Ex @KyberNetwork @KrystalDeFi. Builder at @VemoNetwork and @Brownfiamm. Trying to retire on yield farming.

Joined April 2021

- Tweets 2,348

- Following 1,892

- Followers 1,639

- Likes 4,202

495 Photos and videos

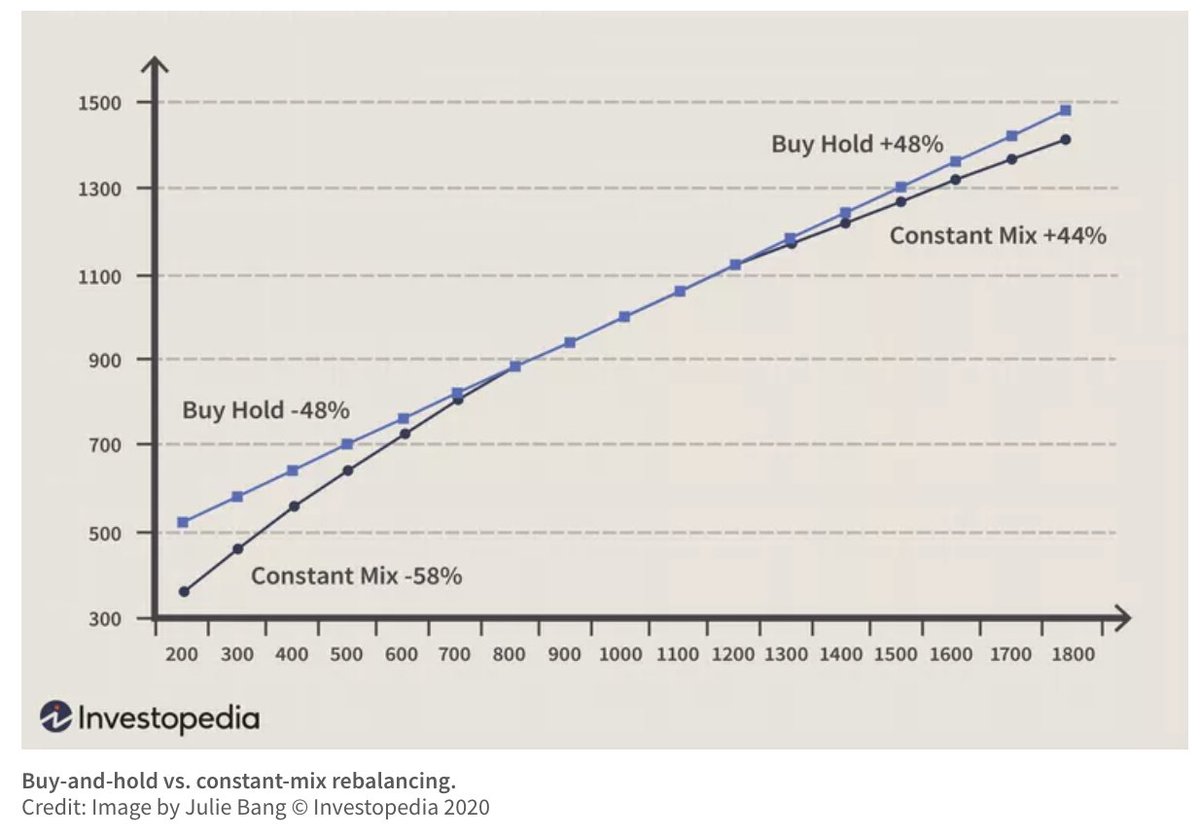

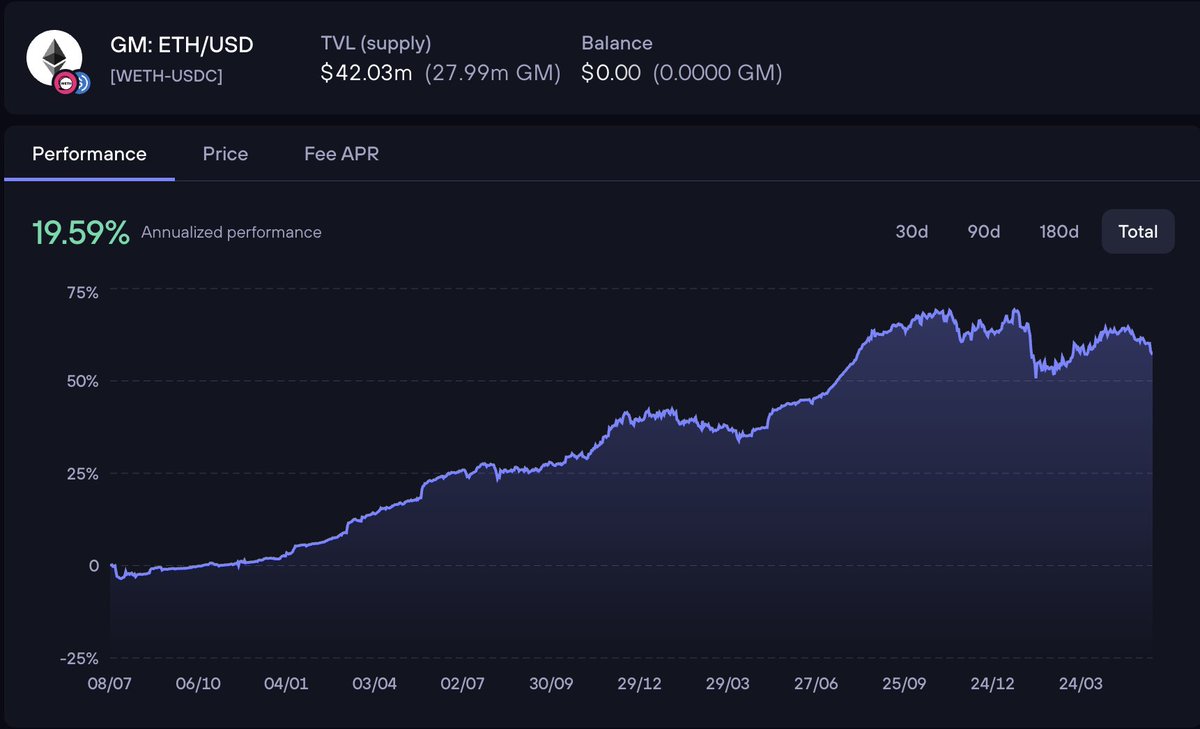

Imo, UniV2 curve is a good benchmark for measuring the performance of a MM platform in DeFi. This curve represents a constant-mix portfolio management strategy, one of the lowest-risk approaches to lping.

Why is this benchmark useful?

- Market making is inherently risky.

- Compared to UniV3 CLMM, UniV2 carries the lowest IL.

- The tradeoff is yield. With competition from high liquidity concentration of UniV3, simply sitting on a V2 curve earns almost zero nowadays.

- But if a protocol like @GMX_IO can offer 20% on top of the V2 baseline while keeping IL low, that is an excellent RR ratio, especially during a down cycle.

We took note of this, and we will be applying this benchmark in @brownfiamm V3. Stay tuned!

Jun 5

I missed the best LP benchmark in DeFi.

@JasonvuTech from @brownfiamm told me something I didn't know: @GMX_IO, the first perpetuals protocol to popularize revenue sharing, benchmarks its pools against @Uniswap v2.

The outperformance charts are public and the gap is insane. I've been using the wrong reference point entirely.

> I honestly don't know if there are structured products on top of GMX that hedge the 50% volatile exposure. Do you?

BrownFi v2's original pitch was that LPs earned more than simply holding the underlying 50/50 pair. That worked well until October's crash, where it basically stopped.

> BrownFi v3 is adding more customization layers with the explicit goal of competing against both benchmarks; not just v2 but GMX too.

The benchmark was always there. I just wasn't looking at the right chart.

