Startup Operator with Special Operator Perspective/ Currently Big Tech AI Strategy / Thoughts on company building and the VC game, embracing controlled chaos

Joined June 2022

- Tweets 789

- Following 31

- Followers 324

- Likes 15,769

166 Photos and videos

Pinned Tweet

8 Oct 2025

Great piece on PE becoming a commodity by @PEoperator linked below.

His statements eerily ring true to VCs as well. My limited take.

The commoditization of VC is very similar. The pay, prestige, and lack of required effort are just too attractive, creating an industry whose goal is raising more funds (2% fees), not finding winners (20% returns).

Obviously, there are good VCs, but most add no value, and many add negative value. I’ve been on over 200 pitch calls. Anecdotal, but still a data point, even if biased.

The Pitch: For VCs to raise a fund, they must claim some type of unique differentiator, usually a combination of some expertise and a unique startup network advantage. From my experience, those two values fall far short in reality.

The Reality: From the outside, they (the long-tail) are all the same. The only unique group is the top 1–5% who get the lion’s share of top startups, carrying the industry similar to the S&P 500 and tech stocks.

The Game: Start a fund, have a compelling hook (previous partner or successful founder are go-tos), create a unique selling point for LPs, align with LPs’ charters and mandates (ESG was the quintessential example), disperse the fund into startups that align with the thesis, and then try to raise a second fund before it becomes apparent that the J-curve isn’t coming up. If you have one startup even getting close, that becomes your poster child for the second fundraise. Most VCs can’t get past funds two or three.

The Payout: Why do VCs do this? Simple. The 2% management fee allows for an incredible paycheck and lifestyle while they know the 20% return is incredibly hard to obtain and will be forgiven in the short term. It’s an 8–10 year investment horizon, with losses really only being captured in years 3–5 of a fund. The pressure to hit startup home runs is far lower than the pressure of getting LPs capital for the second and third fund.

The Outliers: This doesn’t apply to all. The kingmakers (Sequoia, a16z, etc.) are unique because they will get first dibs on any successful startup, creating a flywheel of success. They are sought out by the most desirable startups. The signaling of having them in a round is too impactful to pass up. There are some very niche and quality VCs, but even those are far and few between from my experience.

The State of the World: VC land is now oversaturated, with East Coast hedge funds wrapped up in West Coast Patagonia jackets. The perfect example founders all lament is the recent MBA analyst with no real-world experience screening startups and the lack of conviction from VCs to lead a round. They want their own signaling guaranteed by another more prestigious VC. Ultimately, the vast majority are just blindly throwing darts at a dartboard, knowing no active founder wants to bite the hand that feeds.

The Future: Just like in sports, when tactics of a game are solidified universally, unique opportunities arise for those thinking outside the box. It will be interesting to see who brings the West Coast offense and evolves the VC game. My thoughts are that the power is much more in the founders’ hands than the founders know.

VCs need founders. Founders do not need the current state of VCs. Curious to see what the future brings.

8 Oct 2025

The private equity industry has become commoditized.

Folks inside the industry will point out how different one firm is to another.

But from the outside, they are indistinguishable.

Buy a company with debt, cut costs, try to grow, avoid investments that don’t pay back in 3-5 years, sell.

And selling is often a shell game where one private equity firm hands off a portco to the next, bigger fish.

There are some differentiators- Thrive, Silver Lake, Alpine - all have differentiated playbooks. The LMM guys often have an angle too, providing the first phase of sophistication for SMBs.

But the truth is most traditional PE firms exist at this point because they generate ~S&P500 returns while old school LPs (often the GPs alma mater endowment) feel “diversified”.

The only people consistently getting outsized returns are the GPs.

Many “pre-partners” inside the industry dream of launching their own fund, doing things their own way. But the promise of more money - the payoff - keeps them around.

Those folks should be careful. There are no guarantees. Past performance may not indicate future.

There is no doubt PE is in a tough spot right now, but it is an industry made up of very smart, rich people. They will fight.

The endgame here is going to be interesting.

1

6

798

FoundersFirst_ retweeted

BREAKING: December PPI inflation comes in at 3.0%, above expectations of 2.7%.

Core PPI inflation unexpectedly RISES to 3.3%, above expectations of 2.9%.

Core PPI inflation is now at its highest level since July 2025.

PPI inflation is running hotter than expected.

