Everything on Japanese Culture & Investing 🌱 Local market insights 🗺️ Quality 📈 Hidden Gems 🔍 Unique mental models 🧠 Views my own. Not investment advice.

Joined March 2023

- Tweets 5,241

- Following 987

- Followers 11,892

- Likes 9,197

749 Photos and videos

Pinned Tweet

Apr 19

The First episode of the Made in Japan podcast is finally out. (Link in reply)

We felt our interview with Philip was going to be the perfect first episode as an introduction to Japanese markets.

Over the last 2 decades, he’s seen the country as a lawyer, investment banker and now an investor. He’s worked with truly the pioneers of Japanese activist investing like Yoshiaki Murakami of M&A Consulting and Seth Fischer of Oasis.

Through his adventures not just in Japan but in East Asia, he has so many interesting stories to tell!

We learnt

⚪︎Why Activism Struggled in the past and why that’s changing

⚪︎Why Activism, and Japan, is still a huge opportunity today

⚪︎Some of the misconceptions of Activism

⚪︎Japan’s unique business culture and how Japanese companies think about M&A

⚪︎And some of his favourite things to do in Japan!

We still have alot to improve on so we’d love to hear your feedback, thoughts or suggestions if you have any!! Or even any guests that you’d want us to interview!

We hope you enjoy this conversation. If you liked it and want to hear more, we would really appreciate it if you like this post, retweet, and subscribe!

Thank you for your interest and support ♥️🎌

Finally a special thank you to the people around us who’s been so encouraging and supportive for this project. Ben and I still have no idea where this’ll go but we hope to bring some unique perspectives!

5

13

86

40,559

Jun 13

Friend showed me this a while back. Overwhelmingly the current infrastrcuture is in the US.

Makes you think in the context of AI sovereignty...

1

9

1,640

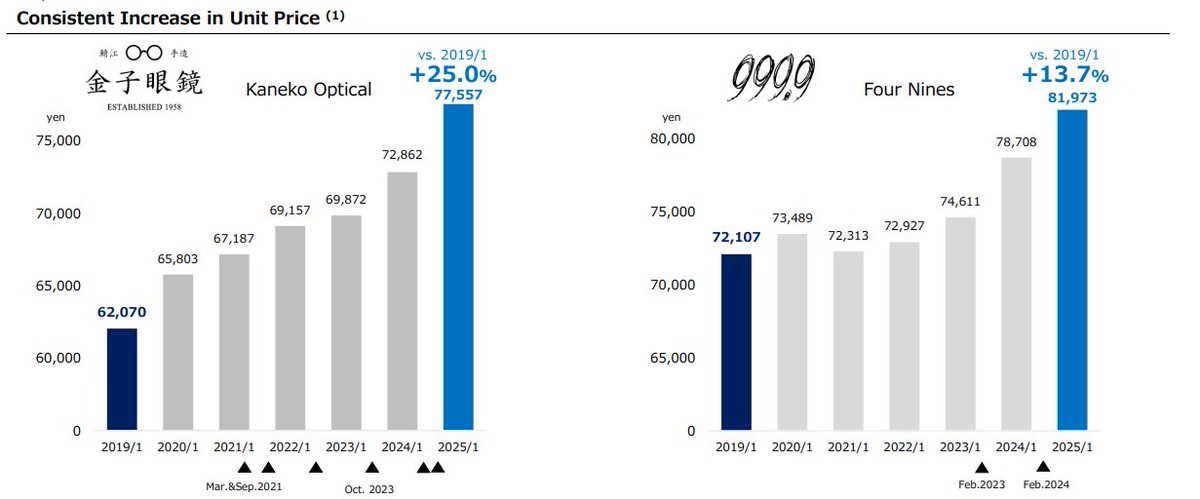

Jun 13

JEH's Q1 results looked good. Revenue 15.8% and Operating profit 28.5%.

And as suspected so far $5889.JP is showing "No China, No Problem" with any of the meaningful impact being completely offset by visitors from HK, S.Korea and Taiwan. Inbound sales is Growing 14.7% so pretty much in line with the rest of the company.

Still trades at what I think is a cheap valuation.

Disc: I own.

13 Mar 2025

Since @MikeFritzell mentioned..

JEH has gone through a lot of unnecessary Drama lately but they took it on the chin and handled it well.

Company Q4 results were a banger.

Q4 revenue: 19%

EBITDA: 31% (Margin 40.5%!)

