Research-Driven Quant Finance|GARCH Volatility Modeling|VaR/CVaR|Copula Academic Research

Joined April 2026

- Tweets 129

- Following 62

- Followers 15

- Likes 113

35 Photos and videos

Jun 11

Working notes on implementing a five-layer framework inspired by Medallion. We made several adjustments in signal detection, factor modeling, regime representation, and position sizing under uncertainty.

Full observations here:

open.substack.com/pub/garchq…

1

30

Jun 10

In alpha research, even good factors can lead to misleading results if the regression model is misspecified from the beginning.

One of the most common issues is how the mean structure of factors can systematically bias the intercept term (alpha). This often causes us to over- or under-estimate a signal’s true value.

1

1

40

Jun 10

A proper validation framework should include more than just one out-of-sample test.

Key elements include:

• Stability checks over time (e.g. rolling IC)

• Robust statistical methods (such as Newey-West)

• Evaluation of economic significance after costs and capacity constraints

Without these, it’s easy to draw overly optimistic conclusions.

1

19

Jun 10

Even well-validated signals eventually lose their edge as markets adapt and capital flows into popular factors.

Long-term advantage in quant research comes less from any single signal and more from building a repeatable, disciplined research process.

Full article linked in the quoted post above.

11

Jun 10

This post outlines some of the most common yet overlooked issues in alpha estimation — particularly around model specification and factor preprocessing.

At GARCH Quant, we focus on building rigorous, transparent frameworks for quantitative research.

If you’re working on factor models or alpha validation, this may be worth reading.

48

May 18

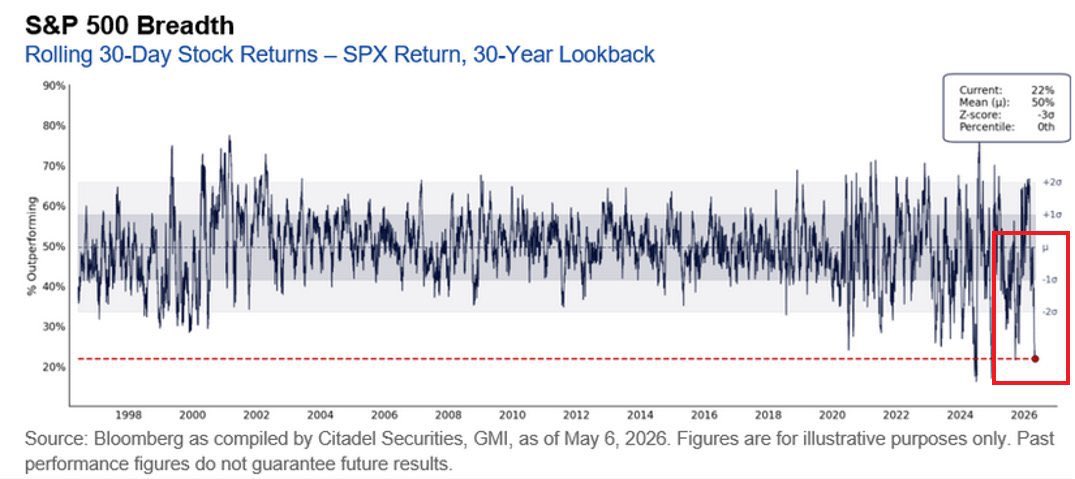

📊 Goldman Sachs Alert: S&P 500 Hits 14 New Highs… But Market Breadth Is Collapsing

The S&P 500 has registered 14 new highs in the past month, yet market breadth continues to deteriorate sharply.

A handful of tech/AI mega-caps (likely the usual suspects) have driven nearly all the gains — the vast majority of stocks are being left far behind.

Goldman’s Momentum Factor GSMEFMOM

(long top 20% of S&P 500 stocks by past 12-month returns, short bottom 20%, equal-weighted, monthly rebalance):

25% in the past 3 months — one of the most extreme surges on record.

Exhibits 3 & 4 show the market concentration is now approaching levels last seen at the peak of the 2000 Tech Bubble.

