NZ space enthusiast | Rocket Lab, hypersonics & launches | Puns, mission updates & $RKLB vibes | Kiwi aerospace fan

Joined December 2012

- Tweets 14,928

- Following 107

- Followers 1,082

- Likes 57,964

3,463 Photos and videos

Pinned Tweet

Mar 8

Fun fact - @WilliamShatner is wearing a @RocketLab jacket on @thebigbanggthry show!

Dose @Peter_J_Beck know this?

(Credit to my daughter Amy for spotting it). #StarTrek #bazinga

7

6

79

12,227

HypaWave retweeted

🚨 JUST IN: The White House has released video of President Trump SIGNING the Iran MOU at the Palace of Versailles

Secretary Rubio, Emmanuel Macron, and the rest of the room CLAPPED as President Trump signed on the dotted line

Way to go, 47! Now, back to DOMESTIC policy🇺🇸

714

2,907

18,342

494,839

HypaWave retweeted

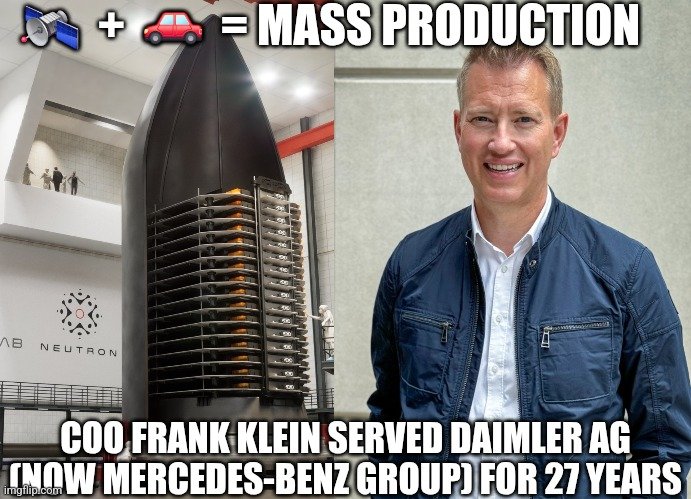

$RKLB here we go guys. The Flatellite is about to change things big time. Be careful selling this one and trying to trade. You will miss the biggest catalyst. Flatellite constellation.

Thanks @scotto2050

20h

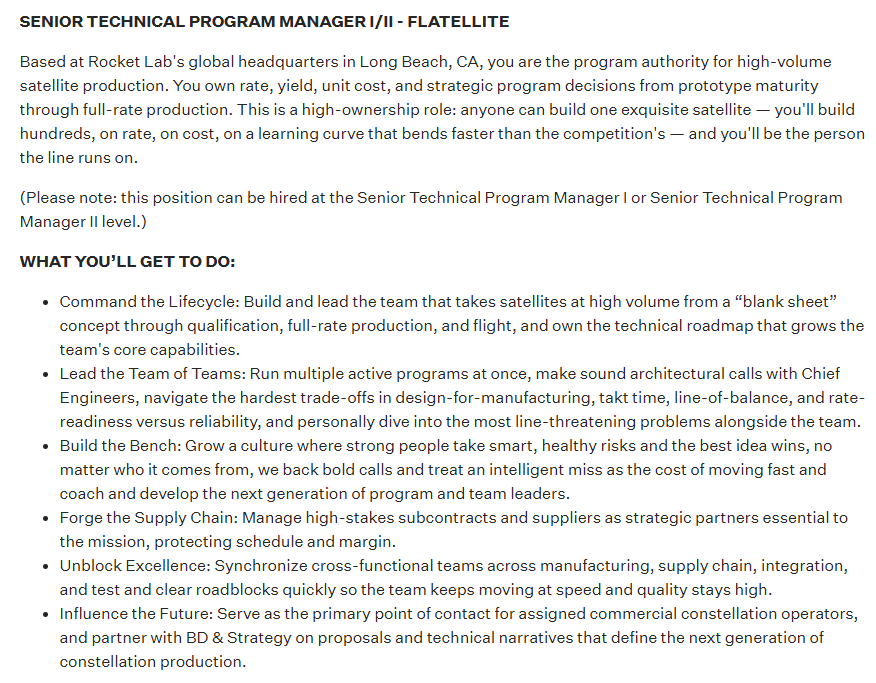

Rocket Lab Flatellite job listing posted, outlining 'hundreds [of satellites], on rate', as well as a mention for being the 'point of contact for assigned commercial constellation operators' 😏

