Making sense of investing through visuals | Early $NBIS (10x), $AMD (5x) & $AXON (4x) | Not financial advice | Join 10,000 readers: investingvisuals.io

Joined May 2023

- Tweets 8,182

- Following 111

- Followers 113,743

- Likes 10,843

2,390 Photos and videos

Every Sunday, I send a newsletter for visual learners about various investing topics.

Tomorrow, it'll be a $SPCX special:

• How they make money

• Who owns it

• Thoughts about their IPO

And much more.

You can sign up for free via my bio or link in comments!

When (not) to buy $SPCX: four phases of the IPO playbook:

1 - PUMP

2 - DUMP

3 - DEAD MONEY

4 - REDISCOVERY

4

24

8,217

Newsletter for visuals learners: investingvisuals.io/

3

3,678

Honest question for $SPCX shareholders: what’s your bull case?

Let’s assume $SPCX delivers outstanding results and stock price followed fundamentals, with their multiple staying flat from current levels.

Let’s assume they become the biggest company in the world and overtake $NVDA.

That’s roughly a 2x from current levels, at best?

I think the upside from here is (very) capped and the easy money is already made by early investors (pre IPO), but curious to hear other opinions.

When (not) to buy $SPCX: four phases of the IPO playbook:

1 - PUMP

2 - DUMP

3 - DEAD MONEY

4 - REDISCOVERY

18

3

79

12,029

When (not) to buy $SPCX: four phases of the IPO playbook:

1 - PUMP

2 - DUMP

3 - DEAD MONEY

4 - REDISCOVERY

38

128

641

66,410

A more detailed breakdown:

Phase 1 – Pump: the stock gets hyped prior to the IPO to gain as much exposure as possible. Individual investors get dragged into FOMO.

Phase 2 – Dump: early investors sell as the valuation is elevated and there is a lot of euphoria. Selling pressure gradually increases as the hype wears off.

Phase 3 – Sideways: the stock goes nowhere because the smart money is out and the price drifts down to more reasonable levels; hype buyers sell at a loss to move on, adding further pressure

Phase 4 – Repricing: as the business continues to deliver, the risk reward becomes increasingly attractive, which is often the best time to buy, right before rediscovery starts.

Don’t be exit liquidity, be the smart money. History has shown that chasing hype is not a great strategy.

Credits to @moninvestor chart below, which inspired me to create this visual 👌

4

6

42

4,785

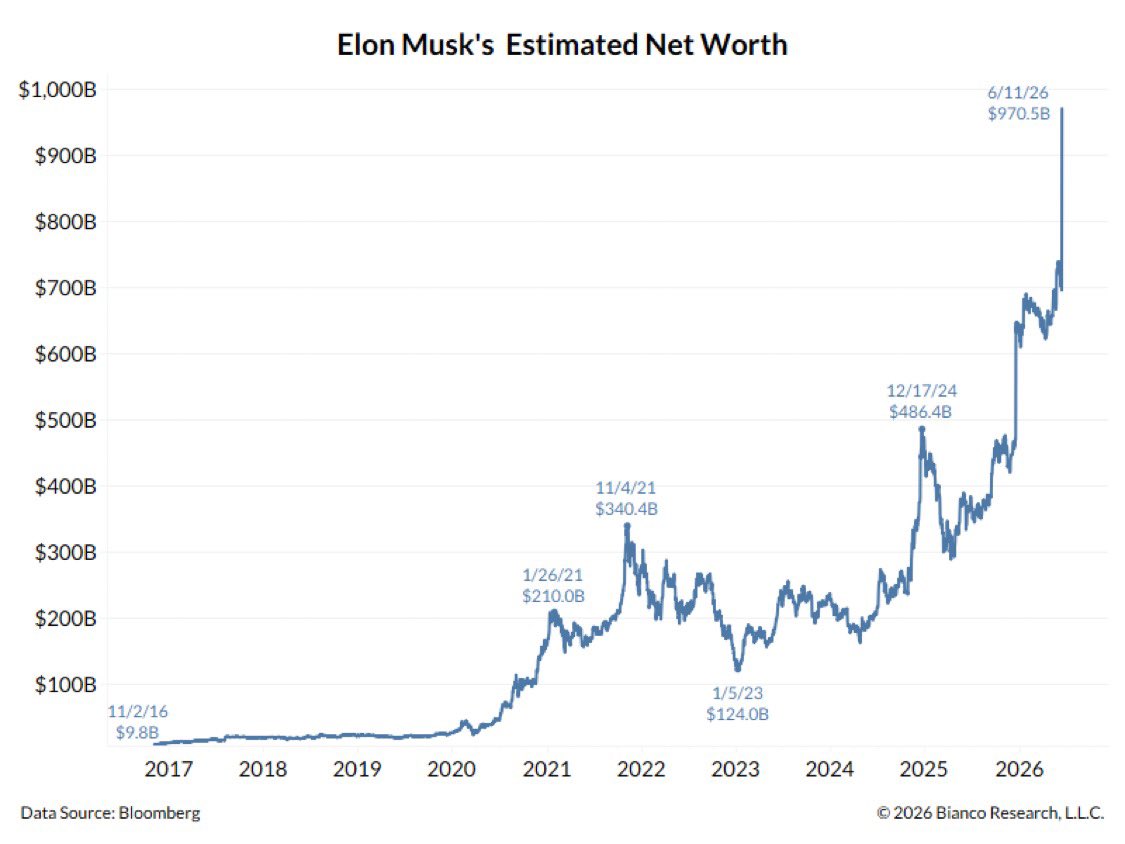

Elon Musk became the world’s first trillionaire today.