Historically, such extreme momentum almost always appears in the late stages of a bull market:

- Short-term momentum can persist

- But when it breaks, the reversal is often sharp and swift

Outlook remains highly uncertain. Watch macro liquidity, rates, and AI capex/earnings realization closely.

⚠️ Not investment advice — purely a market structure observation.

#USStocks #MarketBreadth #Momentum #ConcentrationRisk #AI

1

31

May 16

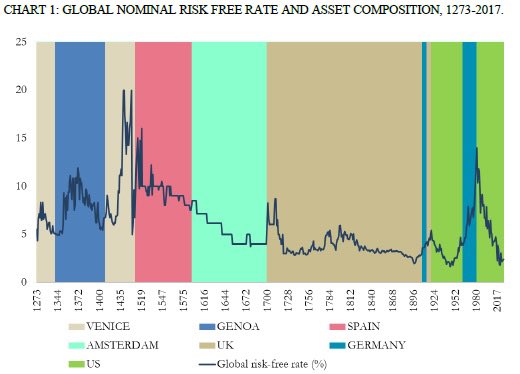

GARCH QUANT Insights| Higher for Longer: An 800-Year Perspective on Risk-Free Rates 1/4

The U.S. 30-year Treasury yield has climbed to 5.12%, reaching its highest level since 2007.

@MarketsManners offers a concise yet profound reply:

"Higher for longer. Come back to normal."

This perspective is well-supported by long-term historical data.

(Chart 1: Global Nominal Risk-Free Rate and Asset Composition, 1273–2017)

1

3

54

May 16

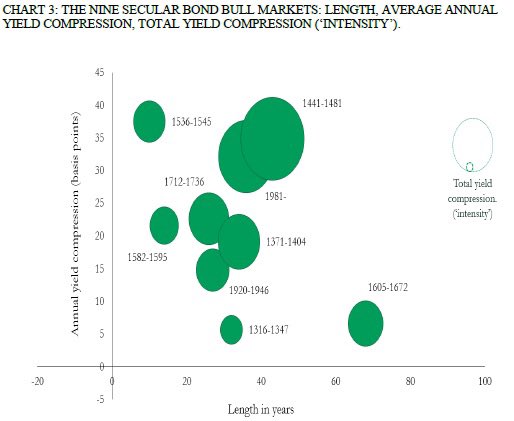

GARCH QUANT Insights| Higher for Longer: An 800-Year Perspective on Risk-Free Rates 3/4

Further insight comes from Chart 3, which analyzes the nine major secular bond bull markets in history by length and intensity (annual and total yield compression).

The 1981–present bond bull market ranks among the longest and most intense in 800 years, making its gradual conclusion particularly noteworthy.

(Chart 3: The Nine Secular Bond Bull Markets)

1

3

60

May 16

GARCH QUANT Insights| Higher for Longer: An 800-Year Perspective on Risk-Free Rates 4/4

This development signals the gradual conclusion of the super bond bull market that began in 1981.

From a long-term asset allocation perspective, the relative attractiveness of value equities, commodities, and gold is increasing.

Long-run historical data provide an essential benchmark for redefining what constitutes a “normal” interest-rate regime.

📈

quantpedia.com/800-years-of-…

#US30Y #InterestRates #HigherForLonger #AssetAllocation #EconomicHistory

2

39

May 15

2/8

GARCH-QUANT GitHub Organization

A focused platform dedicated to independent academic quantitative research in volatility modeling, empirical market cycle analysis, and advanced risk management.

