Retail investor posting into the ether. Fundamental Analysis. Earnings reviews in the link below

Joined February 2023

- Tweets 4,610

- Following 777

- Followers 2,403

- Likes 6,892

751 Photos and videos

Pinned Tweet

1 Jul 2025

Farewell to my Value Edge moniker. I have decided to rebrand, something I’ve thought of doing for a while. I’ll still write under “the value edge” on seeking alpha, but will explain the purpose and future direction of my account here on X.

It’s long been my dream, presumably like many of you, to run my own investment operation as my full time job. While I don’t yet have the capital required to do that, I want to start taking definitive steps to make that dream a reality. Step 1 is a rebrand to the name I ultimately will use, which is Entropy Capital.

Why Entropy? Entropy is the phenomenon that all matter tends towards randomness. It’s a constant reminder that markets are far too complex for us to predict with 100% accuracy. There is always some seemingly random variable that can blow a hole in your thesis. You must always remain vigilant, and your stocks must always earn the right to be owned by it.

The concept of entropy ties quite nicely with my fascination of nonlinear dynamics. The concept that small changes in the starting state of function can yield drastically different outputs. Beating the market is a pursuit for nonlinearity. Every day upon market open out portfolio has a starting state for that day. You control what that state is. Over time, finding the optimal state for your portfolio (what stocks you own) is the only variable that matters.

My content moving forward will remain primarily focused on my portfolio as it always has. Eventually I’ll monetize my X and Substack, but I have no plans to do that in the foreseeable future.

With that, I’m excited to continue along on this journey with you! Let’s get richer together.

1

6

2,798

Entropy Capital retweeted

Jun 2

Documenting the headwinds I now see for AI.

It won't seem like it, but I love AI and am long-term positive. But when "math doesn't math" I take note.

1. The core thesis for foundation model lab investment has been high upfront investment made worthwhile by significant long-term profits.

2. These are capital intensive businesses and the compute commitments are very high relative to revenue and require strong growth over long time periods. The "leverage" (commitments versus revenue) is extremely high.

3. The fundamentals are not as positive as they previously were:

• Input costs are higher (commodities, chips, power)

• Interest rates are higher

• Competition is more intense

• Scaling Laws are now problematic: exponential costs/power cannot continue

4. Forecasting compute spend is challenging and high risk due to (a) revenue uncertainty and (b) algorithm uncertainty

5. Revenue growth appears to be slowing. The technology is valuable, but ROI is proving to be more expensive and take longer than anticipated.

6. The future is likely "different models for different use cases" with the lower end of the market being highly competitive.

7. Core use cases such as agentic software engineering are likely to need approaches beyond next-token prediction. They are Σ₂ᴾ complexity problems requiring multi-objective optimization and likely a combination of Transformers and other methods.

8. Current forecasts in memory makers are built largely on quadratic attention. That will not persist: we are already seeing work from DeepSeek, Minimax and Nvidia that can cut RAM needs by 80% or more.

9. This means semiconductor valuations are substantially overinflated and will go through the traditional glut versus shortage cycle.

10. For foundation model providers: lower costs with competitive differentiation is good. However, lower costs with a lack of differentiation would mean lower revenues. This makes it harder to (a) service commitments and (b) pay back investors.

11. Leverage is substantially higher than in previous cycles, evidenced by leveraged ETFs, call option activity and margin loans. Korea is particularly susceptible.

12. 0DTE options create a profile that has stronger parallels to portfolio insurance and 1987 than any other point I can remember.

13. The combination of exponential increases in call activity coupled with the ties of semiconductors to structured products means there is a non-trivial systemic risk to the financial system.

14. Implied earnings growth rates are inconsistent with other periods in history.

15. Macroeconomically we cannot and should not fund exponential cost increases. History has shown us repeatedly that there are better ways (see Quick Sort and Simplex).

16. Significant supply is hitting the market via IPOs.

––

Taken together: costs and competition are increasing while revenue growth is likely slowing. Valuations are fragile and prone to technology disruptions that are already here. Systemic financial market risk is extremely high.

