Joined April 2024

- Tweets 7,869

- Following 323

- Followers 40,400

- Likes 2,912

3,119 Photos and videos

TrendForce just revealed the CoPoS supply chain

Group Up $6664.TWO looks very interesting

$700M market cap

20x forward P/E

Net cash

Strong margins

It supplies film lamination, baking, peeling, and coating equipment for $TSM’s panel-level packaging and glass substrate flows

2

7

54

9,965

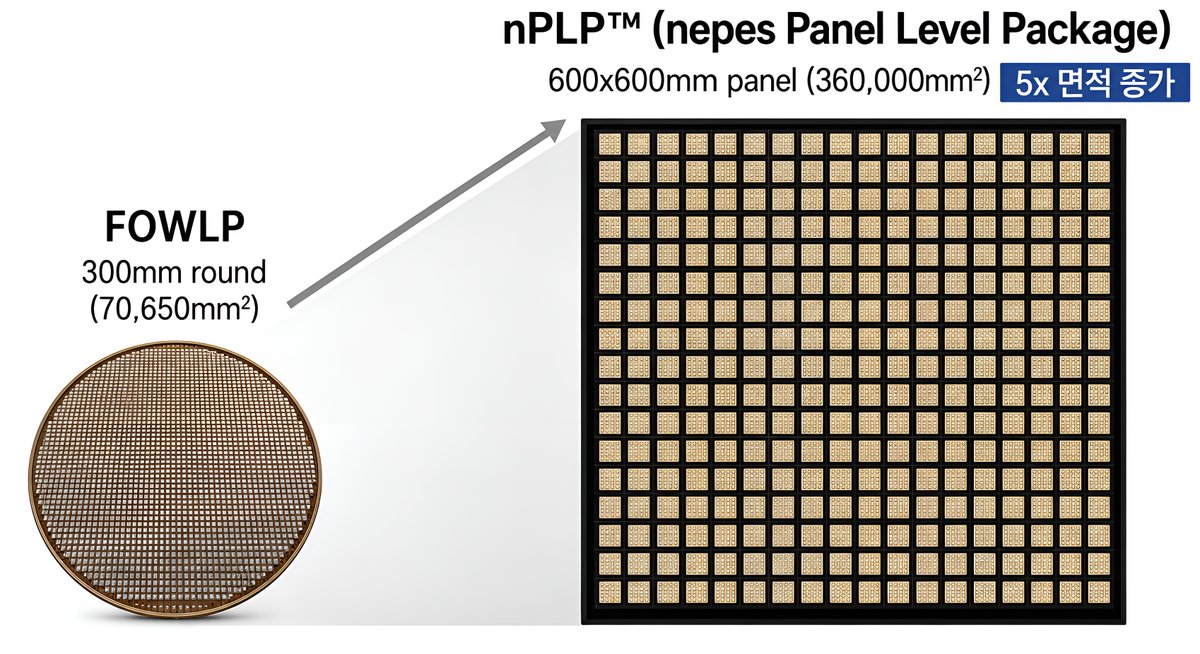

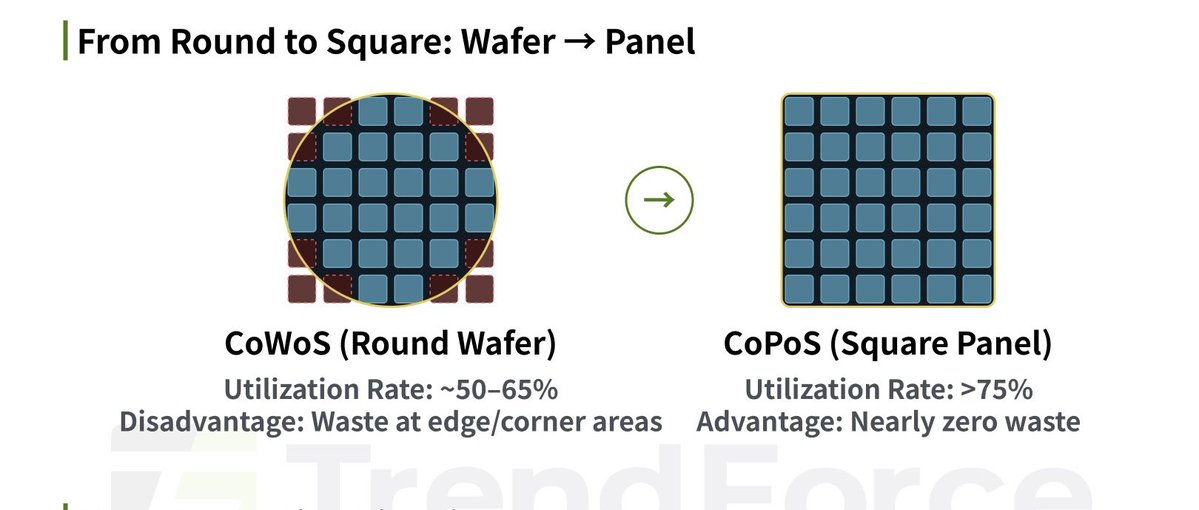

Panel-level packaging isn’t just about shape

The panels are also much larger than round wafers, so you get both less edge waste and more total package area per process step

PLP is already used in niche applications, but because it is a more complex process, panel-level packaging is still not widespread across the semiconductor supply chain

That will change soon, and it could become a true packaging revolution

Hence why you should start positioning for it

2

14

79

13,794

Ajinomoto $2802 says ABF is not currently in shortage

Ajinomoto’s CEO says AI demand is putting pressure on ABF supply, but the company expects to meet demand through 2030. Beyond that, visibility is less clear

The CEO says Ajinomoto has not raised ABF prices just because it has monopoly-like power, despite investor pressure. He argues that aggressive pricing could damage customer relationships and encourage customers to look for alternatives

However, he leaves the door open to higher prices if substrates keep becoming more complex and higher value-added. In other words, prices may rise structurally, but not through opportunistic price gouging

Ajinomoto is already preparing for longer-term demand by securing land for new facilities in central Japan. New production is expected to begin in 2032, though the timeline could be accelerated if customers need it