Company continues to exhibit incredible pricing power in line with their strategy. I continue to like this name as a unique expression of the Japan opportunity!

Guidance was the wildcard given the new factory but looks like they'll continue to deliver mid-teens growth - which is in line with my expectations. Continues to be a 'long term earnings compounder' type biz for me.

Insanely strong inbound tourism may be potential upside??

Valuation gap vs EssilorLuxoticca also still huge. Despite that I think JEH is still early.

JEH : 8.7x

$EL: 17.8x

And you know which products I prefer!!

Disc; Long

1

13

3,347

Jun 13

I have no strong opinion valuation but you can’t deny what Elon has done for human progress.

And even in Japan you can get some indirect exposure to $SPCX! Did you know Meiko electronics apparently makes high density substrates for Starlink? It’s 3xed since this tweet tho 😂

20 Dec 2024

An interesting business that started running up in the last years is Meiko Electronics $6787.JP . A top manufacturer of Printed Circuit Boards (PCB) in Japan. They also make semiconductor package substrates where they are one of the few in the world to be able to mass produce high density substrates.

End market is pretty diversified but they've recently seen an accelerated contribution from a 'satellite communication customer' which the company doesn't confirm but is widely believed to be Starlink.

Pretty cool that you can get exposure in things like that in the public markets if you know where to look (I didn't lol). Japan houses many such component manufacturers. Some potentially to crucial tech in the world.

PER 14.8x and EBITDA 9.3x

23

3,835

Jun 12

Everyone has a short memory of being short memory and a long memory of being long memory

4

1,208

Jun 11

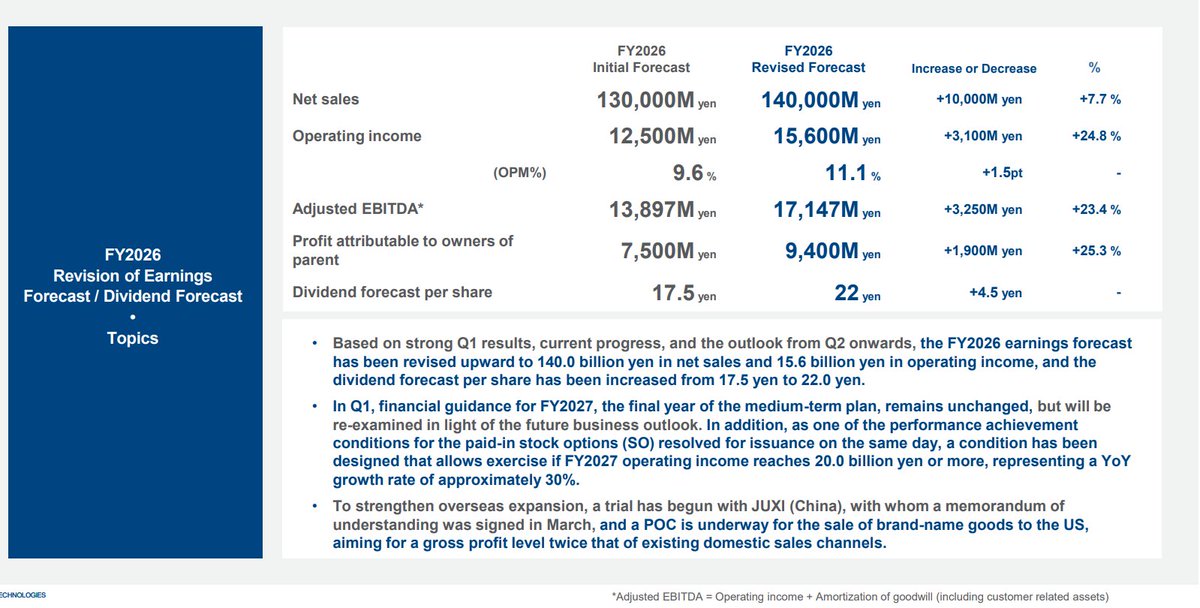

Remarkable, I am down on this name since i wrote abt it. Seems like this is only correlated to AI stocks on the downside 😂

I still think the market is sleeping on fundamentals, notice that their new slides also includes new customers never mentioned before like Santec.

Mar 25

New write up!

A few days ago I wrote about my new long position Ebrains.

Trades at 3x EBIT.

