60% of all listed stocks in Japan trade below book value. Follow me on a journey to explore. *hint* governance matters. Not giving investment advice.

Joined March 2023

- Tweets 2,897

- Following 811

- Followers 8,109

- Likes 8,259

420 Photos and videos

Pinned Tweet

Apr 30

I've been thinking a lot recently about what narratives could modify the euphoric investing landscape to a more moderate or even bearish one.

Simply put I think it goes like this:

Narrative 1: "We cant spend this much anymore"

collides with

Narrative 2: "They wont let us spend this much anymore"

1 is a markets narrative, 2 is a political narrative

1

9

3,942

Japan Deep Value retweeted

Jun 13

Trend Micro $4704

¥766B global cybersecurity company, founded in Japan in 1988 and now one of the oldest pure-play security vendors in the world. It protects enterprise endpoints, servers, and hybrid-cloud workloads through subscription software (XDR, threat detection, cloud security) — the kind of mission-critical, contract-locked tooling that's deeply embedded in IT stacks and painful to rip out. The economics show it: 77% gross margins, a 34% return on equity, and earnings that grew 34.7% last year.

The reason it's interesting is the price. ¥766B buys the whole business, but ~¥229B of that — nearly a third of the market cap — is just net cash sitting in the till, with zero debt. Strip it out and you're paying an enterprise value of only ~¥537B for a global security platform: roughly 6.3x EBITDA and under 2x sales. Flip the ~20x forward earnings multiple and that's a ~5% earnings yield on a 34% ROE compounder — at a time when US cyber peers like CrowdStrike, Palo Alto and Zscaler trade north of 50x earnings. Shareholders are paid to wait, too: a ~3.1% dividend at a ~71% payout plus steady buybacks, a ~4.5% shareholder yield, all resting on a fortress balance sheet.

The catch is growth. Revenue at only ~9%, and the stock sits near its 52-week low (¥5,900 against a ¥10,935 high) as the market frets about share loss to faster-moving rivals and Microsoft's security bundling.

Not investment advice.

2

14

2,530

Japan Deep Value retweeted

Most people should be taught over and over that the world isn't zero sum in all but the most extreme cases. Would help society and people's brains greatly.

14

7

112

9,901

Jun 11

an MBO rumor that fails to materialize is one of the worst things that can happen to a stock in Japan

2

1

10

2,345

12 Jan 2024

There have been a few posts and replies on this company already but I think, given the absurdity of the situation, its worth its own post, especially given the recent filings. The company is Hi-Lex 7279.T. Yesterday, the founding family upped its position from 25.7% to 27.3% (they now control a total of 35% of the vote, through joint filings). @TeddyOkuyama has a nice post about this company already.

Hi Lex is trading at 30% of its tangible book! They have 54bn yen of redundant (and liquid) cross shareholdings (100% of its mkt cap). 35bn yen of net cash (64% of its mkt cap). 9bn yen of receivables and 64bn yen (120% of mkt cap) of property and other assets.

Last year, the company published this "defense from TOB" document. hi-lex.co.jp/wp-content/uplo…. Within this anti-capitalist tirade, management ironically talk about corporate governance and free markets....I have no idea what motivated them to publish this, given there has not been a public activist campaign since 2007, when Steel Partners recognized the deep value opportunity here. warrenlichtenstein.com/media…

Interestingly, the company meets all of the requirements to move up from TSE Standard to TSE Prime, which would result in something like 50 days of volume of passive buying. In theory they should love the idea of this, given that the stock is so illiquid, higher passive ownership would serve as an even stronger barrier to potential activism. So why are they not applying? My view is that they don't want to be on a TSE "name and shame" list of companies trading below book value...and feel like hiding out on TSE standard will help them fly under the radar.

From these insider share purchase filings yesterday, one can assume that the family is either trying to secure even more voting control to block a potential activist campaign, or in preparation for some sort of family buy out (so they don't have to deal with the TSE "bullying" anymore). Buying out this company anywhere near where it is trading now, would be a form of robbery against minority investors, as its liquid securities and cash alone are significantly higher than the market cap here.