In other news, glass substrates are unlikely to replace ABF soon. Even if glass packaging advances by 2028, analysts expect it to be used together with ABF, not instead of it

3

4

46

5,165

Nobody guessed it

I’ll have to just say it

14

60

31,672

Jun 13

CPU shortages to ease in H2, according to MSI’s chairman

MSI says GPU chip supply has fallen around 30% because $NVDA cannot fully meet demand due to limited memory availability

PC demand is weakening because of higher prices. MSI says its DIY segment is down around 20%, while the broader PC market is down 10–20%

$AMD and Intel are reportedly increasing their priority on PC CPUs again. AMD supply should improve in Q2, while Intel supply should improve in Q3

7

14

158

27,319

Jun 13

There is one key $SPCX supplier trading at 13x 2026 EPS, and nobody is talking about it

27

4

110

80,303

Jun 13

Engrave this supply chain in your brain if you want to outperform in 2027

As an investor, it’s your duty to learn about glass substrates and PLP

Jun 12

Understanding the Panel-Level Packaging and Glass Substrate Ecosystem

3

9

75

12,285

Jun 13

This US action will push more countries toward sovereign AI

Some stocks helping countries build that:

$NBIS: leading sovereign AI partner in Israel and the UK, so far

$PENG: system enabler for sovereign AI data centers

$SKM: will become Korea’s main sovereign AI neocloud

$035420.KS / NAVER: direct Korea sovereign AI play. Will start with 55 MW and scale toward gigawatt-level sovereign AI infrastructure

$OVH.PA: Europe’s purest listed sovereign cloud

The whole ecosystem will benefit anyway, as this push will create many redundancies that are unnecessary from an efficiency perspective, but bullish for supply-chain stocks because they push demand even higher

What I mean is that not every country occupies a bottleneck position in the AI supply chain the way Korea or Taiwan does.