328

1,053

6,058

727,910

FoundersFirst_ retweeted

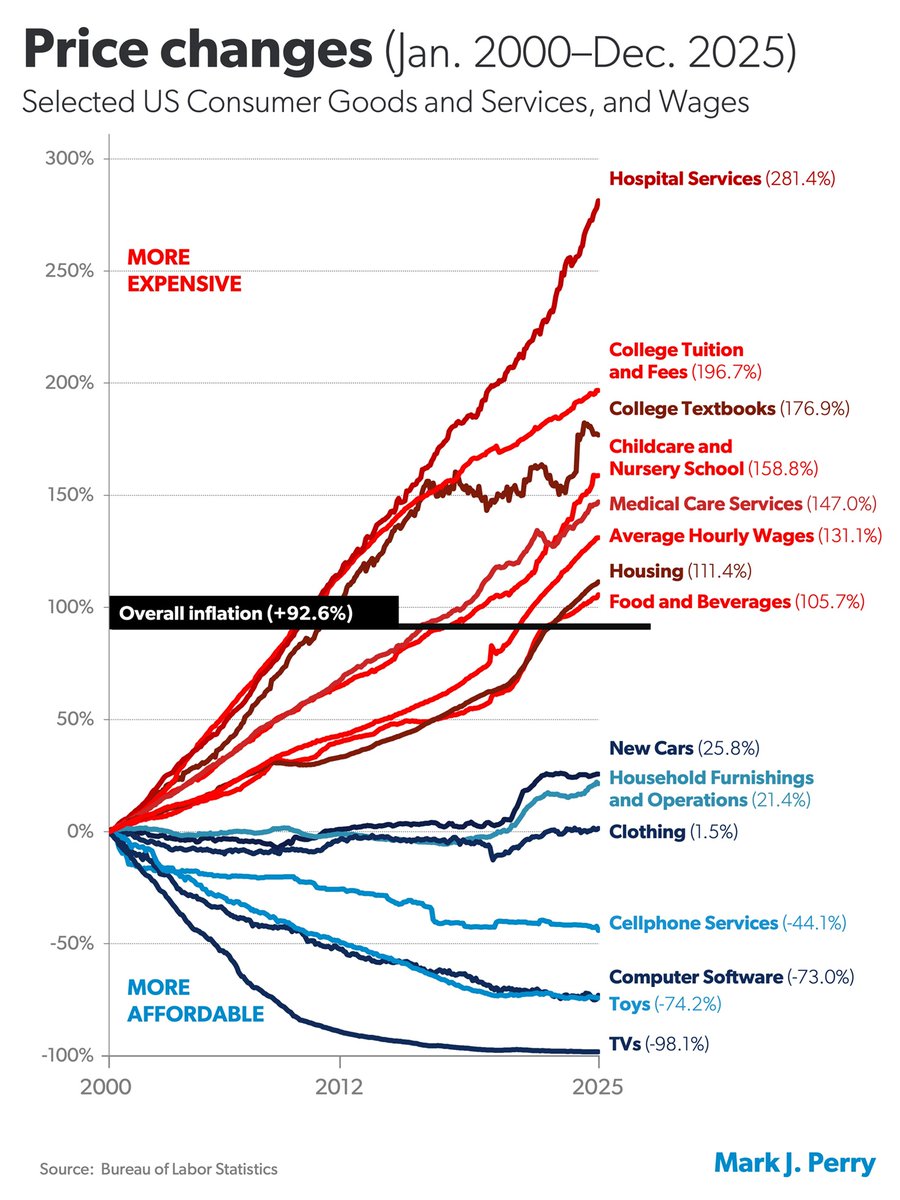

Jan 25

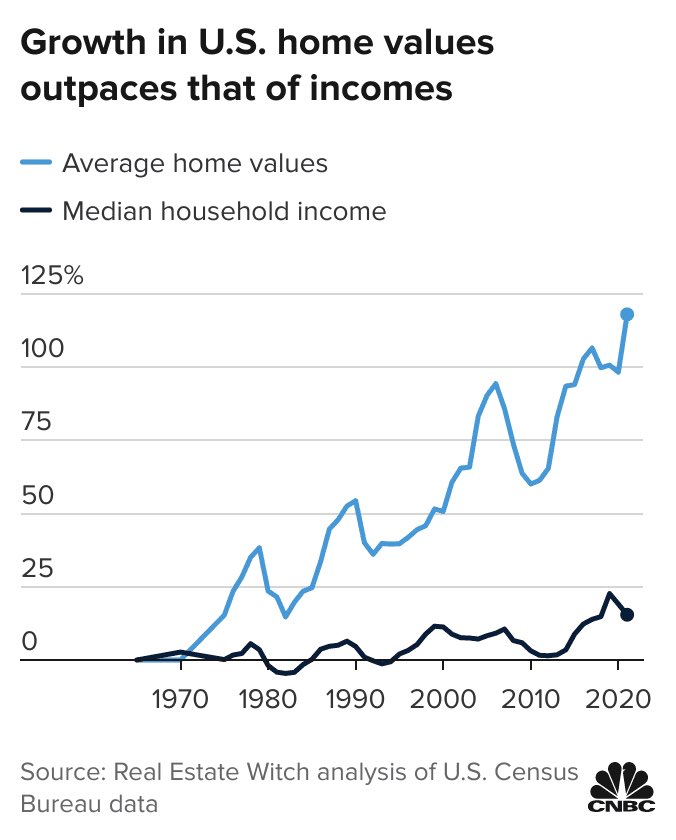