Long $RKLB 🚀

3

10

182

13,437

HypaWave retweeted

Jun 17

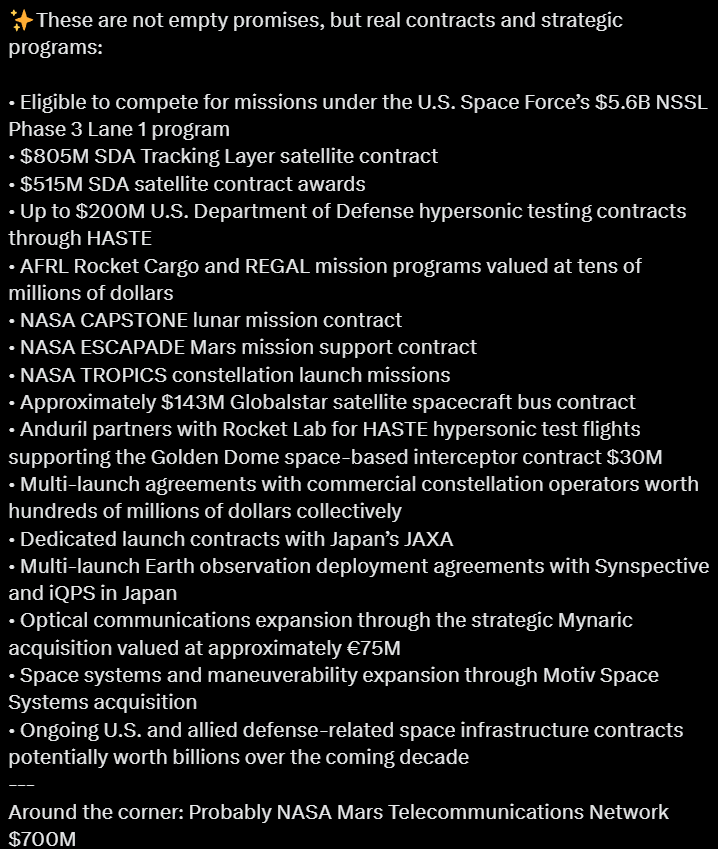

$RKLB --- Nasdaq officially announced $RKLB will be added to the Nasdaq-100 Index prior to market open next Monday, June 22, 2026. This mandates trillions of dollars in passive funds tracking the benchmark (including QQQ) to purchase $RKLB unconditionally ahead of the inclusion date. Though the stock pulled back roughly 10% on the announcement day due to profit-taking and short-term news selloff, the long-term upside is clear: liquidity will surge dramatically, and $RKLB will land firmly on the radar of top-tier institutional investors across Wall Street.

$RKLB also disclosed a joint bid with Raytheon to participate in validation work for the U.S. Space Force’s Space Interceptor Program, a core national defense strategic initiative. Separately, defense firm Anduril awarded Rocket Lab a $30 million follow-on contract to launch HASTE hypersonic test vehicles.

1.Complete De-Rocketing Transformation — Space Systems Is Its Cash Cow

Most retail investors mislabel Rocket Lab as merely a small-launch provider operating the Electron rocket, yet Q1 earnings completely dismantle this misconception:

Space Systems Segment: Delivered $136.7 million in revenue, accounting for nearly 70% of total top line. This division covers satellite manufacturing for commercial and U.S. DoD clients, solar panels, flight software, plus newly acquired laser communications hardware and components.

