Joined March 2012

- Tweets 1,709

- Following 71

- Followers 133

- Likes 784

20 Photos and videos

Itisha Gupta retweeted

29 Mar 2025

⚠️Lots of threads/posts on tapering, threshold, adjusted etc. Now we have March payslips can I tell you how I would approach it

1️⃣ Get your March 25 payslip. Note your YEAR TO DATE TAXABLE Pay. *IGNORE* gross pay and for now IGNORE pensionable pay. Dont use gross income and deduct pension contributions - the "taxable pay" already has them deducted so dont deduct it again.

2️⃣Do *NOT* add back in salary sacrifice for things likes cars and childcare. You are required to add in "relevant salary sacrifice arrangements made after 8 July 2015" - the key word here is relevant defined as "the individual gives up the right to receive general earnings or specific employment income in return for the making of relevant pension provision," - so DONT add cars etc back in.

3️⃣So you now have your NHS taxable income for the year. Now you need to add any other taxable income - think other PAYE, private practice, property, BIK, dividends, interest etc. Basically anything else that is subject to income tax. Less employment related Income Tax Reliefs claimed via tax return i.e. GMC, BMA, MDU etc

4️⃣Do NOT take off gift aid for normal charitable donations which is another common mistake Ive seen experts make. Note you can do this for the ridiculous £100k cliff calculation, but not threshold/adjusted

5️⃣So your NHS taxable income plus all other taxable income, less any other NON NHS pension contributions i.e. a SIPP, is THRESHOLD INCOME.

If this is below £200k you are not tapered and have the full £60k allowance and any carry forward (use the HMRC carry forward calculator to work out if you have carry forward - you will have needed both your RPSS to the 22/23 tax year and 23/24 PSS to work this out, latter obviously also delayed in England & Wales - you can estimate 23/24 using the tool below).

6️⃣If threshold income above £200k you need to work out ADJUSTED INCOME. You wont find out your PIAs for 24/25 until October 2025 but can estimate them using the link to the free tool and video below. If you are in 2008 its a bit more involved, and I wouldnt advise the NHS Employers modeller for this as for 2008 it ignores reckonable pay so is wildly innacurate. Adjusted income is THRESHOLD plus deemed PIA pension growth accross both schemes plus any other pension growth or SIPP contributions etc. The free tool below will help you calculate this.

7️⃣The free tool below will help you estimate your threshold and adjusted income, so see if you can expect a liability for 24/25 (due Jan 26, scheme pays Jul 26)

WHY IS THIS SO IMPORTANT in 24/25

Because of the 23/24 pay award paid in 24/25 and DDRB 24/25 many people will have VERY LARGE PIAs - Im year 14 (just) and my PIA is over £150k. That means if you go over THRESHOLD income, when you add in the PIA, tapering can be BRUTAL and reduce your allowance from £60k down to £10k - that might increase your AA tax charge by £22,500 (45% x £50k reduction).

So if your THRESHOLD income is CLOSE to £200k you can still DURING THE TAX YEAR ONLY i.e. the next 9 days or so make a SIPP payment to reduce it below threshold income to avoid tapering. Say your THRESHOLD income (step 5 above) is £210k you could make a £11k GROSS SIPP payment which would reduce your threshold income to £199k which could reduce your AA liability by £22.5k making the SIPP free.

See the worked examples in the video below

Free tool and video to work all this out is below

Free Tool: bit.ly/Goldstone2325PIA

Self help video: youtube.com/watch?v=CNYcurbD…

9

22

73

35,318

Itisha Gupta retweeted

24 Mar 2025

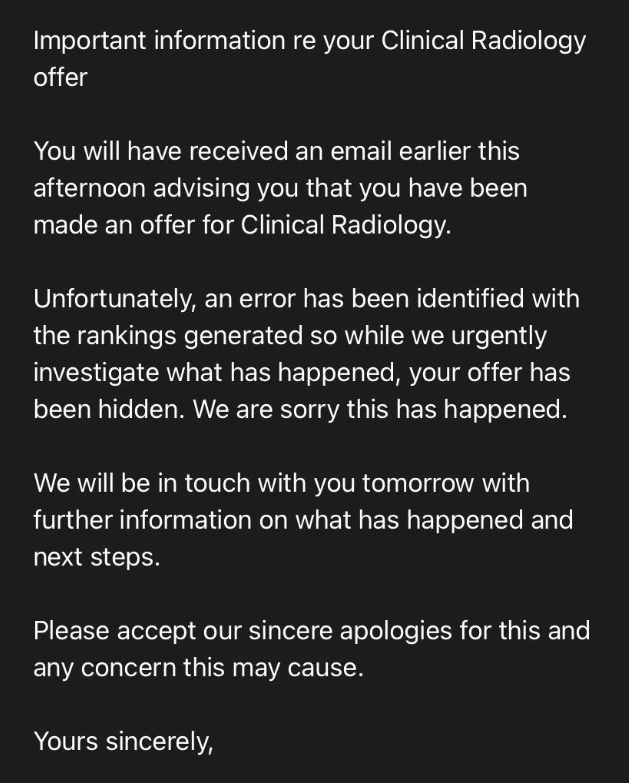

Im sorry this whole national recruitment mess is a complete disaster. Why do we keep on seeing these monumentally damaging errors? I feel so bad for those caught up in this mess with lives on hold @RCRadiologists

The whole thing needs a rethink in all specialities IMHO.

24 Mar 2025

Doctors received offers for Radiology training posts at around 3-4pm. They were able to accept these offers on Oriel and received confirmation of acceptance. Offers then began to disappear on Oriel. At 6:30pm they received this email.

Simply unacceptable.