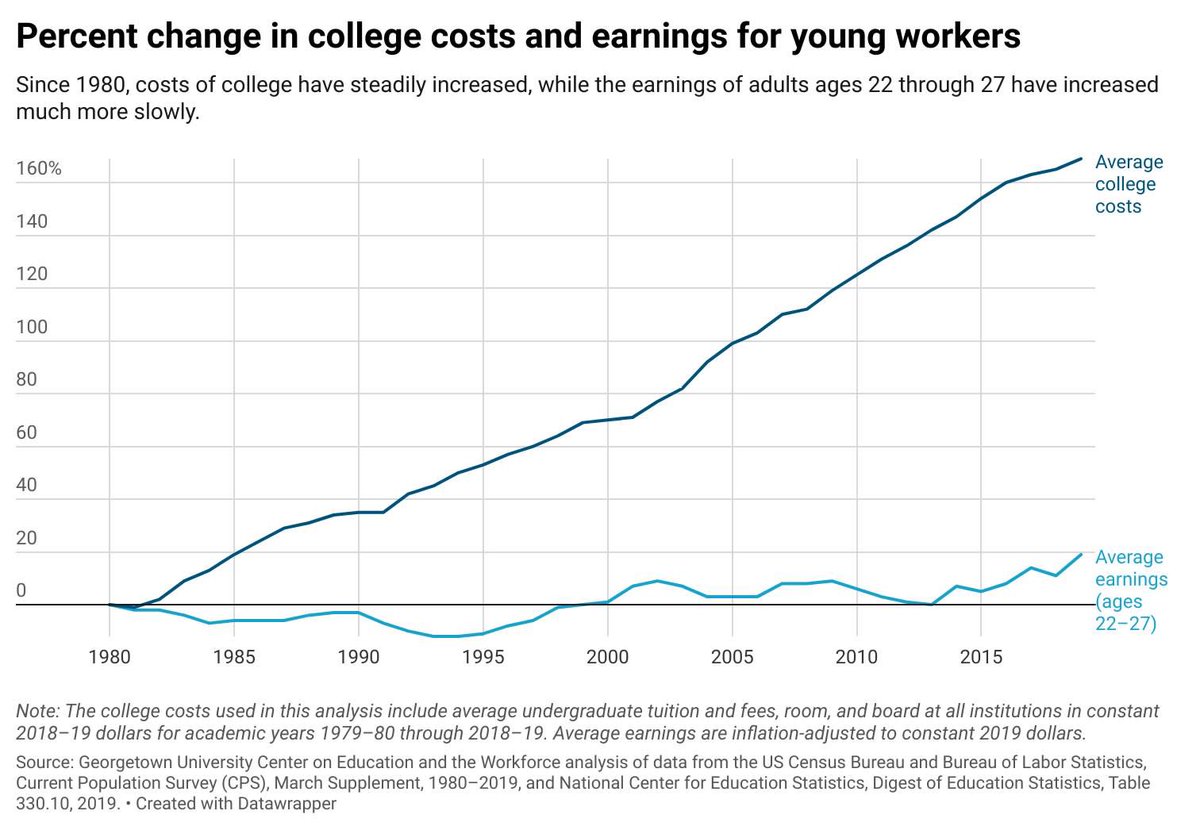

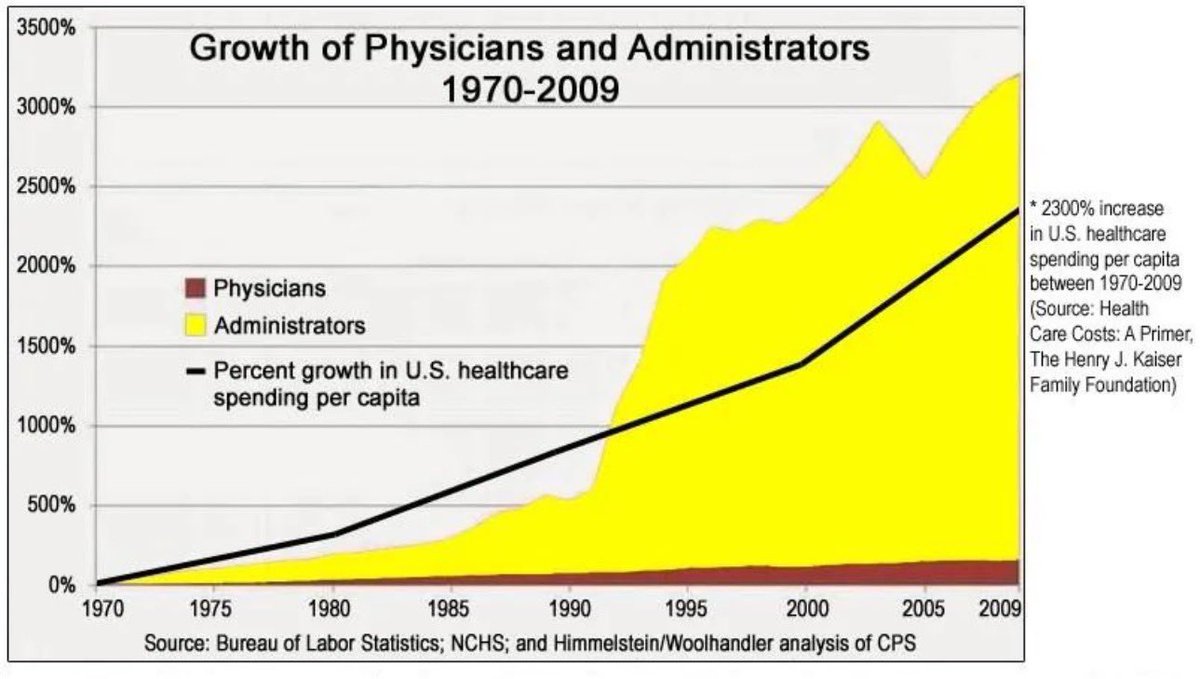

"Chart of the Century" updated through December 2025.