In 10 years, his net worth grew from $10B to $1000B 🤯

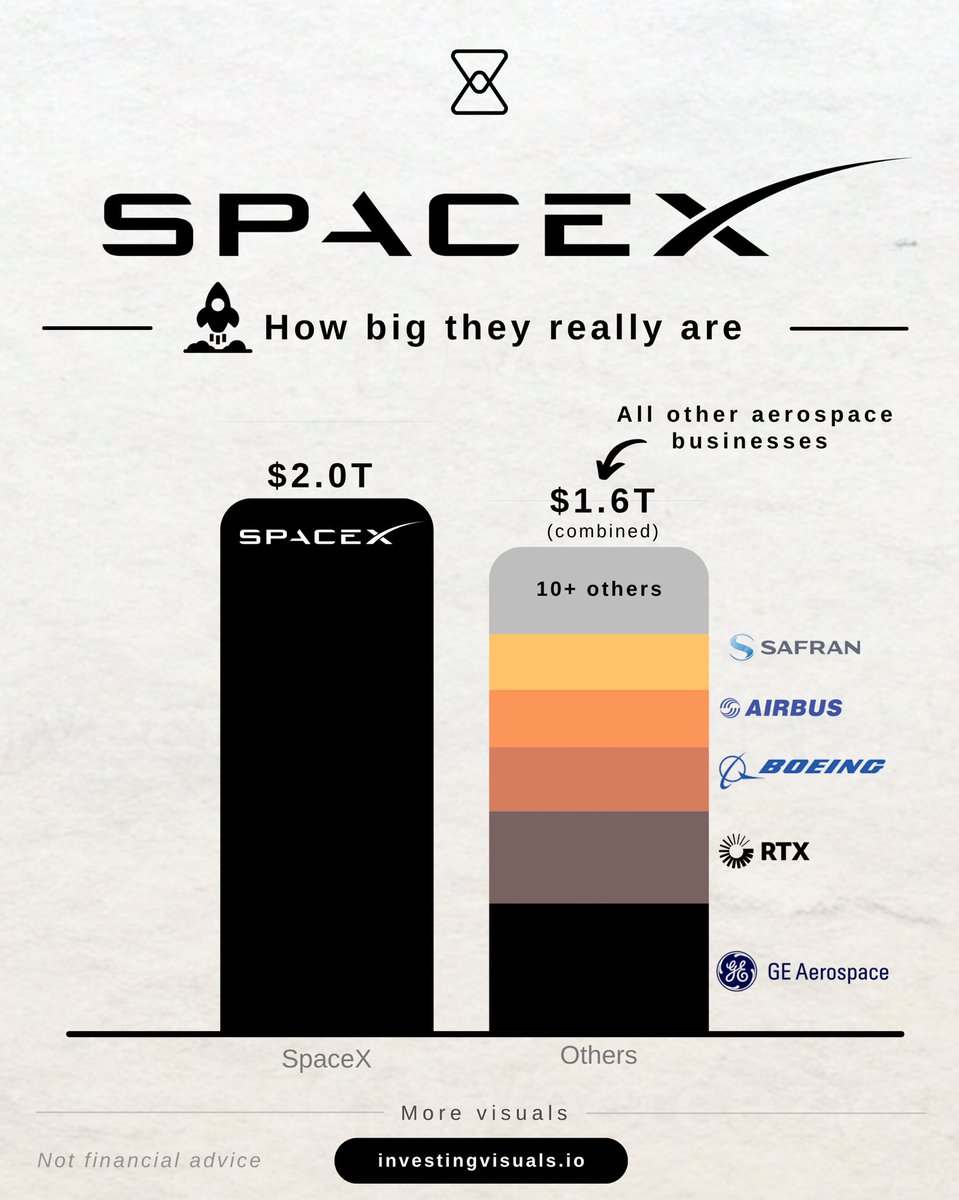

SpaceX is now worth more then all other aerospace businesses combined.

5

26

139

13,909

SpaceX is now worth more then all other aerospace businesses combined.

