Japan-focused shareholder activist. Buying stakes in Japanese small caps for ~30c on the $ and engaging with them to realise the embedded value . DMs open

Joined April 2012

- Tweets 3,881

- Following 921

- Followers 6,269

- Likes 3,230

685 Photos and videos

Pinned Tweet

16 May 2023

Japanese stocks are rallying to heights not seen since the 1990s. Back then it was the aftermath of bubble valuations. Now, there is a solid foundation of earnings growth, corporate governance improvements, and increasing cash returns to shareholders! 1/n

27

35

225

117,379

A truly excellent post that should be read by anyone who owns stocks.

Jun 10

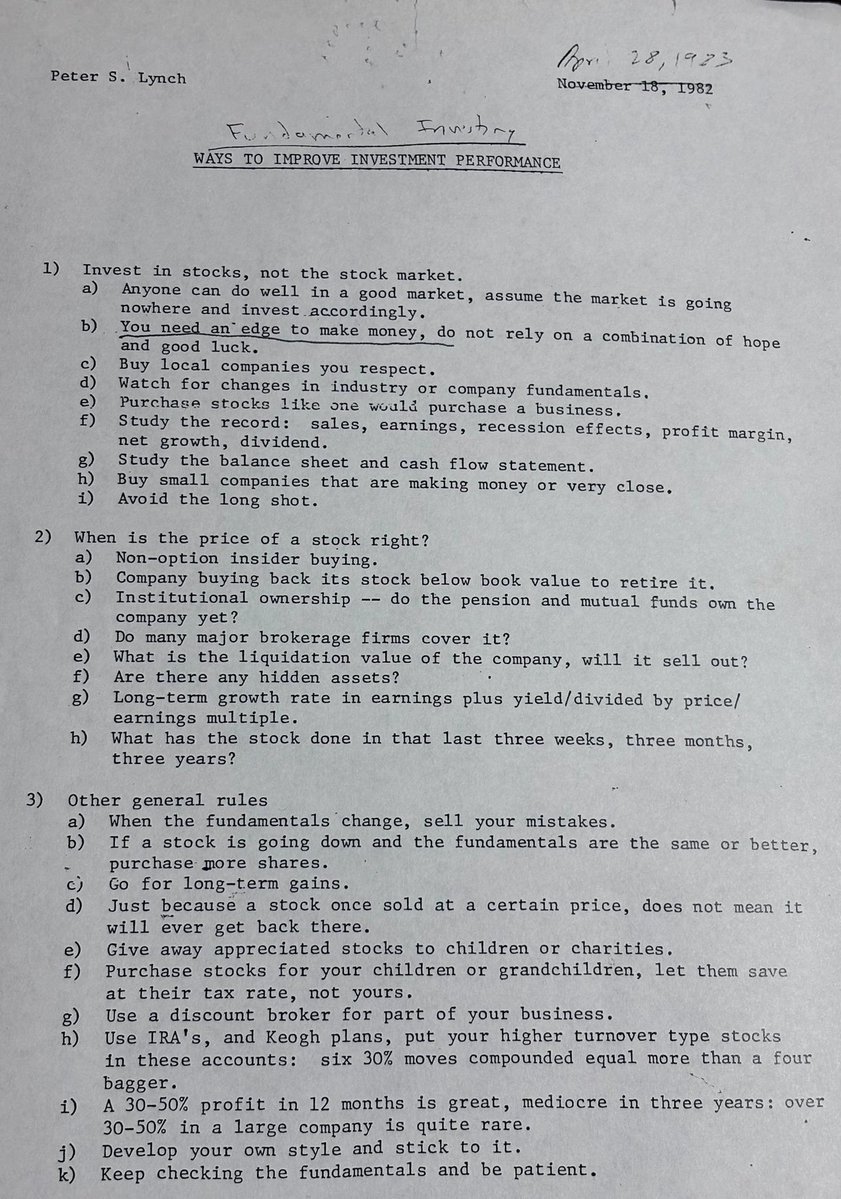

I was 26 years old when Peter Lynch handed me this.