And the same applies to Korea and Taiwan as well. The very fact that there is now a visible possibility that the U.S. could cut off access to powerful LLMs for Korea creates uncertainty in itself.

Because of this, every country will rush into sovereign AI.

6

17

120

15,427

Jun 12

Understanding the Panel-Level Packaging and Glass Substrate Ecosystem

6

22

113

20,340

Jun 12

Jun 12

If you like $TE, you’ll love $TOYO

Same theme: U.S. solar manufacturing domestic content tariff reshoring

Different valuation

Market value

→ $TE: ~$2.4B market cap / $2.7B EV post-raise

→ $TOYO: $510M market cap / ~$500M EV

So $TE trades at roughly 4.6x TOYO’s market cap and around 5x TOYO’s EV

2026 production

→ $TE: 3.1–4.2GW module production guide from G1_Dallas

→ $TOYO: 5.5–5.8GW solar cell shipments 1.0–1.3GW module shipments

Q1 financials

→ $TE: $178M revenue / 16.4% gross margin / $9.1M adjusted EBITDA / -$72.9M operating cash flow

→ $TOYO: $143M revenue / 33.5% gross margin / $48.3M adjusted EBITDA / $33.4M operating cash flow

$TE has more slightly more revenue

$TOYO has better margins, EBITDA conversion, profitability, and cash generation

Expansion plans

→ $TE: 5GW G2_Austin TOPCon cell plant, with first 2.1GW phase targeted for initial production in Q4 2026

→ $TOYO: 1.5GW Houston HJT cell plant, co-located with its U.S. module facility

$TE is the larger U.S. platform

$TOYO is the cheaper earnings/capacity play

→ Acquiring KORE Power for about $32M EV makes $TE more diversified across solar BESS data center power infrastructure, but it does not erase the valuation gap

Balance sheet

→ $TE: better working capital, but heavier debt/preferred/convertible structure and still funding G2

→ $TOYO: tighter liquidity, negative working capital, and Houston funding risk

So the apples-to-apples conclusion is:

→ $TE = bigger, more institutional U.S. policy platform

→ $TOYO = smaller, already profitable, and trading at a fraction of the valuation

8

2

41

14,594

Jun 12

Wells Fargo models $IREN reaching 5.8GW by 2030

The company has a 5GW secured power pipeline, anchored by:

- > $9.7B / 200MW Microsoft GB300 contract, phasing in through 2026

- > $3.4B NVIDIA contract, adding another 60MW of AI cloud capacity from early 2027

- > $3.7B targeted ARR by YE26, rising to $4.4B after the Blackwell deployment

The back half is driven by Sweetwater, Kiowa, Spain, and Australia

Notably, Wells Fargo still looks conservative versus company guidance, modeling 2GW in 2028 versus the company’s 5GW target