- sells mission critical products

- high switching costs, many are customers for decades

- the # of players that can do this have reduced significantly over the last decade

- exposed to key sectors for 🇯🇵 and is set to accelerate

- as a result theres operating leverage potential mix improvements

- 60% of market cap in cash

- their IR deck looks like it was made 20 years ago (🔥)

- under the radar and no english IR. Their english website was last updated in… 2003!

What I liked is that it’s set to benefit from not just 1 but 3 major sectors: semis, defense and power. due to it’s position in the supply chain, the huge capex into semis hasn’t shown up yet on the PnL but my bet and the main catalyst is that its going to accelerate in a 12 month time frame.

I guess one comp in the US is nVent $nvt though this is much smaller.

TLDR:

If you sell mission critical products to 3 industries seeing major tailwinds and your customer base looks like this, i’m not sure 0.9x book or <5x FCF makes sense.

Find it in the usual place.

This is not a recommendation, please do your own due diligence!

1

12

3,726

Jun 10

This is a fascinating insight in the context of Japan:

“That is a risk with AI, in that these big companies are very security-conscious and can be slow to move.

There are a lot of cultural issues with AI, where you really need a few evangelists to push it through.

The top management needs to push it through, but then IT is saying this is risky. And that happened with cloud too.”

In the sense that the big companies in Japan are even Slower, and because many companies lack IT engineers, there aren’t even evangelists on the client side to push it.

So you end up with this idiosyncrasy where friction for corporate adoption of AI is going to be very slow (and therefore relatively more insulated) yet you’ll find some of the cheapest software companies in the world.

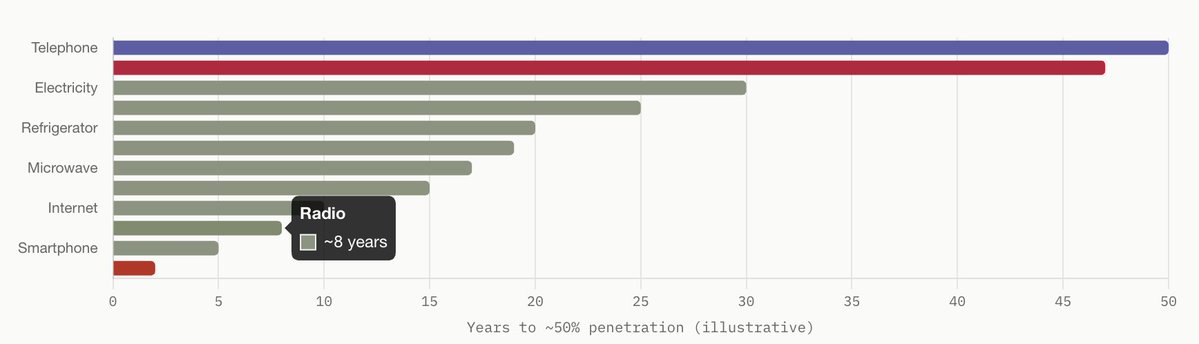

Fascinating that the radio is the third fastest technology in history to reach 50% penetration

It spread faster than the internet (only AI and the smartphone beat it)

But the dishwasher took 47 years

I loved Alex's analogy for the two models of adoption, the radio and the dishwasher:

"We commissioned Horace Dediu, who used to work with Clayton Christensen, to go look at S-curves over the last 100 years.

The radio S-curve is one of the fastest ever. But the dishwasher S-curve is the opposite, because it needs to be plugged into the back end.

B2B stuff can take a long time, because it needs to be plugged into the existing systems. Consumers generally tend to go a lot faster.

I covered B2B internet at Fidelity.

The underlying infrastructure wasn't in place for B2B to happen. It ultimately happened 20 years later, with SaaS.

That is a risk with AI, in that these big companies are very security-conscious and can be slow to move.

There are a lot of cultural issues with AI, where you really need a few evangelists to push it through.

The top management needs to push it through, but then IT is saying this is risky. And that happened with cloud too.

Everybody was afraid that it's not secure to have your data in the cloud. And then we saw the CIA do it, and we saw Capital One.

We talked to the Capital One CIO, who said it's more secure in the cloud. And then it really started to take off.

But what's amazing about AI is that you just open up the browser and it's there. And so that's why we're getting this straight up, we call it the backwards L-curve."

1

5

2,340

Jun 10

Last 10 years of Japanese 10 year treasuries, what a chart...