61

235

1,720

551,246

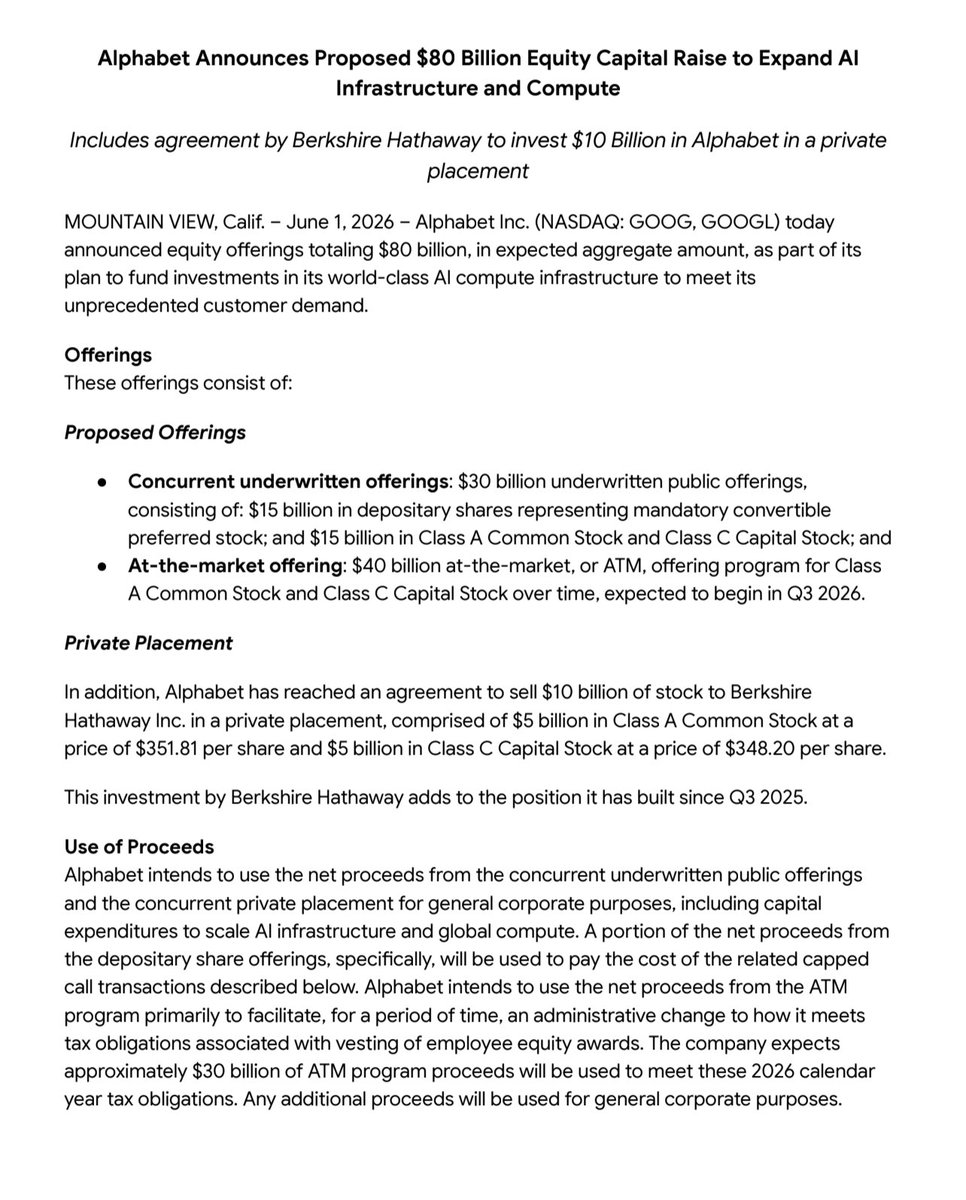

Buffett didn’t do anything, actually!

Jun 1

Alphabet is raising 80B to buy compute “to meet unprecedented customer demand”

Berkshire put in 10B of it

Read that again

The most patient capital on earth just underwrote a GPU bet

Jensen says compute equals revenue

Buffett just priced the collateral

$GOOGL $BRK.A $NVDA

1

1

506

Mar 20

The longer the war drags the more amplified the ripple effects will become

Oil production doesn’t turn back on overnight and the US is now stuck in a strategic rock and hard place. I am becoming moderately more bearish and that feeling is increasing at a rapid rate as this drags