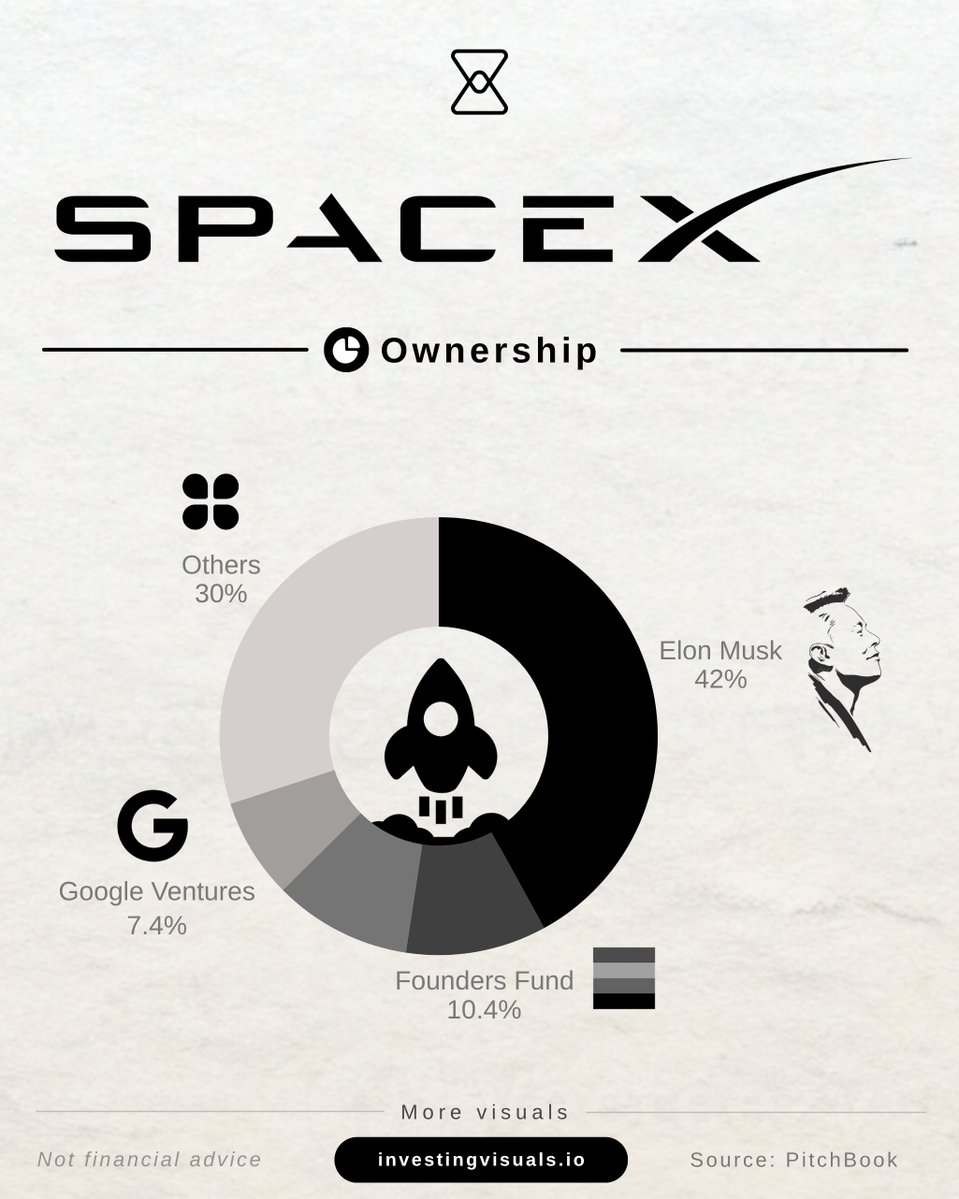

SpaceX will IPO in three days. Who currently own it:

• Elon Musk: 42%

• Founder Fund (Peter Thiel): 10%

• Google Ventures: 7%

• Others: 30%

13

95

631

49,901

Investing visuals retweeted

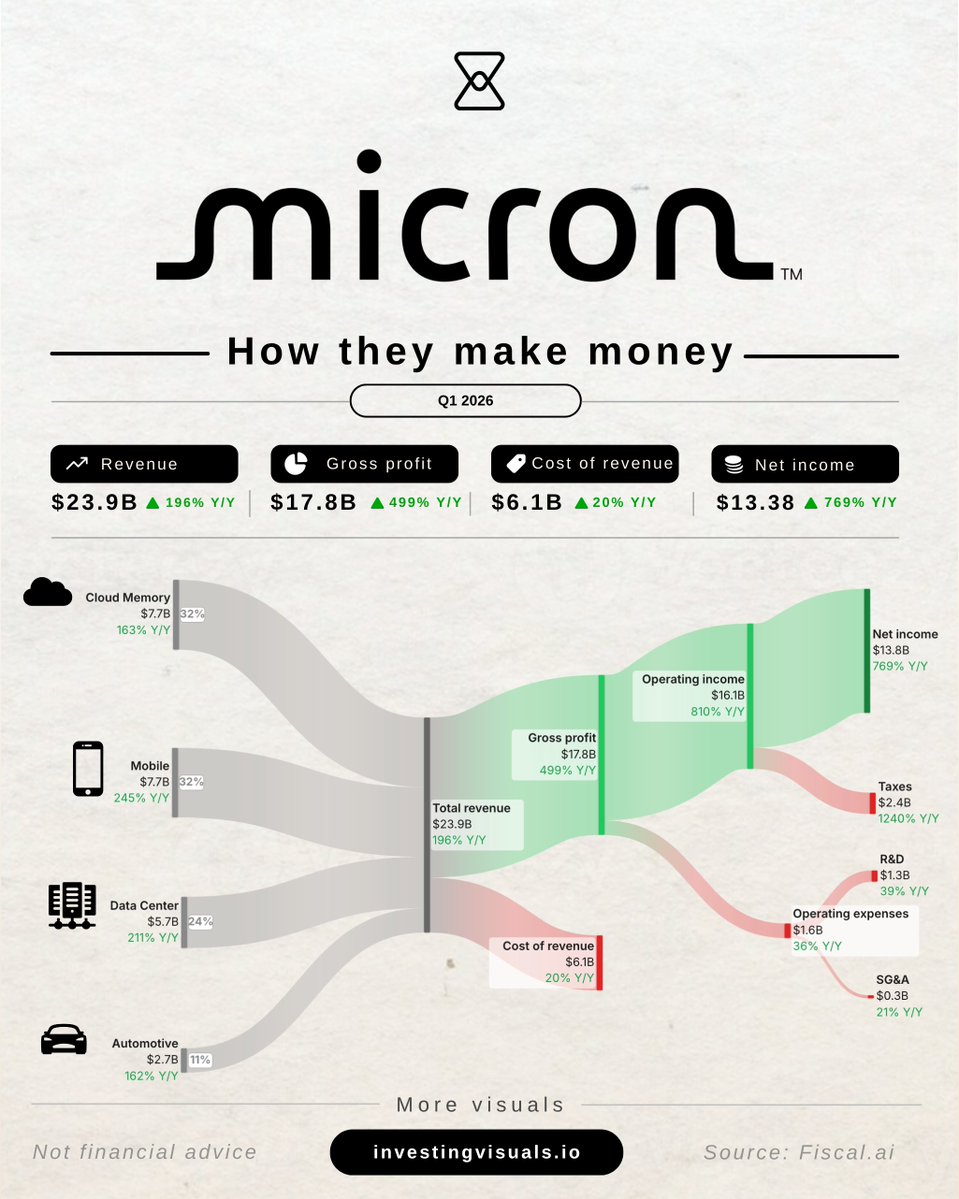

$MU net income growth is insane:

• Q1 2025: $1.5B

• Q2 2025: $1.8B

• Q3 2025: $3.2B

• Q4 2025: $5.2B

• Q1 2026: $13.7B

From $1.5B → $13.7B in just 5 quarters.

Three businesses control the entire High Bandwidth Memory (HBM) market:

• $HXSCL (SK Hynix, 61%)

• $MU (Micron, 21%)

• $SSNLF (Samsung, 17%)

Do you have a favorite?

29

114

869

188,682

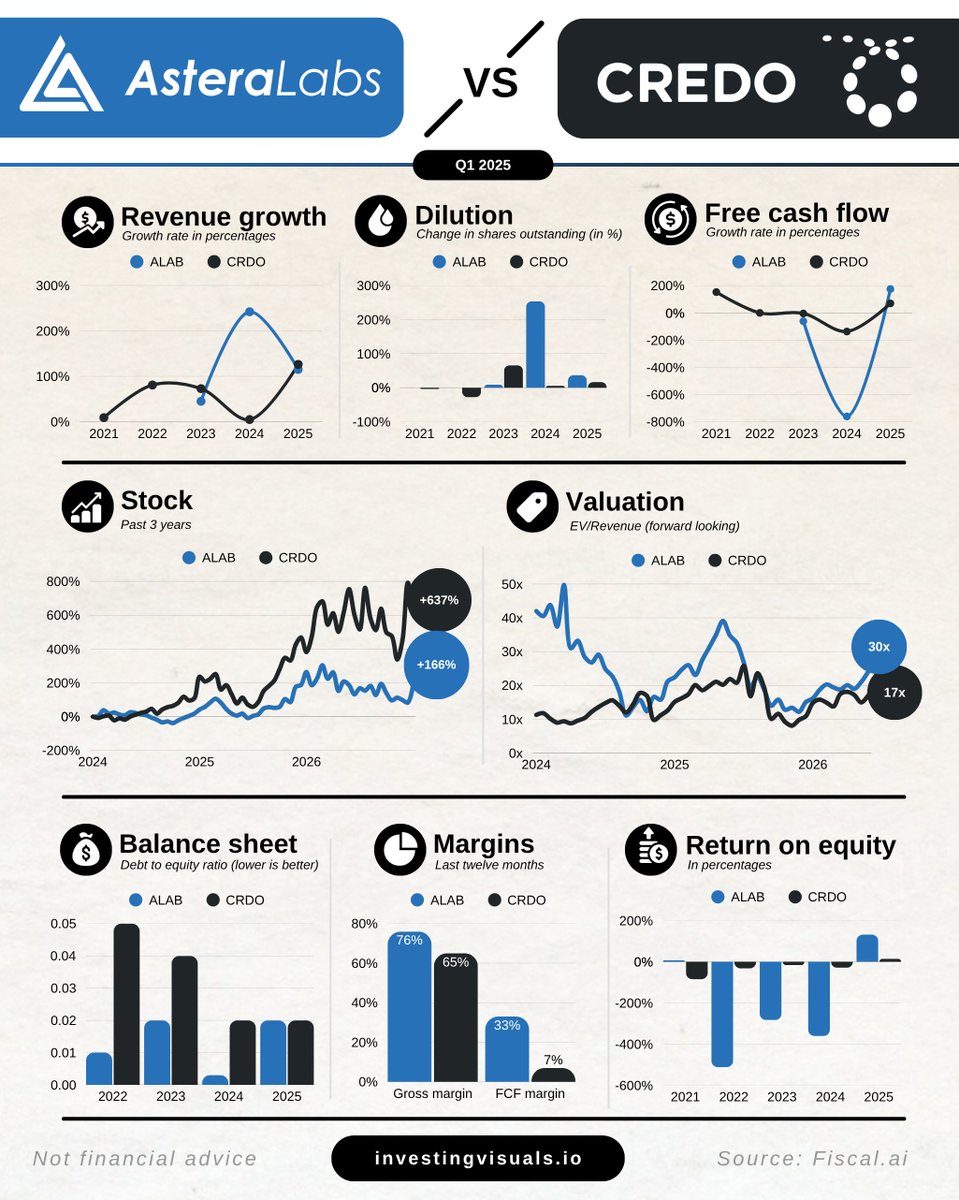

Just a few month ago, I added $ALAB to my portfolio as an underappreciated AI connectivity play.