329

1,938

8,480

1,617,562

FoundersFirst_ retweeted

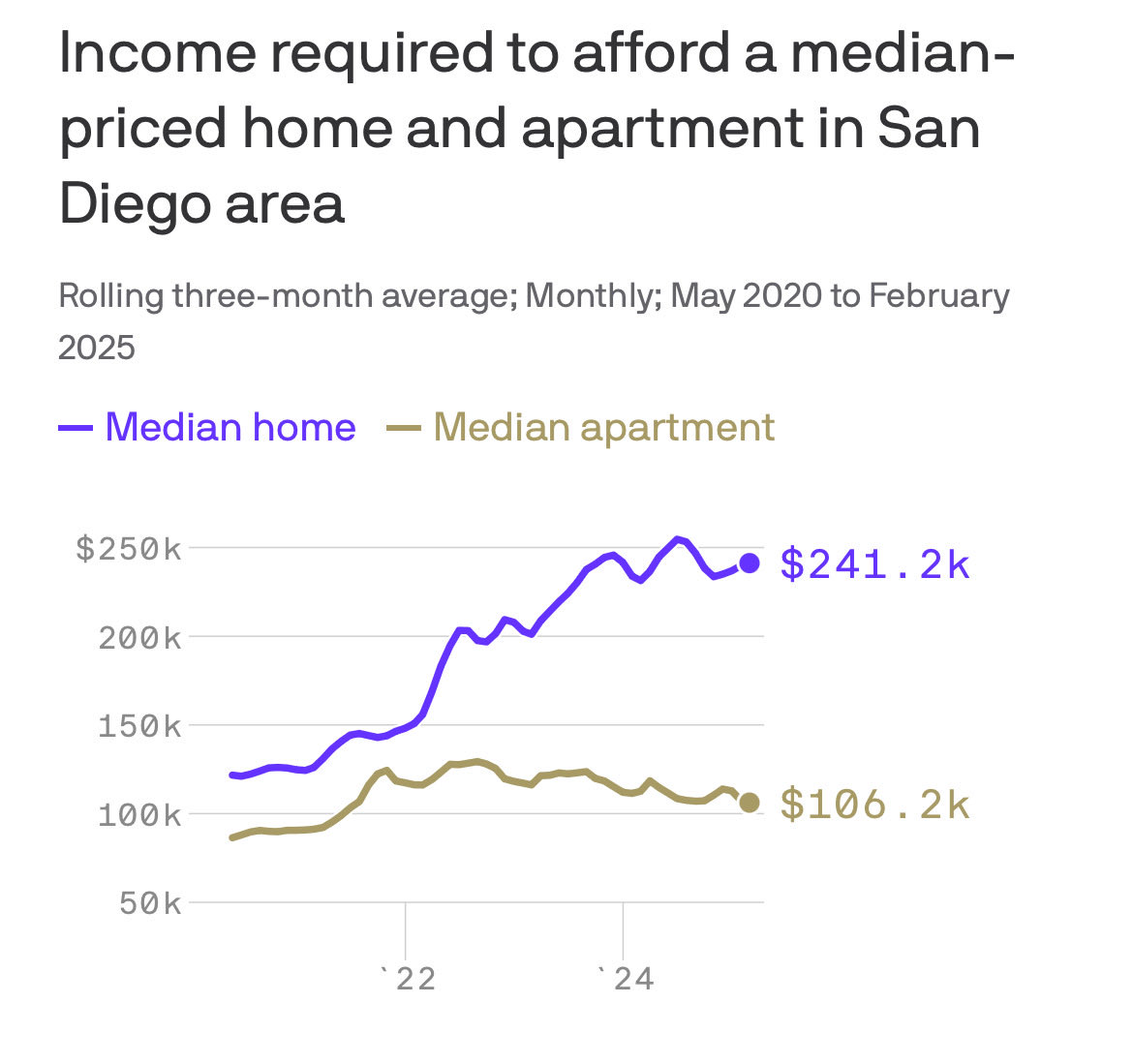

Jan 22

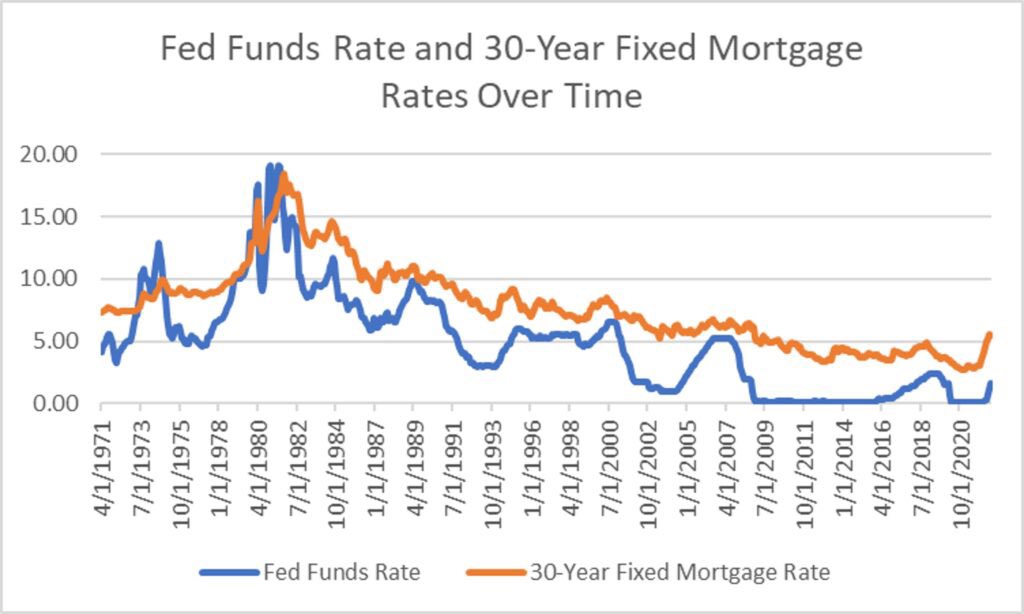

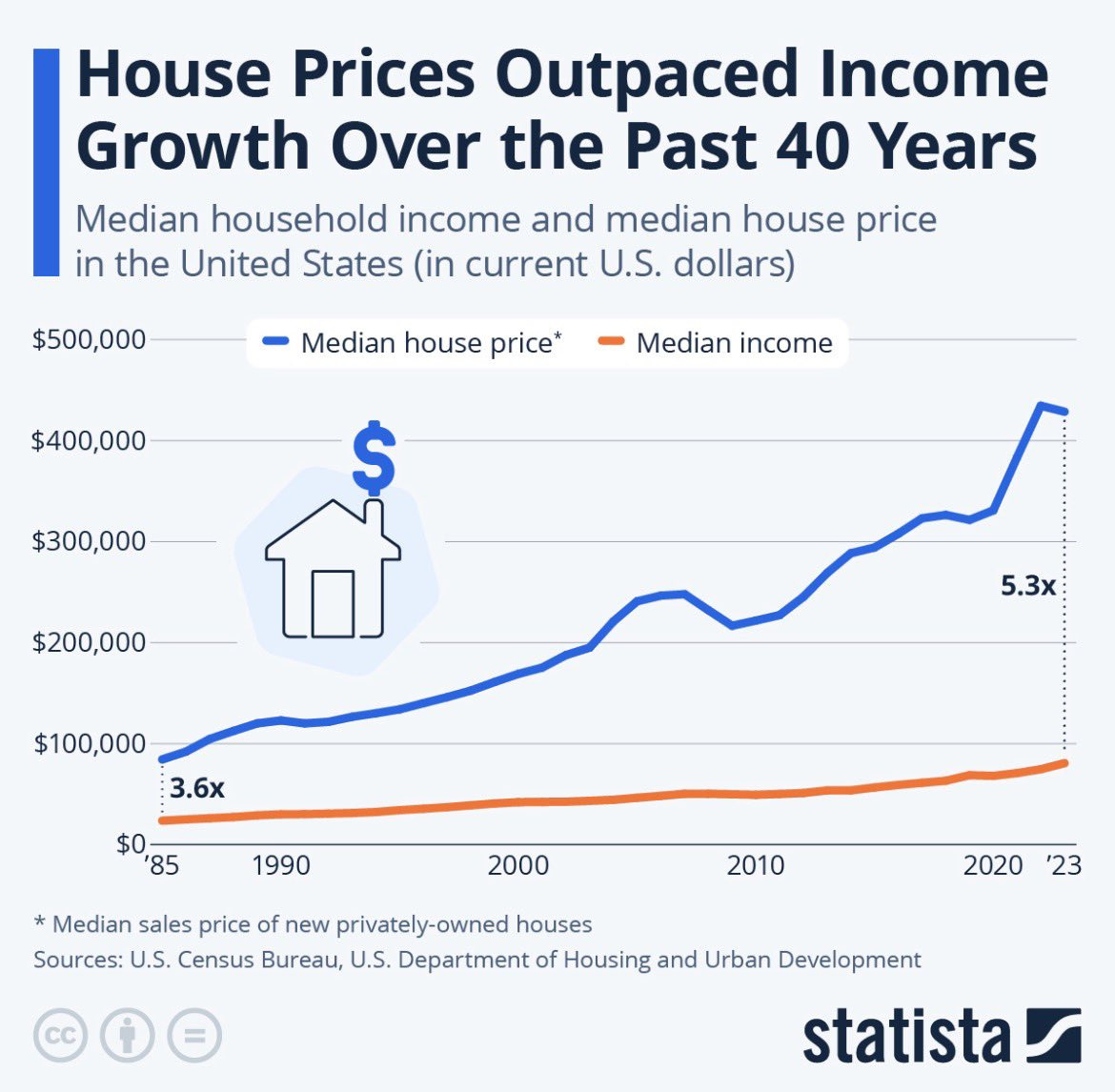

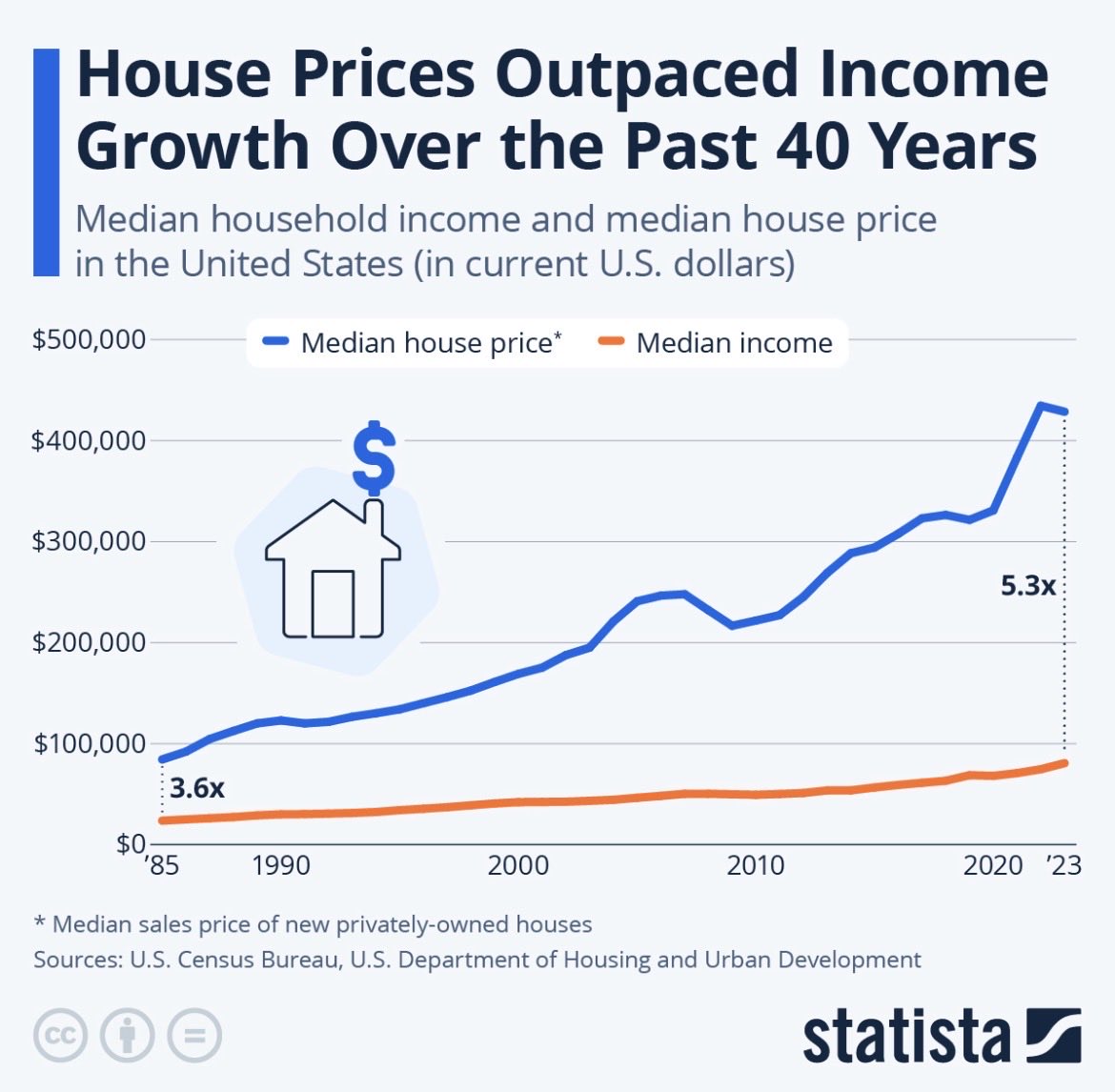

All else being equal, we'd return to pre-pandemic 2019 housing affordability levels...

IF U.S. incomes spiked 56%

IF U.S. home prices fell 35%