132

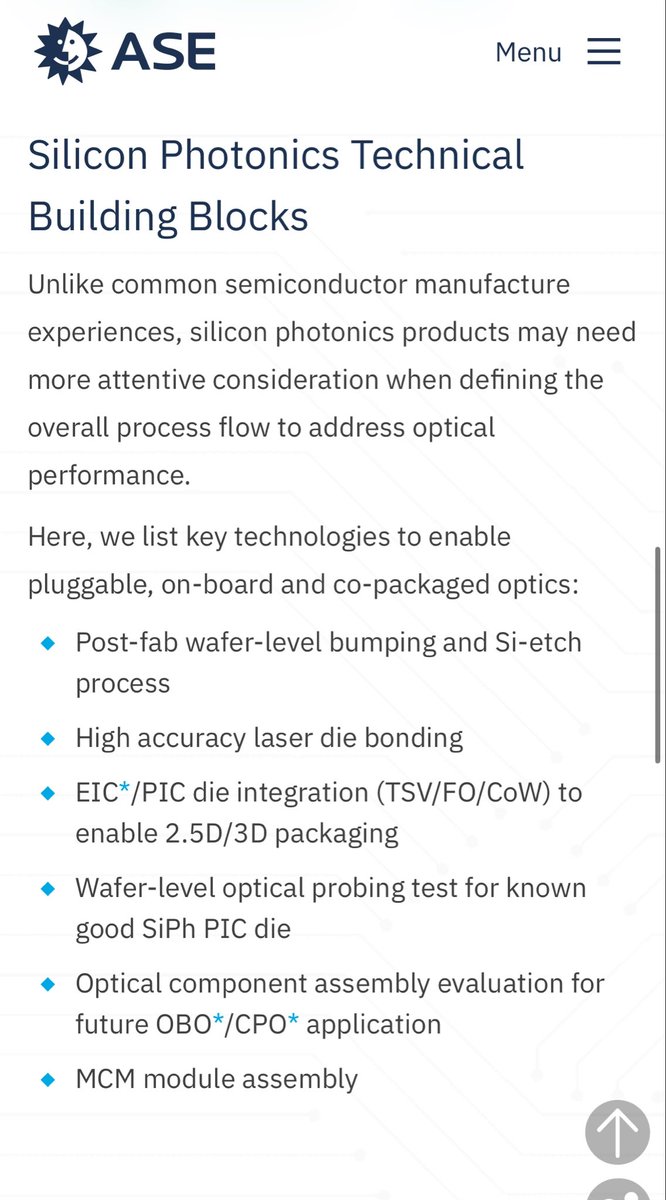

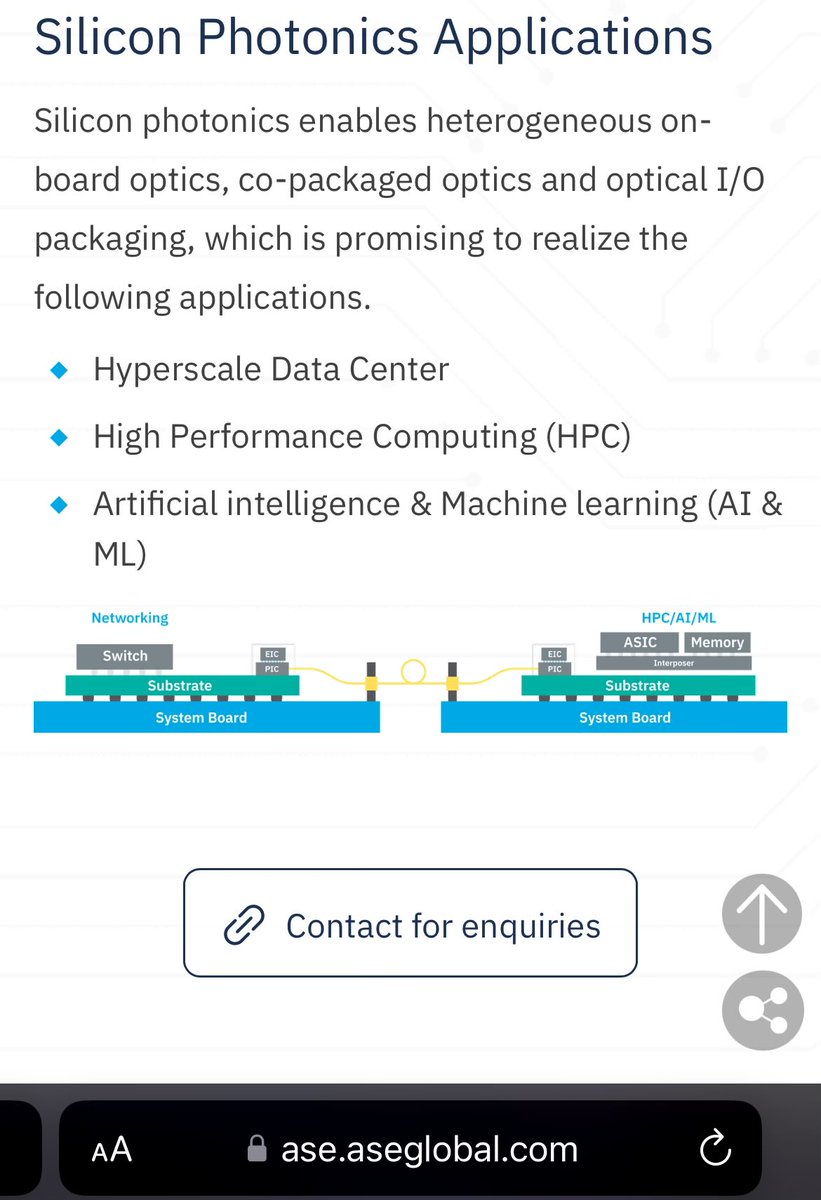

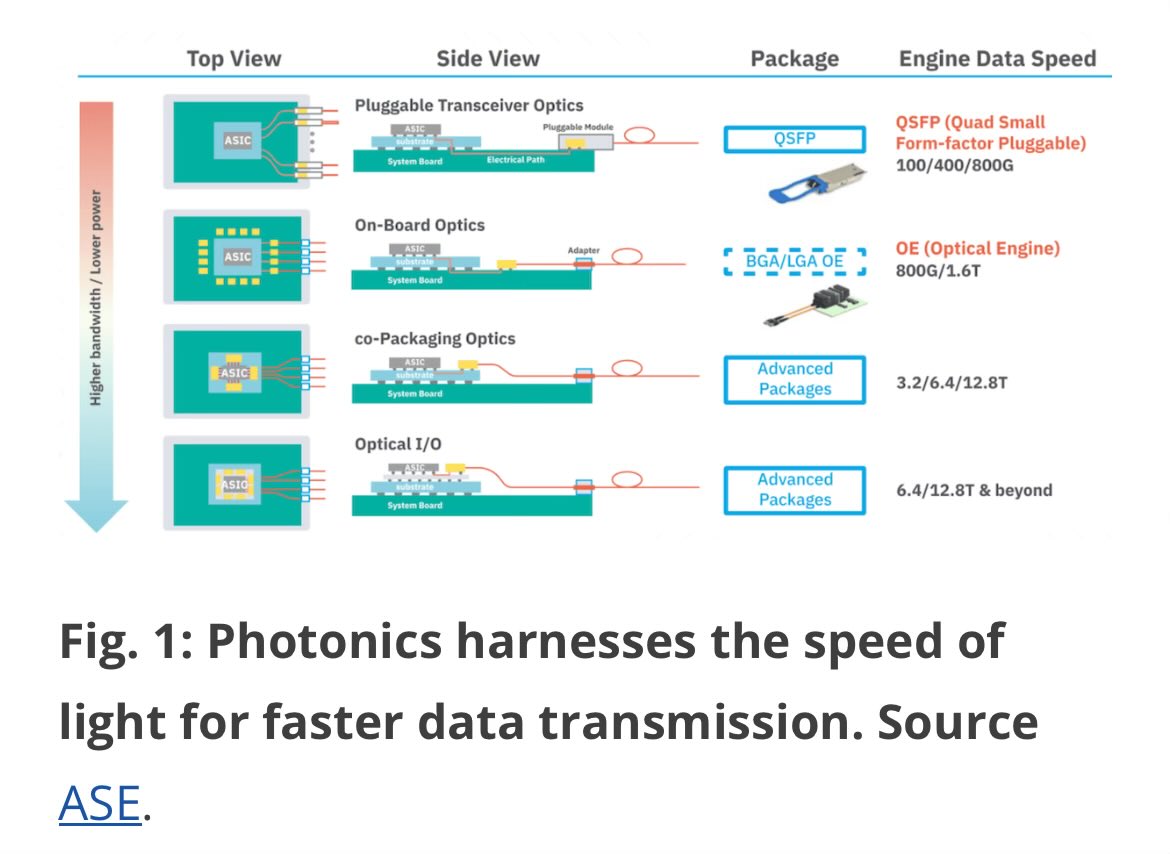

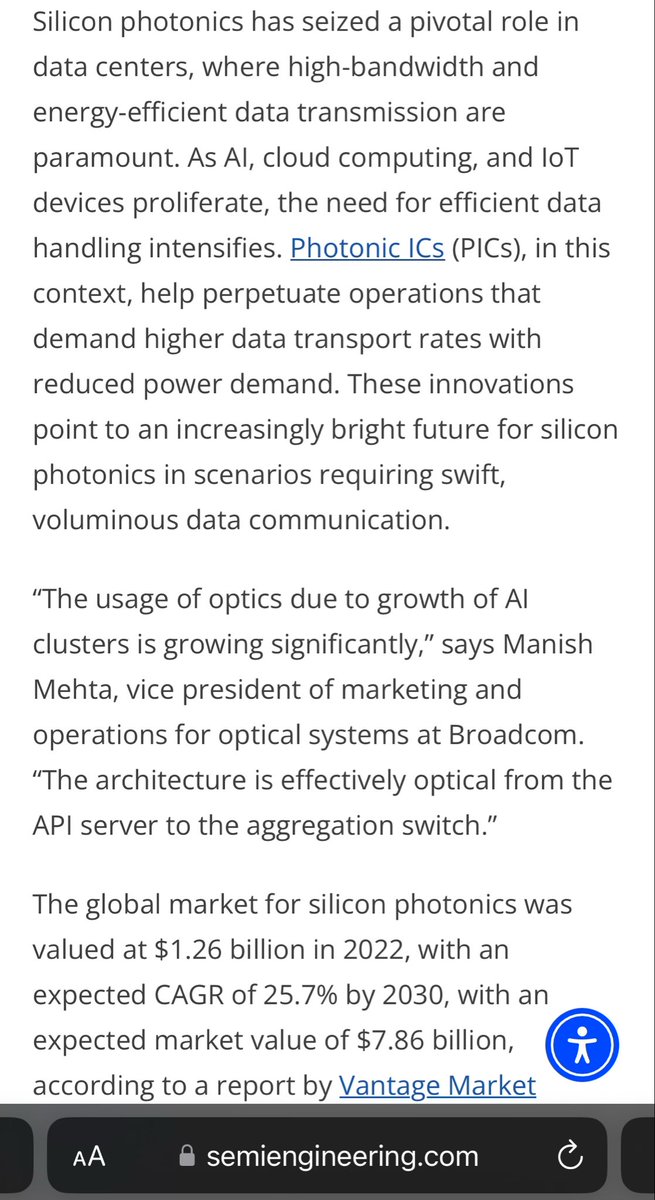

I was really early but really not wrong on the silicon photonics opportunity

28 Mar 2024

Silicon Photonics - some basics…

Notes -

- “Wafer-level optical probing test for known good SiPh PIC die” — this is where $AEHR comes in w/ wafer level prober

(SiPh = silicon photonics, PIC = photonics integrated circuit)

- MCM stands for “multi-chip module”, SiPh leans us deeper into chiplets

- will likely require curvilinear masks in manufacturing. Toshiba $tosbf recently acquired NuFlare, a leader in curvilinear masks

- advantest, $ateyy, supplies metrology equipment that would be important for these masks as well

- manufacturing silicon photonics at scale remains a challenge because it’s extremely complex

- thermal management is important because temperature changes can impact optical signal quality, chip cooling becomes more important, perhaps benefits $VRT?

- Some research estimates the cost of packaging, assembly, and test for photonics devices is as much as 80% of the total module cost. This is in stark contrast to traditional silicon chips today where packaging is a minor cost relative to the overall chip

- “Apart from data centers, silicon photonics is trailblazing developments in other areas, such as lidar in automobiles, which along with cameras and radar is considered essential for object detection. It also is revolutionizing optical projection technology for advanced imaging systems, augmented reality (AR) displays…

But despite significant advancements and potential market opportunities, existing manufacturing processes are limiting the scalability and mass production of silicon photonics components. Manufacturing is often manual and labor-intensive due to the intricacy and precision required in fabricating optical components.”

303

Feb 17

Few