8

17

167

30,204

Jun 12

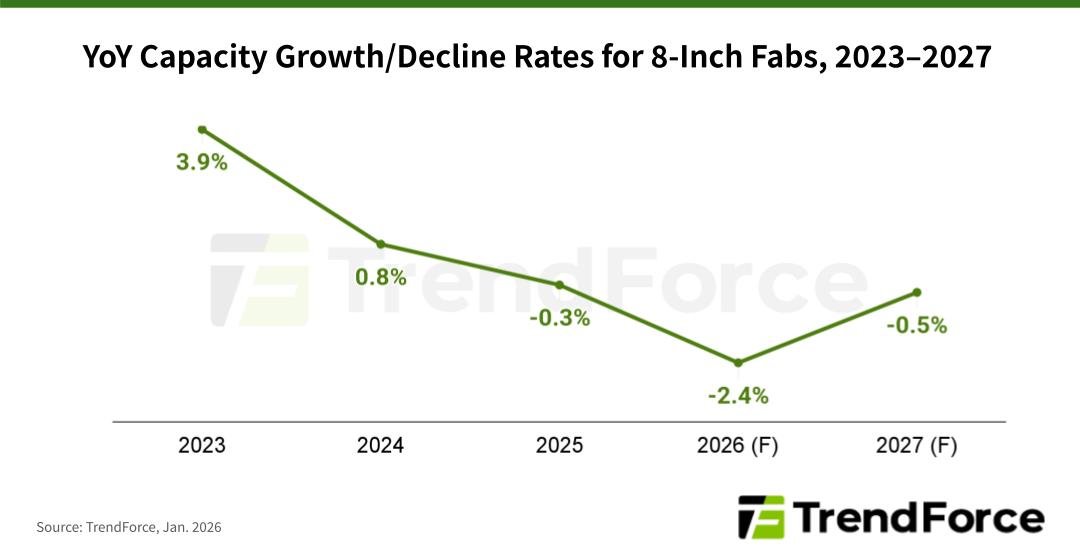

Bullish for:

$000990.KS — DB HiTek

$6770.TW — PSMC

$TSEM — Tower Semiconductor

Jun 12

8 inch fabs capacity has been declining. But demand is increasing e.g. PMICs, GaN/SiC and other power chips used in Data Centers. Result is overloaded fabs and increased prices.

3

4

28

7,950

Jun 12

If you like $TE, you’ll love $TOYO

Same theme: U.S. solar manufacturing domestic content tariff reshoring

Different valuation

Market value

→ $TE: ~$2.4B market cap / $2.7B EV post-raise

→ $TOYO: $510M market cap / ~$500M EV

So $TE trades at roughly 4.6x TOYO’s market cap and around 5x TOYO’s EV

2026 production

→ $TE: 3.1–4.2GW module production guide from G1_Dallas

→ $TOYO: 5.5–5.8GW solar cell shipments 1.0–1.3GW module shipments

Q1 financials

→ $TE: $178M revenue / 16.4% gross margin / $9.1M adjusted EBITDA / -$72.9M operating cash flow

→ $TOYO: $143M revenue / 33.5% gross margin / $48.3M adjusted EBITDA / $33.4M operating cash flow

$TE has more slightly more revenue

$TOYO has better margins, EBITDA conversion, profitability, and cash generation

Expansion plans

→ $TE: 5GW G2_Austin TOPCon cell plant, with first 2.1GW phase targeted for initial production in Q4 2026

→ $TOYO: 1.5GW Houston HJT cell plant, co-located with its U.S. module facility

$TE is the larger U.S. platform

$TOYO is the cheaper earnings/capacity play

→ Acquiring KORE Power for about $32M EV makes $TE more diversified across solar BESS data center power infrastructure, but it does not erase the valuation gap

Balance sheet

→ $TE: better working capital, but heavier debt/preferred/convertible structure and still funding G2

→ $TOYO: tighter liquidity, negative working capital, and Houston funding risk

So the apples-to-apples conclusion is:

→ $TE = bigger, more institutional U.S. policy platform

→ $TOYO = smaller, already profitable, and trading at a fraction of the valuation

8

7

69

22,359

Jun 11

2026 was the year of photonics

2027 will be the year of PLP and glass substrates

18

50

725

88,988

Jun 11

$MU flirting with $1,000 again. I love this company

Today: 11.66%

YTD: 215%

Best part is that memory could re-rate another 100% and still feel fairly valued

17

13

259

12,765

Jun 11

I was told today was going to be a bloodbath

Where are the dips I was promised?