3

35

128

14,238

Itisha Gupta retweeted

27 Feb 2025

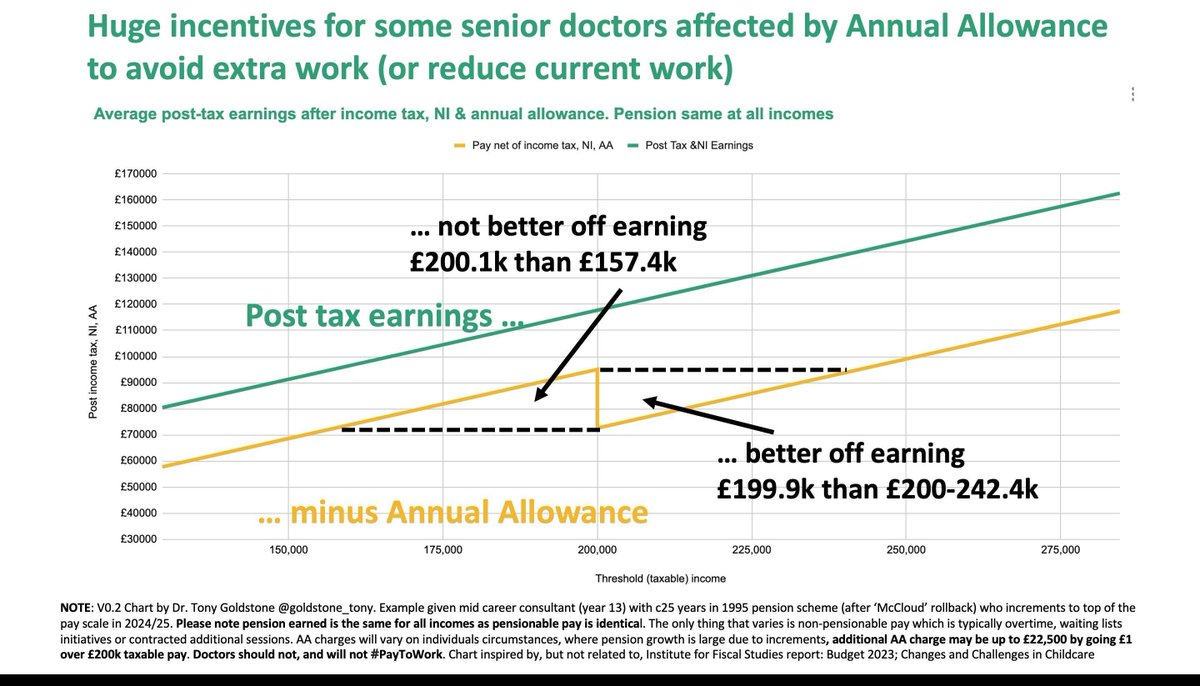

🚨little over 1 month left of this tax year. If you are a consultant or other high earner that had a signfiicant pay rise in 24/25 its more important than ever you #knowyournumbers & crucially understand this ridiculous graph 👇

Free tools & videos in tweets below. Don't ignore

1 Jan 2025

1/3 ICYMI Ive done a couple of videos 📹 FREE TOOL calculating annual allowance for self assessment 23/24 (needed by 31/1/25) without *MISSING* brown envelopes.

And crucially also looking at the 24/25 tax year that could bring BRUTAL tax charges for some

Please share 👇 👀📹

3

7

26

19,575

Itisha Gupta retweeted

2 Mar 2025

Received a brown (or white in Scotland!) "RPSS" envelope & have no idea what is it, nor what to do ... start here👇

I open mine and talk you through the numbers, what they mean and what you need to do

