I help grow your long-term portfolio | Elite Popular Investor on eToro🏆 outperforming BTC, ETH, NASDAQ, and the VisionTrack crypto hedge fund indices 👇🏽

Joined February 2018

- Tweets 2,707

- Following 495

- Followers 2,403

- Likes 2,556

831 Photos and videos

Filip Brnadic retweeted

Jun 11

*IRAN AGREES TO OPEN STRAIT OF HORMUZ IN RETURN FOR SPACEX IPO ALLOCATION

378

544

10,383

1,213,709

Jun 11

100% - and the WSJ valuation graphic tells a thousand words

x.com/i/status/2061403725634…

2

440

Jun 11

Always a great convo talking markets with @AlexSaundersAU and @DaxxTrader 💪🏼

Crypto Market Update June 2026 - Bottoming

👉 youtu.be/t9jFzmY_EU8

2

6

1,005

Jun 8

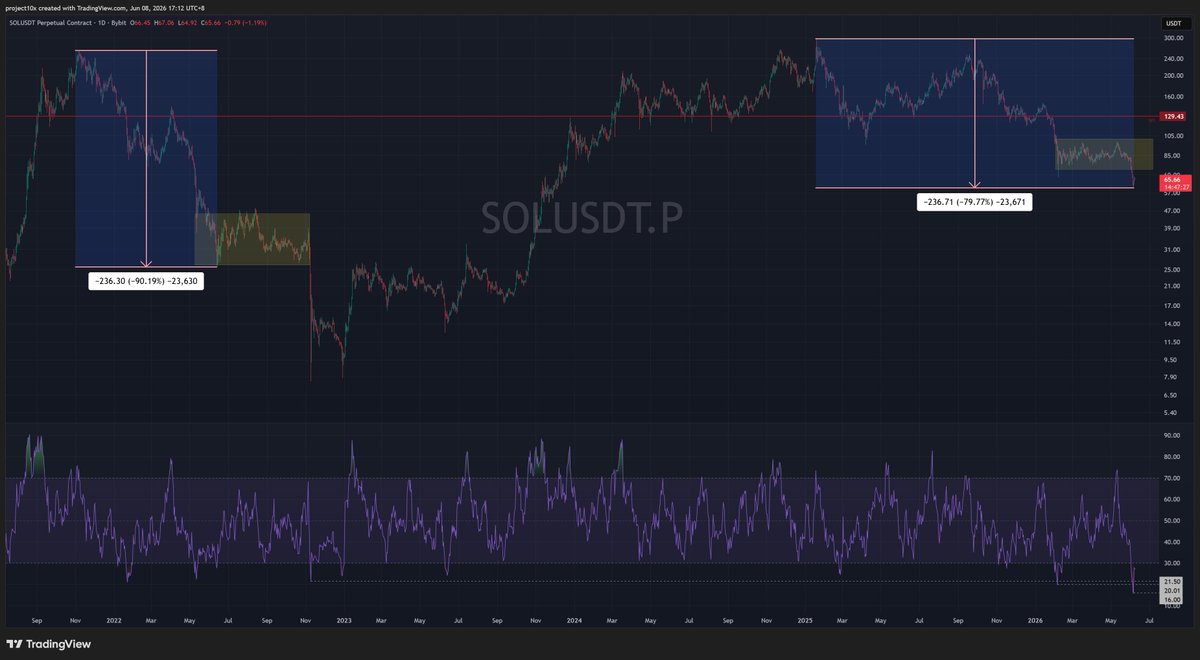

I'm sure in the depths of a bear market many folks will disagree, but these prices (using SOL as an example) are going to look great on the HTF.

➡️ SOL had the lowest D1 RSI on record

➡️ median HTF (6mo) return is 53%

If your thesis RE: crypto is not invalidated, these are fantastic HTF entries, regardless of other data, macro, etc.