1

1

19

May 15

3/8

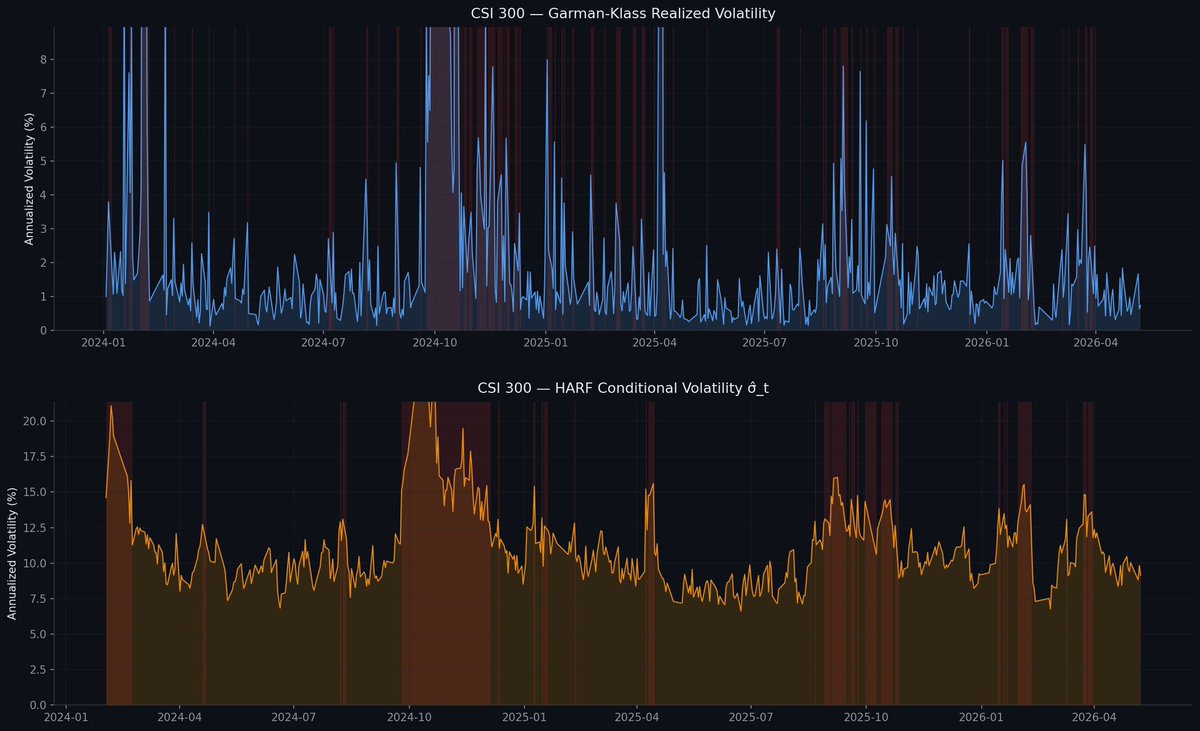

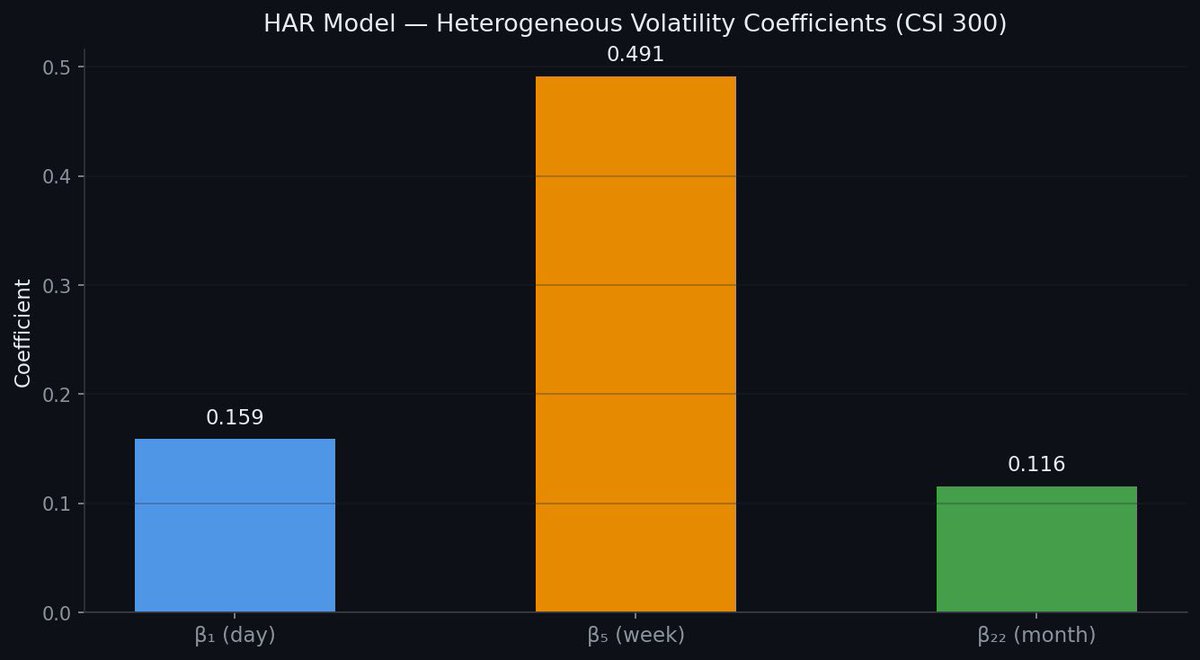

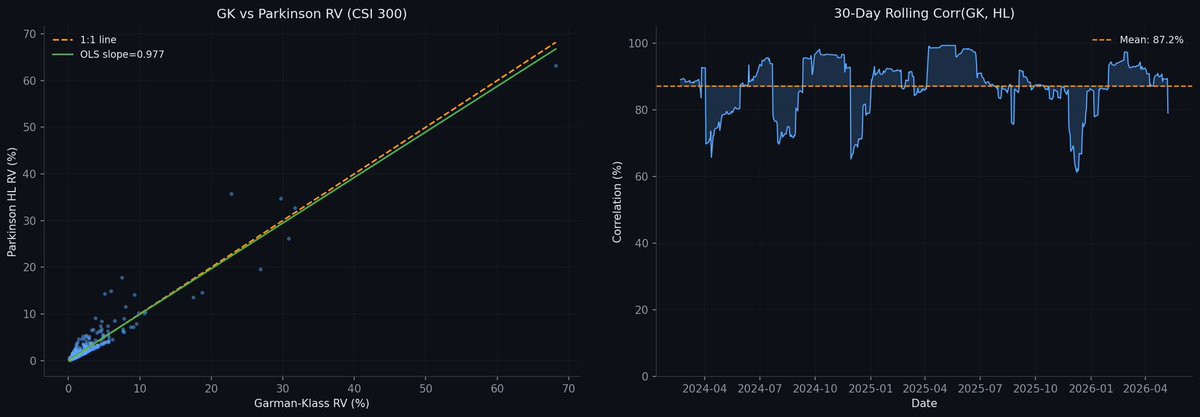

