Professional-grade terminal, built by traders. Advanced execution, orders, and positions in one place. $850B in volume since 2021. Free to use.

Joined September 2021

- Tweets 1,248

- Following 172

- Followers 34,991

- Likes 3,874

410 Photos and videos

Pinned Tweet

Advanced server-side execution conditional orders are now live on Insilico Terminal 5.0!

Set the logic. Close the app. Execution keeps running.

19

27

261

54,606

Did you know?

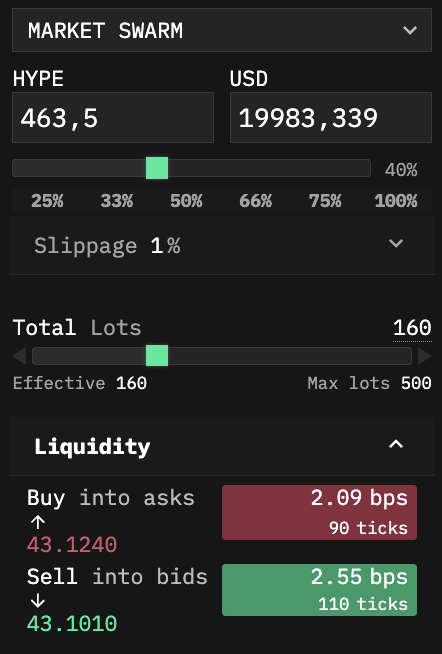

Before placing a Market or Swarm order, you can use the Liquidity option to see the estimated slippage in basis points.

Quickly check how much liquidity is available for your order size before executing.

4

3

35

2,250

“You got rugged by a sitting president.”

@Sellingvol on why the current crypto market feels so bad even after bouncing from the lows.

“Retail loves options when they don’t know they’re options.”

@Sellingvol joins the Insilico Terminal Podcast to talk about crypto options, market making, and why perps became the default product for retail traders.

We covered FTX, Deribit, Hyperliquid, prediction markets, structured products, vol selling, and why options can be both more powerful and more dangerous than perps.

00:00 Marty’s path from early Bitcoin to market making

06:17 Becoming a top FTX perps and spot market maker

12:00 Why crypto options are still behind perps

16:17 How institutions use structured products

20:31 Why DeFi options struggled and what changed

25:03 Prediction markets, binary options, and retail gambling

30:37 Better ways to express directional trades with options

37:51 Surviving 10/10, volatility spikes, and exchange outages

43:14 Why Marty is skeptical about the current crypto market

52:01 Bitcoin’s narrative problem and what could bring it back

2

1

21

4,864

Insilico Terminal retweeted

Jun 12

guy who has motion

15

7

155

10,629

Insilico Terminal retweeted

Jun 11

⚠️ Scheduled maintenance

We will perform a one-time migration this Saturday at 3:00 AM CET.

Expected downtime is around 15 minutes, but services may be affected for up to 1 hour.

Hyperliquid server-side execution / Cortex will be unavailable during this time. Conditional orders that trigger during the window may not execute.

4

12

1,935

Hyperliquid Prediction Markets (HIP-4) are now live on Insilico Terminal.

Trade the World Cup Winner and all other outcomes with the same advanced order types and execution workflow you already use for perps.

One terminal for every market on @HyperliquidX.

16

11

123

13,959

Rewards on every World Cup market. Win or lose.

Your group chat takes finally have EV.

x.com/Outcomexyz/status/2064…

Jun 10

Here we go!

Every World Cup Market pays. Win or lose.

$60K rewards, up to $3k distributed daily to traders in USDC. 3x rewards boost during live play.

The Outcome is inevitable.

2

1

23

2,455

2

39

3,591

Welcome home

Jun 10

Man @InsilicoTrading terminal where the fuck have you been all my life.

7

6

165

5,392

Trading options can get as complex as you want.

You can have a PhD-level model and still lose money.

@Sellingvol explains why pricing options is only one part of the game.

“Retail loves options when they don’t know they’re options.”

@Sellingvol joins the Insilico Terminal Podcast to talk about crypto options, market making, and why perps became the default product for retail traders.