1

1

6

181

Jun 4

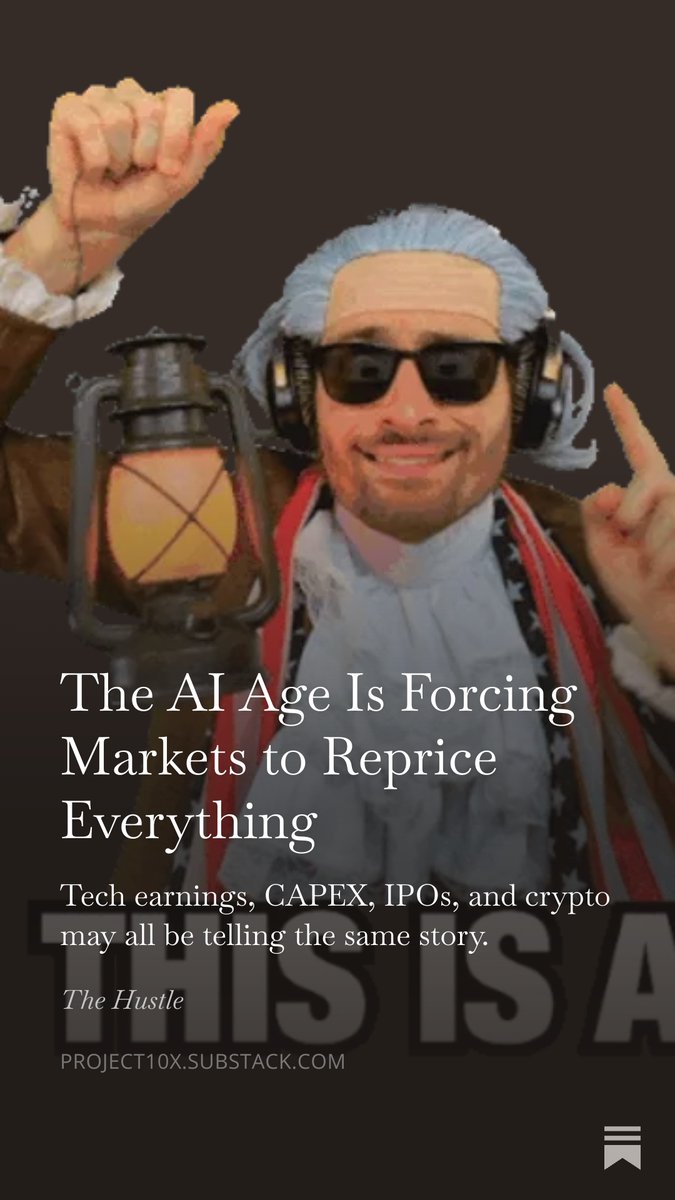

More and more signs of AI bottlenecks and second-order effects are starting to emerge.

This could result in a pullback in weeks/months.

Scam Altman noted that AI budgeting has become a "huge issue" for some companies.

If we extrapolate:

➡️ less AI spending means lower demand for compute.

➡️ lower demand for compute means slower revenue growth for hyperscalers that sell compute.

➡️ slower revenue growth can eventually lead to lower infrastructure spend.

➡️ that flows through to the companies supplying the AI buildout, particularly the small and mid-cap names that have been rallying on hyperscaler demand.

➡️ Ultimately, it could result in NVIDIA and other GPU/TPU/memory providers delivering earnings below expectations.

Remember, NVIDIA is not just another stock at this point. It is one of the key pillars holding up the broader AI trade and, by extension, a large part of the market.

TLDR: If AI budgets slow, the entire supply chain gets repriced.

We may get our pullback and buying opportunity discussed in the latest newsletter drop) soon 👇🏽

project10x.substack.com/p/th…

Sam Altman said AI budgeting has recently become a "huge issue" for some companies, something that "never came up" earlier this year. bit.ly/4uxIGnv

1

176

Jun 4

hear hear

Jun 4

#BREAKING MP Kevin Hogan blasts PM

Anthony Albanese in Parliament for destroying Australia's risk reward economic model.

Hogan's critique is razor sharp, the government has systematically inverted incentives for private enterprise.

Historically, risking capital meant keeping the return.

Now, the framework forces a parasitic transfer of wealth “You take the risk and the Albanese Government gets the reward” Hogan argued.

Hogan then rages that this isn't just failed policy, it's a calculated “unforgivable" deception of the Australian electorate.

Hard to argue.