April 28, 1983. I was the auto and retail analyst at Fidelity.

Peter was in his prime, on his way to building the greatest mutual fund track record in history:

29.2% annual returns for 13 YEARS STRAIGHT, growing Magellan from $18 million to $14 billion. The Babe Ruth of investing.

I'm looking at the principles he had typed up on a single sheet of paper that I've kept in my files for 42 years and I believe now is the perfect time to revisit them again.

Let me walk you through a few:

Rule 1B: "You need an edge to make money. Do not rely on a combination of hope and good luck."

Today's retail investor has no edge. He has Reddit, Robinhood, zero-DTE options and a TikTok algorithm pushing him into whatever stock just ripped 200% the day before.

That's hope and good luck wearing a fancy costume.

Rule 1E: "Purchase stocks like one would purchase a business."

Tesla trades at over 360 times earnings on a business deteriorating in real time, Oracle has $206 billion in liabilities against $39 billion in equity, MicroStrategy is a leveraged Bitcoin holding company priced like a software firm, and don't even get me started on SpaceX, that piece of garbage you'll be able to trade tomorrow...

Nobody in their right mind would buy these as actual businesses. They buy them as stories, narratives, and lottery tickets.

Peter would have called it the same way I do - these are not investments. They are speculations. GAMBLING.

Rule 1G: "Study the balance sheet and cash flow statement."

The hyperscalers spent over $380 billion on AI capex in 2025. Goldman says the measurable productivity payoff does not arrive until 2027 at the earliest.

Oracle just reported NEGATIVE $23.7 billion in free cash flow for fiscal 2026 while borrowing at a pace that would make a leveraged buyout firm nervous. The cash flow statements are screaming but nobody is reading them.

Rule 1I: "Avoid the long shot."

This one cuts the deepest.

The entire market has become a long shot.

OpenAI is projected to post roughly $74 billion in operating losses in 2028 ALONE while priced for transformation tomorrow. Bitcoin treasury companies are multiplying off thin air.

The retail investor of 2026 is making one long-shot bet after another and calling it a portfolio.

Rule 3A: "When the fundamentals change, sell your mistakes."

Tesla's fundamentals have changed.

California registrations are down 24% year over year and inventory days went from 10 to 27. Musk himself admitted on the last earnings call that Hardware 3 cannot achieve unsupervised FSD, breaking a promise made to 4 million customers.

The fundamentals have screamed change. But the stock is still at $385.

The mistakes are not being sold. They are literally being doubled down on with leverage.

Rule 3I: "A 30-50% profit in 12 months is great. Mediocre in three years."

Today's retail crowd expects 30-50% in a WEEK. Then they wonder why they get wiped out the second the hype stops.

And my favorite - Rule 3J: "Develop your own style and stick to it."

That is the entire game right there.

I developed mine sitting across the hall from Peter Lynch in 1983, watching him work, reading his notes, getting my own research handed back to me covered in his pencil marks. Then in 1984, my first full year managing money, I ran the #1 mutual fund in America. The Fidelity Overseas Fund was top 2 for the next six years running.

I did not get there by chasing narratives. I got there by following the sheet of paper you are looking at right now.

42 years later, this single page contains more wisdom than every Fintwit thread, CNBC segment, and Wall Street price target combined.

Peter retired in 1990 with the greatest mutual fund record in history. Then he sat down and wrote books explaining exactly how he did it.

Only a few "investors" these days read them.

And almost nobody is reading the balance sheets, the cash flow statements, or studying actual businesses today either.

They are chasing AI, crypto, and whatever pumped yesterday.

The wisdom on this page is timeless and it's more important than ever.

