Hashem Pesaran is the John Elliott Distinguished Chair in Economics at USC, Emeritus Prof. of Economics at Cambridge University, and Fellow of Trinity College.

Joined December 2014

- Tweets 217

- Following 190

- Followers 2,860

- Likes 136

34 Photos and videos

Apr 30

An Economic Model for Securing Hormuz by Massoud Karshenas, et al @ProSyn prosyn.org/3rfGDKC

6

5

17

2,049

24 Jun 2025

Economic sanctions and embargo are effective as prelude to wars. Israel and US attacks on Iran provide further evidence that sanctions as political tools do not succeed and often lead to wars. Negotiations accompanied by trust and mutual respects are the only way forward.

2

5

53

3,328

14 Dec 2024

We show that mean-variance portfolio need not be efficient when risk premia of a traded risk factor differs from the factor’s mean. See my recent paper with Ron Smith published last week:

academic.oup.com/jfec/advanc…

3

22

2,213

Hashem Pesaran retweeted

17 Aug 2024

The very last presentation of our three day EMCC-VIII conference is by my brilliant co-author @matt_burke1 on #ClimateChange & Sovereign #Credit Ratings.

In our latest work with Matt, @JosephEStiglitz (@Columbia) @MatthewAgarwala (@BennettInnovate) & @PatrycjaKlusak (@HeriotWattUni) we link #climate science with sovereign #risk assessment to produce a single measure of country-level climate change risk.

More specifically, we integrate climate change scenarios from integrated assessment models with an analysis of sovereign creditworthiness to simulate the impact of climate risks on credit ratings, cost of debt and probability of default. In our sample of 48 countries, a Fragmented World scenario yields an average downgrade of 2.5 notches, a mean increase in the cost of debt of 61 basis points and an increase in the probability of default of 4.7%, by 2050.

Stay tuned for the working paper which will be out at the end of this month!

The Econometric Models of Climate Change (EMCC) VIII Conference, is taking place at @Kings_College, and is organised by @Cambridge_Uni #climaTRACES Lab in collaboration with @janewayinst, the @KingsELab, and the Cambridge Endowment for Research in Finance (CERF) at the @CambridgeJBS.

@Gates_Cambridge | @CRASSHlive | @CamEcon | @BennettInst

4

12

1,678

29 Jul 2024

Cutting investment in infrastructure is not the best way to reduce UK debt-output ratio. We find debt-output ratio to be much more responsive to fiscal shocks as compared to technology/investment shocks.

ideas.repec.org/p/fip/feddgw…

1

4

30

2,086

Hashem Pesaran retweeted

23 Jun 2024

There is a lot of talk this weekend about the impact of #Brexit on the UK economy. The process not only damaged us directly but most probably exacerbated the impact of #Covid and #energyprice shocks.

@NIESRorg analysis from Nov 2023:

🎩 @NiGEMmodel

niesr.ac.uk/publications/rev…

1

24

40

7,696

Hashem Pesaran retweeted

2 Jun 2024

Our next monthly International #Iranian Economic Association Webinar is on Measuring and Battling #Corruption with Daniel Kaufmann (@kaufpost, Nonresident Senior Fellow @BrookingsInst & Chief Advisor @NRGInstitute) and Nadereh Chamlou (@nchamlou, IIEA & Nonresident Senior Fellow @AtlanticCouncil).

Join us on Monday 10th of June at 16.00 UK time: zoom.us/webinar/register/WN_…

NOTE: this is happening on Monday as opposed to the usual Wednesday #IIEAWebinar.

