1,130 Photos and videos

RT @jaebersole1: Doing tokenized stocks right takes time. Rushing leads to delivery failures.

@SoloTex_com Stock Tokens — coming shortly v…

68

FutureDigitalAsset retweeted

Jun 12

This week in markets 📊

• SpaceX IPO blasted off and is trading at a ~$2.2T valuation

• On-chain RWAs crossed $32B, up 200% year-over-year

• S&P 500, Dow, and Nasdaq all bouncing back into the green

• Hyperscaler capex is acting as a macro stimulus for global equities

Here's what moved ↓

14

20

88

4,083

6

2

16

1,454

Jun 10

RT @iamartikyoul8: tx:native Tokenize X is the gold standard for RWA tokenization. 🏆 @txEcosystem @txRWAs

7

FutureDigitalAsset retweeted

Jun 10

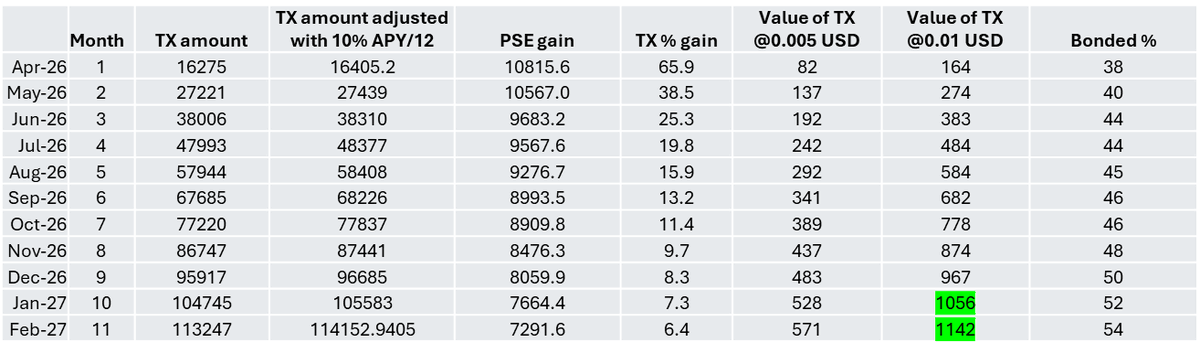

And let's take that math a step further. If tx:native hits my 2.618 Fib extension target of $0.11, that exact same staked portfolio doesn't just break even—it balloons to over $10,000. That turns a stressful 91% drawdown into a massive 10x return on the initial $1,000 investment. This is why you don't play dead in a dynamic market; you stake, compound, and let the math work for you.

1

3

16

746

FutureDigitalAsset retweeted

Jun 10

Anyone who understands basic math knows that recovering from a 91% drawdown requires an 11.1x (1,110%) pump if your token balance stays exactly the same.

But that is exactly where the critic’s logic fails: they are calculating recovery math for a dead, static portfolio.

When I say we will most likely break even on tx:native through PSE, I am not crossing my fingers hoping for an 11x miracle pump—even though the Fibonacci extension targets comfortably sit at $0.10 to $0.17. I am looking at the power of compounding mechanics.

Let’s use the exact example provided by @808cryptobeast:A $1,000 investment split evenly between SOLO and COREUM at the pre-merger snapshot converted into roughly 16,275 TX. At today’s price of ~$0.0055, that static balance looks grim at $89.50.

However, the math completely changes if you have been fully staked from day one.

Because early network participation is lower, initial PSE gains are disproportionately massive. If you are compounding those rewards, your token count isn’t sitting still—it is aggressively multiplying.

Look at the staking models: with a fully staked position, you don't need tx:native to hit $0.0615 (or 11X) to see your $1,000 back. By January 2027, a fully staked holder can achieve a total portfolio break-even at a mere $0.01 per TX (~2X).

That is only a ~100% price increase from here—a minor move that doesn't even require reaching the basic 0.236 Fibonacci retracement level.

Many have been at a loss from this same team for multiple cycles, including this one with TX.

Using a simple $1,000 example, if someone held a portfolio that was split evenly between SOLO and COREUM at the pre-merger snapshot, they would have received roughly 16,275 TX after the conversion. At today’s price of around $0.0055 per TX, that position would be worth approximately $89.50.

That represents a loss of about 91% from the original $1,000 investment, which aligns with what many participants have experienced.

This is where understanding recovery math becomes important. A 91% drawdown is not recovered by a 91% gain. To get back to the original $1,000 value without considering additional emissions or rewards, TX would need to rise to roughly $0.0615 per token, an increase of more than 11 times from current levels.