IF mortgage rates fell 3.50 percentage points (from 6.15% to 2.65%)

59

48

453

40,838

“Show me the incentive and I’ll show you the outcome.”

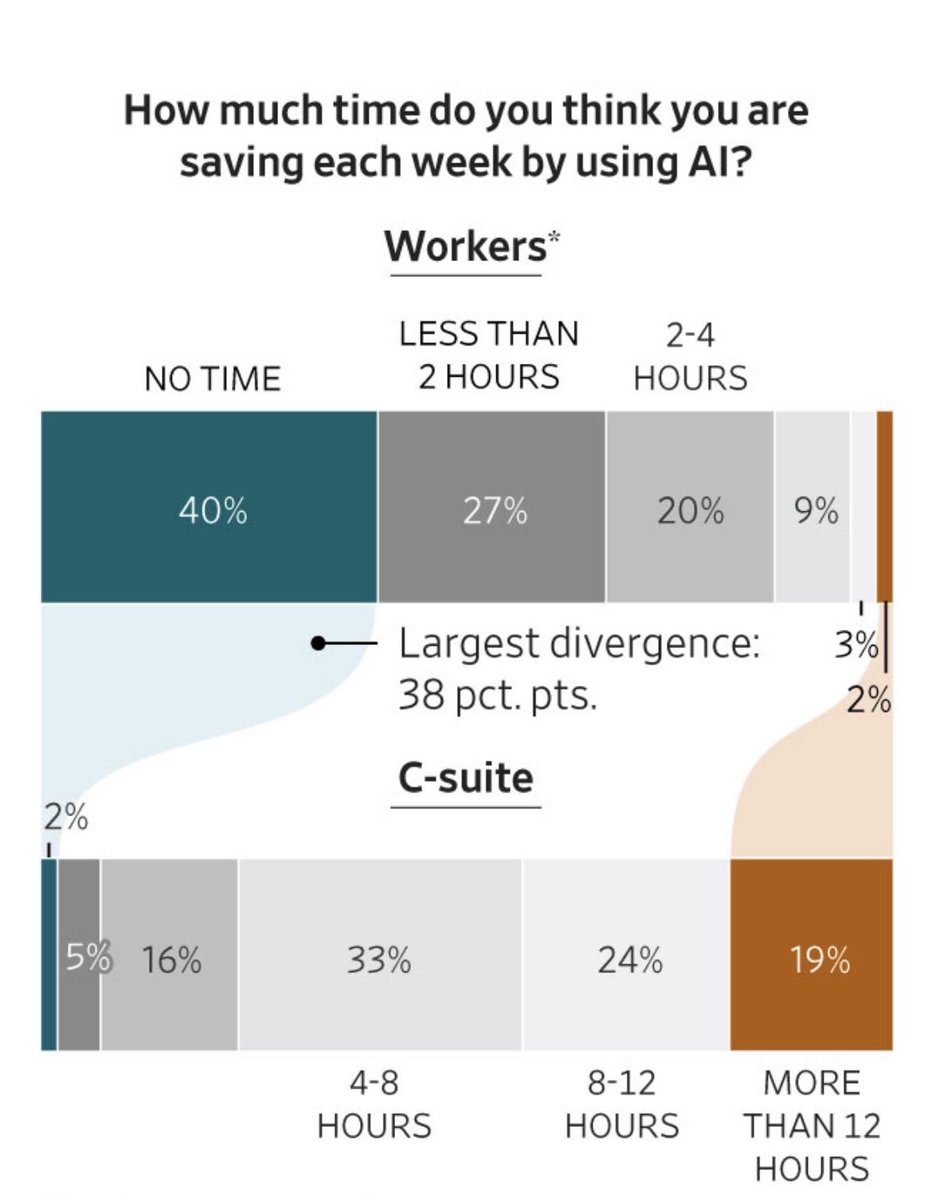

“CEOs Say AI Is Making Work More Efficient. Employees Tell a Different Story.” - WSJ

1

42

FoundersFirst_ retweeted

Jan 18

If you were in SaaS it’s probably time to pivot to infrastructure

2

1

11

2,485

Equity escalator is accelerating out of reach, Gen Z is responding rationally

YR | Avg Wages | Avg Home Price | Home % of Wage

2026 | $83k | $410k | 490%

~2030 | $95k | $490k | 520%

~2040 | $130k | $750k | 580%

~2050 | $178k | $1.15M | 650%

Jan 13

Gen Z is defiantly ‘giving up’ on ever owning a home, per YF.