Launch Services Segment: Generated approximately $63.7 million in revenue.

Rocket launch operations are widely viewed as low-margin, high-risk commodity labor within the aerospace sector. By contrast, its satellite ecosystem hardware business runs a high-margin defense contractor playbook. This dual-revenue shield insulates the firm from the existential risks plaguing pure-play launch companies.

2.The Only Pure-Breed Second Supplier Capable of Absorbing SpaceX’s Spillover Launch Demand

The global commercial launch market remains drastically lopsided, with SpaceX controlling the vast majority of orbital lift capacity. However, the U.S. DoD, NASA, and large commercial satellite operators all demand a viable Plan B secondary launch vendor for antitrust compliance and supply chain resilience.

Development work on Neutron, Rocket Lab’s reusable medium-lift rocket, is in its final sprint, and the firm locked in its largest-ever bulk launch contract during Q1. A successful Neutron maiden flight will position Rocket Lab as the sole private medium-launch provider able to compete head-to-head with SpaceX’s Falcon 9, triggering a major valuation re-rating.

3.Ample Cash Reserves as M&A War Chest

Aerospace is an extremely capital-intensive industry, evidenced by bankruptcies among peers like Virgin Galactic. Rocket Lab’s balance sheet, by contrast, is rock-solid. Proceeds from its prior at-the-market (ATM) equity offering leave the company holding $1.48 billion in cash, with total liquidity exceeding $2 billion and zero near-term debt. This robust cash pile enables aggressive vertical and horizontal acquisitions (such as its two recent tech firm takeovers) without triggering shareholder dilution.

5

23

149

14,388

HypaWave retweeted

Jun 17

$RKLB

These are currently the highest price targets for Rocket Lab.

But from my experience, analysts are often on the conservative side.

I think the upside is significantly higher. My 12 month price target is $200.

11

27

224

17,924

HypaWave retweeted

Jun 15

🇺🇸 ✈️ Federal News Network recently covered Dawn Aerospace's Suborbital Spaceplane Challenge.

In its debut US operations from Infinity One Spaceport in Oklahoma, Dawn Aerospace CEO @Stefan__Powell joined host Eric White to discuss what a spaceplane capable of flying to the Kármán line twice per day could mean for science, technology development, and national security.

Designed for aircraft-like operations and rapid reuse, Aurora aims to provide a capability unlike anything currently available: routine access to the edge of space from a runway.

🎙️ Listen here: eur05.safelinks.protection.o…

#Aerospace #Spaceplane #Science #Research #Defense

3

14

969

HypaWave retweeted

We recently partnered with @GilmourSpace to conduct vibration and thermal characterisation testing at their Common User Facility!

Testing spanned across two days on the vibration table and another half day for data processing, with thermal conditions ranging from 10°C to 60°C, capturing critical insights on how our hardware behaves under the demanding environment of hypersonic stresses.