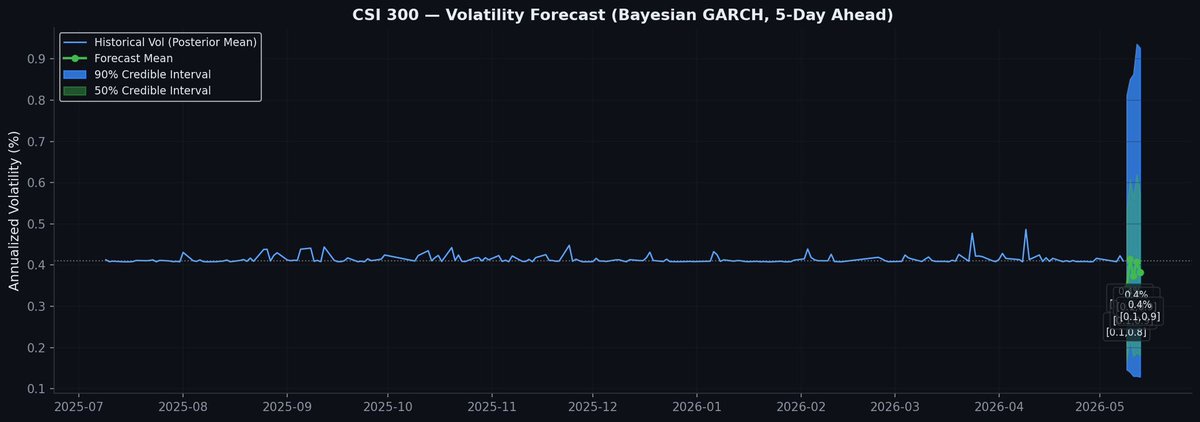

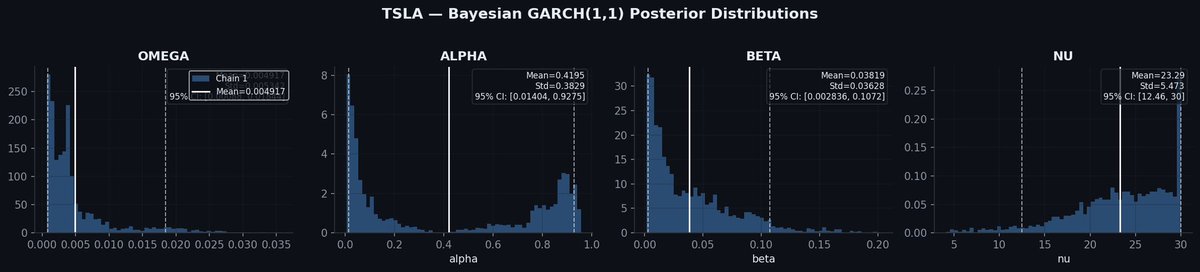

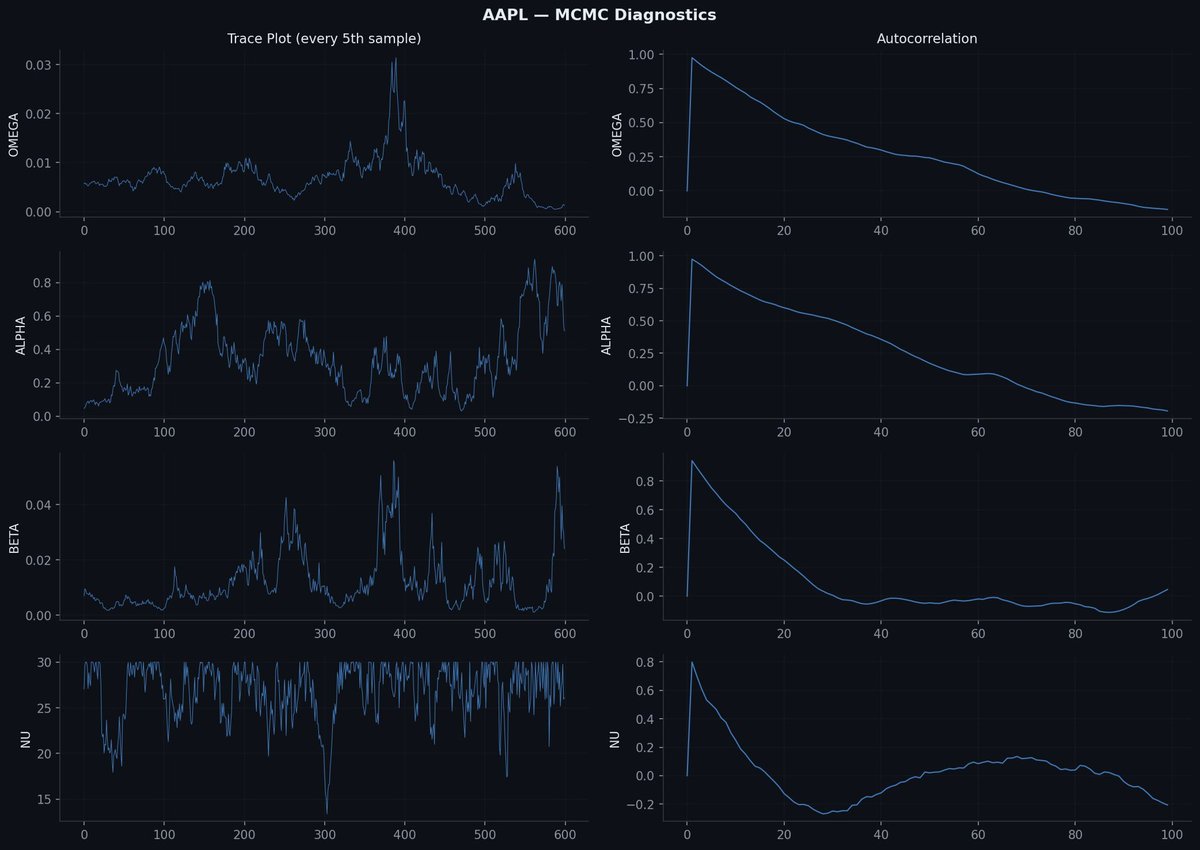

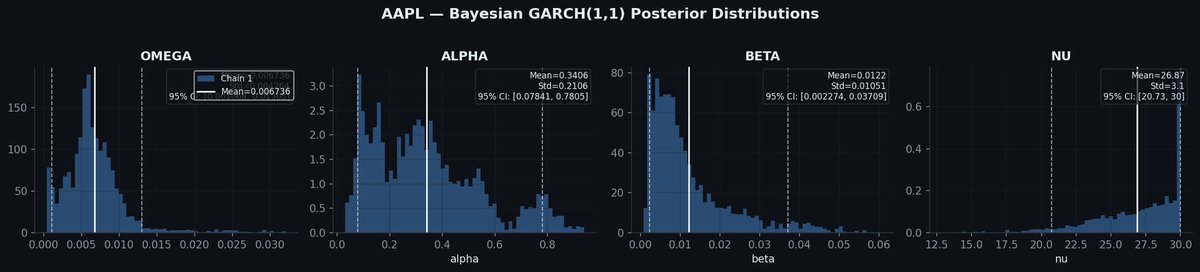