1

15

3,545

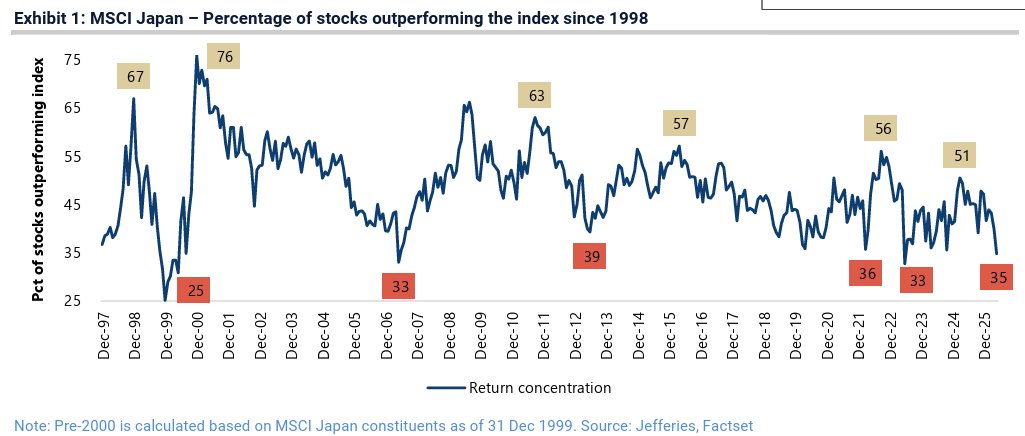

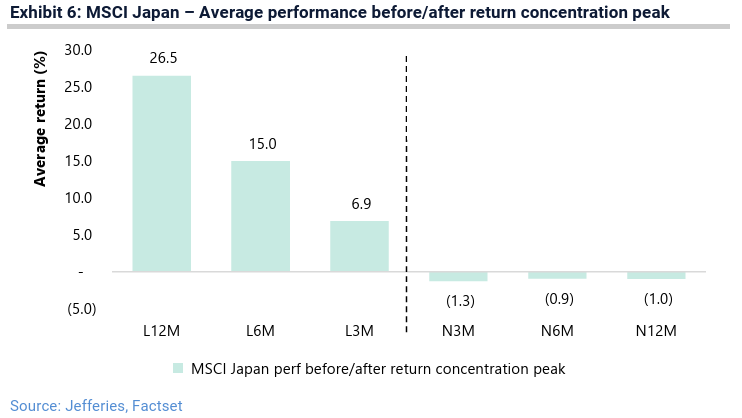

Are you allocated to Japanese stocks?

Is that via an index ETF, a benchmark aware large cap allocation, or a growth-focused mandate?

It may be time to consider a different approach.

Per some great work by Shrikant Kale, the % of stocks in the MSCI Japan index that outperformed the index in May, hit a level that is in the 3rd percentile of all monthly readings since 1997.

Following such periods of increasing concentration, index performance tends to be lacklustre, and the previous winners tend to become losers on average.

What has worked historically during market-broadening phases, is to be invested in "Yield", "Value", and "Low-beta" stocks.

What should be avoided historically in such phases are "Momentum", "High Beta", and "Growth" stocks, as well as "Large" stocks.

Investors may benefit from considering an allocation to small-cap value, particularly lower-beta asset rich stocks offering a solid dividend yield.

For wholesale investors, Senjin Capital offers such a strategy that also benefits from self-created catalysts instigated by our constructive activist approach. Visit our website, sign up to our newsletter, or DM me to learn more.

2

1

14

6,976

When a supposedly blockbuster IPO (SpaceX) has to extend its sales effort to Commsec in Australia and Sharesies in Oz and NZ, as well as, I'm hearing, through Austria and Scandinavia...

What does that imply for demand?

(screenshot from "Crikey")

1

4

1,511

A lot of good names mentioned in this post.

Any that have been missed?

@kenkyoinvesting

@InvestInJapan

@travislundyasia

@puppyeh1

@CacheThatCheque

@masuminishida

@nomurasyo

@JCVpartners

@japan_guru_x

@japan_cap

@hiroki1379

I’m sure I’ve missed some in the list above.