On paper, selling something at $200 after buying it at $7 looks like a brilliant masterpiece. It feels like you nailed it, the screenshots look legendary and the percentage gain sounds absurd. But almost nobody does or often times even considers the real math. I see this mistake made over and over again.

If you bought at $7 and sold at $200, your gain is $193. After 30% long term capital gains taxes, that’s about $58 gone immediately. Now you don’t have $200 per share to redeploy, you have about $142.

If the stock drops to $131 and you buy it back, you’re not capturing a 35% decline. You’re turning $142 into $131. That gives you roughly 8% more shares than before.

After all these brilliant looking trades on paper and trying to time the markets you’re getting ONLY 8% MORE!

That’s the real edge after a “perfect” sell and a 35% pullback. This is what most investors miss. They calculate price returns, not capital returns. Once you sell, Uncle Sam immediately becomes your largest partner and gets his cut. To overcome him, you need a very big reset, not just a 30% dip because such a pullback doesn’t justify the big tax bill you paid.

The uncomfortable truth is that trading around great winners is much harder than it looks. Every time you sell, you shrink the base that compounds for you. Unless the valuation was insane or the fundamentals broke, you’re often just interrupting your own long term math.

My point is not to ridicule this person. I do not know him, and for all I know he lives in a low tax jurisdiction where the math is different. The point is simply that most people do not know how to calculate their real returns, and the gap between paper profits and actual wealth creation is often much larger than you think.

🌹

425

The great amorality of markets

Great post fwiw

Jan 3

US has now invaded Venezuela.

Everyone is probably wondering the same thing:

How do you profit off the situation?

1. Heavy Sour, Ammonia, and Nitrogen Fertilizers disruption ( $CF , $CVE).

These are Venezuela's biggest exports.