Please RT/share with colleagues who are struggling

youtube.com/live/zlcFZjv_Jys…

3

6

14

10,293

Itisha Gupta retweeted

12 Oct 2024

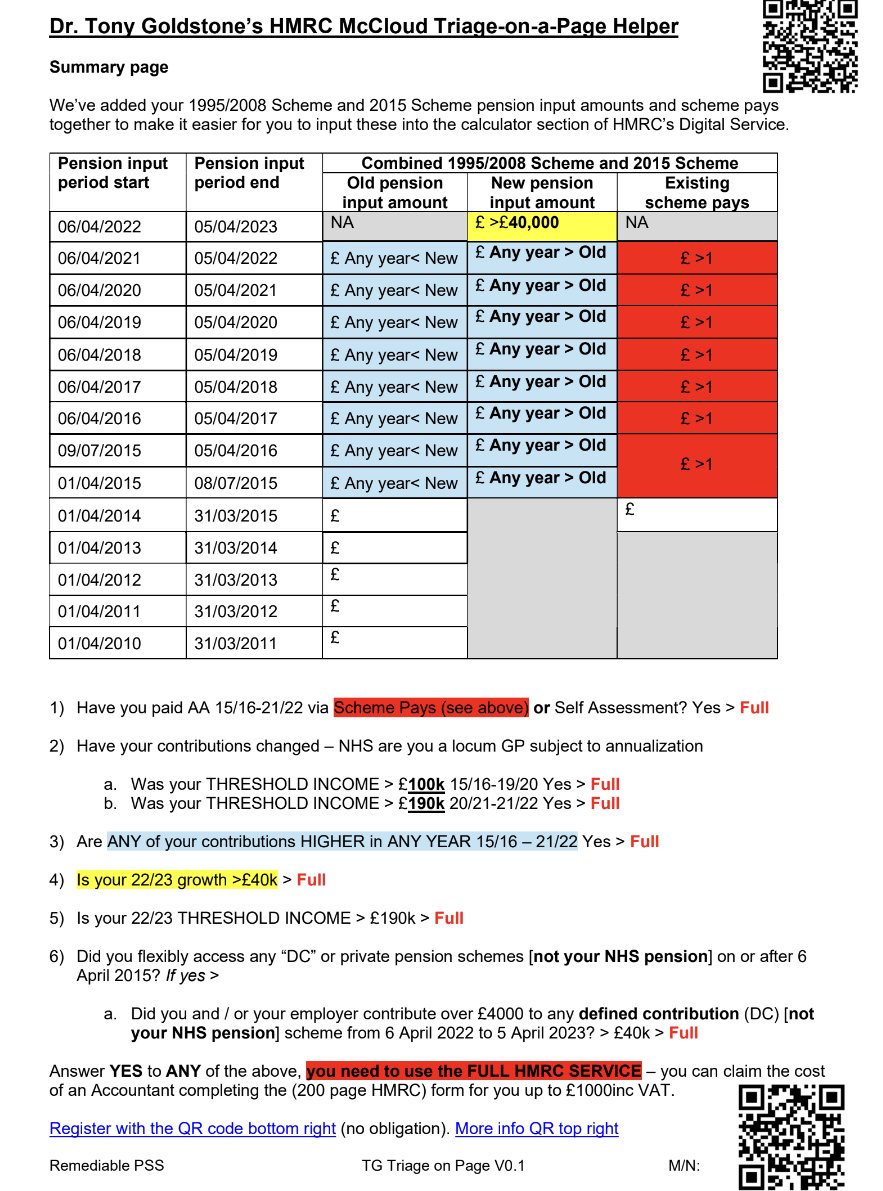

If you have received your brown envelope, I hope you are coming my "live opening" Sunday 6pm see 👇

To get the most of it please print out the attached single page "triage on a page helper" (from the link)

bit.ly/TGMcCloudTriage

Don't worry, Ill talk you through it

Pls shr/RT

11 Oct 2024

I'll be opening my "brown envelope" live on Sunday 13th @ 6pm and talk you through it & answer these 5 questions 👇 Please spread the word/RT

3

25

53

28,217

Itisha Gupta retweeted

9 Oct 2024

Hi Dr Asad- the scheme pays indicates you had AA charges. That almost certainly means you are due compensation because they almost always go down (watch my video on this)…. But only if you claim

Help is available as it’s a complex, with your costs fully recoverable - the HMRC process is 200 pages long and a minefield of traps to go wrong

So if you need help, I've built tools in partnership with leading specialist medical accountants who can help - register with no obligation here bit.ly/MazarsGoldstone

More info here

bit.ly/MazarsGoldstonePenFin…

9 Oct 2024

Hi @goldstone_tony

I have amount in “scheme pays” column. Do I need to process it through HMRC? Or just leave as it is??

1

5

7

6,105

Itisha Gupta retweeted

4 Sep 2024

IMPORTANT: Its crucially important higher earners at risk of #taper understand risks, especially in year where pay/pension has *started* to be *restored*👇[still way down]

With upcoming budget its crucially important policy makers understand risks @wesstreeting @jamesmurray_ldn

9

48

93

41,979

Itisha Gupta retweeted

6 Aug 2024

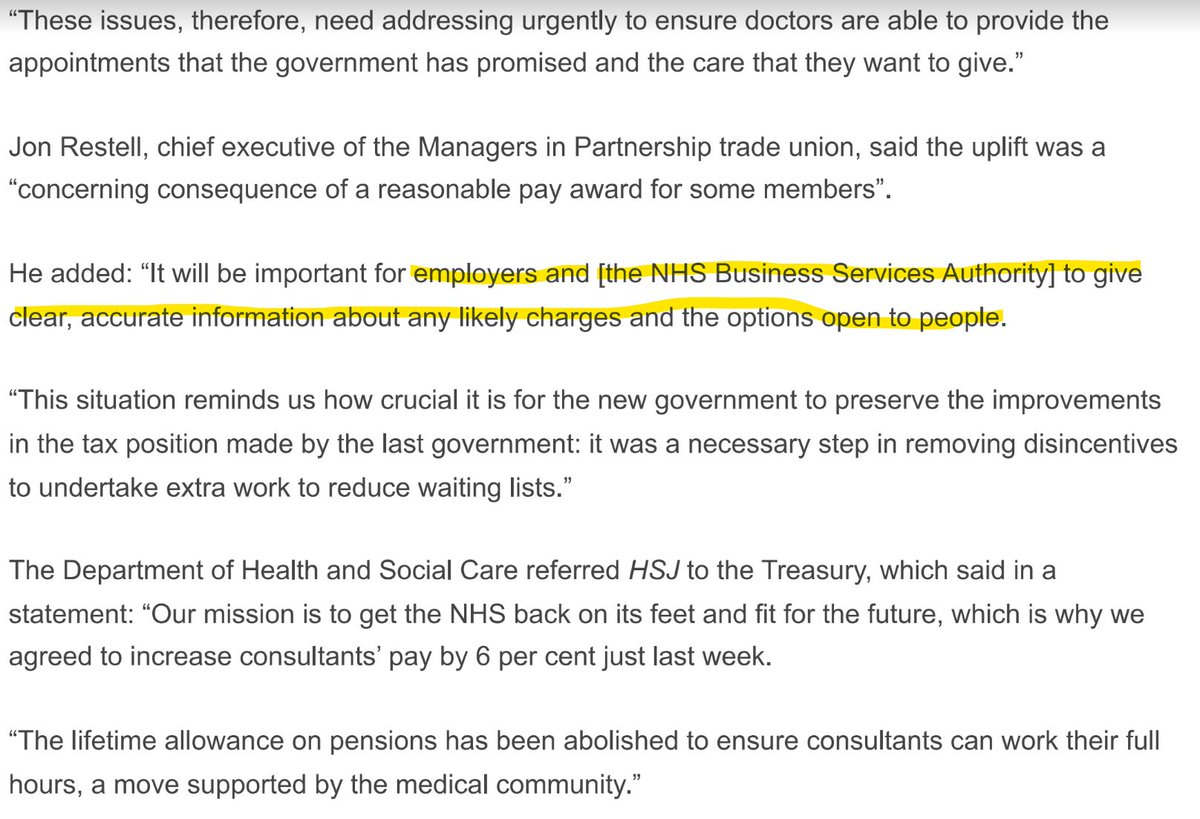

10/ Finally slightly concerning response from Treasury who proclaimed LTA was abolished to 'ensure consultants can "work the hours"'.