Read more: unusualwhales.com/news/gen-z…

1

48

218

865

4,620

2,675,985

FoundersFirst_ retweeted

16 Dec 2025

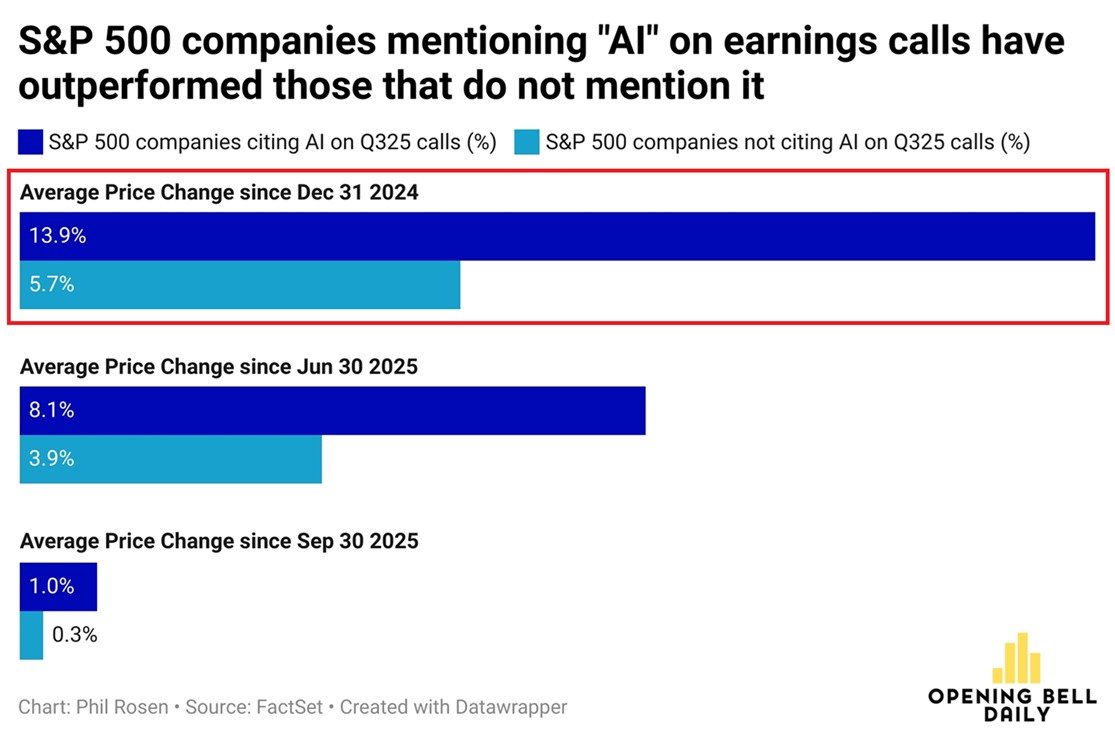

Mentioning AI on earnings calls is paying off:

S&P 500 companies mentioning AI on earnings calls are up 13.9% year-to-date.

This is more than 2 TIMES stronger than the performance of companies not citing AI, which are up 5.7%.

Furthermore, since June 30th, AI-mentioning stocks are up 8.1%, double the gains of firms not discussing AI.

A record 306 S&P 500 companies mentioned AI on their earnings calls in Q3 2025.

This figure is 460% above Q2 2022 levels, the quarter before ChatGPT launched in November 2022.

Investors want more AI.

70

69

631

88,040

16 Dec 2025

Potential Explanation - Overhired during pandemic due to QE creating unnatural uptick in share value, forcing public’s to fund growth machines to beat last quarter to keep the street happy, growth machine no longer needed, AI is the greatest gift as a scape goat, fire all the over hires, publicly say your all in on AI, fluff AI numbers with soft data, stock goes up with layoffs, your board thinks your genius, if you beat last quarter skip last step, if you got beat by last quarter, rinse and repeat.