It's now up 175%

I trimmed it down a bit lately, but along with $CRDO, it's still my favorite pick in the AI connectivity theme.

The latest addition to my portfolio: $ALAB - The ‘neural network’ of AI.

Great management team, critical AI infrastructure and reasonably valued after a 50% drop from it’s 52-week highs.

I recently created a deep dive about them, link in the comments!

6

10

45

11,759

Why I won’t buy the SpaceX IPO:

• Revenue grew only 15% in Q1 2026

• It has 23B in long term debt

• At a $1.75T valuation, it would trade at roughly 100x trailing revenue

At such a high multiple, with a sub optimal growth rate and a not so great balance sheet, I see very little upside.

There might be a short term pump, but I would not be surprised to see the stock move lower in the months and years ahead as the IPO is used as exit liquidity for early investors.

Additionally, 64% of IPOs underperform the market in the 3 years after going public.

So the odds are stacked against you when buying at IPO.

SpaceX will IPO in three days. Who currently own it:

• Elon Musk: 42%

• Founder Fund (Peter Thiel): 10%

• Google Ventures: 7%

• Others: 30%

36

25

149

25,484

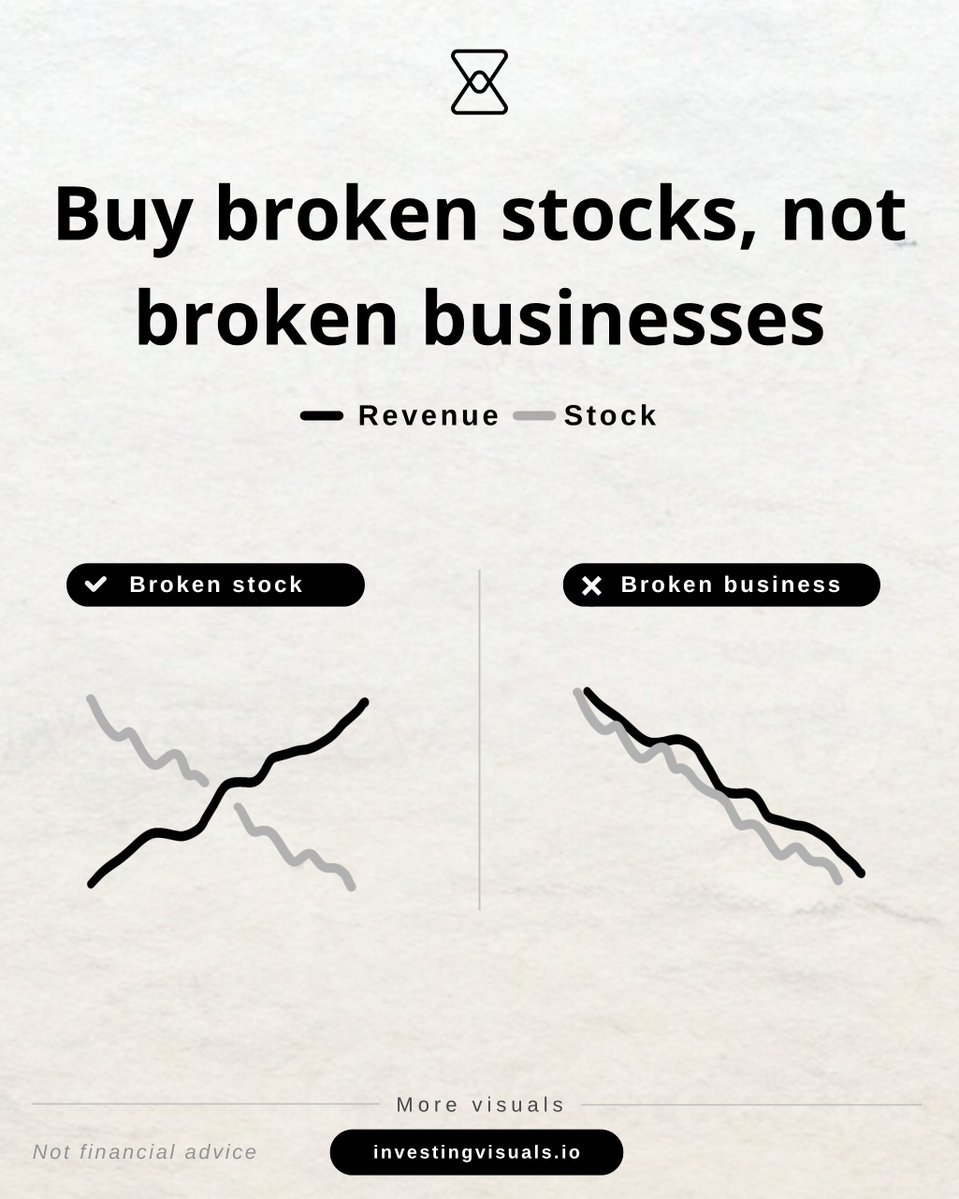

Stock price can be a very powerful driver of narratives.