#AustralianSpace #SpaceInnovation #AerospaceTesting

2

29

3,770

HypaWave retweeted

Jun 15

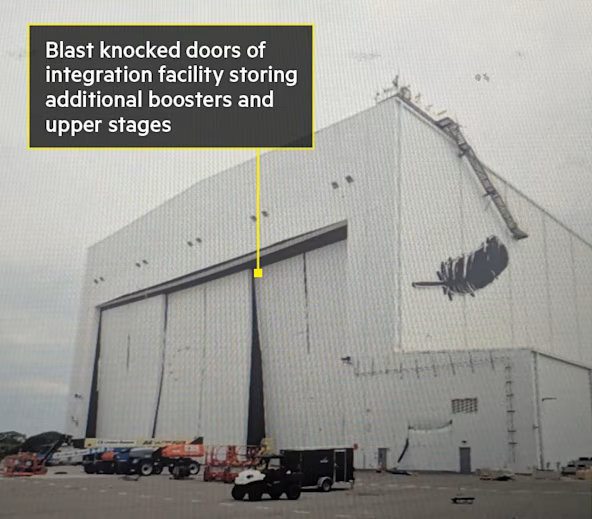

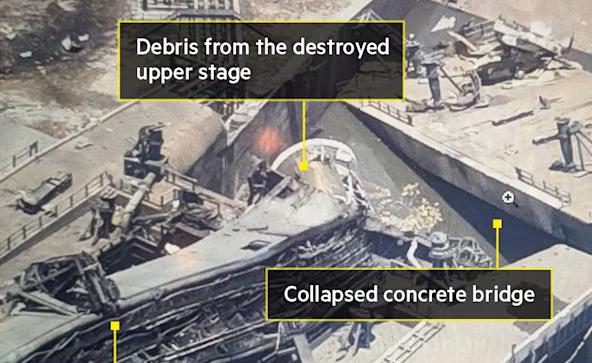

Close-up images from LC-36 shared with the Financial Times give a good view of some of the damage. The HIF doors took quite a beating, and the interstage can be seen among remains in the flame bucket. The damage to the lightning tower doesn't look too bad. ft.com/content/00db424b-be85…

8

58

443

36,058

HypaWave retweeted

Jun 15

$RKLB is not like any other space stock.

It's Sir Peter Beck's Rocket Lab Corporation. 🚀

7

5

155

8,349

HypaWave retweeted

Jun 14

$RKLB CEO Peter Beck said some space valuations are “completely untethered to reality” but reliable launch is the exception because almost nobody has actually scaled it.

Out of 142 small-launch startups tracked when Rocket Lab was founded, only two reached reliable orbital cadence: $SPCX & $RKLB.

Thats why access to orbit carries a premium since its scarce, demand is growing and very few companies can actually deliver it.

63

95

1,078

121,325

HypaWave retweeted

Jun 15

$RKLB

🚨New Rocket Lab $135 price target: KeyBanc upgrades Rocket Lab to Overweight

10

30

372

33,984

Jun 15

#HASTE Hypersonic testing in orbit?

Jun 13

US Space Force has cataloged the Electron rocket stages from the Jun 11 HASTE launch as being in orbit, but with no associated orbital data.

Does this mean CURVEBALL reached orbit and then the payload was deorbited on first orbit? Are there NOTAMs?

1

6

840

HypaWave retweeted

Jun 12

We just ran DOOM on Starcloud-1! 😅

Jun 12

Yes, Starcloud-1 runs DOOM on its H100.

Hardest part of running DOOM in orbit wasn't radiation, thermals, or bandwidth. It was resisting the urge to do this on day one.

4

35

2,120

HypaWave retweeted

🚀 $RKLB 🚀 $SPCX today:

🧑💼"Rocket Lab is the best company at acquiring and integrating businesses, imho. Here's how they do it:"

ValueOverPrice @ValueInIdeas

👨🦱"I treat them actually like startups, so they have to come pitch to me for money. They're expected to grow a certain amount every year [...] But we very much run them fast and hard and like little startups, and that's worked out really well for us."

Sir Peter Beck, Rocket Lab CEO

👨🦲"We mandate that they basically pay for themselves and sell their solutions to the merchant market, which does a couple of things. It forces them to run the business from a true P&L ownership perspective. And it also puts that competitive dynamic where they're not just getting the inputs on the roadmap from what we need, but they're really getting it from the broader kind of customer set out there, which allows us to have the best thinking about what really is the next best great thing."

Adam Spice, Rocket Lab CFO

🎦tinyurl.com/mrc7aeed

🧑💼"and now they have more capital than ever to accelerate this even further. Exciting times ahead!"