3

361

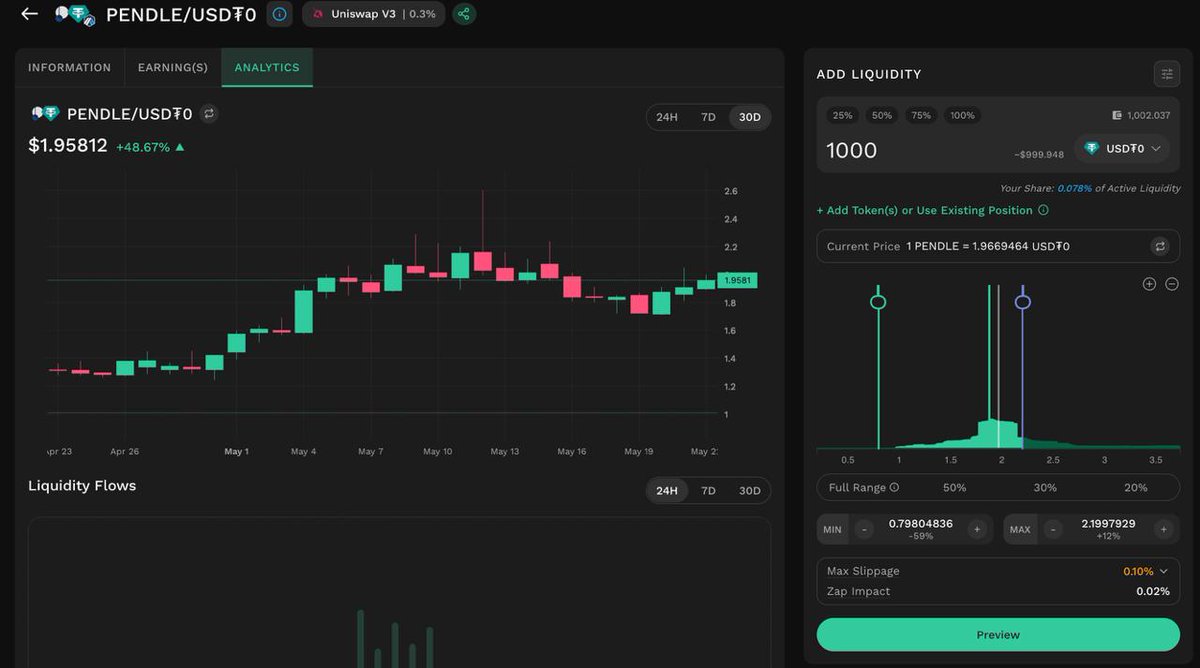

Update on the single-sided USDT Lping strategy

PENDLE has declined significantly since I entered the position, falling from $1.97 to $1.22. Despite the drawdown, I decided to harvest all accumulated fees and convert them into USDT.

The reasoning is simple: no one can reliably predict the market in the short term. If market conditions continue to deteriorate and PENDLE drops further, I do not want to watch the portfolio lose value without having a contingency plan in place.

By converting yields into stablecoins, I am gradually building a cash reserve. If the position eventually moves below my lower bound and I need to exit, I will still have capital available to deploy into a new opportunity. Preserving flexibility is more important to me than maximizing exposure during uncertain market conditions.

Check my portfolio here: debank.com/profile/0x0f45cd4…

I know many of you argue that my strategy/model does not completely eliminate IL. This discussion is mainly about IL theory and the mathematics behind it, and I am fully aware of that.

The point is that I never explicitly claimed in my article that “I can hedge IL.” This is a totally different story, I used to try that. Check my articles here:

x.com/JasonvuTech/status/185…

IL still exists. I simply choose a different approach to avoid being heavily exposed to it. You can check the part about IL in my latest article again:

x.com/JasonvuTech/status/205…

Another important point is that IL mainly matters to market makers. If you are using AMMs like Uniswap to provide liquidity and earn fees as an MM, then IL is naturally part of the game. I am not approaching AMMs that way.

Instead, I use AMMs as a system of multiple limit orders to buy low and sell high, similar to spot trading on a CEX. And I can earn incentives (in extra) while waiting for my LOs are triggered.

In that context, explaining IL theory to a trader does not really address the purpose of the strategy.

At this point, I think the theoretical discussion should stop here. A strategy only matters if it works in practice, not just on paper. Because of that, I decided to create a separate wallet and apply my single-sided USDC strategy in real trading, with the goal of increasing my USD-denominated balance over time.