Maybe treasury should ask if THEY would give up their weekend to do extra lists & #PayToWork

Need to find a solution to this quickly

Pls RT!

9

9

9,333

Itisha Gupta retweeted

29 Jul 2024

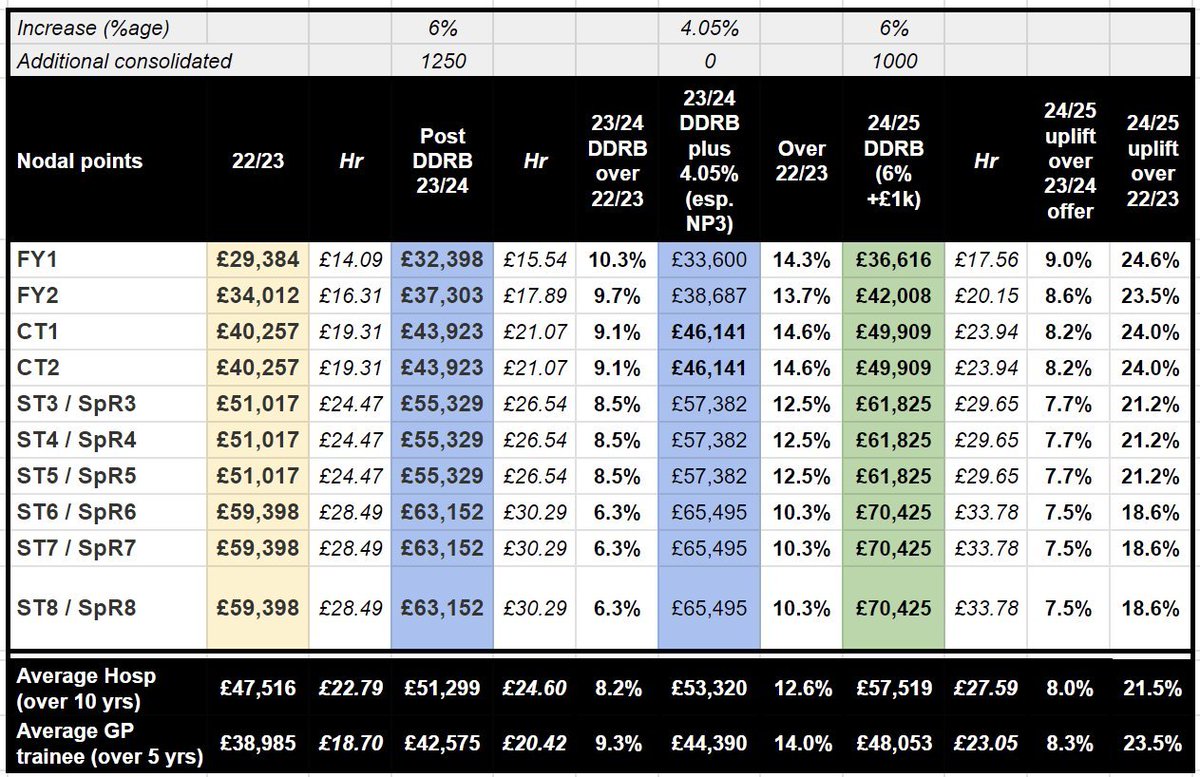

Juniors below - the 22pc is across 2 years not one per below

1

1

2

1,189

Itisha Gupta retweeted

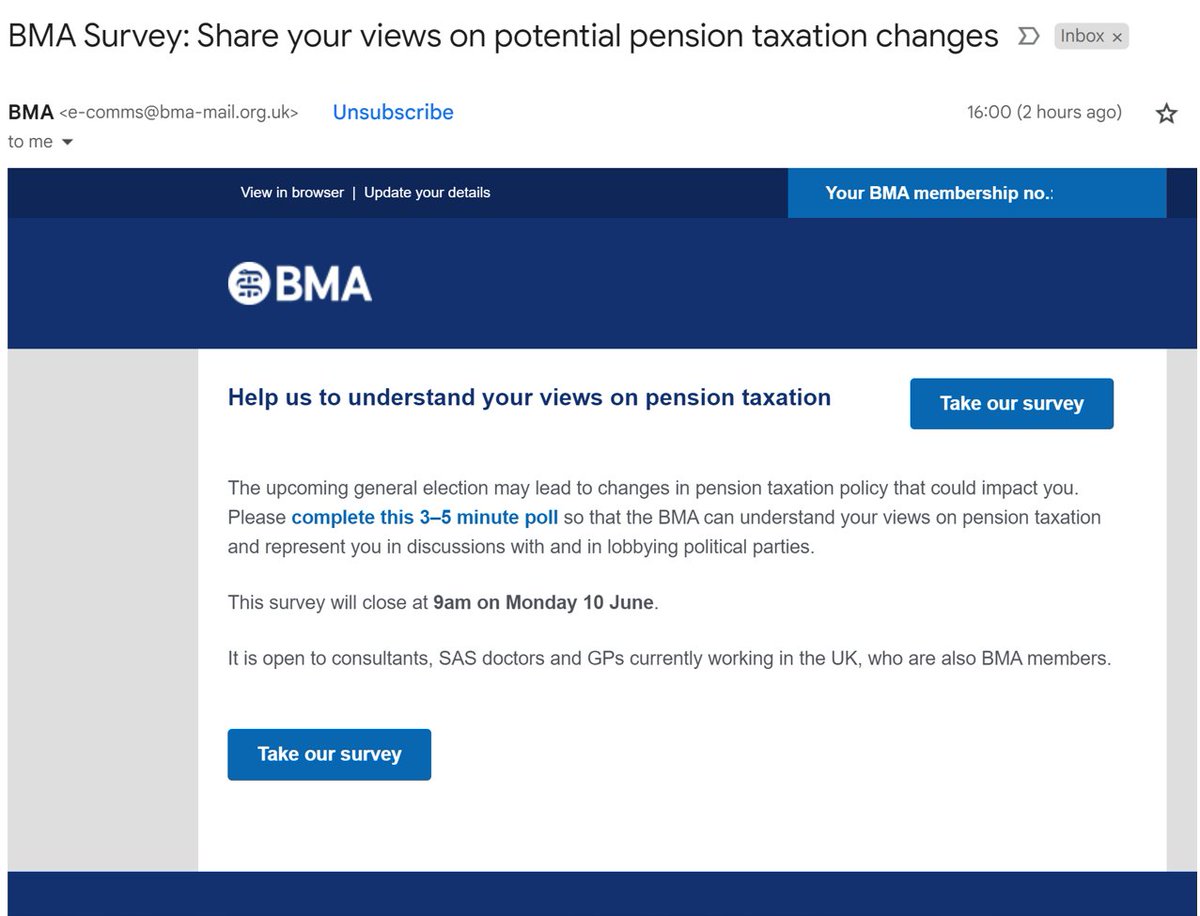

9 Jun 2024

Thank you very much to the 4561 consultants, senior SAS & GPs who have so far responded to our survey 👇&the 1359 who left free text comments.

This closes tommorow at 9am - please respond if you can before then, and if you can leave a comment on how this would affect YOU

7 Jun 2024

Very IMPORTANT: If you're a consultant, senior SAS or GP (& BMA member) you should have received 👇this

We *NEED* to know your views ASAP. Take <5min to do closes Monday 9am. Please, do it now. Please feel free to share your comments / story in the servey too.

Pls Share/RT

1

8

15

6,357

Itisha Gupta retweeted

9 Jun 2024

9/9 And that the tapered annual allowance, one of the worst designed taxes of all times still has brutal cliff edges and can operate in a perverse way to disincentivize extra work / overtime