Some often point to PSE as a way to accelerate recovery. While PSE can increase an individual’s token count through staking and compounding, it does not eliminate the need for significant price appreciation. The emissions are distributed across the network over seven years and are shared among participants, meaning everyone is competing for a portion of the same allocation.

Even under optimistic early-stage scenarios where staking rewards substantially increase a holder’s TX balance, the investment would still require meaningful price appreciation to fully recover losses. A larger token balance helps, but the primary driver of recovery remains the market value of the token itself.

This is why it is important to separate token accumulation from actual portfolio recovery. Receiving more tokens can feel encouraging, but unless the market places a higher value on those tokens, the loss remains largely unchanged.

The math is straightforward. after a 91% decline, recovery requires both substantial appreciation and sustained demand. Emissions alone do not change that reality. And this is just an example some have been in more of a loss with even adding more money trying to recouped better positions.

3

12

44

2,611

FutureDigitalAsset retweeted

Jun 10

$TX, RWAs, and AMA Latenight Livestream x.com/i/broadcasts/1AKEmmbBY…

3

15

346

Jun 10

RT @smartmemetoken: @txEcosystem’s strategic partner @krakenfx named official exchange supporter for the FIFA World Cup 2026!

Imagine own…

6

RT @iamartikyoul8: tx:native is now #9 amongst RWA protocols! Track now at smartmemetoken.com/rwamart

@smartmemetoken @rwamart @coingecko ht…

9

RT @smartmemetoken: It’s RWA o’clock 🚀🚀🚀🚀🚀

@txRWAs are coming soon, all markets, all assets on tx:native ! Be $MART 🤓 Own your world. htt…

7

RT @iamartikyoul8: ICYMI : @texture_capital runs a validator node on only 2 chains right now, tx:native & canton-network:native .

@txEco…

9

FutureDigitalAsset retweeted

Jun 7

1

6

235

FutureDigitalAsset retweeted

Jun 6

3

5

19

441

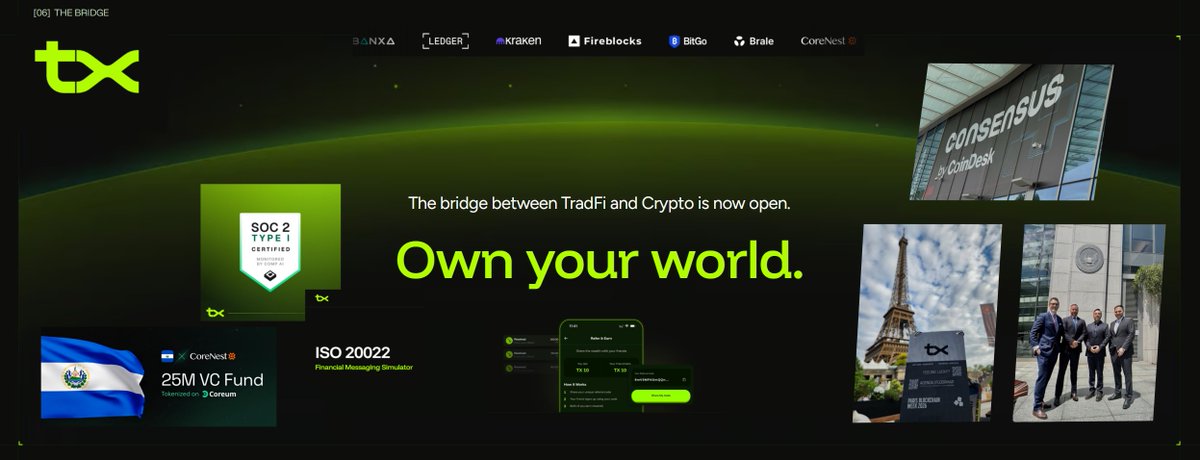

RT @jaebersole1: Further demonstration of the #txecosystem team’s commitment to providing the safest institutional-grade rails for complian…

51

FutureDigitalAsset retweeted

Jun 6

Fear is volatile but the ascent never stops, and the ones who climb through it define the structure, whether they build the rails or secure the network. Congratulation to all, happy PSE Day ! tx:native

2

4

42

1,157

FutureDigitalAsset retweeted

Jun 6

Say hello to the newest, fastest TX Wallet.

wallet.txdex.live

Add as a PWA. Chome extension coming soon

9

20

87

2,718

RT @iamartikyoul8: Today the Operating System for RWA tokenization got SOC 2 compliance, RWA SZN is here. tx:native

6