1

121

Jun 4

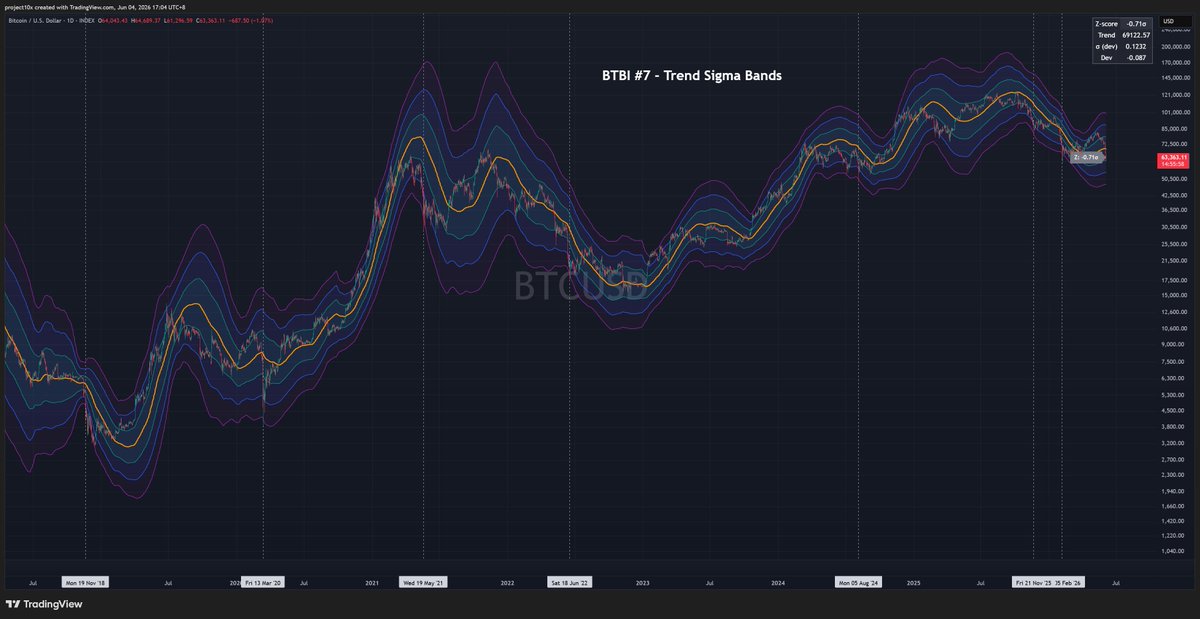

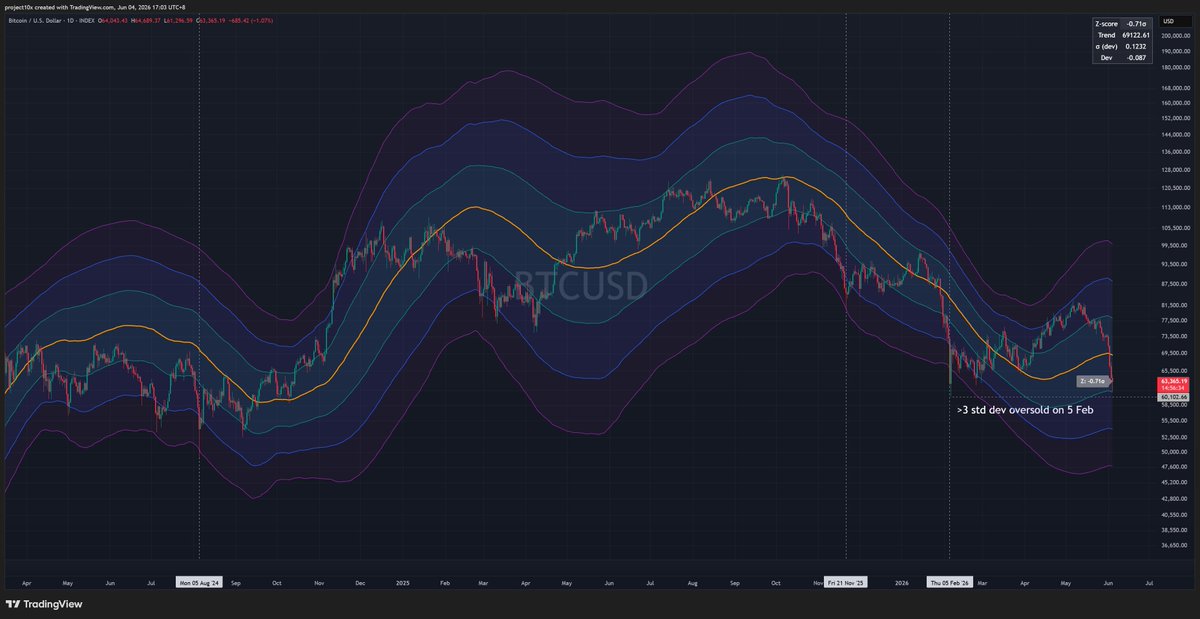

Several months ago, $BTC tagged $60K.