Pls RT the first tweet in this 🧵to share @JosephineCumbo's excellent article

4

8

4,935

Itisha Gupta retweeted

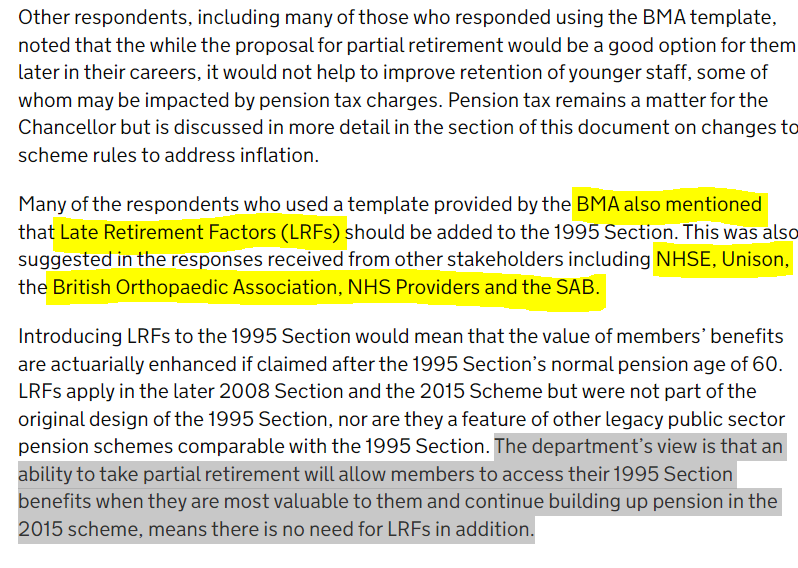

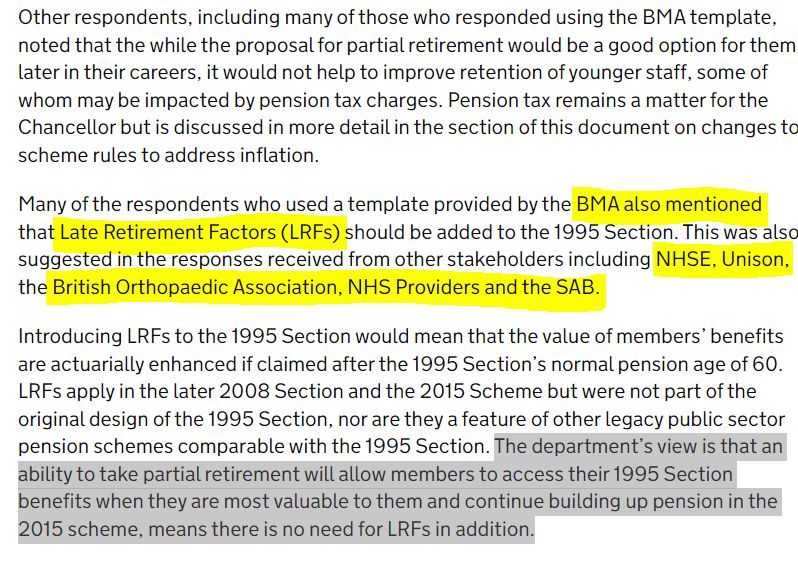

17 May 2024

3/3 Furthermore although #LateRetirementFactors would solve this as we have been suggesting for years, we believe the scheme @nhs_pensions has a DUTY to inform members of the 1995 scheme that they are giving up pension if they dont retire at their 1995 pension age (60 or 55)

6

13

3,073

Itisha Gupta retweeted

17 May 2024

2/3 Whilst DHSCs view that that do not need to bring in #LateRetirementFactors because of #PartialRetirement - I'm afraid that's nonsense unless partial retirement is available to ALL who want it

Its GROSSLY unfair to not allow any member to access benefits they paid for at NPA

3

6

13

4,681

Itisha Gupta retweeted

17 May 2024

1/3 REMINDER: Work a day past your retirement age in the 1995 section and you are donating or 'burning' your pension back to gvmnt.