Most people will buy generic oil ETFs or light sweet crude producers. This is inefficient because light oil is not a perfect substitute for heavy oil in complex refineries. If Caribbean ammonia is stranded, the global price of nitrogen spikes. The biggest beneficiary is a US-domestic producer that uses cheap US natural gas and doesn't rely on Caribbean shipping lanes

2. Dirty Crude Processing ( $VLO ) - If competitors are starved of Venezuelan oil, Valero’s ability to source heavy crude from diverse locations (and its leverage to diesel margins) makes it resilient.

3. Naval Warfare ( $LDOS) - While retail investors buy Lockheed Martin (F-35s), the operations in the Caribbean focuses on maritime surveillance, warfare, and autonomous patrolling to enforce blockades without risking US personnel. Companies like Leidos provide these tpyes of naval tech.

4. Defense and aerospace from $AVAV to $HII and $LHX also benefit.

- $AVAV recently unveiled the Red Dragon and updated Switchblade 600 variants specifically for maritime operations

- $LHX provides the sensors and communications gear that link the drones ($AVAV) to the ships ($HII) and the jets ($BA).

- A blockade requires significant maritime surveillance and naval assets, which benefits shipbuilders ( $HII )

5. Direct Suppliers of recent military operation:

- F/A-18E/F Super Hornet from $BA (Precision strikes on Caracas)

- B-1B Lancer from $BA

- UAS (Drone), MQ-9 Reaper - $RTX (MTS-B Sensors), $HON Honeywell for the Engine

- Tomahawk (TLAM), $RTX

So far:

$AVAV - 5.91%

$BA - 4.91%

$LHX - 3.72%

$CF - 3.61%

$CVE - 3.61%

$HII - 2.85%

$RTX - 2.1%

$VLO - 1.55%

$LDOS - 1.7%

$HON - .4%

1

2

370

20 Dec 2025

He also doesn’t understand how math works apparently

And this guy has a following?

Inordinate amounts of wealth to be destroyed my this type of content

Literally just buy bitcoin and chill. Stop trying to amplify returns with synthetic structures. You will go broke

20 Dec 2025

21 million total supply.

8 billion people.

That's 0.002625 BTC per person maximum.

Your financial advisor: 'Put 5% in Bitcoin'

Math: That's literally impossible for everyone lmao

2

339

20 Dec 2025

Friendly reminder banking has existed basically since the birth of farming and widespread settlement

Through both hard and soft money regimes

Neither blockchain nor Bitcoin destroy banking, they just disrupt & revolutionize it

But banking IS NOT hoarding hard money & creating synthetic yield atop that horde

$MSTR is decidedly not a bitcoin bank & saylor branding it as such is folly & a misunderstanding of millennia of financial history

145

20 Dec 2025

This is so beyond retarded that I almost think he’s joking but he is indeed serious

MSTR has far higher likelihood to implode & cause the next major Bitcoin bear market than it has of returning 20x in 10 years

Bitcoin itself will yield far better returns than MSTR commons

19 Dec 2025

MSTR Stock Price Modeling: 10 Years Out

MSTR seems like an amazing entry here and the amplification outweighs the premium you're paying.

Current BTC price: $87,829

BTC CAGR: 30%

Time horizon: 10 years

MSTR amplification: 27%

Current MSTR price: $165.27

1. Bitcoin price in 10 years

30% CAGR over 10 years:

Growth multiple: 1.30¹⁰ ≈ 13.79

Future BTC price: $87,829 × 13.79 ≈ $1.21 million

2. Amplified Bitcoin exposure (MSTR)

27% amplification means MSTR compounds at:

BTC return × 1.27

So effective growth multiple:

13.79 × 1.27 ≈ 17.5×

3. Implied MSTR stock price

Apply the amplified multiple to today’s price:

$165.27 × 17.5 ≈ $2,890 per share of MSTR

✅ Final Answer

Bitcoin (10Y): ~$1.21M

MSTR multiple: ~17.5×

Implied MSTR price: ~$2,900 per share

This assumes:

No multiple expansion

No contraction, stays at 1.1x

They maintain 27% amplification

Pure Bitcoin CAGR structural amplification only

But.... remember MSTR has a BTC Yield this year of 24.9% this year.

What if we model in a conservative 10% BTC Yield per year AND an mNAV rerating to 1.5x?

Bitcoin per share exposure increases 10% per year, compounding:

BTC/share multiple: 1.1010≈2.59×1.10^{10} ≈ 2.59×1.1010 ≈ 2.59×

This is independent of BTC price appreciation. It stacks on top.

mNAV re-rating from 1.11 → 1.50...

Total MSTR multiple:

Now multiply all three effects:

13.79×2.59×1.35≈48.2×13.79 \times 2.59 \times 1.35 ≈ 48.2×13.79×2.59×1.35 ...

≈ 48.2×

Apply that multiple to today’s price:

Implied MSTR price: ~$8,000 per share

BULLISH MSTR.

8

4

6,602

18 Dec 2025

Probably a good call to buy $BTC dips when they emerge here because volatility goes both ways

107

15 Dec 2025

yes. Banking and trading should be moved fully to the blockchain within 10 years

Banking itself is undergoing two foundational shifts - 1) AI disruption, 2) blockchain disruption

Note that bitcoin itself doesn’t disrupt banking but blockchain technology. Banks have existed in some capacity since the dawn of civilization when currency was first created. Through millennia of hard money and soft money regimes. Banking is currency agnostic - Bitcoiners that tell you otherwise are coping

10 Dec 2025

SEC CHAIR Paul Atkins U.S. markets could move on-chain "within a couple years"

Bro just said the quiet part loud

$68T equity market

$35.8B currently tokenized

Nasdaq filing for blockchain trading

We're so fucking early it's insane

209

13 Dec 2025

Geminiii has completely replaced ChatGPT on my day to day

144

10 Dec 2025

Mr financelot doesn’t know about step up in basis (actual tax avoidance strategy for heirs) just wants clicks

Also a $6.25b donation that benefits the donor is still a $6.25b donation. Not really a scam!