At the time, it was more than 3 standard deviations oversold on the medium-term trend.

Historically, those conditions have been some of the best long-term entry zones for people who actually believe in the asset.

Today, we are back near those same price levels.

2

2

12

959

Jun 4

These are not short-term timing tools. They do not mean price cannot go lower tomorrow, next week, or next month.

But on a HTF basis, if you believe in $BTC, this is the type of zone that has historically rewarded patience.

TLDR - if you believe in $BTC as an asset, this is a great HTF entry.

1

140

Filip Brnadic retweeted

May 30

Well said Simon.

These parasites are taking the piss

58

597

2,777

75,325

Filip Brnadic retweeted

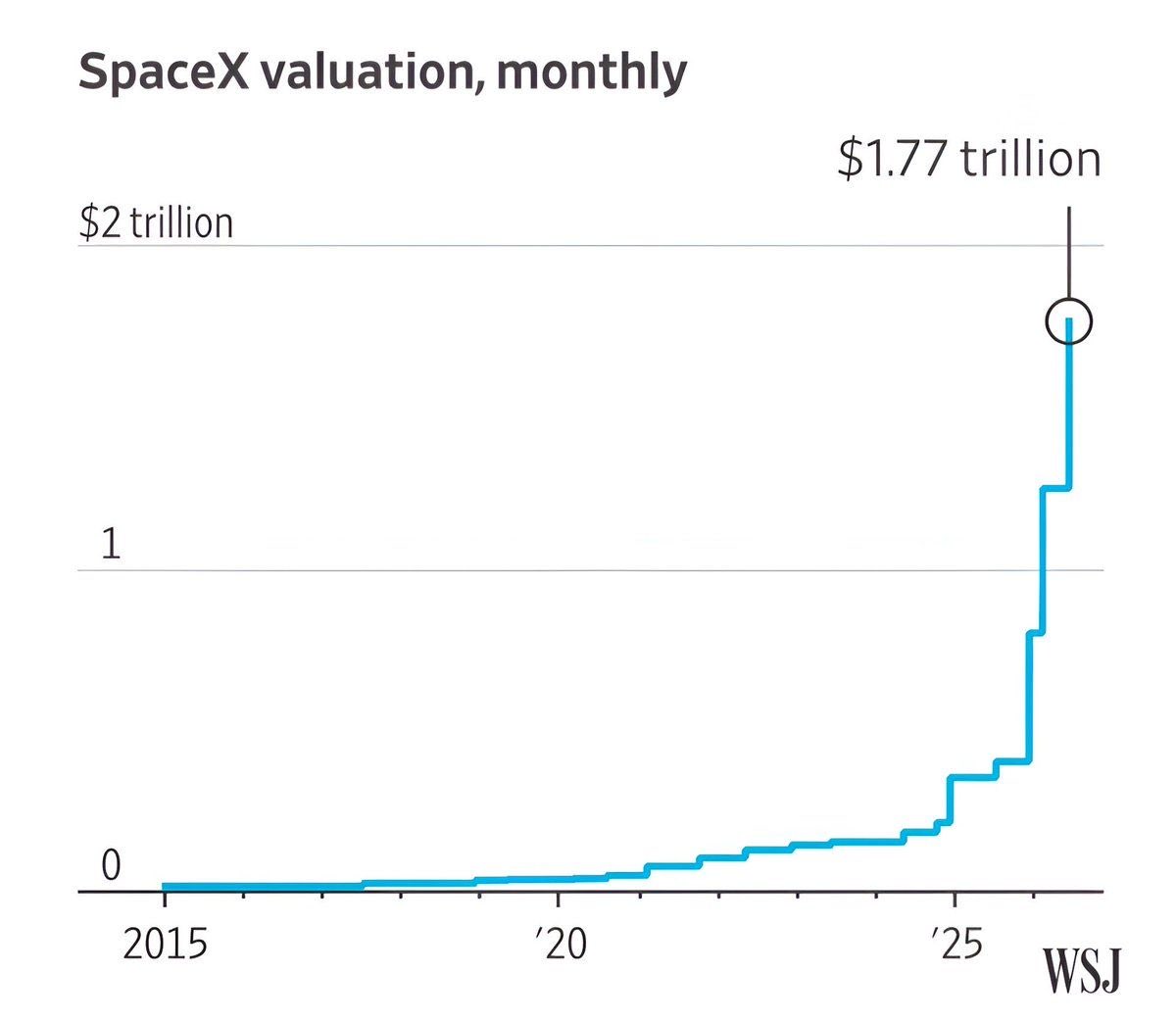

Jun 1

We already have a rough idea of how Space X will trade in terms of revenue multiples given TSLA is public.

➡️ TSLA is still a vehicle, robotaxis, energy, AI, and robotics play commanding a 14-16 rev multiple.

➡️ Space X (no doubt a sexy narrative) is commanding a 94x multiple.

A 50% correction of Space X would put it at 3x the multiple of TSLA..

So, 1) it will not be able to sustain the IPO price and 2) it's way overpriced even for retail to keep a $1.8T valuation afloat 3) if you've made money as an insider/ early employee, you are no doubt going to be taking profits into what is the large IPO in history.

1

1

280

May 28

I will continue to beat this drum. We saw it happen in the UK, and we'll see it happen in AU.

May 27

Shocked - but not surprised - at the number of clients who are planning on moving overseas as a consequence of the budget changes to CGT and trust taxation. I am fielding daily calls from HNW clients. And this isn't an emotional outburst: you call your tax lawyer to plan, not to vent. There is going to be a massive capital outflow from Australia.

1

258

Here is my advice for avoiding 47% CGT on shares.

Step 1 - Take all your money, put it in the bank, and collect 5% interest.

Step 2 - Get a doctor to diagnose you as autistic, and register for the NDIS.

Step 3 - Buy a PlayStation 5, sit on the couch, and punch cones.

157

200

2,925

80,377

May 19

If BTC was still in a broken regime, this is where it should have made new lows.

➡️ War headlines.

➡️ Oil fears.