16 Dec 2025

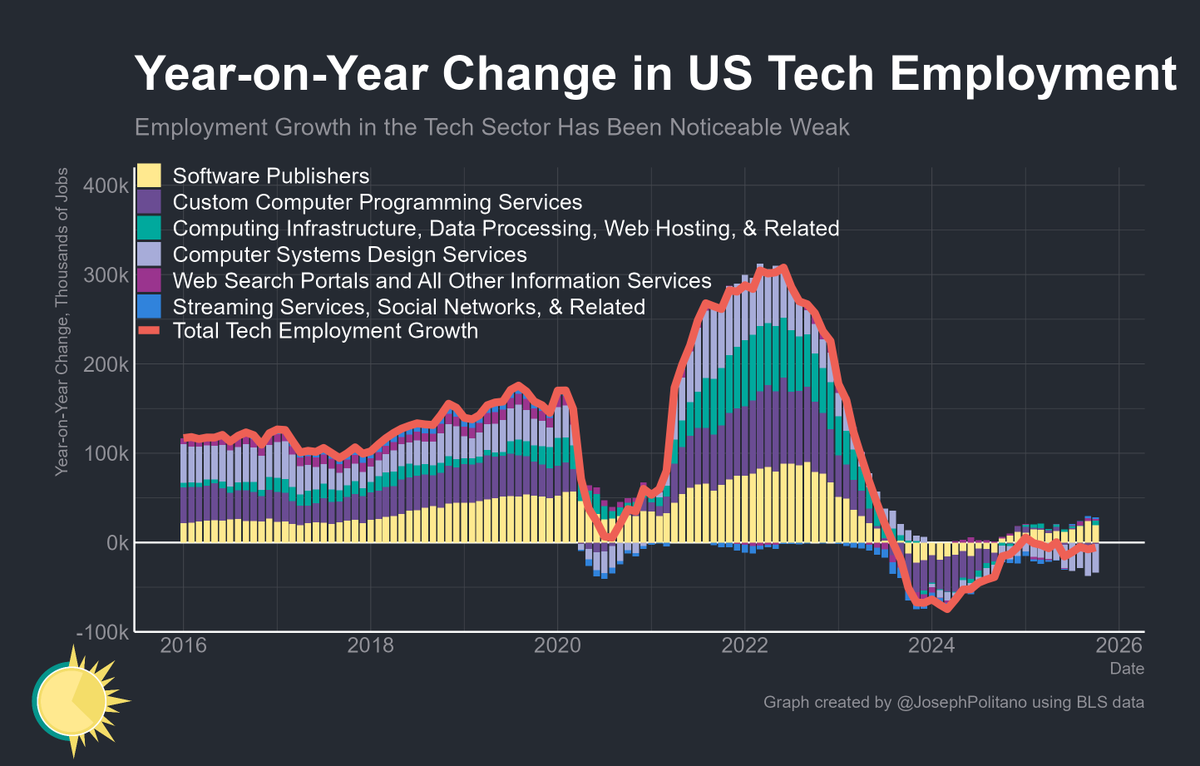

The US tech sector continues losing jobs—overall, employment decreased by 400 last month and is down 6k over the last year

That's not as bad as the worst of the 2024 tech-cession, but extremely bad compared to the 2022 boom or even pre-2020 norms

53

28 Oct 2025

You can’t fight the fed, it’s just that simple

68

FoundersFirst_ retweeted

27 Oct 2025

No one is cutting capex when you have 100% year 1 bonus depreciation.

No one.

10

10

351

53,101

20 Oct 2025

This is almost line by line the identical play during .com mania…companies had incredibly multiples if they could sell they were an internet company, if not they were forgotten for a brief period. This was especially true for legacy trying to play keep up with the valuation inflation mania…not saying the outcomes the same but this playbook is identical

NEWS: Starbucks CEO Brian Niccol says the coffee giant is now “all-in on AI.”

1

72

FoundersFirst_ retweeted

17 Oct 2025

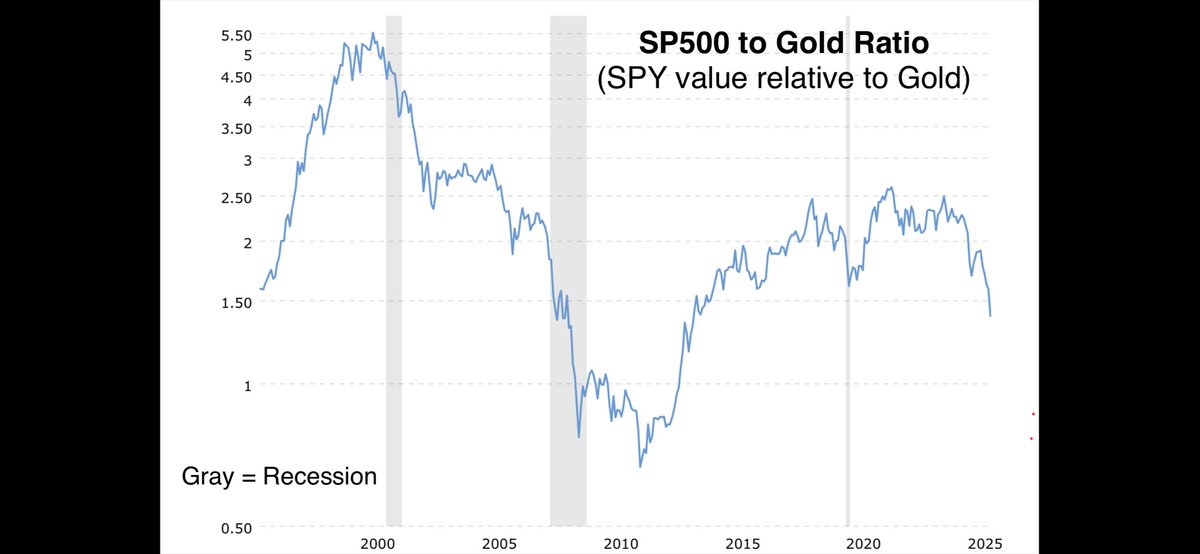

A "pet rock" should not outperform equities long-term in an economy broadly engaged in positive economic value-added activities.

A "pet rock" should absolutely outperform equities long-term in an economy broadly engaged in debt-fueled financial engineering to drive returns.

17 Oct 2025

$GLD outperfoming $SPY since it launched in 2004 is mind-melting.. flies in the face of so much conventional wisdom.

182

727

4,882

498,047

11 Oct 2025

Maverick I think is under appreciated as a catalyst of the cultural tipping point (9th largest grossing film in the last 5 yrs). Why? 1 - Classic hero story 2 - No lecture, just entertainment

1

56

10 Oct 2025

Nature is the best teacher

“1. Fire suppression makes wildfires more severe and accentuates impacts of climate change and fuel accumulation — Kreider et al., Nature Communications (2024)”

You want a conflagration (massive fire)? Keep letting dead timber accumulate unnaturally and never let it burn via artificial means.

10 Oct 2025

BREAKING: Scott Bessent says US Treasury ready to take immediate exceptional measures to ensure market stability

Community note

Need context: Secretary Bessent’s comment was in reference to the Argentinian market, not the United States market.

yahoo.com/news/articles/…

2

128