We covered FTX, Deribit, Hyperliquid, prediction markets, structured products, vol selling, and why options can be both more powerful and more dangerous than perps.

00:00 Marty’s path from early Bitcoin to market making

06:17 Becoming a top FTX perps and spot market maker

12:00 Why crypto options are still behind perps

16:17 How institutions use structured products

20:31 Why DeFi options struggled and what changed

25:03 Prediction markets, binary options, and retail gambling

30:37 Better ways to express directional trades with options

37:51 Surviving 10/10, volatility spikes, and exchange outages

43:14 Why Marty is skeptical about the current crypto market

52:01 Bitcoin’s narrative problem and what could bring it back

2

2

28

3,208

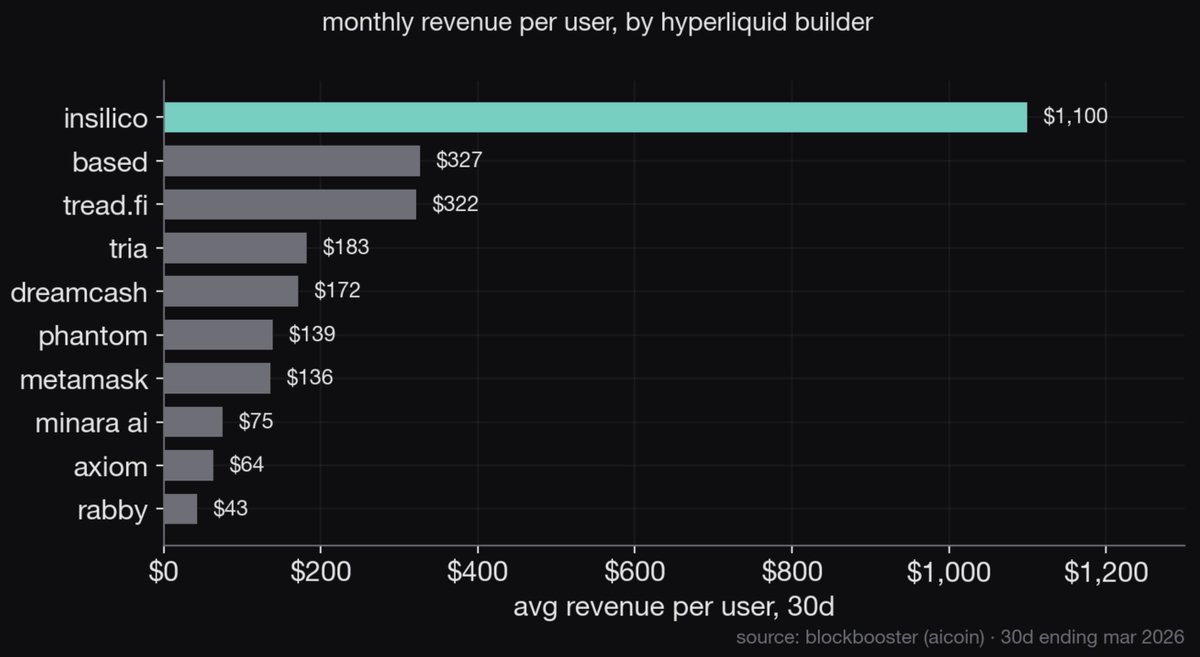

There is no second best

Jun 8

The most profitable hyperliquid frontend per user isn't Phantom, isn't Based, isn't pvp.

It's insilico. $1,100 per user per month at a 0.01% fee.

Axiom charges the same 0.01% fee and makes $64/user.

One's a retail brokerage, the other is a hedge-fund terminal.

4

15

190

25,682

Insilico Terminal retweeted

Jun 8

🔧 Insilico Terminal Updated v5.2.5

Added:

✅ WalletConnect integration for hardware wallets

✅ Tangem wallet support via WalletConnect

Fixed:

☑️ OKX regional domain connectivity for EU/EEA and US accounts

☑️ Privacy mode fuzzy entry and last price display

☑️ Mobile position action drawer applying actions to the wrong position

2

17

1,432

Insilico Terminal retweeted

Jun 5

Great episode with @Sokio8D and @Sellingvol.