3

6

2,472

Hashem Pesaran retweeted

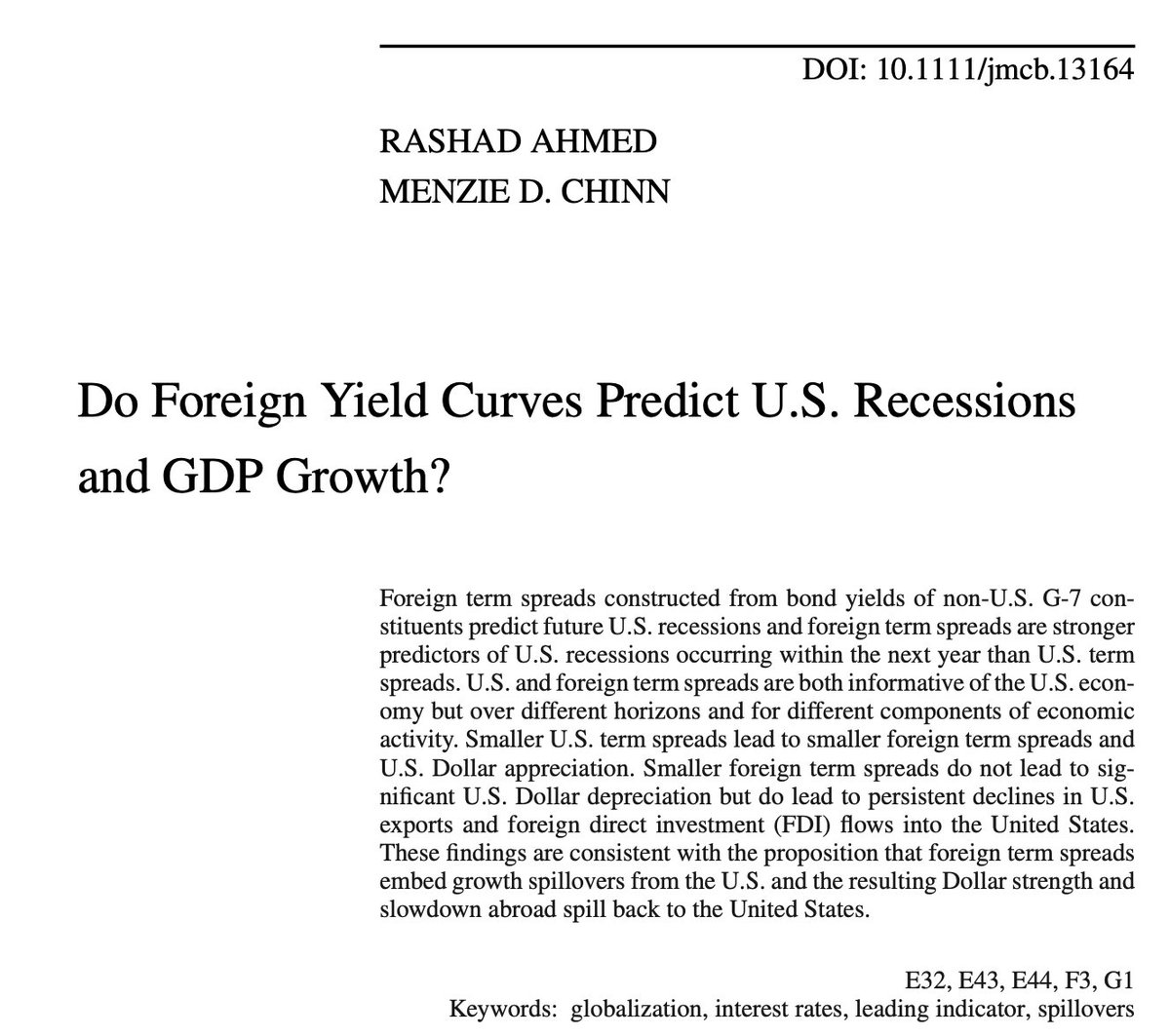

8 Jun 2024

Our paper (@menzie_chinn) showing that foreign yield curves contain information about future US economic activity is officially out in the Journal of Money, Credit and Banking!

link: onlinelibrary.wiley.com/doi/…

WP version: papers.ssrn.com/sol3/papers.…

6

17

112

17,603

Hashem Pesaran retweeted

26 May 2024

Happy Birthday to the one and only Kamiar Mohaddes!! 🥳 🎈 🎉

#EMBA #CambridgeJudge #BirthdayJoy #Brilliance

1

14

4,244

2 May 2024

In a paper just released

paper: lnkd.in/emZ3KeRX

code/data: lnkd.in/eKAr9fxQ

we propose a new estimator for autoregressive panel data models with individual-specific effects and heterogeneous autoregressive coefficients that allow for unit roots. #EconTwitter

1

9

30

14,244

24 Apr 2024

It was a pleasure to present my paper (with Ron Smith) on high-dimensional multi-step ahead forecasting discussing Lasso and OCMT at CalPoly, and meet Cyrus Ramezani, Hamed Ghoddusi, Mahdi Rastad and many others. Enjoyed the discussion and the amazing location. #EconTwitter

8

132

18,814

23 Apr 2024

Data and codes available for the paper wit Timmermann & Pick on the trade off between estimation uncertainity and parameter heterogeneity in panel forecasting with large number of units and a short T. A combination forecast is proposed. #EconTwitter

arxiv.org/abs/2404.11198

14

46

4,046

17 Apr 2024

Replication of empirical results is now routinely required for economic publications. Why not apply the same standards to BoE research and forecasts?

17 Apr 2024

Three errors in inflation control via @FT

on.ft.com/3xCLNml

3

18

2,206

5 Apr 2024

The final version of my paper with Ron Smith on high-dimensional forecasting, developed from my Deane-Stone Lecture at the NIESR June 2023 is now available together with data files. Thanks to Hayun Song for excellent RA. doi.org/10.48550/arXiv.2401.…

#EconTwitter

11

60

4,717

I guess all good things must come to an end... 🥲

It has been a huge honour to captain this fantastic @TrinCollCam team on our #UniversityChallenge journey.

We had so much fun and this is due to the hard work of the production team, @rogertilling, and the brilliant @amolrajan.

15

8

188

7,466

28 Mar 2024

Hayun Song at the end of his PhD viva at USC. Many congratulations. Tahnsk also to Tim Armstrong, Cheng Hsiao and Gourab Mukherjee for their support.

Hayun will join Korea Institute for International Economic Policy (kiep.go.kr/eng/) as a Research Fellow #EconTwitter

4

37

3,657

8 Feb 2024

Lasso is routinely used for variable selection in high-dimensional settings. The paper we just released discusses the conditions under which it is justified to apply Lasso to economic time series data, and more.

arxiv.org/abs/2401.14582

20

108

10,137

Hashem Pesaran retweeted

3 Jan 2024

Thanks . The updated GVAR data can be used to shed light on the implications of increased global interactions for national economic policies.

1

5

1,060