I with BMA & many others including NHS England, Unison, NHS Providers & schemes own advisory board have been calling to end this for years

2 Aug 2022

6/ But for the vast majority (who are in 1995), staying a day past 60 is quite literally, burning their pension - as in 1995 there is no uplift for late retirement (in fact due to massive pay cuts, its quite the opposite, as pension deflates with final salary linking).

12

35

78

54,332

Itisha Gupta retweeted

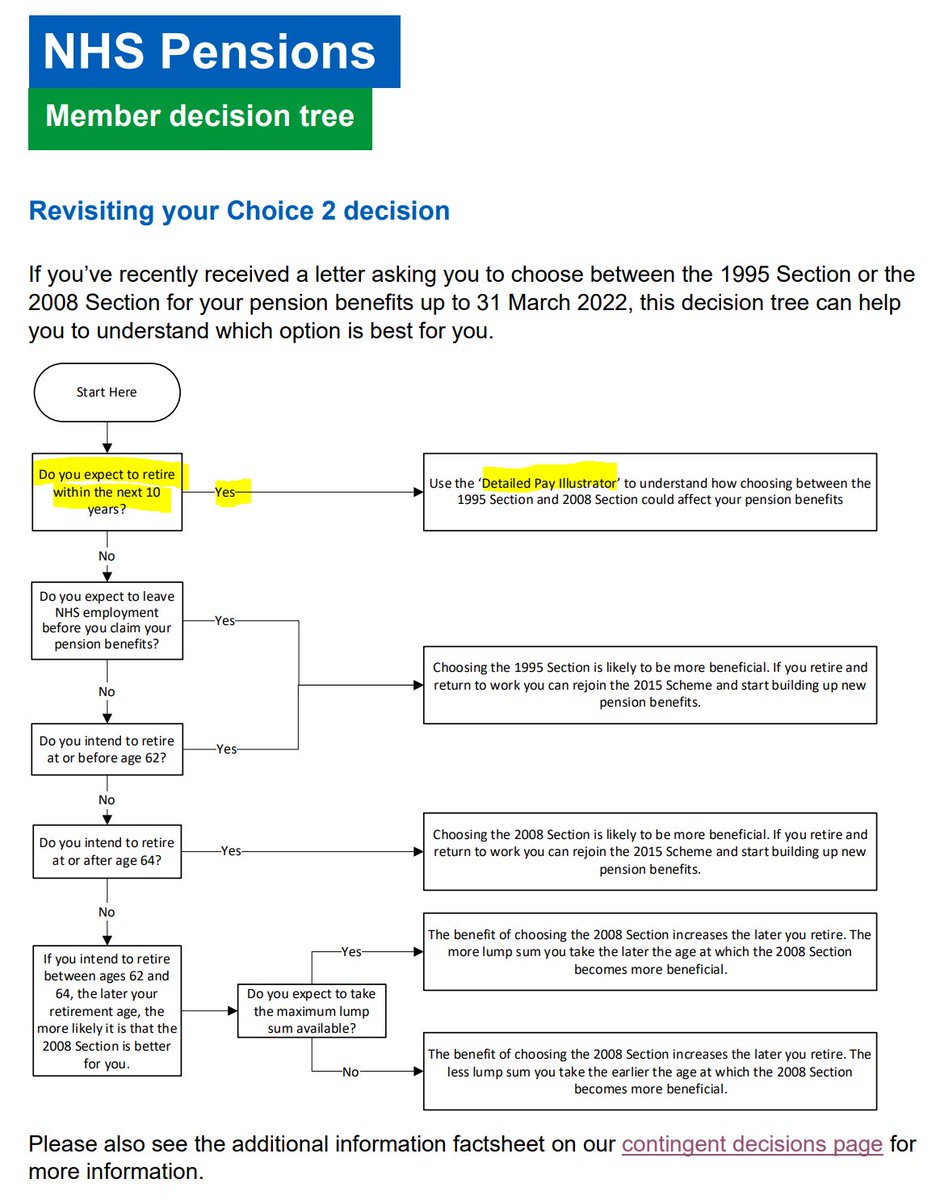

7 May 2024

3/ A new decision tree has been added - first crucial step if you plan to retire in the next 10 years, i.e. "reckonable pay" may benefit from recent very high inflation - use the detailed modeller provided by NHS BSA before making your decision (or to revisit your decision)