Appreciate the s/o.

Full disclosure, we bribed @Sellingvol with a funded account (which he 3x'd in two days by the way).

Recommend you listen to the whole thing.

Below are the intern notes for future reference:

---

The core tension in crypto options is that retail wants simple red/green directional gambling (perps, binary options, zero-DTE) while institutions want structured products (principal protected notes, barrier options) — and the market is not mature enough to serve either group well. "Retail likes clicking red or green up down. They don't care about Greeks." A retail user can deposit $1,000 on Hyperliquid, use 10x leverage, and trade with a spread of one cent. Options have a $500 spread, and even if you are directionally right, a vol crush can turn a win into a loss. On the institutional side, TradFi wants complex multi-leg payoff structures they can block trade in size. Crypto earn products masquerade as no-fee products but the exchange takes 60-70% of the premium. The gap between these two poles is why options volume is still 1% of perp volume.

The "vol is meant to be sold" thesis is correct in the long run — as the market matures, more players sell structures and dampen vol — but the Turkey Chart shows that 2 months of losses can wipe out 22 months of gains, and when vol compresses into the 30s, a spike to 80-100 vol inevitably follows and destroys the complacent. Back-test selling 10-delta calls for two years yields 22 profitable months and 2 losing months, and those 2 months erase everything. The 1010 event is the textbook example. Vol was compressed. Then Bitcoin dropped ~$14k in a day. Over 200 people blew up on Deribit alone. "APIs went down, Binance API went down, Deribit — we have a collocated server and we couldn't reach it. If you can't delta hedge and the APIs are down, you implode." Anecdotal chatter said one of the biggest players on a major exchange lost hundreds of millions or billions in that single day.

DeFi options failed initially because requiring 100% collateralization to sell premium was capital-inefficient to the point of absurdity — the fix is a hybrid onchain/offchain model with portfolio margin, which is finally arriving in 2026. "When Bitcoin's $100,000 and I want to sell one contract and make $200 in premium, I have to post $100k to make $200. It makes no sense." The new generation (Derive, Cayenne, and others) runs the risk engine offchain because it is not possible to run portfolio margin calculations onchain, then settles onchain. Portfolio margin lets multi-leg strategies offset each other and actually gives more leverage than perps if used correctly. Deribit has had this for years, but DeFi options are just now catching up.

Deribit controls 70-80% of crypto options volume, and 70-80% of that volume is institutional — leaving a wide-open niche for small market-making teams to operate on smaller exchanges and protocols where the spread is fat and the big shops do not bother to compete. Marty's team is four people. "We swim in this niche pool of capital where maybe the big shops it's not worth their time to do it. We'll market make a smaller exchange or a smaller protocol or get these crazy DeFi incentives. If we make $100k in a month, that's insane to us, but to the big shop, that's not enough." Deribit's SMA (separately managed account) program only has about 10 firms on it. The options space overall is "still so new that you still have opportunity for the space to grow."

Bitcoin is in a narrative crisis — it was supposed to be digital gold but gold rallied while BTC stayed flat, it was supposed to be tech beta but tech rallied while BTC stayed flat, and the strategic reserve narrative was priced in as a buying program when in reality it was just consolidating existing government holdings under the Treasury. "Bitcoin is a chameleon. Risk asset, digital gold, inflation hedge. Every narrative, we change. Then the narrative runs out." BTC has been in the same ~$70-100k range for two years. "We priced in a strategic reserve that never meant buying with taxpayer money — it meant they would take crypto scattered across agencies and put it under the Treasury. That's it." Saylor is the marginal buyer and "everyone laughs at him when it's down, but if he's right and Bitcoin goes to 200k, nobody will be laughing."