Interestingly, the stock market is the only place where people get excited when prices go up and stressed when they drop.

Don’t let stock price fool you.

Stock prices and business fundamentals can diverge in the short term. Over the long term, they always follow fundamentals.

19

13

59

5,967

SpaceX will IPO in three days. Who currently own it:

• Elon Musk: 42%

• Founder Fund (Peter Thiel): 10%

• Google Ventures: 7%

• Others: 30%

37

102

702

98,491

$MU net income growth is insane:

• Q1 2025: $1.5B

• Q2 2025: $1.8B

• Q3 2025: $3.2B

• Q4 2025: $5.2B

• Q1 2026: $13.7B

From $1.5B → $13.7B in just 5 quarters.

Three businesses control the entire High Bandwidth Memory (HBM) market:

• $HXSCL (SK Hynix, 61%)

• $MU (Micron, 21%)

• $SSNLF (Samsung, 17%)

Do you have a favorite?

29

114

869

188,682

If you like these visuals, you can find 20 others including $NVDA, $SNDK, $AMD here:

investingvisuals.io/tag/how-…

5

4,565

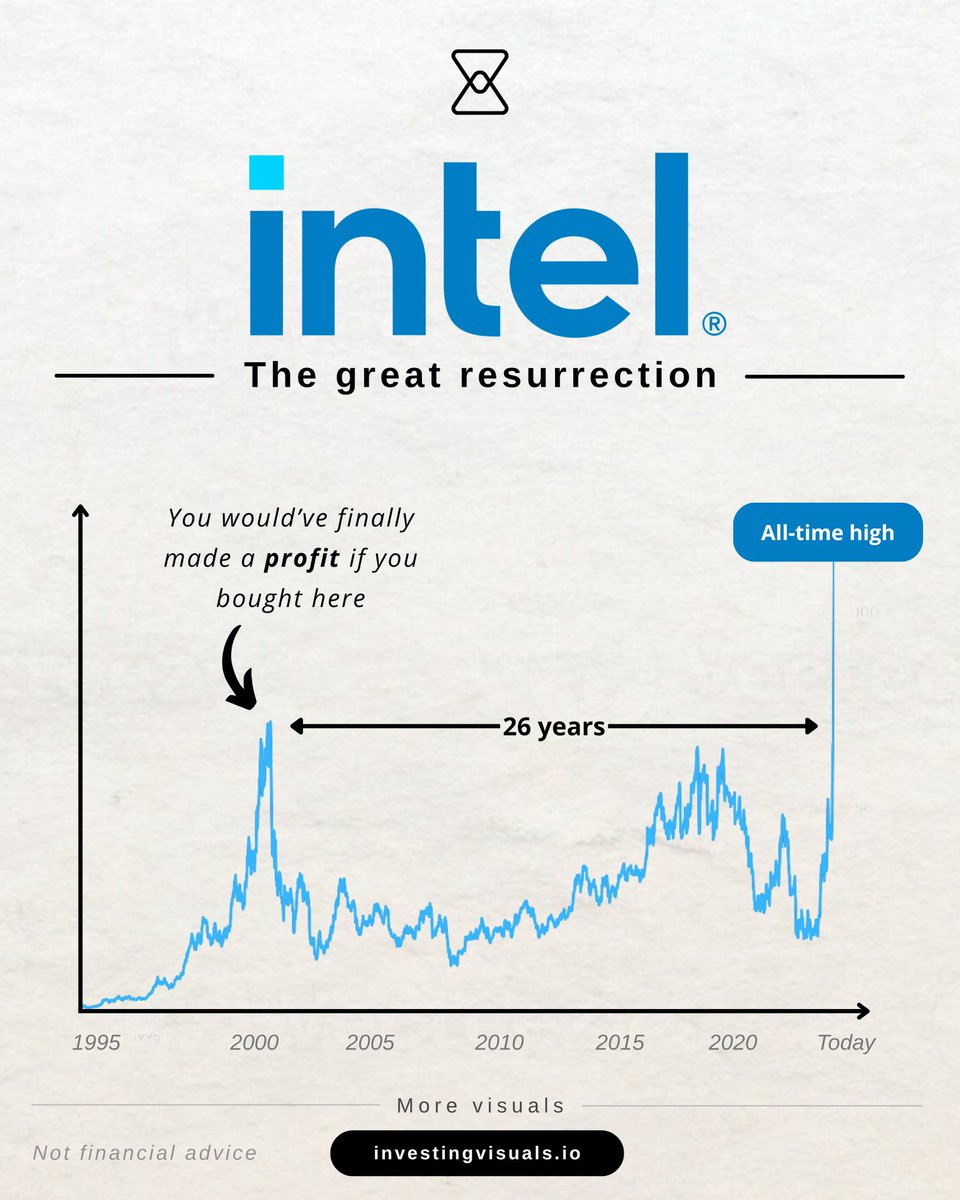

Bernstein expects HBM prices to triple in 2027.