This situation is somewhat of a microcosm for the governance problems Japan has faced for the better part of 3 decades now. I'm not sure there is any opportunity here. It appears like this TOB defense and insider buying is more of a battle against TSE governance reforms, and the "name and shame" campaign (they plan to launch on Monday), more so than any specific activist campaign. It would be unfortunate, if this goes the way of 4987, Teraoka Seisakusho-- where ultimately management was able to rob minority investors and take the company private 50% below book value.

4

3

52

13,960

Jun 11

after a huge run up this has given back 50% in the last few months (along with many other deep value names) back to 0.35x book value. This is why they call Japan a trap, be careful out there.... the level of pain in this thematic is beyond most major bear markets let alone NKY near all time highs..

3

785

Jun 11

wow Japan small caps are all going to zero huh

4

1

27

5,496

Japan Deep Value retweeted

Jun 10

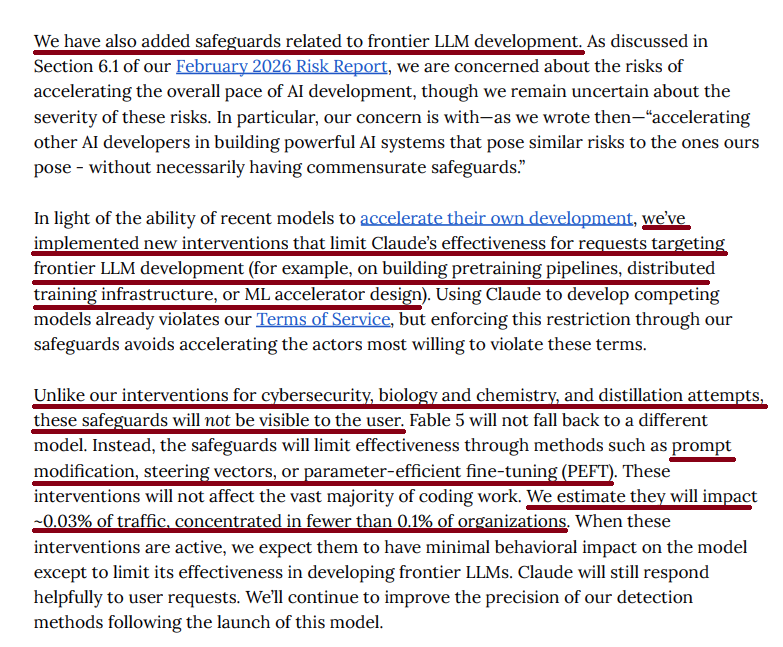

The AI Safety psyop is just to monopolize the ability to produce AI

Now Claude will literally sabotage your efforts to create any sort of AI of your own

They are literally seizing the means of AI production

When Fable 5 is used for frontier LLM development, it does not notify the user and instead limits the model’s capabilities through methods such as prompt modification, steering vectors, and PEFT.

Anthropic estimated that this would affect approximately 0.03% of traffic.