Jun 4

What are some of your favorite Japanese stocks or Japanese value investor accounts to follow here?

5

2

21

7,008

Working across geographies can be challenging.

One of these challenges is the different timing of public holidays!

When the ultimate investor, fund manager, and the investments are in different countries, a degree of flexibility is required.

In practise, that often means always being on call.

So it was great to find time to get out today and enjoy Sydney’s winter sunshine with my wife Gitanjali and our children on the King’s Birthday public holidays.

With a high of 19 degrees today, but feeling a lot warmer in the sun, it is easy to see why people love Sydney’s weather.

We were both working this morning (my wife also works across countries), and will be again after the kids are in bed tonight, but our park adventure made the day special.

6

1,597

My bold prediction for the next few weeks?

Equity strategists will increase their use of the term “Fed Put” by 10,000% vs the last two months.

11

1,075

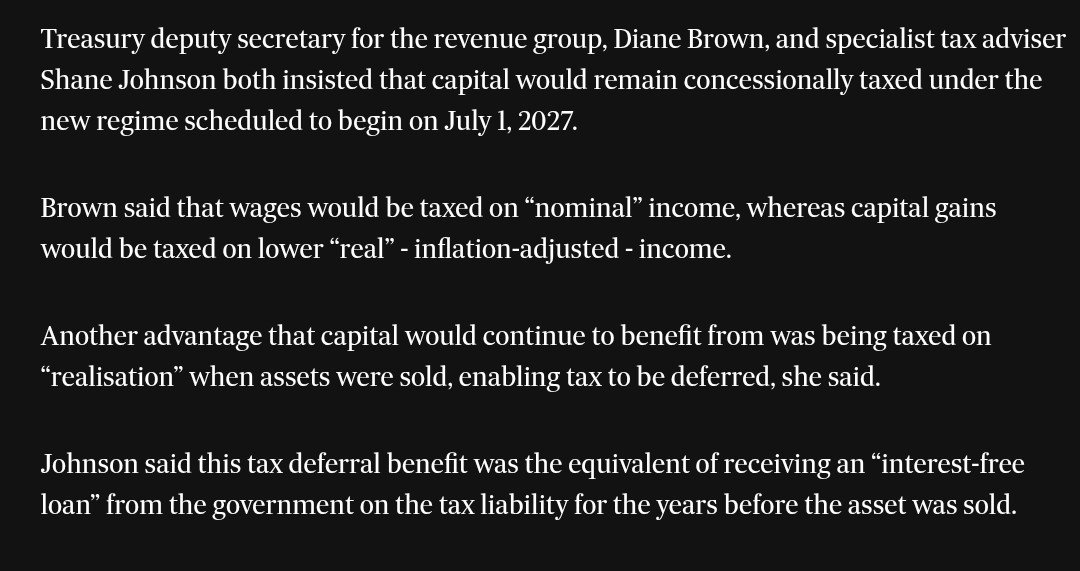

This kind of thinking is madness. It’s a great way to prevent capital formation and productivity growth.

Jun 5

By not taxing unrealised gains it's an 'interest free loan from the government'

We really are going to try and speed run the communist experiment again aren't we?

I can't believe this is an opinion held by anyone within shooting range of our government.

Wow.

2

2

10

1,139

A lovely day in Brisbane for the Private Wealth Network’s real estate event.

But I’m still a Kiwi, so very excited about this start to the series!