🍀 Initial setup:

- 1,000 USDT as starting capital

- Around 0.02 ETH for gas fees on Arbitrum (not included in performance tracking)

- I identified PENDLE/USDT as a suitable pair because of its recent volatility and strong movement

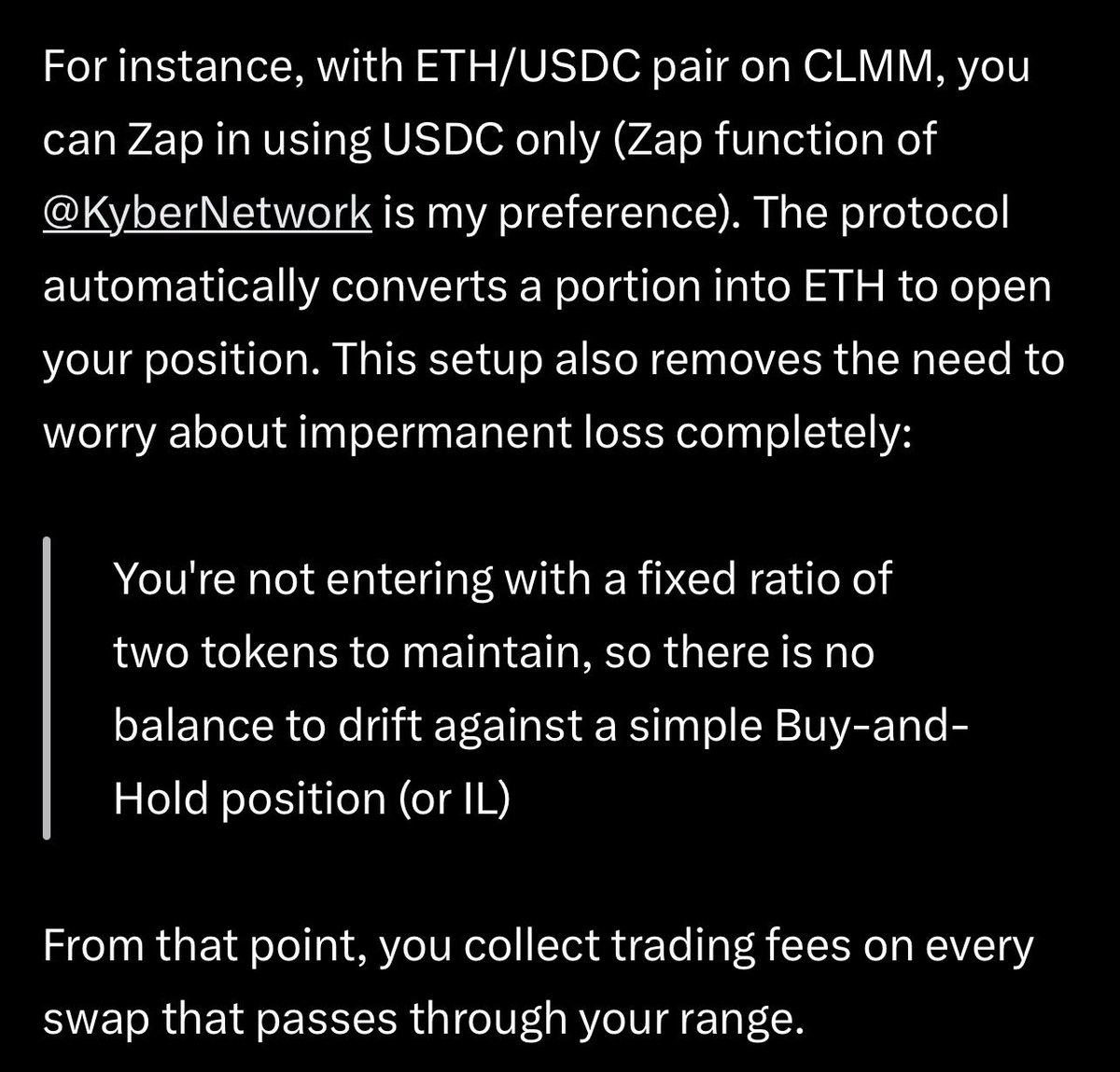

- I entered the position with a range of ($0.8,$2.2) using @KyberNetwork Zap function

🍀 Reasoning behind the setup:

- Worst scenario: if PENDLE falls below $0.8, I will cut the loss and move on to another opportunity.