➡️ Bond-yield fears.

➡️ Inflation fears.

➡️ FED hiking fears.

➡️ ETF-flow weakness.

and yet, BTC did not break...

Even better, it has been trading up against USD, gold, SPX and, until recently, NDX since the war began.

Markets bottom when the same news that used to nuke the market starts getting absorbed.

That is why my thesis is simple.

It is going to be much harder to push BTC below $60k when this much bad news has already failed to do it.

Read more, here 👇🏽

open.substack.com/pub/projec…

1

6

123

May 18

If you want to get ahead in Australia, you can only do so in a vehicle that locks up your money until you're 60 years old minimum.

Dreams of working hard and retiring at 30, 40 or 50?

Too bad. You must remain a cog in the wheel until 60.

May 17

Super is increasingly the only viable investment vehicle in Australia.

Setting aside the potential for losses - what happens if the government says they’re increasing the retirement age because they need you to work longer to pay more tax?

Or what happens when they decide to simply tax your withdrawals in retirement after you’ve been forced to invest it there under current settings for decades?

This isn’t about stomping on super - which has its merits - but to highlight the risks for future generations whose opportunities to invest are increasingly centralised under government control.

4

1

9

907

May 15

To the mid-curvers saying this is not a death tax because the Government didn't label it DEATH TAX in bold...

1. You are the definition of this meme.

2. Testamentary trusts, set up in a will and only taking effect after death have been popular for decades because the discretionary version lets trustees distribute income and capital tax-efficiently to beneficiaries while protecting assets from creditors, divorce etc.

Any new ones created after budget night including assets purchased after that date will now be subject to a 30% minimum tax on income.

Call it what you will, but if you fall into this bucket, talk to your accountant to see if you can amend the will to switch from discretionary to fixed testamentary trusts. Also consider gifting while you're still alive. Both options sidestep this tax.

My 2c✌🏽not financial advice!

May 14

Oh and they have now introduced a death tax too...

1

2

269