ValueOverPrice

Jun 14

$RKLB

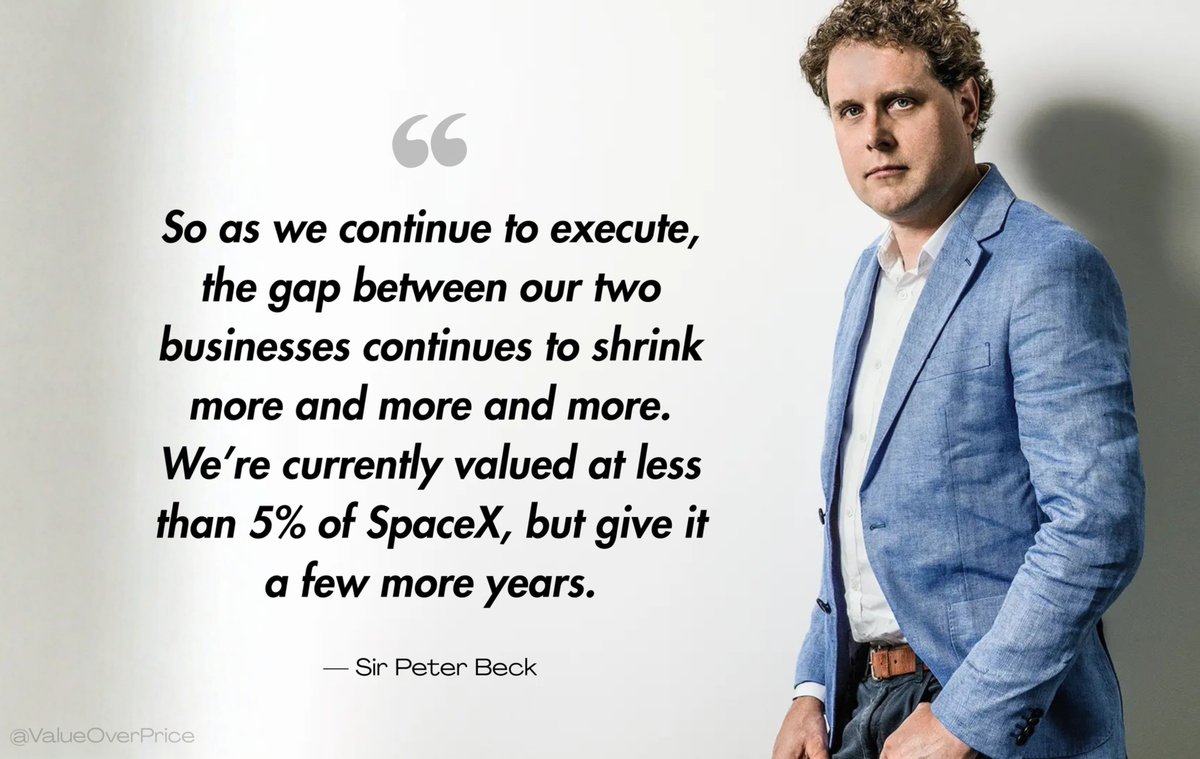

A 2024 quote from Sir Peter Beck about the valuation gap between SpaceX and Rocket Lab.

Still holds true today, with Rocket Lab's market cap at just 2.8% of SpaceX's.

"If you look at our competitors, one competitor is — as you know — the wealthiest person on the planet. But if you look at that company, its current valuation is somewhere between $250 billion and $350 billion. If you're looking for a space company that is looking like it's going to be an analog to that company, it really is us. So as we continue to execute, the gap between our two businesses continues to shrink more and more and more. We're currently valued at less than 5% of SpaceX, but give it a few more years."

I'm not saying Rocket Lab should be valued purely by comparison, but I do agree with SPB that the gap will keep tightening as they execute.

The market's expanding, Rocket Lab's hitting its milestones and all of that combined makes me incredibly bullish.