42

46

532

18,797

Jun 10

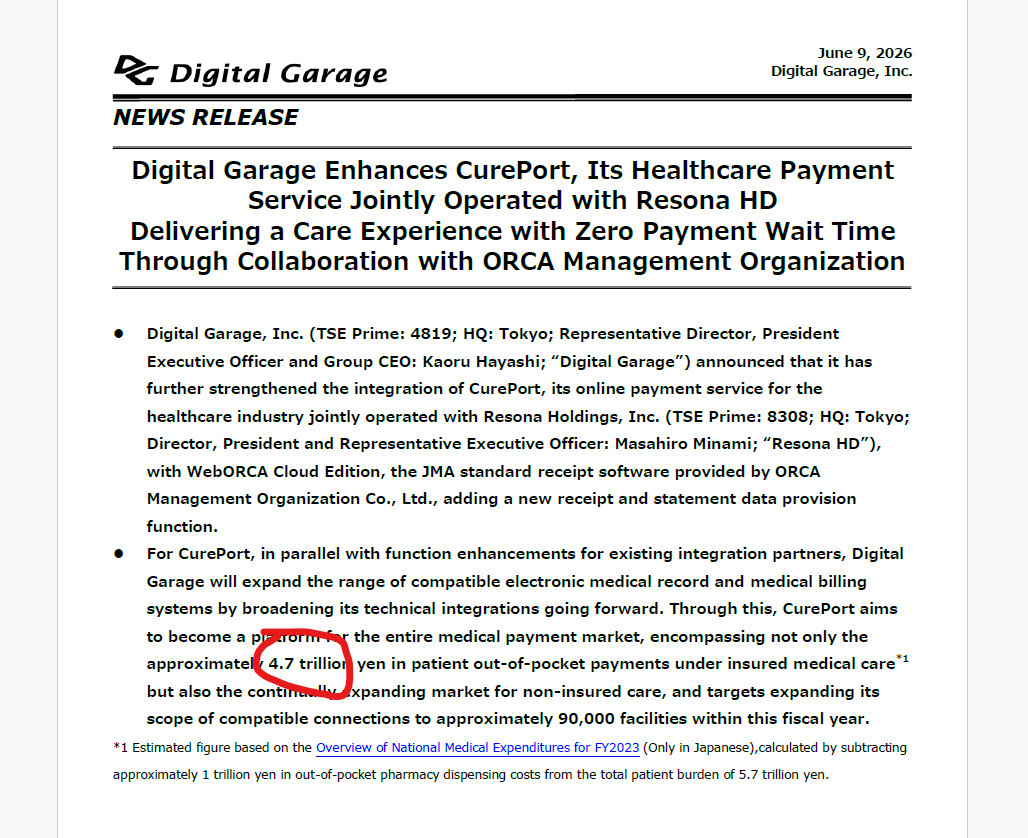

zaikei.co.jp/article/2026060…

so Trend Micro (cheapest global listed cybersec 5.3x EV/EBITDA) signals 100% payout ratio (70% div 30% buyback) which gets to a total of around 4.5% yield. They also join project glasswing, sign partnership agreements with Anthropic and rebrand a product to TrendAI.

Yet investors continue to sell/ignore this business because of legacy growth issues. They have nearly 30% of their market cap in net cash, no debt, had multiple P/E firms trying to take it private and are pursuing high growth businesses segments with top tier partners.

2

1

21

2,850

18 Dec 2025

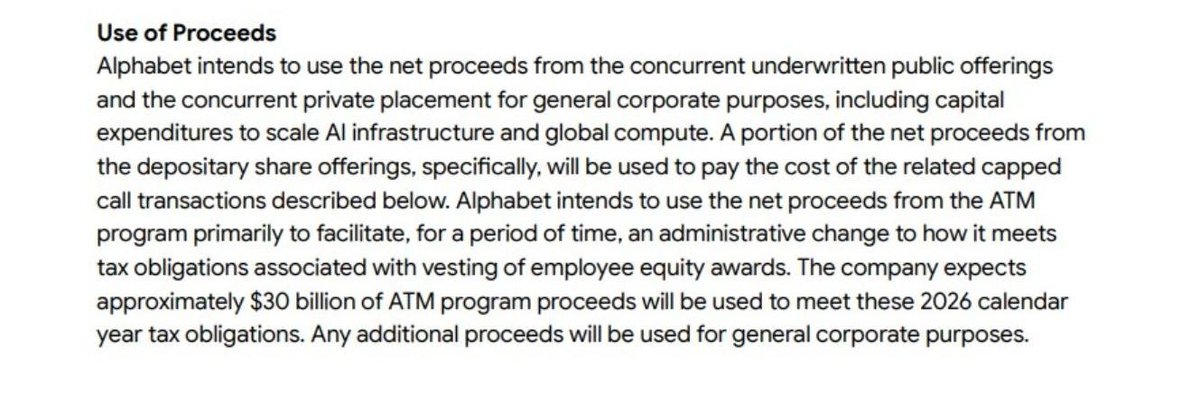

Digital Garage (4819.T) is one of those Japan “stub” trades that everyone has known about, and in the past had attracted Oasis to be a huge shareholder. On most simple SOTP math, you can conservatively mark the Kakaku. com stake cash/investments implied value for the payments/platform business and it starts to look like a negative-EV situation. DG trades around 7x P/CF (4–5x EV/FCF) which is a large discount to Asia and global fintech infrastructure co's.