- Base scenario: if PENDLE remains within the range, I simply collect trading fees and realize profits into USDT (or USDC) over time.

- Best scenario: if PENDLE rises above $2.2, I will already have gradually DCA-ed out through fees and trading execution. I can then close the position and move on to another setup.

👉 Put my Account here so anyone can track: debank.com/profile/0x0f45cd4…

2

218

"Low IL like Uniswap V2, high yield like Uniswap V3" sounds too good to be true, but that is exactly what we are building toward at @brownfiamm .

Our latest version is almost ready to launch. Before we do, we want to make sure the pools are set up in a way that actually fits what LPs need. So we are running a short survey to understand your experience, your pain points, and what you look for when providing liquidity.

It takes 2–3 minutes and is fully anonymous:

forms.gle/e2xzhCkrzK2hzkYAA

If you know other LPs who would have useful input, please pass it along. 🙏

Thanks for your help @Neoo_Nav @itsvietquoc @0xcarnation @crypto_linn @jarvisnnn @lochie_sol @meta_world_peas @DeFiVoyager_X @NaveenCypto @DeFi_Perryy @DeFi_Ted @SpotWiggum @ruwaiting4 @ayvee_bera @Joedark01 @0xDevinG @0x_vikt0r

2

5

25

1,594

same energy here

May 23

My new LP strategy is simple:

I don’t care if the token already pumped hard 👀

I enter with SOL only and set my DLMM range 50% lower.

If it keeps running → I farm fees

If it dumps → the position automatically buys lower.

And if the fees become weak, I exit fast even with a small loss.

At the end of the day, I only want pools that keep printing 🔥

solana:5hiLgyybrAYPpUwNFa38agfZ8iEtnahWKAPixcfspump

#Solana #Meteora #DLMM #LP #DeFi #Memecoins @MeteoraAG

4

421

I know many of you argue that my strategy/model does not completely eliminate IL. This discussion is mainly about IL theory and the mathematics behind it, and I am fully aware of that.

The point is that I never explicitly claimed in my article that “I can hedge IL.” This is a totally different story, I used to try that. Check my articles here:

x.com/JasonvuTech/status/185…

IL still exists. I simply choose a different approach to avoid being heavily exposed to it. You can check the part about IL in my latest article again:

x.com/JasonvuTech/status/205…

Another important point is that IL mainly matters to market makers. If you are using AMMs like Uniswap to provide liquidity and earn fees as an MM, then IL is naturally part of the game. I am not approaching AMMs that way.

Instead, I use AMMs as a system of multiple limit orders to buy low and sell high, similar to spot trading on a CEX. And I can earn incentives (in extra) while waiting for my LOs are triggered.

In that context, explaining IL theory to a trader does not really address the purpose of the strategy.

At this point, I think the theoretical discussion should stop here. A strategy only matters if it works in practice, not just on paper. Because of that, I decided to create a separate wallet and apply my single-sided USDC strategy in real trading, with the goal of increasing my USD-denominated balance over time.

🍀 Initial setup:

- 1,000 USDT as starting capital

- Around 0.02 ETH for gas fees on Arbitrum (not included in performance tracking)

- I identified PENDLE/USDT as a suitable pair because of its recent volatility and strong movement

- I entered the position with a range of ($0.8,$2.2) using @KyberNetwork Zap function

🍀 Reasoning behind the setup:

- Worst scenario: if PENDLE falls below $0.8, I will cut the loss and move on to another opportunity.

- Base scenario: if PENDLE remains within the range, I simply collect trading fees and realize profits into USDT (or USDC) over time.

- Best scenario: if PENDLE rises above $2.2, I will already have gradually DCA-ed out through fees and trading execution. I can then close the position and move on to another setup.