1

6

2,347

Jun 10

Fascinating data points in the fintech space, Stripe in Japan did ¥49.5bn in revenues and ¥0.98bn in Operating Profit.

For comparison GMO Payment Gateway $3769.JP did ¥82bn in revenue and ¥31.4bn and OP last year.

Huge margin difference may be bc Stripe revenue is ‘gross’ vs Net. (For comparison GMO’s online GMV is ¥13.1trn)

Jun 10

決済・金融プラットフォームなど「Stripe」日本法人 ストライプジャパン 決算公告(第12期) kanpo-kanpo.blog.jp/archives…

第12期 決算公告

売上高:495億6707万円

売上総利益:59億2768万円

営業利益:9億8490万円

経常利益:6億4080万円

純利益:3億4869万円

利益剰余金:11億575万円

1

2

11

4,750

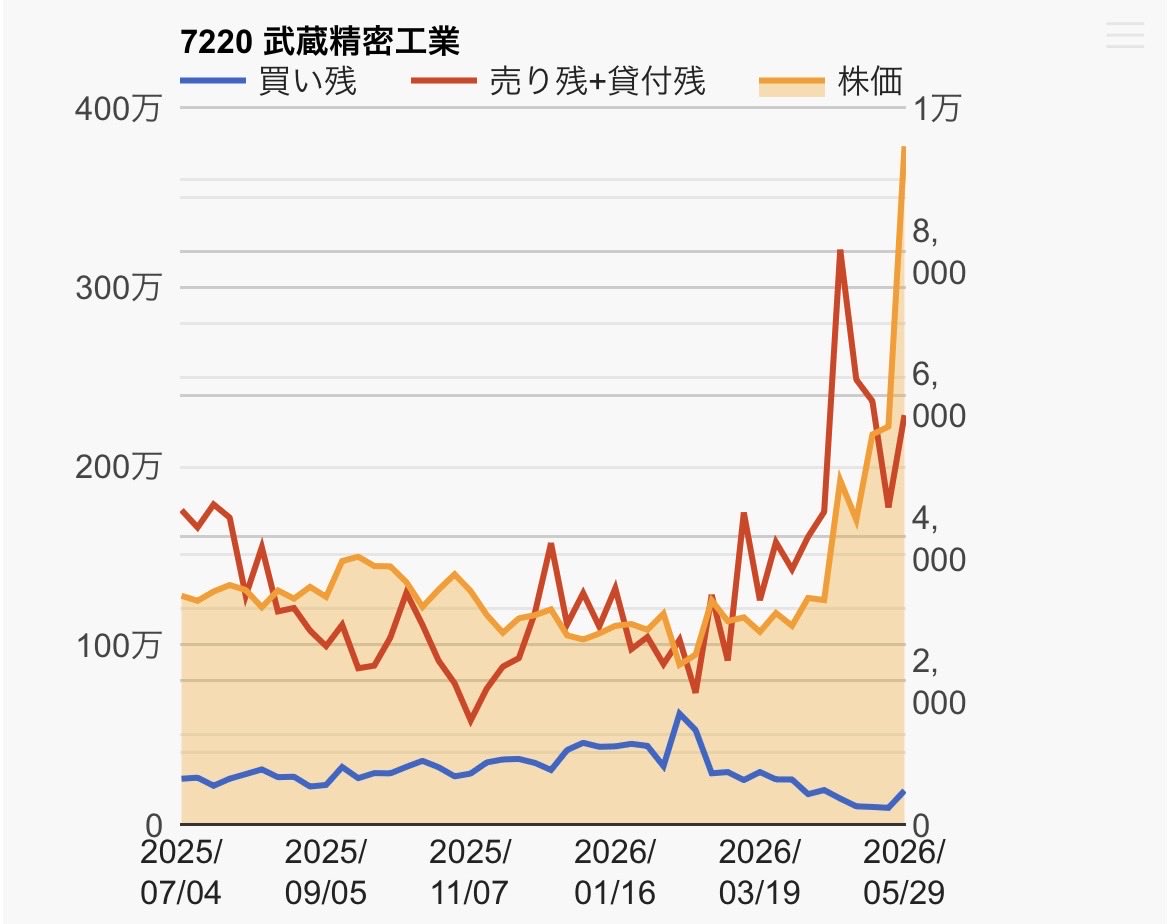

Jun 10

Still doesn’t change the fact I’ve missed a 100% run in 2 months but momentum in Japan can be scary!