1

2

30

2,959

HypaWave retweeted

Jun 13

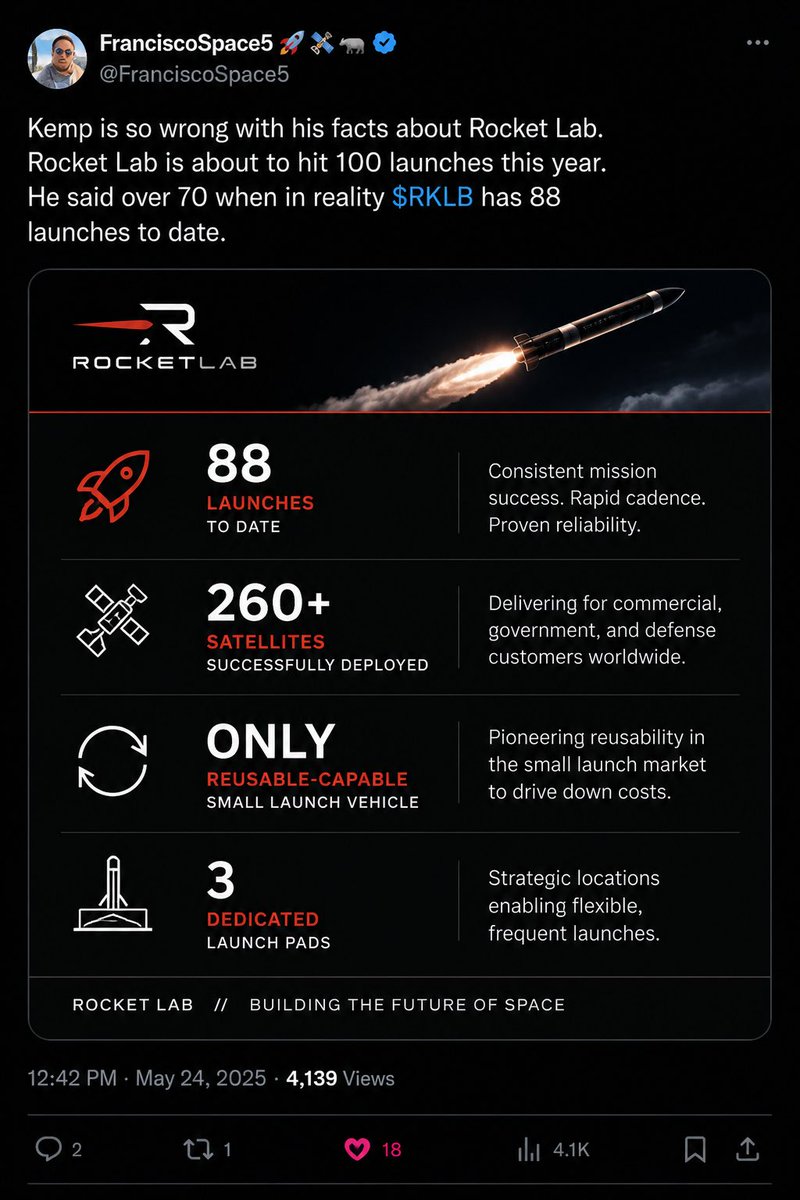

$RKLB People still think Rocket Lab is just a small rocket company.

It’s not.

Someone on CNBC mentioned Rocket Lab having “over 70 launches,” but the company has already reached 88 successful launches and deployed 260 satellites into orbit.

That’s not a startup trying to prove itself anymore. That’s execution.

Rocket Lab is quietly building an entire space ecosystem:

🚀 Frequent launches

🛰️ Satellite manufacturing

🛡️ Defense and government contracts

🌍 Space infrastructure

🔄 Reusable launch technology

And with Neutron on the horizon, the opportunity becomes even bigger.

While everyone is focused on today’s AI race, another long-term trend is unfolding in the background: the commercialization of space.

The companies that consistently execute often become the biggest winners.

Sometimes the best investments are the ones the market is still underestimating. @FranciscoSpace5

7

16

162

12,807

HypaWave retweeted

Jun 13

About to go live with the $RKLB Weekly Crew

youtube.com/live/w7Mh1aS07Yk

3

4

22

2,400

HypaWave retweeted

Jun 12

📰 What To Do with A Suborbital Spaceplane?✈️

In our latest thought piece, we explore:

💉 Microgravity pharmaceutical research

🛰️ Testing space hardware before it goes to space

🎯 Radar tracking and threat simulation

🔬 Accelerating the speed of science

📰 Read more: dawnaerospace.com/latest-new…

2

12

43

2,333

Jun 13

Found the reson why $RKLB dipped.