👉 Put my Account here so anyone can track: debank.com/profile/0x0f45cd4…

2

1

13

1,399

jasonvu.tech (🦇🔈 ,💧,🐻⛓️) retweeted

May 21

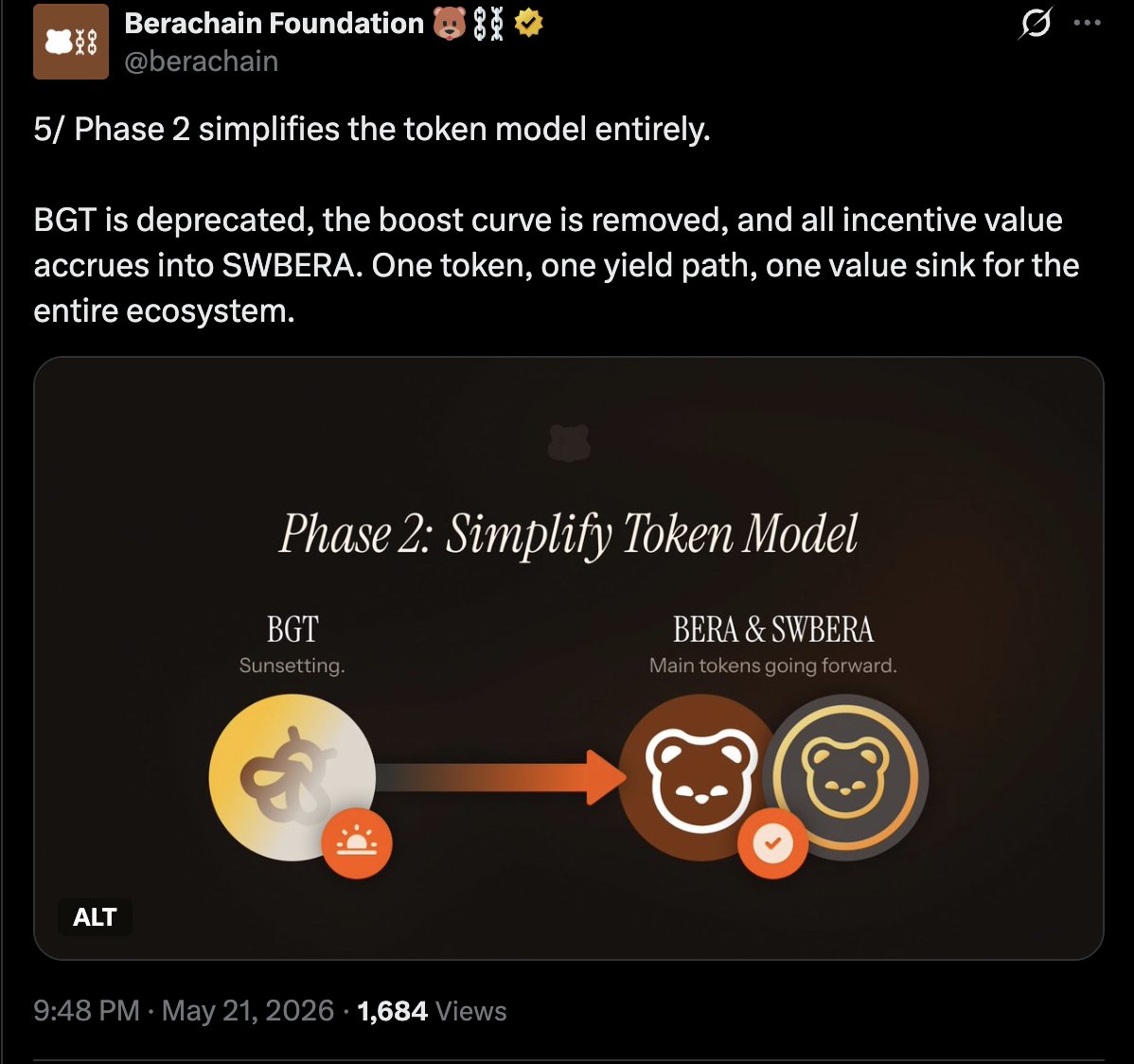

POL Next is centered around simplicity, efficiency, and scalability.

As a retail user, you no longer need to worry about farming BGT, boosting validators, or claiming fragmented yields. All you need to hold is the yield-bearing token swBERA.

This is a major improvement to Berachain POL system coming next month. BrownFi’s next version will also launch around the same time. Stay tuned.

1/ Berachain's Proof of Liquidity is evolving.