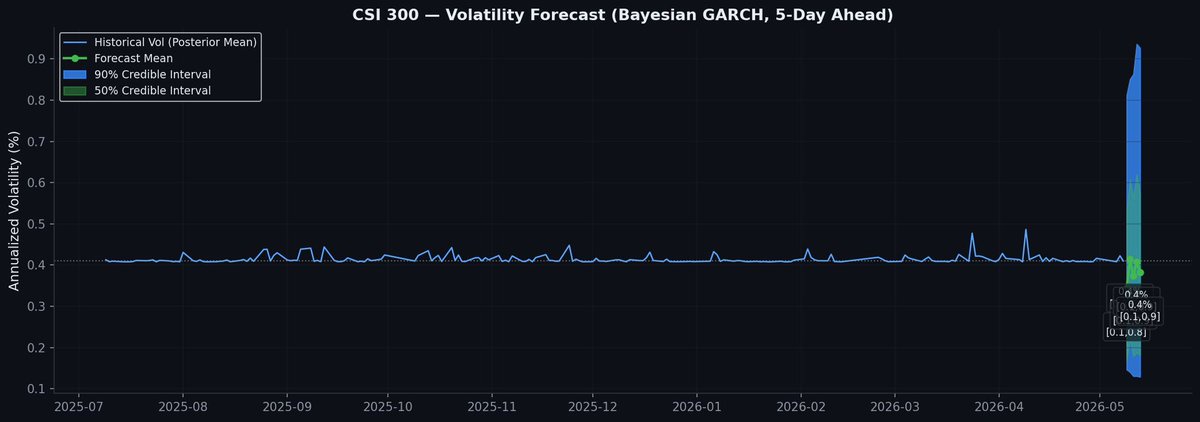

🔹 garch-quant: A comprehensive toolbox for advanced GARCH-family models, covering Bayesian GARCH, DCC-GARCH, MIDAS-GARCH, MS-GARCH, Realized GARCH, and EVT VaR. Designed for volatility forecasting, risk modeling, and option pricing — supporting both academic research and practical strategy development.

1

19