SK Hynix is the market leader with ~62% HBM market share.

I bought the dip 🤝

3

8

72

7,354

Here’s a much more detailed write-up I did in April, comparing $MU, $HY9H.SG and Samsung and why I personally prefer SK Hynix👇

investingvisuals.io/ai-memor…

2

12

3,971

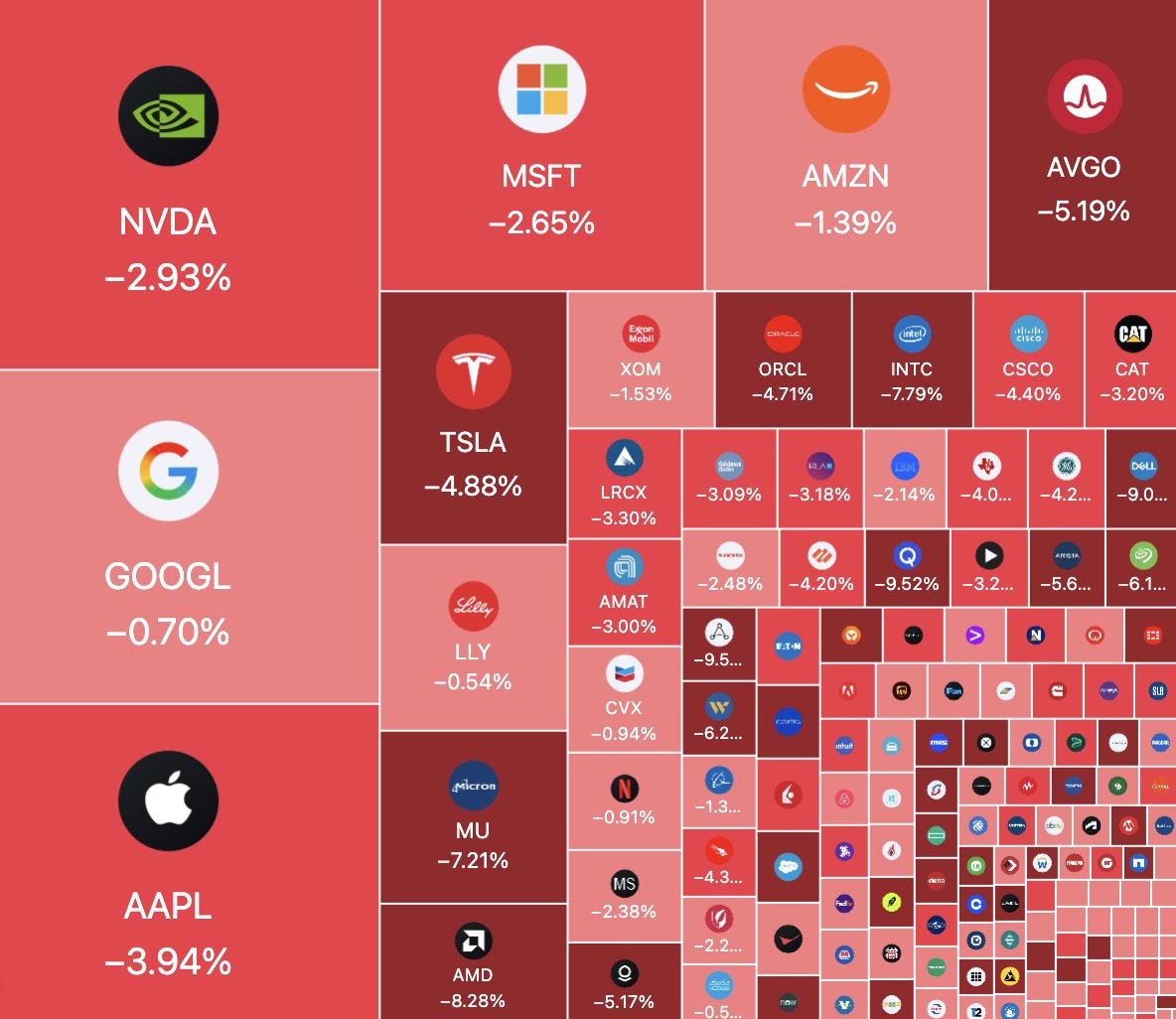

Semi's took a hit Friday but many are still up >100% YTD:

$SNDK 466%

A flash storage behemoth whose NAND and controller technology underpins SSDs and removable storage across PCs, servers, and data centers.

$HXSCL 205%

Leading producer of DRAM and NAND and one of the primary suppliers of high bandwidth memory for AI GPUs.

$ARM 198%

Licenses the processor architecture that powers nearly every smartphone and an expanding share of data center, automotive, and edge AI chips.

$MRVL 194%

Develops custom AI accelerators, networking silicon, and storage controllers for hyperscalers, increasingly embedded in the core of cloud AI infrastructure.

$MU 173%

Manufactures DRAM and NAND flash memory, with high bandwidth DRAM for AI training and inference driving a powerful upcycle in pricing and margins.

$INTC 152%

Designs and manufactures CPUs for PCs and servers while rebuilding its foundry business to become a second source to $TSM for advanced chips.

$LITE 123%

Builds optical transceivers and photonic components that move data inside and between AI data centers, riding the surge in bandwidth demand.