9 Dec 2025

What a scam this is..

Michael Dell gets to write off 74% of his $6.25B "donation" right away because it's a fed gov program for public purposes

It shrinks his estate, avoiding 40% tax on his heirs while maintaining family control

The investment accounts are funneled into $DELL

1

227

29 Nov 2025

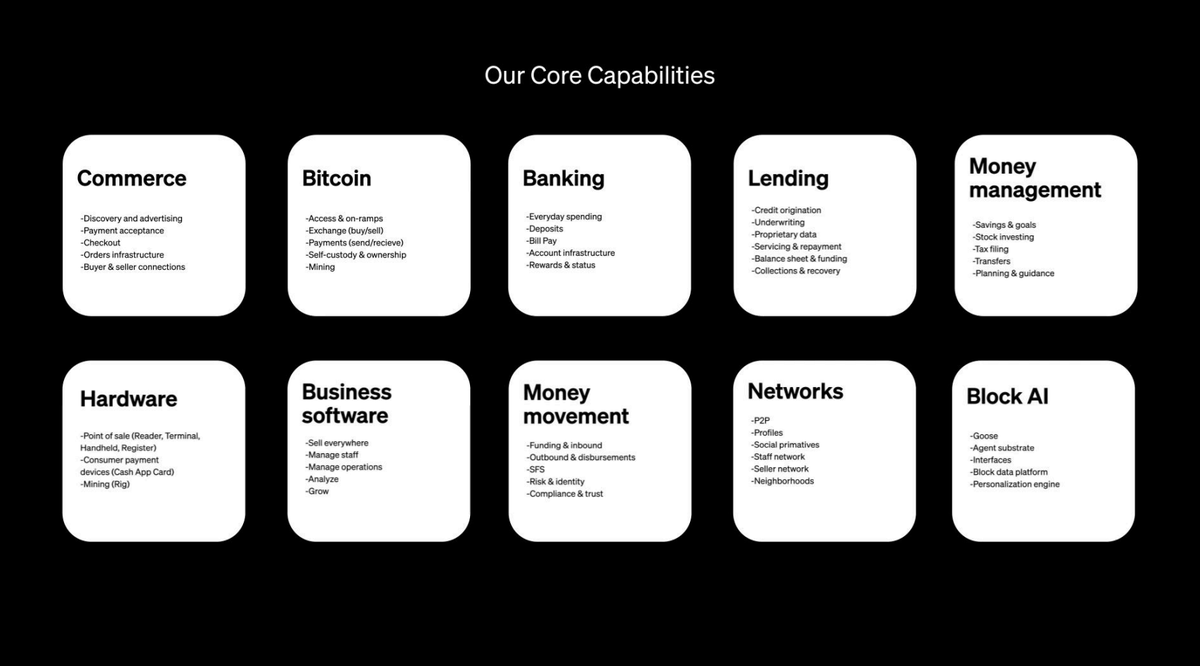

I would be interested to learn how $XYZ manages cash app marketing / user engagement metrics internally

It seems the only marketing strategy is to give money away. And that’s neither good nor bad. It’s just a strategy.

But the goal for cash app should be converting its nearly 60m users to *fully engaged* users. What does that mean? It can mean several things. For cash app, this would probably be a combination of one or several of the following:

- Cash app card active user (5 transaction monthly)

- Afterpay active user ($100 spent per month)

- investing active (holds a non-zero $BTC or stock balance)

- cash app borrow active user (borrowed money in past month)

- direct deposit user

You’ll note that none of these are about P2P payments, cash apps perceived “purpose”

P2P is the top of funnel acquisition engine. Deepening user relationships requires peeling back a few layers, monitoring engagement metrics, and rewarding highly engaged users as they have the highest revenue multiple.

Cash app has a breadth of products/services that is unmatched - now just time to join the big leagues by incentivizing users to rely on cash app as their *primary* financial institution

1

6

1,523

21 Nov 2025

Complete nonsense argument

If they began liquidating bitcoin to cover dividends, bitcoin price would fall, requiring more liquidation, further price falls, more liquidation….

Understand cycles, both virtuous and vicious

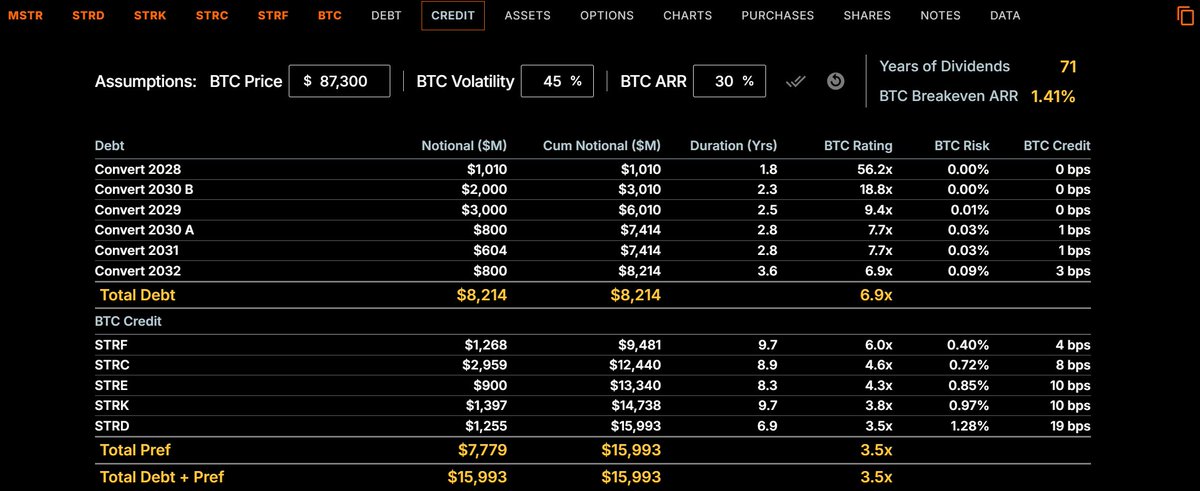

At current $BTC levels, we have 71 years of dividend coverage assuming the price stays flat. And any $BTC appreciation beyond 1.41% a year fully offsets our annual dividend obligations.

