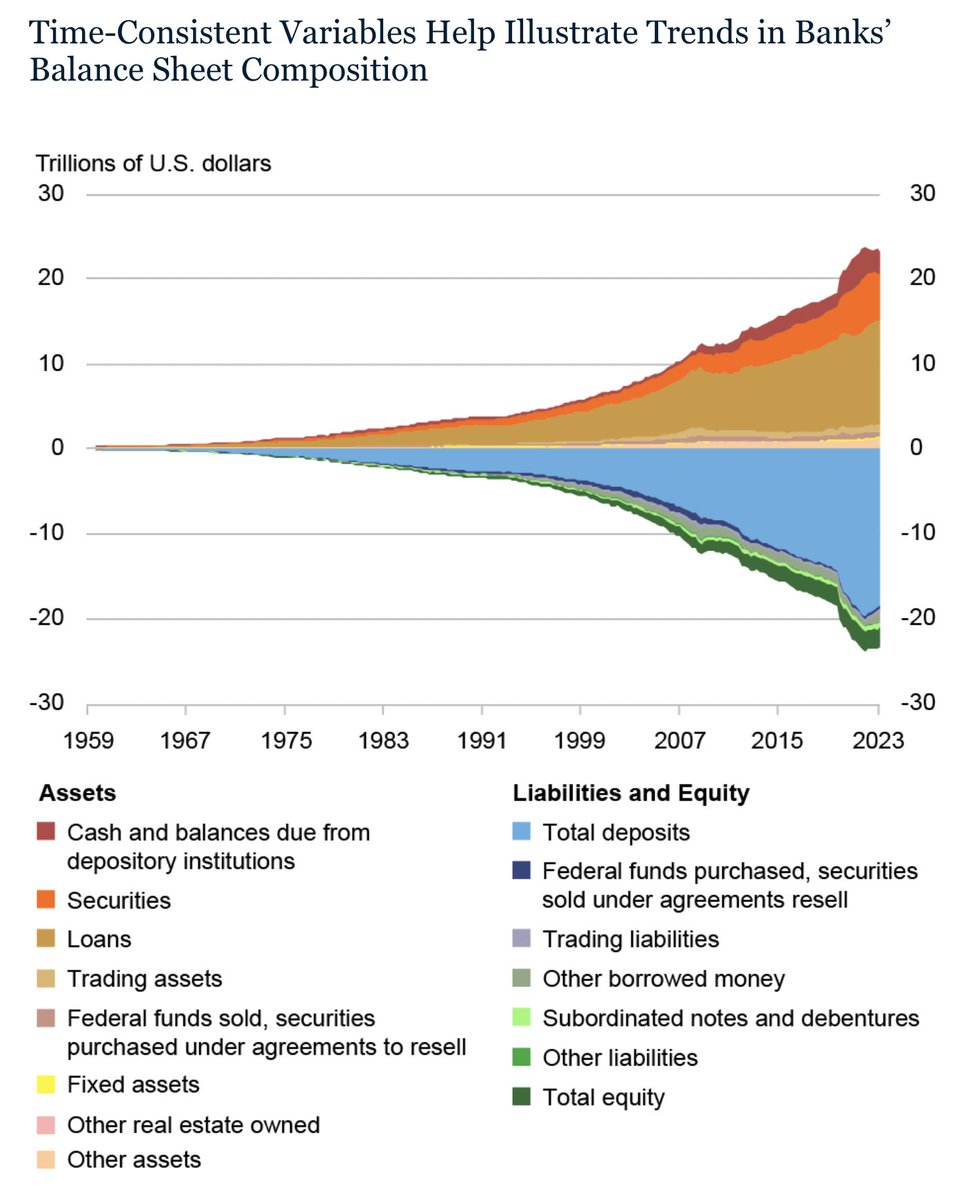

🚨New dataset🚨

Time-consistent balance sheets and income statements for commercial banks in the United States from *1959* to 2025.

newyorkfed.org/research/bank…

1/

2

1

11

1,082