$AMD 107%

Designs high performance CPUs and GPUs for data centers, gaming, and PCs, steadily gaining server share and expanding its AI accelerator lineup.

$COHR 93%

Supplies lasers, optics, and photonics components used in chip manufacturing, optical communications, and industrial applications.

$ALAB 76%

Provides AI oriented data center hardware and connectivity solutions, giving cloud customers higher performance at lower power budgets.

4

13

101

9,899

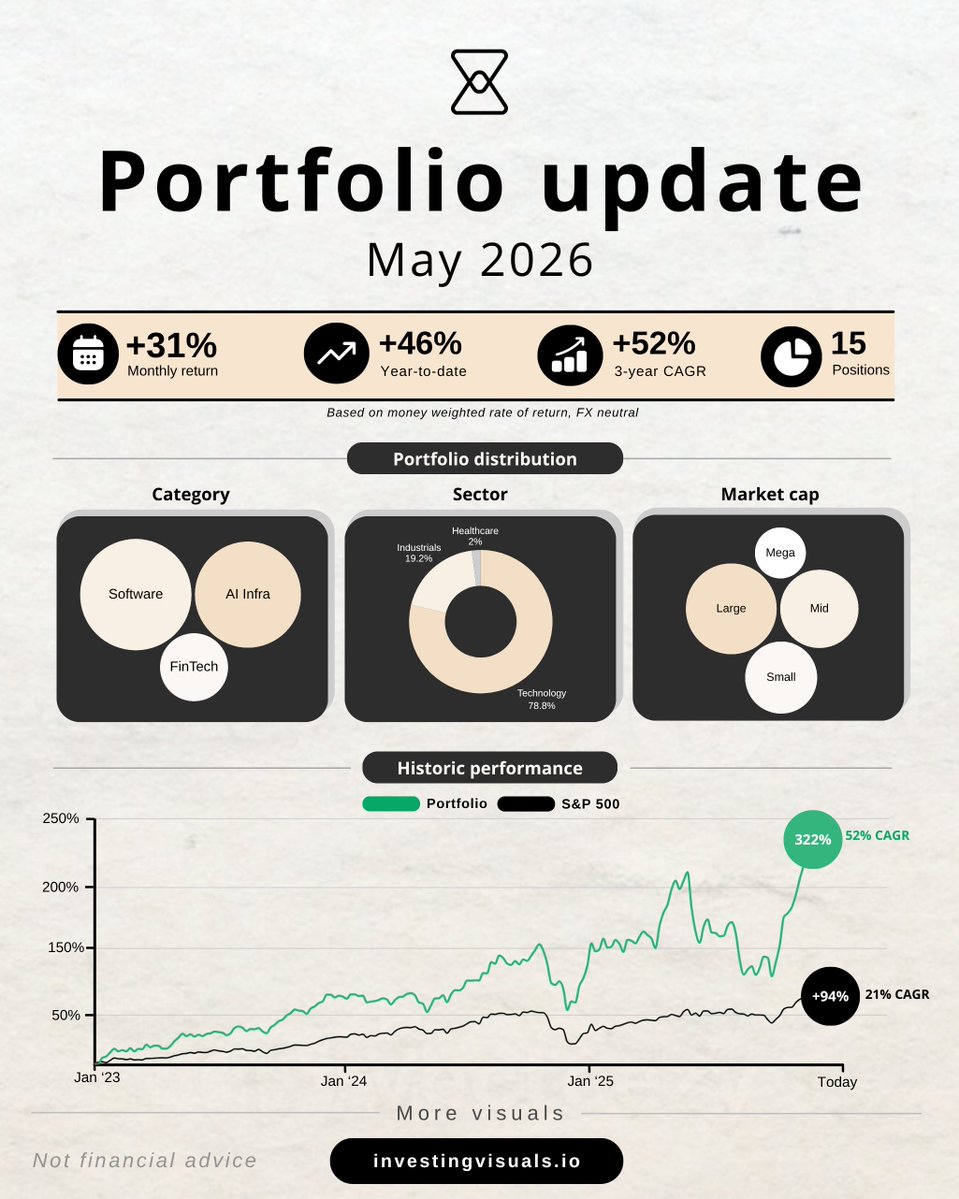

Portfolio update May

• Monthly: 31% vs $SPY 7%

• YTD: 46% vs $SPY 11%

• 3-years: 322% vs $SPY 94%

Last month I significantly reduced my exposure to semis, rotated some of it into software, and raised my cash position to around 25%.

I am still very bullish on the AI buildout and well positioned businesses in the AI supply chain, but valuations are getting frothy across the board.

Some of the positions I reduced:

• $ALAB

• $NBIS

• $AMD

I think the market pullback last Friday is a very healthy one, and it remains to be seen whether it is a short lived dip or the start of a correction.

While software has already had something of a revival from its absolute bottom, I still think there is significant upside left.

But not all software is created equal, so I only focus on the highest quality names such as $PLTR. And if semis continue to slide, I will happily add along the way.

Let’s see what Mr. Market has in store for us!

5

3

57

6,582

I shared a more detailed portfolio update for subscribers, where I walk through my thoughts, the reasoning behind recent moves, and my plan for the months ahead:

investingvisuals.io/portfoli…

5

3,621