Noting that there’s still an elevated level of margin shorts [red line] by retail (vs margin buys) so it could still rip…

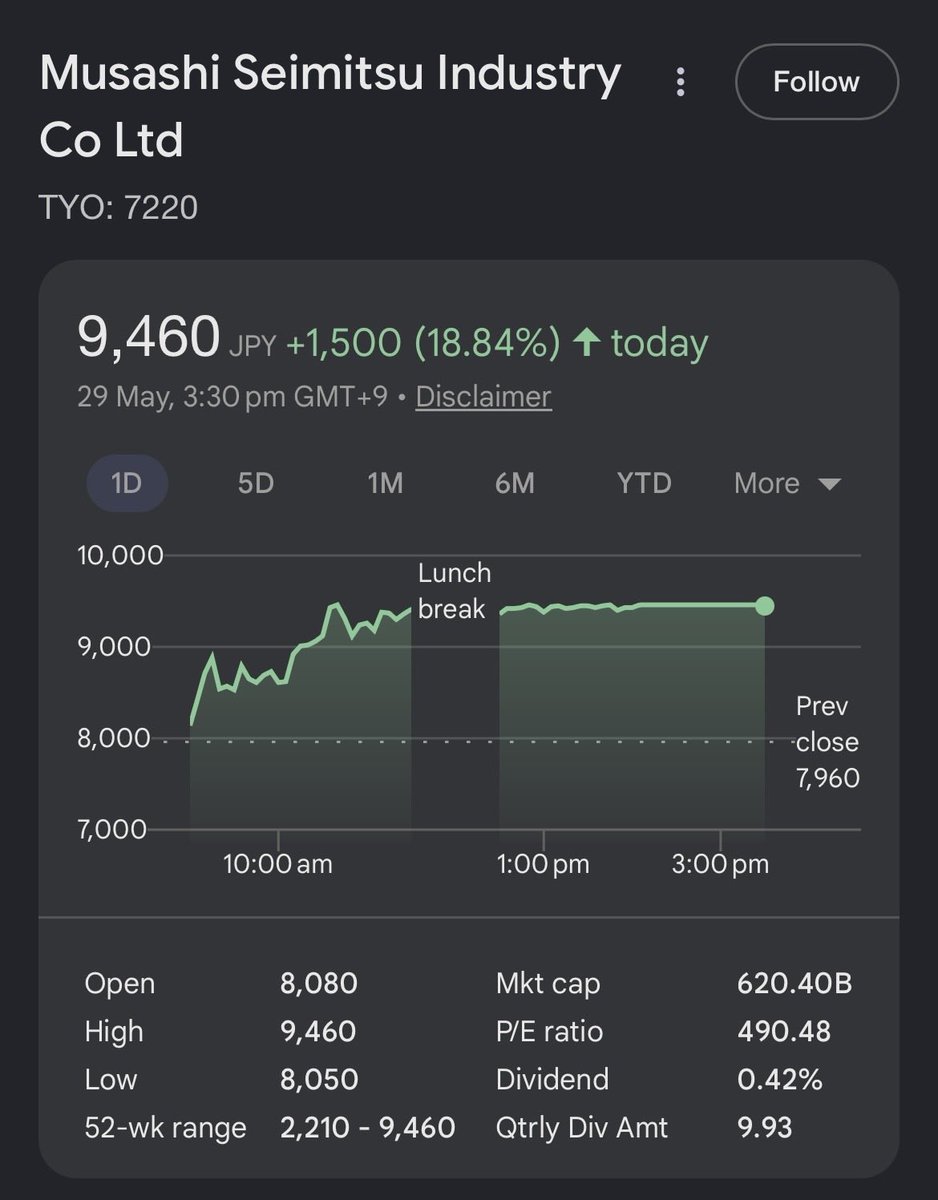

$7220.JP

1

7

4,362

Made in Japan 🇯🇵 retweeted

Jun 9

Bank of Japan set to hike rates to 1.0% s.nikkei.com/4g6E43Q

1

1

19

3,204

Now on vacation and Been reading the stock market wizard series of books. Was always on my list so not sure why it took so long. A new one came out recently too.