321

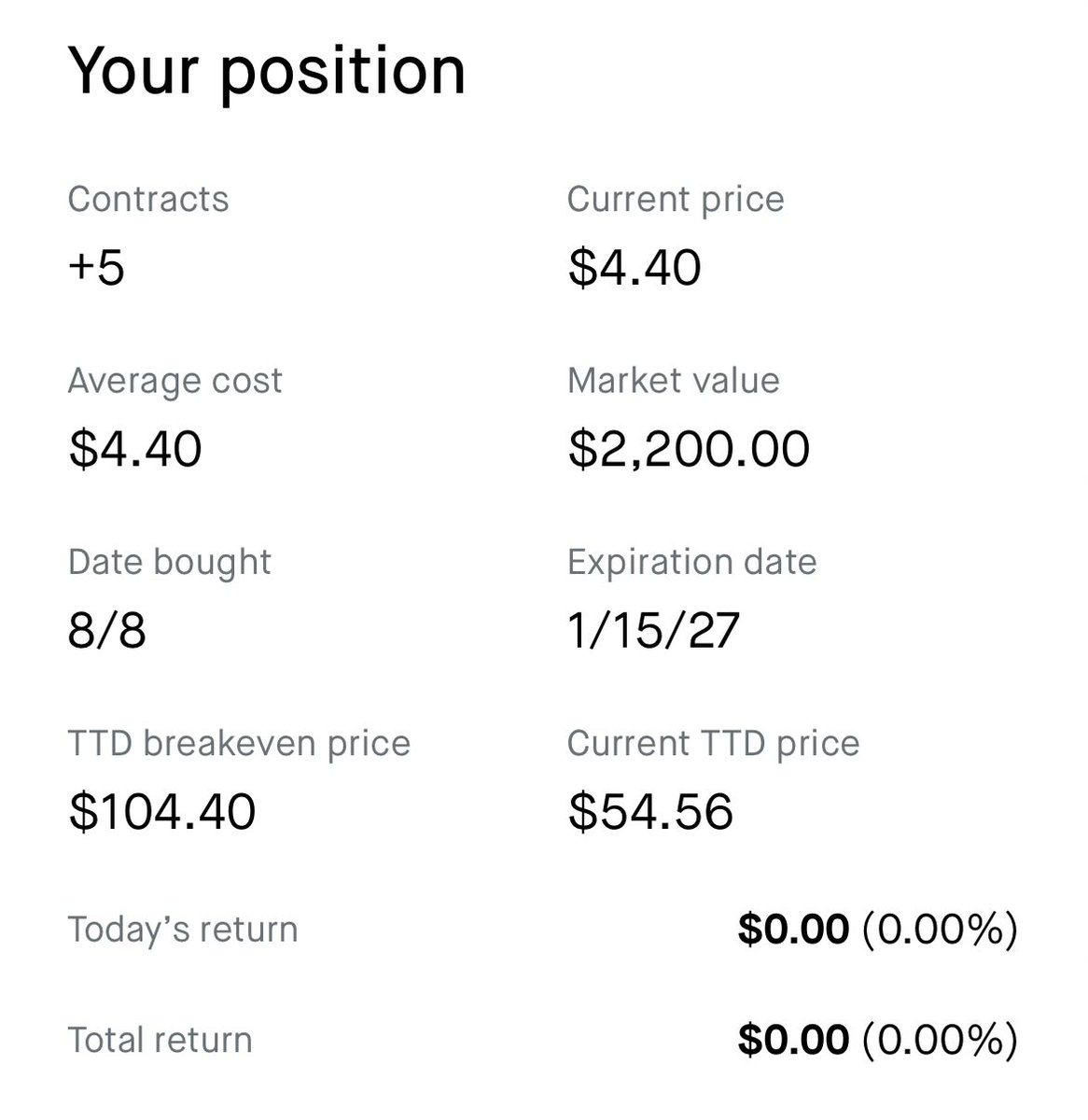

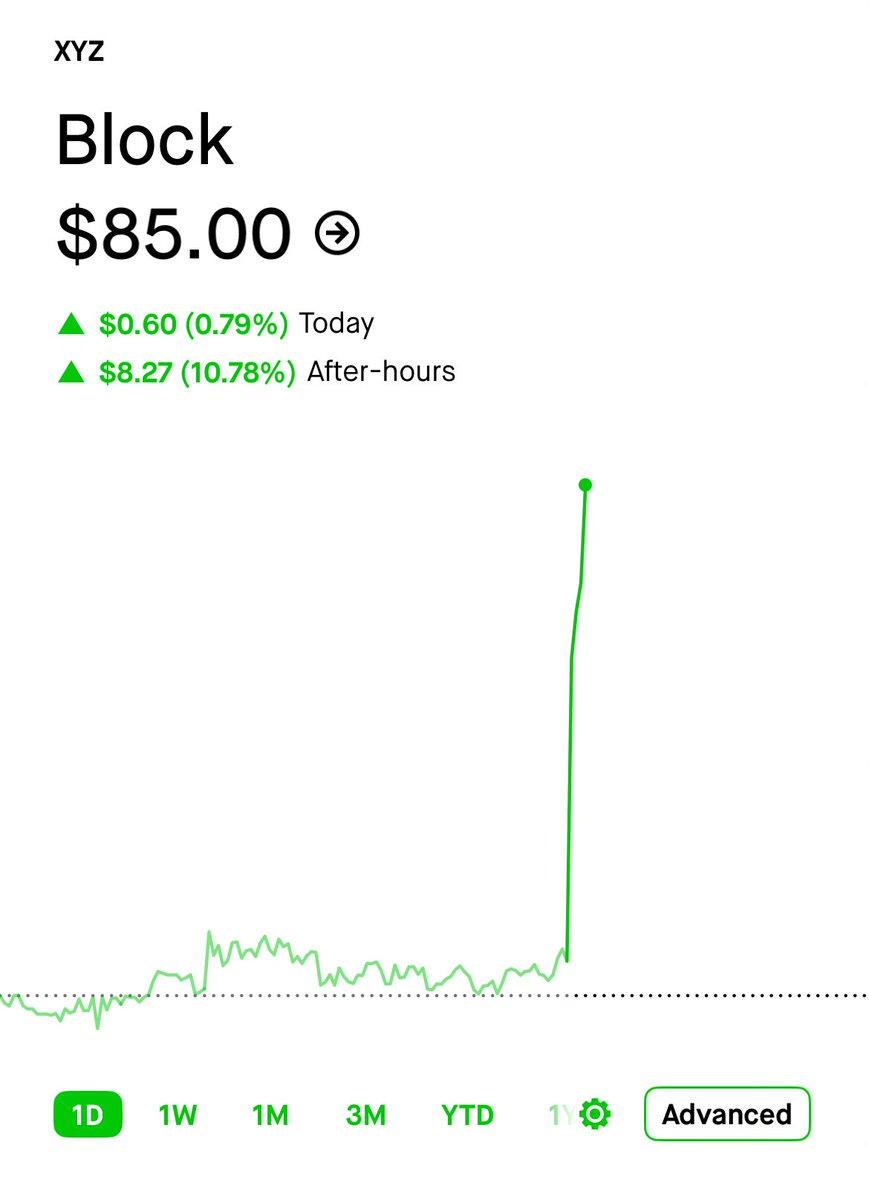

20 Nov 2025

If you’re looking to short $XYZ stock I have plenty of shares I’ll happily lend to you

20 Nov 2025

yesterday was great!

we're going to:

• build the smartest app for small businesses

• build the smartest app for consumers to run their financial life

• connect neighborhoods globally through both apps

• remove dependencies & single points of failure with bitcoin

... only we have the capabilities to do this

1

10

1,996

19 Nov 2025

Cash app score - look it up - it’s only a pilot for now but revolutionary product to break from the chains of standard credit agencies

Block is breaking the traditional personal finance paradigm before our eyes and Wall Street just ignores it and sells the stock on ST #’s

$xyz

1

6

951

19 Nov 2025

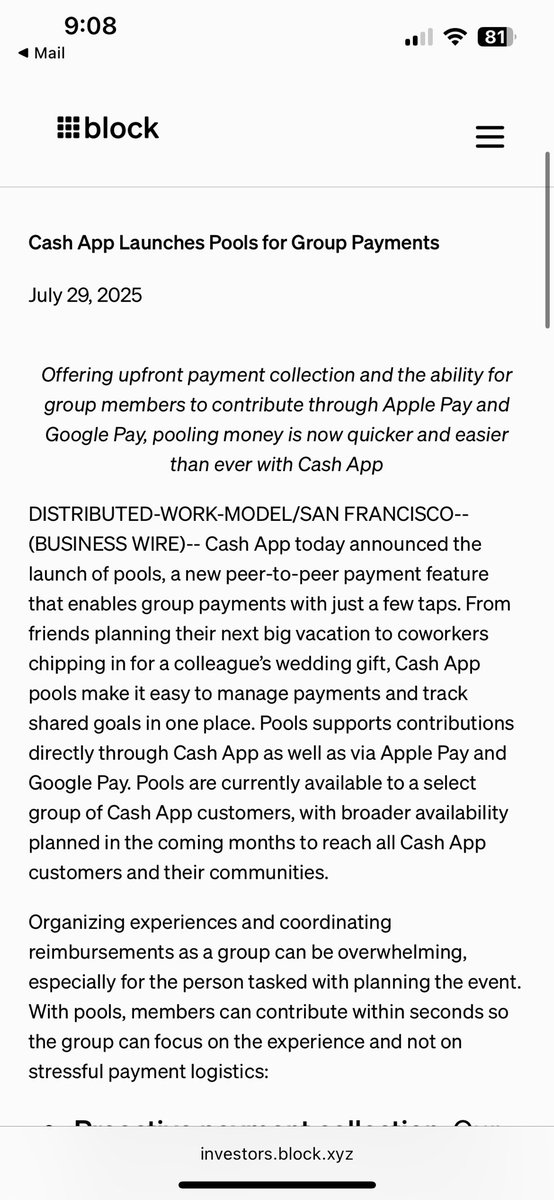

$xyz $5b increase to buyback. Quite a nice gift for LT holders. Will get ‘26 and 3 year outlook tomorrow

9

753

17 Nov 2025

Hahahaha that’s not what convexity is

16 Nov 2025

Why I like buying MSTR over IBIT:

IBIT = 1:1 Bitcoin exposure.

MSTR = 1:1 Bitcoin exposure PLUS consistent growth in Bitcoin per share.

BTC grows at whatever CAGR the market gives you.

MSTR grows BTC holdings per share on top of that.

That’s convexity.

That’s leverage without liquidation.

That’s why I buy MSTR over IBIT.

In a world where exposure is free, I want the asset that increases my exposure every year.

30% BTC CAGR and 10% BTC Yield gets you 2.58x outperformance over a decade.

$100k into IBIT: $1,378,600 after 10 years

$100k into MSTR: $3,560,000 after 10 years

I'll take a 35.6x over a 13.8x.

158% outperformance.

1

322

14 Nov 2025

So $MSTR is facing its first real selling pressure and his decision is to post an image of him abandoning the ship and escaping by himself in a life raft?

🤣🤣🤣🤣🤣

3

449