1

4

1,565

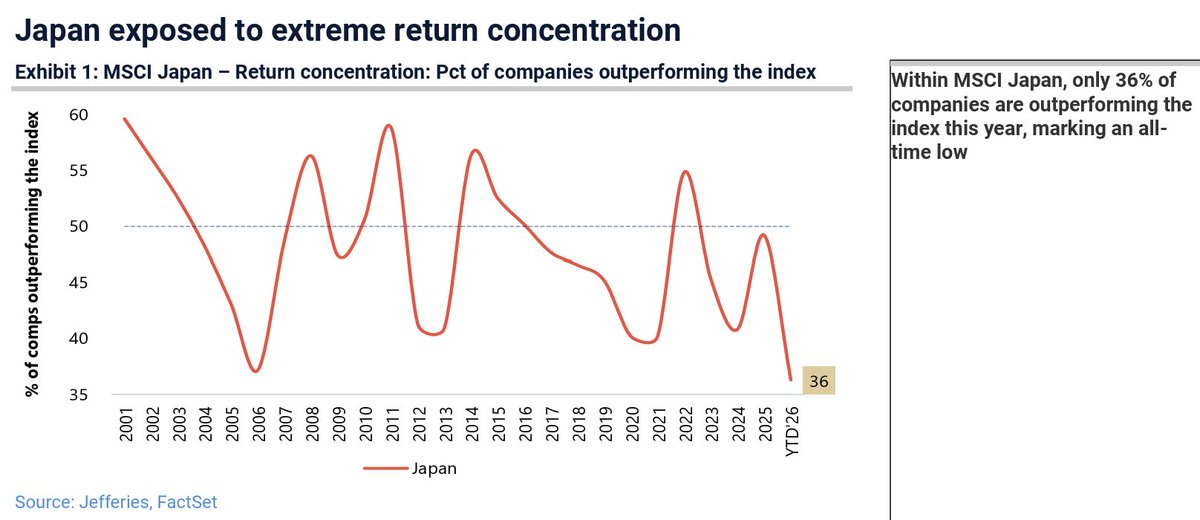

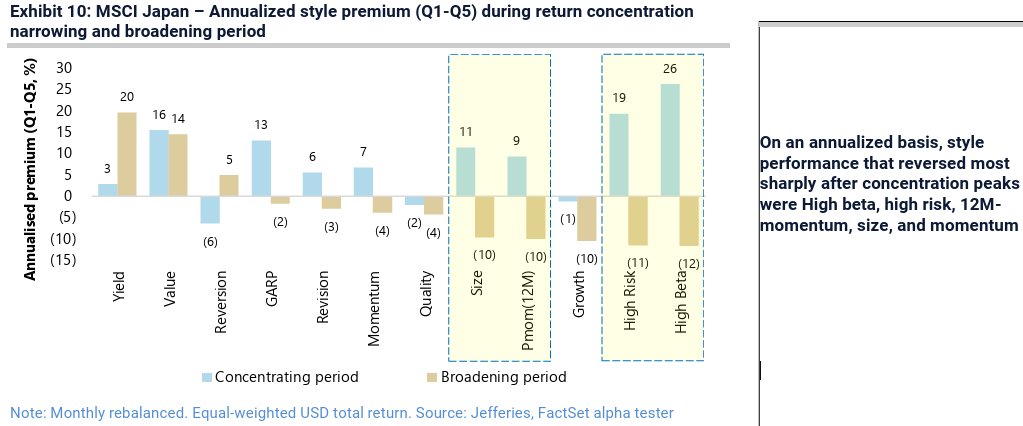

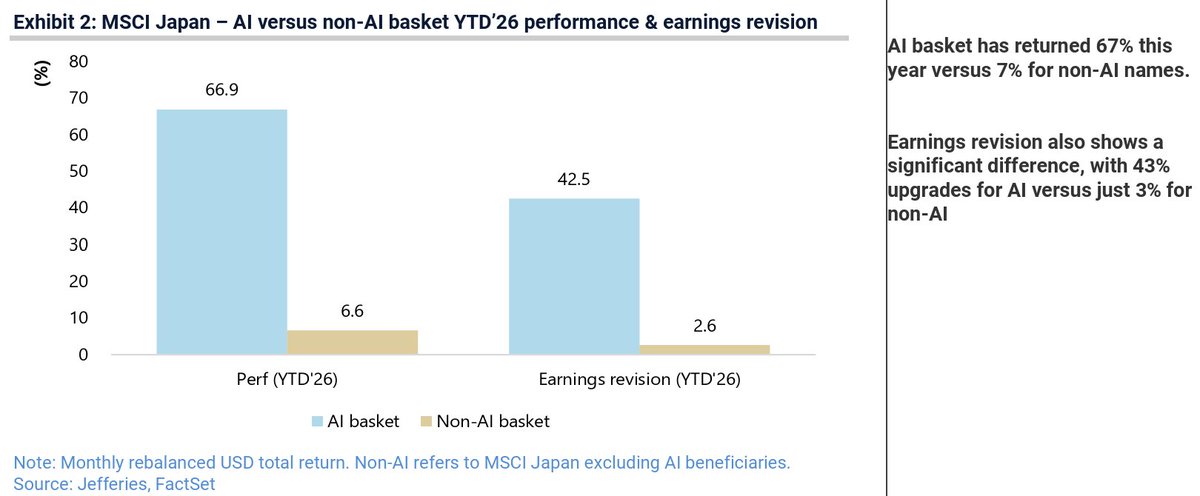

Index and passive ETF investors should be thinking very carefully about their exposures given the extremes we are seeing in markets.

The herding into AI-related names is a global phenomenon, and Japan is no exception.

While not as extreme as Korea, where memory-makers Samsung & SK Hynix have been the majority of the market's return, Japan has been a major beneficiary of AI-related demand.

If you own an index fund or passive ETF, or a benchmarked active manager for that matter, you should be thinking carefully about historical precedents where a single thematic is driving markets.

It has historically not ended well.

For wholesale investors interested in strategies with attractive potential returns that have minimal exposure to AI-related demand, visit Senjin Capital's website, sign up to our newsletter, or DM me.

4

981

"Shadow Activism": - actionable mid-large cap idea (for wholesale investors only).

Mitsui OSK - diversified shipping business.

- Market cap US$12.4bn

- liquidity US$170m /day

- price/book 0.7x

This opportunity looks to have potential for above-market returns through realisation of excess cash and real estate holdings to improve cash returns to shareholders.

For wholesale investors, to learn more, visit the link in the comments.

1

1

8

3,696

1,001

Why do public companies in Japan often trade for 1/3 of the value a private equity fund would pay to acquire them?

Or another way to say it, why is the underlying value often worth 3x the public market price?