Far better than reading another value investing book tbh:

Some bangers:

On finding your own contra indicators, people that you listen and bet against: “he is wrong by such a large percentage than random that it’s hard to believe. I will never have a position on if he is recommending it”

4

29

3,884

On day traders after a significant drawdown:

Now, they are sitting on stocks that are down 70% or 80%. Suddenly they are not trading anymore; they are “investing”

😂😂😂😭

1

8

1,145

When the founder started this business with his winnings from Mahjong, one of the key concepts he ‘invented’ for the store was “high density store display” where you’re overwhelmed with a jungle of products at a bargain. Pure sensory overload. It’s like if a supermarket was on drugs.

That was the point, it created serendipity and became a treasure hunt for customers and they loved it.

Today its a ¥2.5trn company $7532.JP Pan Pacific Holdings.

Jun 8

I don’t get how this store works. But I doubt Americans are ready for this particular type of retail experience

29

422

36,902

One potential second order effect of this is going to be some offset of the negative stigma of Private Equity in Japan - which many JP biz owners prefer not to deal with. Not only will Bain get their accolades but I think the whole PE industry might after this behemoth.

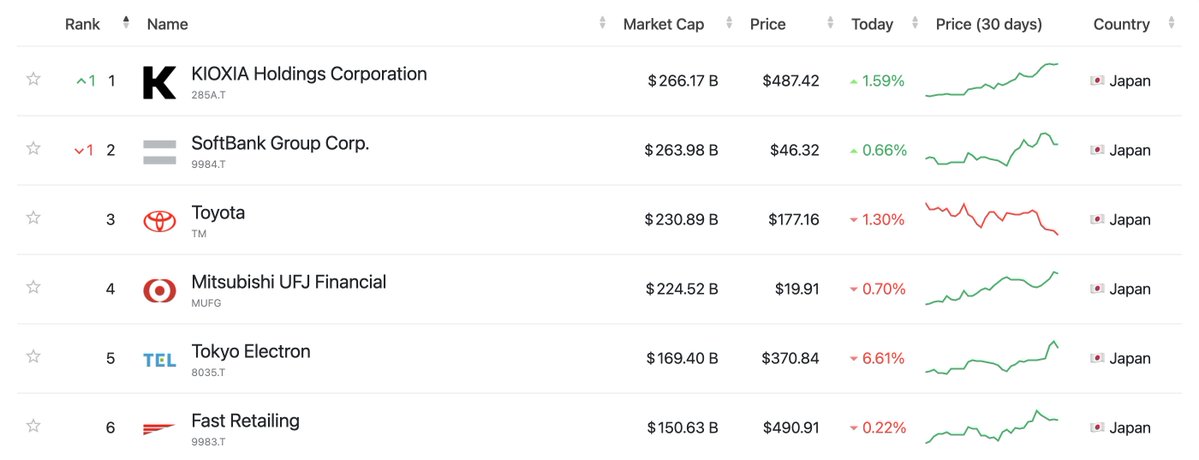

Kioxia has now become the company with the largest market capitalization in Japan.

8

4,482

100% @willschoebs was on the case early, and his write up on this is def worth checking out.

Jun 5

Most of what I see on my timeline these days is AI or 🇯🇵 defense tech…

I’d like to personally take credit for the 🇯🇵 defense tech wave, thank you very much 🤣

In all seriousness, exciting to see & necessary. Think there’s a lot more oppty & upside beyond the “tech” tho

5

2,161

Not to add fuel to the fire and still cautious but we might be surprised by how wildly off guidance is for some of the JP semicap names. Esp for downstream bizes.

Realise they usually make forecasts in Feb. Alot of the large orders came in March which is not accounted for!

1

7

2,037

Btw this divergence could go longer than people wish too, if the AI trade really has legs going out into 2030, I see a world where it's possible to get uber screwed for not having any exposure as well. I dunno. Investing is hard.!!!

May 29

I guess everyone is starting to see this but at least for the fund managers around me focused on Japan, quite consistently there's been a divergence in performance between those that are betting on AI and those that are not in recent months.

It's starting to remind me of 2024 where all the money and attention went to large cap value and some of the cheap growth names were left by the way side. It's not just institutions but retail which are the main constituents of small/micro caps that drove this.

Feels similar where all the attention/flows are going to AI at the moment. All the money/attention from retail are also moving to this theme. At least in years past, such trades in Japan can get crowded fast.

I also continue to have exposure into AI but increasingly more cautious, There are quite some non AI/Semi companies that are growing fast trading at single digit earnings, some even improving shareholder returns that's simply not getting as much attention.

1

9

3,214