Turns out being bearish simply sells more

8

28

3,819

Jun 11

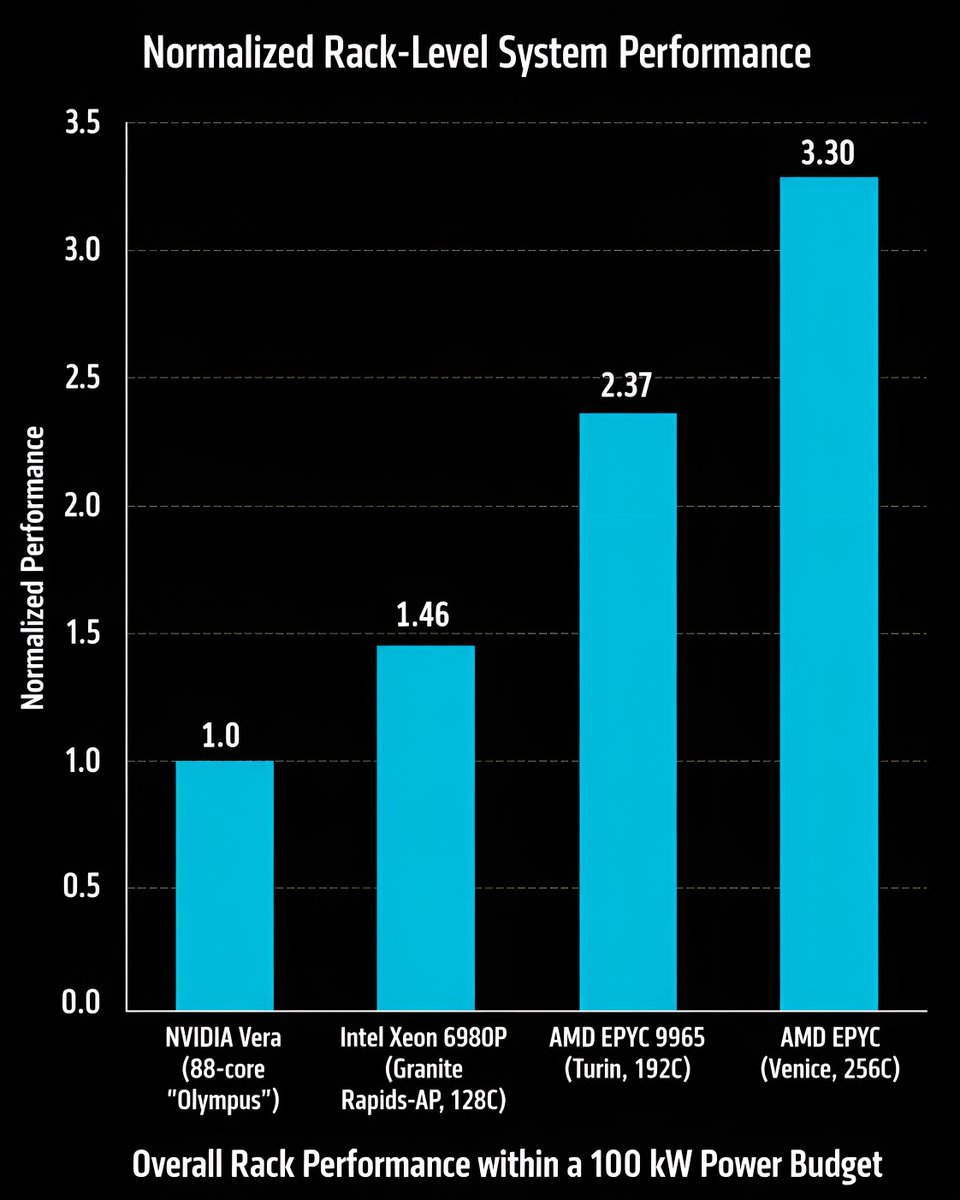

When you connect these two posts, the bull case for $AMD becomes clear

-> With the current approach (near/mid term), CPU demand will explode with Agentic AI

-> Vera is barely better than a 2024 $AMD CPU (based on $NVDA own benchmarks)

-> $AMD Venice seems to be considerably better than Vera

The picture here seems clear: as CPUs become almost as important as GPUs, AMD is a clear leader in the space

There’s also a possibility that AMD’s GPU performance gap with NVIDIA is smaller than NVIDIA’s CPU performance gap with AMD

Once you combine this with AMD improving its networking and software, primarily through collaboration with open source, clients, and other open-source standardization advocates, it may seem like the valuation gap between AMD and NVIDIA is still too large