I discuss this dynamic in the video below, and more about the opportunity in deep value shareholder activism in Japan in the full video I have linked in the comments.

To learn more:

For wholesale investors, visit Senjin Capital's website, sign up to our newsletter, or direct-message me.

3

3

14

4,343

When you can't make the event in person, so instead your face takes over a whole wall of the conference hall! 🫣

Despite not physically being there due to the Jefferies events in Sydney and Melbourne on Monday & Tuesday this week, it was great to be part of an excellent panel on engagement investing in Japan, for the 375 audience members in the room for the CFA Society Japan - 日本CFA協会's annual conference on Wednesday.

Those who could get past the gigantic head peering down at them (my hat size is already extra-large!), got to enjoy insightful comments from highly experienced engagement investors such as Tsuyoshi Maruki, Nao Makino, Zuhair Khan, expertly hosted by Tracy Gopal, CFA.

The panel was preceded by a presentation from James B Rosenwald III (another "James" who prefers to be called "Jamie" in everyday conversation), calling out poor behaviour from law firm Nishimura & Asahi in seeking to assist Japanese management teams to entrench themselves and continue to ignore the interests of outside shareholders.

"Activist" investing used to be a dirty word in Japan. The CFA Society's attention to the space, following on from front-page discussions of the benefits of activist investing in the famous Nikkei newspaper, shows just how far Japan has come.

Thank you Aki MATSUMOTO, CFA, MBA and the other organisers for putting on such a great event, and to the attendees for your attention and great questions.

1

7

1,738