2

4

7

4,481

Itisha Gupta retweeted

7 May 2024

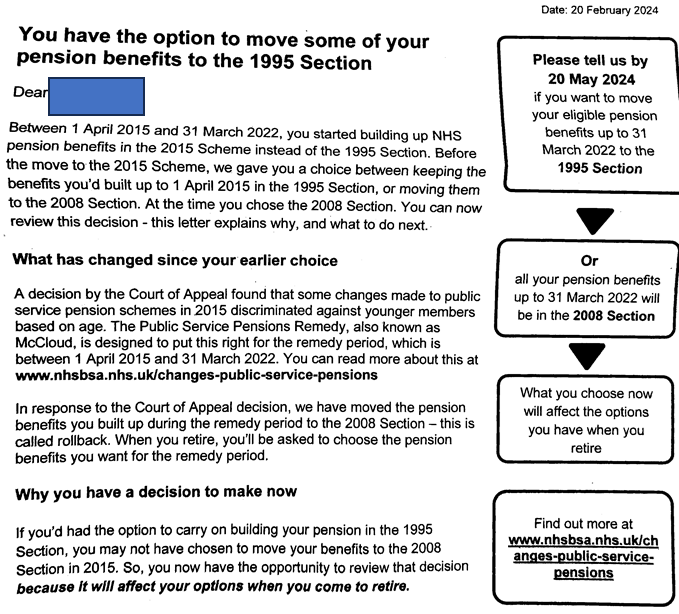

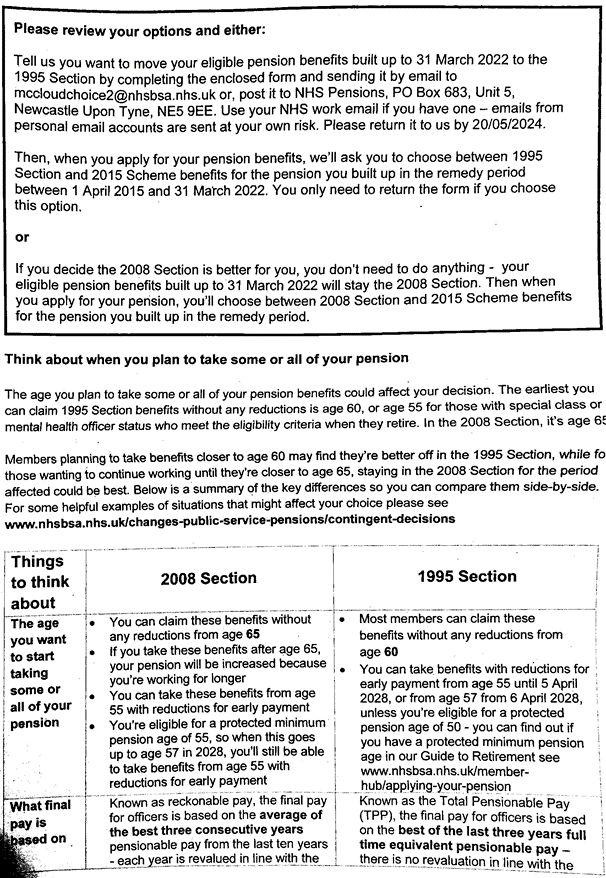

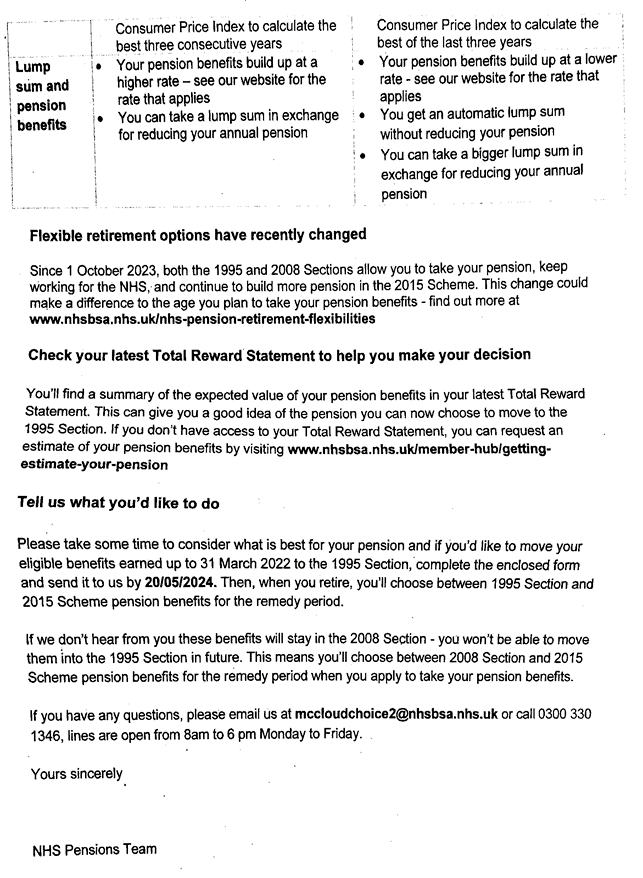

1/ BREAKING: Following our complaint to DHSC / BSA that the quality and type of information going to choice 2 members was poor & would not allow them to make an #informedchoice on reversing a choice 2 decision, BSA have today released updated information 👇

24 Feb 2024

1/ *VERY* concerned about the quality & type of information coming to @BMA_Pensions members to allow them to make choices in regards to McCloud.

For members who chose to move to 2008 (so called "choice 2", we saw the first of this information last week - deep dive 🧵