ETH has been flat at ~$2,100 for 5 years — Marty shared an anecdote of an ETH maxi friend in Rio who is a VP of engineering at a major crypto company, only holds ETH, and is flat or under on every buy captures the grim reality that all the institutional building on Ethereum has not translated to price appreciation. "If everybody is building on ETH and wants to build on ETH, then why isn't the price up? Because we don't need the price to go up for people to build on ETH. We actually need it less — gas needs to be near zero, which means ETH is worth less." He contrasts with a simple alternative: Brazil's Selic rate has been 15%, and the BRL depreciated 20% against the USD in the last year, meaning holding dollar-based assets returned 20% from currency alone plus 15% from rates. "That was one of the greatest trades I've ever taken in a forex kind of situation."

On Hyperliquid, Marty went from critic to believer — 11 people making a billion dollars with a cult following and a working product — but the regulatory risk is existential when the US administration changes in 2028. "I was a big critic. The features were kind of bad. They did maintenance during FOMC and CPI. But now the product works. They have $2B Bitcoin open interest vs OKX at $3B. They are not a small player anymore." The risk is enforcement — "when you get too big, you are a target. We saw it with BitMEX, with Luna." What if the US says "we're done"? Hyperliquid is the target now. "I feel like we have until Trump isn't president anymore. If we get a Democrat in 2028, it might all be over."

The simplest way for a retail trader to express a directional view in options is a call spread, not an outright call — because the spread caps theta decay and creates a defined-risk payoff that actually works if the trader is right, whereas an outright long call into an event is "thanks for the donation to the Marty fund." "If you buy the 77 call and sell the 78 call, and it's above 78, you make money. Max profit is $1,000. It probably costs $400-500. You doubled your money. If you bought the outright 77 call, now you have theta decay and you were right directionally but still lost because vol crushed." The caveat: this is not a scalable strategy, and the vol selling dynamic means there will always be losing months that wipe out the winners. "It's not as easy as people want to make it out to be."

“Retail loves options when they don’t know they’re options.”

@Sellingvol joins the Insilico Terminal Podcast to talk about crypto options, market making, and why perps became the default product for retail traders.

We covered FTX, Deribit, Hyperliquid, prediction markets, structured products, vol selling, and why options can be both more powerful and more dangerous than perps.

00:00 Marty’s path from early Bitcoin to market making

06:17 Becoming a top FTX perps and spot market maker

12:00 Why crypto options are still behind perps

16:17 How institutions use structured products

20:31 Why DeFi options struggled and what changed

25:03 Prediction markets, binary options, and retail gambling

30:37 Better ways to express directional trades with options

37:51 Surviving 10/10, volatility spikes, and exchange outages

43:14 Why Marty is skeptical about the current crypto market

52:01 Bitcoin’s narrative problem and what could bring it back

2

11

35

4,439

“Retail loves options when they don’t know they’re options.”

@Sellingvol joins the Insilico Terminal Podcast to talk about crypto options, market making, and why perps became the default product for retail traders.

We covered FTX, Deribit, Hyperliquid, prediction markets, structured products, vol selling, and why options can be both more powerful and more dangerous than perps.

00:00 Marty’s path from early Bitcoin to market making

06:17 Becoming a top FTX perps and spot market maker

12:00 Why crypto options are still behind perps

16:17 How institutions use structured products

20:31 Why DeFi options struggled and what changed

25:03 Prediction markets, binary options, and retail gambling

30:37 Better ways to express directional trades with options

37:51 Surviving 10/10, volatility spikes, and exchange outages

43:14 Why Marty is skeptical about the current crypto market

52:01 Bitcoin’s narrative problem and what could bring it back

11

8

58

17,499

YouTube: youtube.com/watch?v=xVlg96ka…

Spotify: open.spotify.com/episode/4OP…

Apple Podcasts: podcasts.apple.com/us/podcas…

1

13

1,731

Insilico Terminal retweeted

Lastly, we're glad to announce HypurrCo Gathers @ Token 2049 last and final title sponsor - @InsilicoTrading

Insilico Terminal is a professional-grade trading terminal for Hyperliquid power users and active crypto traders, with more than $800 billion in cumulative trading volume since 2021. The platform supports @HyperliquidX and other leading digital asset exchanges and is free to use.

📅 Oct 8th, 11AM - 3PM.

Singapore.

Save the date!

RSVP and meet the @InsilicoTrading team here: luma.com/mmrfj0pz

3

3

66

9,554