Jun 12

Big deal: Corewave, Nebius, Astera, Rocket Lab added to Nasdaq 100. very strong...

1

25

1,299

HypaWave retweeted

Jun 12

$RKLB

Rocket Lab discussed on Schwab again:

"We think Rocket Lab is going to ultimately benefit. And if you can buy it on a dip, I like buying it on a dip."

"they just got added to the NASDAQ, which is pretty cool."

A bit of an understatement imo, but I agree that RKLB is definitely going to benefit long term :)

1

20

213

19,980

HypaWave retweeted

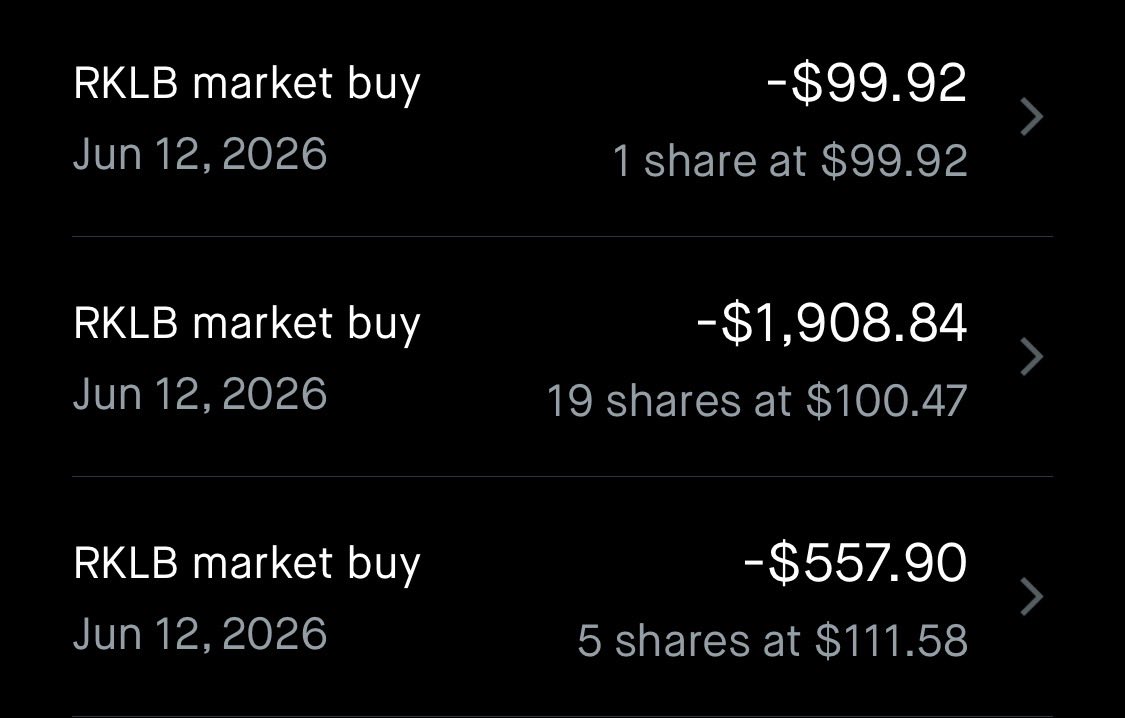

Jun 12

$RKLB This morning has triggered 2 of my BUY rules:

1. Dips greater than 10%

2. Execution (New contract plus NASDAQ 100 inclusion)

I stick to my rules, regardless of price, and block out the noise.

9

7

259

16,510

Jun 12

$RKLB $SPCX

"It might be smart to scoop up some Rocket Lab shares as the market focuses on SpaceX."

fool.com/investing/2026/06/0…

4

2

49

1,569