Jun 11

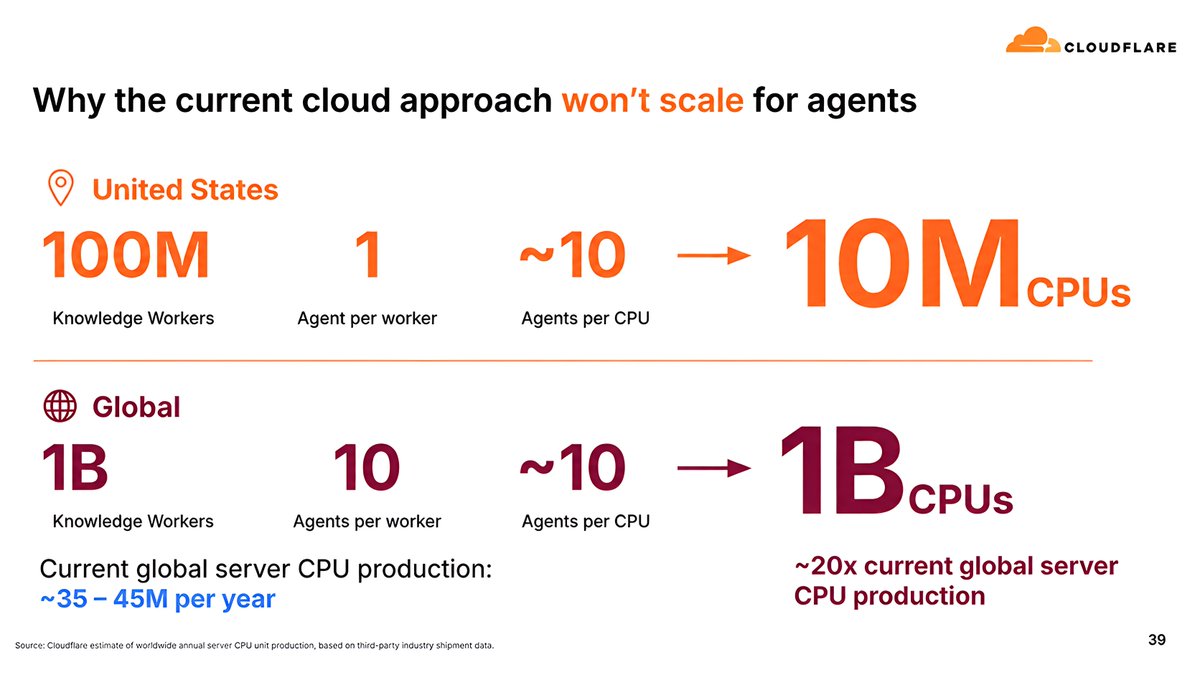

Cloudflare $NET believes CPU demand could 20x with AI agents

$AMD $INTC $ARM

The company argues that AI agents could create a massive CPU/server infrastructure problem if every worker runs multiple agents using today’s cloud model

The math:

US:

⏩ 100M knowledge workers × 1 agent each ÷ ~10 agents per CPU = 10M CPUs

Global:

⏩ 1B knowledge workers × 10 agents each ÷ ~10 agents per CPU = 1B CPUs

Cloudflare compares this to current global server CPU production of only ~35M–45M per year, implying the current approach could require ~20x current annual CPU production

$NET is pitching Agent Cloud as a solution

This is how it would work:

1. Dynamic Workers instead of full containers

Agents can be spun up on demand and put back into cold storage when idle, avoiding one heavy always-on container per agent

2. Durable Objects for state

Agents need memory/state for tasks, files, sessions, progress, and tool outputs. Durable Objects give each agent/app a stateful object with local SQLite-backed storage

3. Workflows for long-running agents

Agents may run for minutes, hours, or days while waiting for approvals, retries, external events, or scheduled steps. Dynamic Workflows allow these processes to hibernate between steps instead of constantly consuming compute

4. Project Think / Agents SDK

Project Think adds agent-specific primitives like durable execution, crash recovery, checkpointing, sub-agents, persistent sessions, and sandboxed code execution

5. Sandboxes only when full computers are needed

For coding agents or tasks requiring bash, git, file systems, browsers, or arbitrary binaries, Cloudflare still offers Sandbox containers. But the idea is to use them only when necessary, not as the default runtime for every agent

6

13

138

10,610