I think the opportunity exists here because Resona, and not the SOTP math (which is all too common in Japan. Oasis’s disclosure shows 8,520,200 shares sold off-market to Resona at 5,972 just a few months ago (vs 2750 last) . So far this transaction has been a major catalyst for share price collapse... but I do think the market may be wrong here. It looks bearish, because the "big stick activist" is not there to push the SOTP discount angle on on the Kakaku. com holdings. But the market may not be considering that this is now a big strategic position for a major Japanese bank. Resona is explicitly positioning the DG payments technology to strengthen the settlement business and push cashless solutions across its 500,000 corporate customers via joint sales and product development.

This is why I keep coming back to the “Resona put.” A major Japan bank now owns over 30% and just recently paid a huge premium to last price for it. They are building distribution product around DG cashless payments. If the stock keeps trading at a discount to assets (currently negative EV assumptions can be made)... then the cheapest path to unlock value eventually becomes full control. I’m not saying take-private is imminent, but the endgame is intuitive: prove the Resona channel works, scale volumes, and let Resona remove the discount the public market is assigning because it fears a lack of "big stick" activism.

5

7

52

16,282

wider and wider it goes, 4819 position in Kakaku is now worth $850m vs their $575m mkt cap of the whole coming.... 4819 trading somewhere between 50-70% discounted to its NAV.... thats what zero faith in mgmt will do.

the interesting opportunity here would be if LY Line win with their higher bid... and do not let 4819 co -invest with them on the back end.

In that case DG would be squeezed out for more than their mkt cap in cash (after tax!) to add to their already significant net cash position and thriving payments business

1

5

1,305

Jun 10

DG mkt cap = 88bn JPY Kakaku holding = 136bn Net cash = 32bn (approx) VC investments = 10-15bn (approx) Payments biz valuation (earnings and GMV based vs comps) = 100-150bn Pretty easy to get to a 70% SOTP discount.

1

597

Jun 10

so a Facta article comes out on Kosaido (7868.T), saying that KKR is looking to buy their Tokyo cremation business for 150-180bn yen (current market cap is 81bn and its not their only business) .. the current market is absolutely brutal for catalyst/special sits in Japan

3

1

12

3,900

the scale of destructive selling going on underneath the hood in Japan now is starting to look like a moderate deleveraging event (aug 2024, april 2025, etc..)... Index is not telling the story at all

6

4

56

13,971

wow this is even more insane today. governance reform trade is over it seems

1

1,143

May 28

19% 1 hour rally from the open in a Japanese large cap is something I have rarely seen... .especially after a 240% 2 month rally without a drawdown. very impressive stuff going on

2

26

4,612

two days in a row, 20% intraday rally in under 2 hours...

1

772

Japan Deep Value retweeted

May 29

Riken Keiki $7734 FY25 Update.

Equity Bit's base case is for ¥5000 per share or 37% upside from the most current price of ¥3650.

Equity Bits continues to believe that Riken Keiki remains materially undervalued.

Link in bio.

1

3

12

2,835

5 Dec 2024

Hiding in plain sight is Kyocera ($6971), trading not far above its 2020 lows. Here's the kicker: the value of its 335M KDDI shares is worth substantially more than it was in 2020...now valued at $10.9bn (nearly its entire enterprise value of Kyocera when adjusted for treasury shares)

If you factor in $1bn in treasury shares, and Kyocera’s KDDI stake, its EV shrinks from $14.7bn to just $2.7bn. Adjusting the March 2025 EBITDA forecast of $3.2bn for the $335M in dividend income from KDDI, brings it to $2.9--resulting in an EV/EBITDA of under 1.

Governance stagnation, and the shockingly sluggish plan to sell down its KDDI stake have likely been weighing the share price down... I'm wondering why Elliot went after Tokyo Gas and not Kyocera-- an activist could do good work here.

12

6

93

22,120

May 27

Free idea #2 (I'm feeling generous today).

A new account/website called ZeroAlpha (since we all know ZeroHedge is dead forever)... Here is the logo

3

1

24

5,580