Pls RT

2

12

28

44,730

Itisha Gupta retweeted

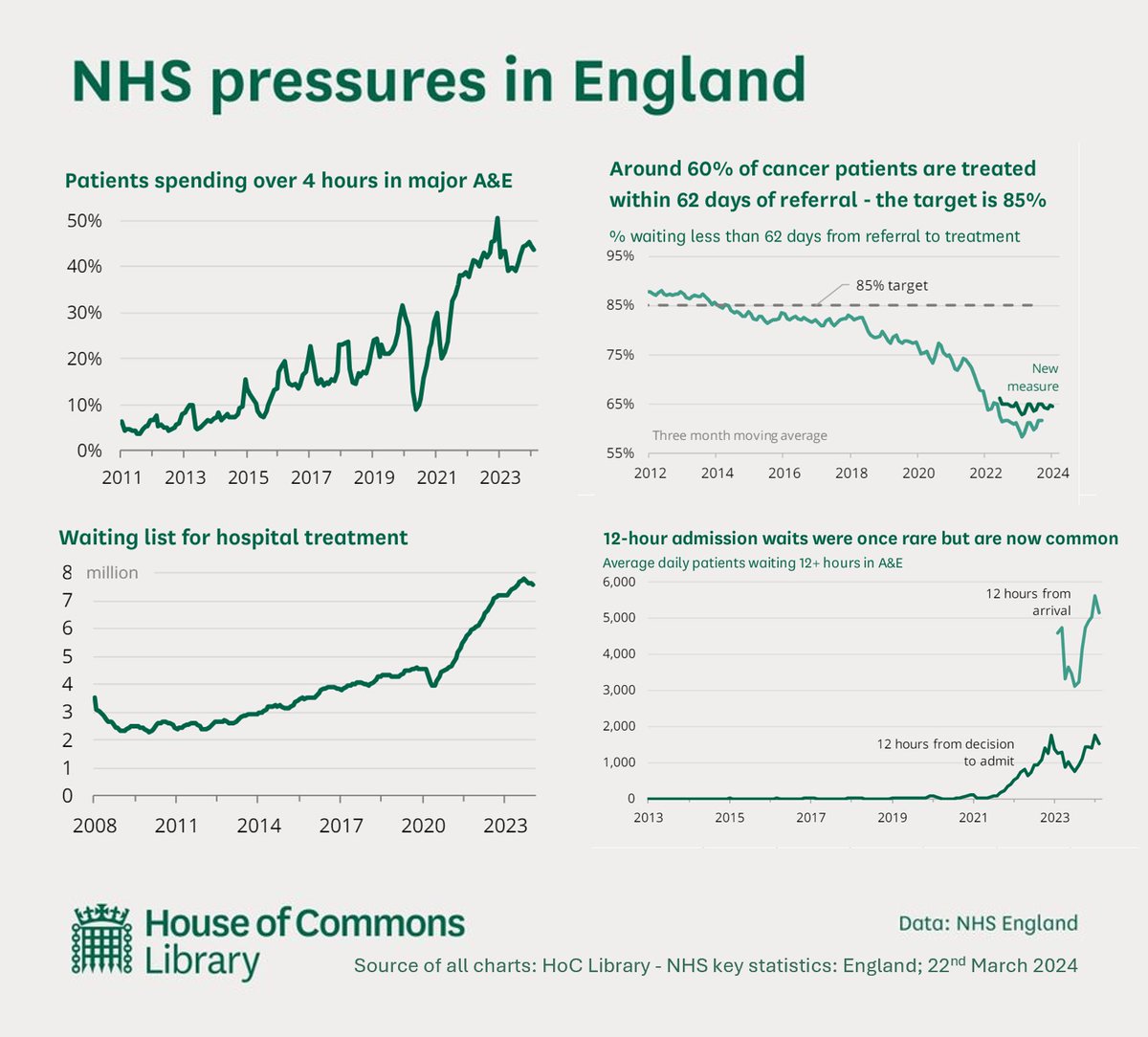

29 Apr 2024

The NHS is completely BROKEN😢

WASNT broken by COVID/Strikes/inflation (*delete excuse)

but by deliberate CHOICES to break it

RT if you want this/next government to make CHOICES to properly fund the NHS, #reward staff & provide better healthcare than 👇 for the UK population

7

204

268

32,037

Itisha Gupta retweeted

15 Jan 2024

I wrote about beta-blockers after MI today on @Sensible__Med

Gosh, I hadn't quite realized how old and out of date and modest that data was.

sensible-med.com/p/a-surpris…

5

15

90

18,495

Itisha Gupta retweeted

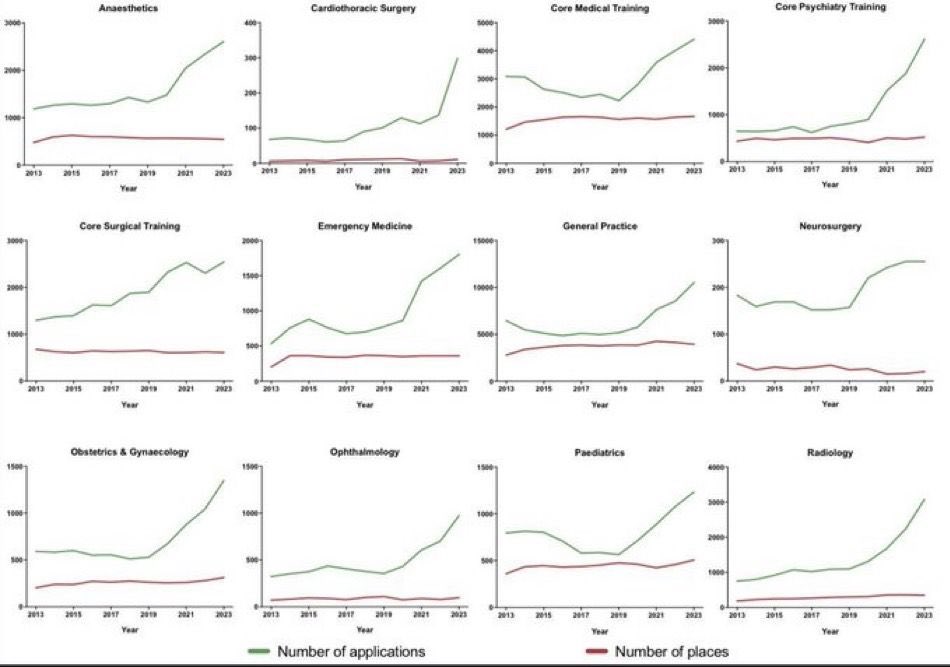

17 Jan 2024

Who is going to train them all... How much can you fill a leaky bucket?

17 Jan 2024

These graphs are *terrifying*👇

It all feels a bit like the MMC/MTAS debacle all over again

So important that we open up sufficient training numbers to fill workforce shortfalls *and* ensure those not in formal training get mirrored T&Cs

3

4

1,991

Itisha Gupta retweeted

13 Dec 2023

1/ NEW: @nhs_pensions have released their partial retirement calculator.

partialretirementcalculator.…

Members (though not all) will be able to estimate how partial retirement looks for them

3

18

41

24,976