As crypto adapts to fit a more mature crowd of asset allocators, the Beras are making some changes.

Here's everything you need to know about the new PoL 🧵

ALT Introducing Berachain Proof-of-Liquidity Next

1

10

337

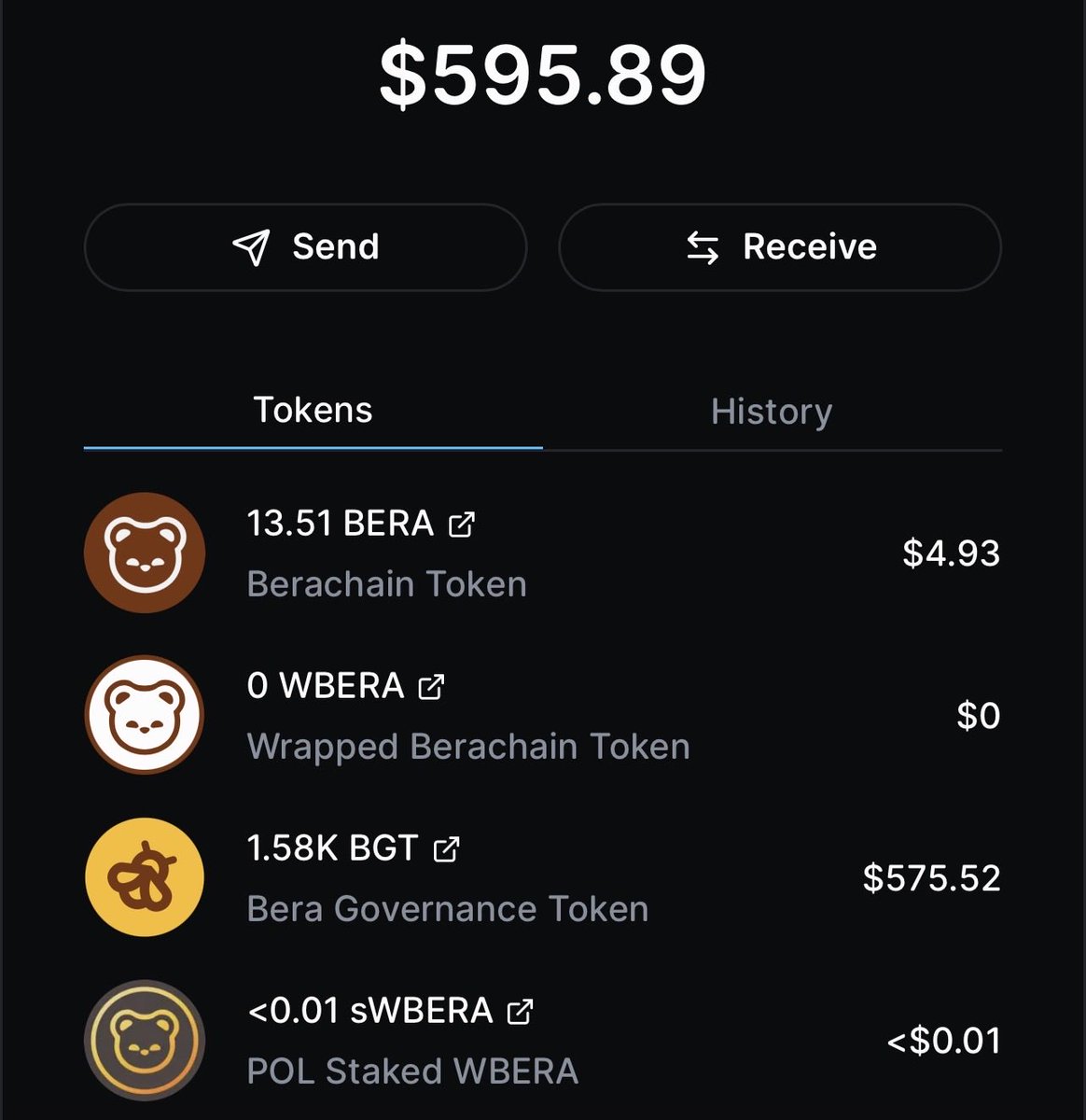

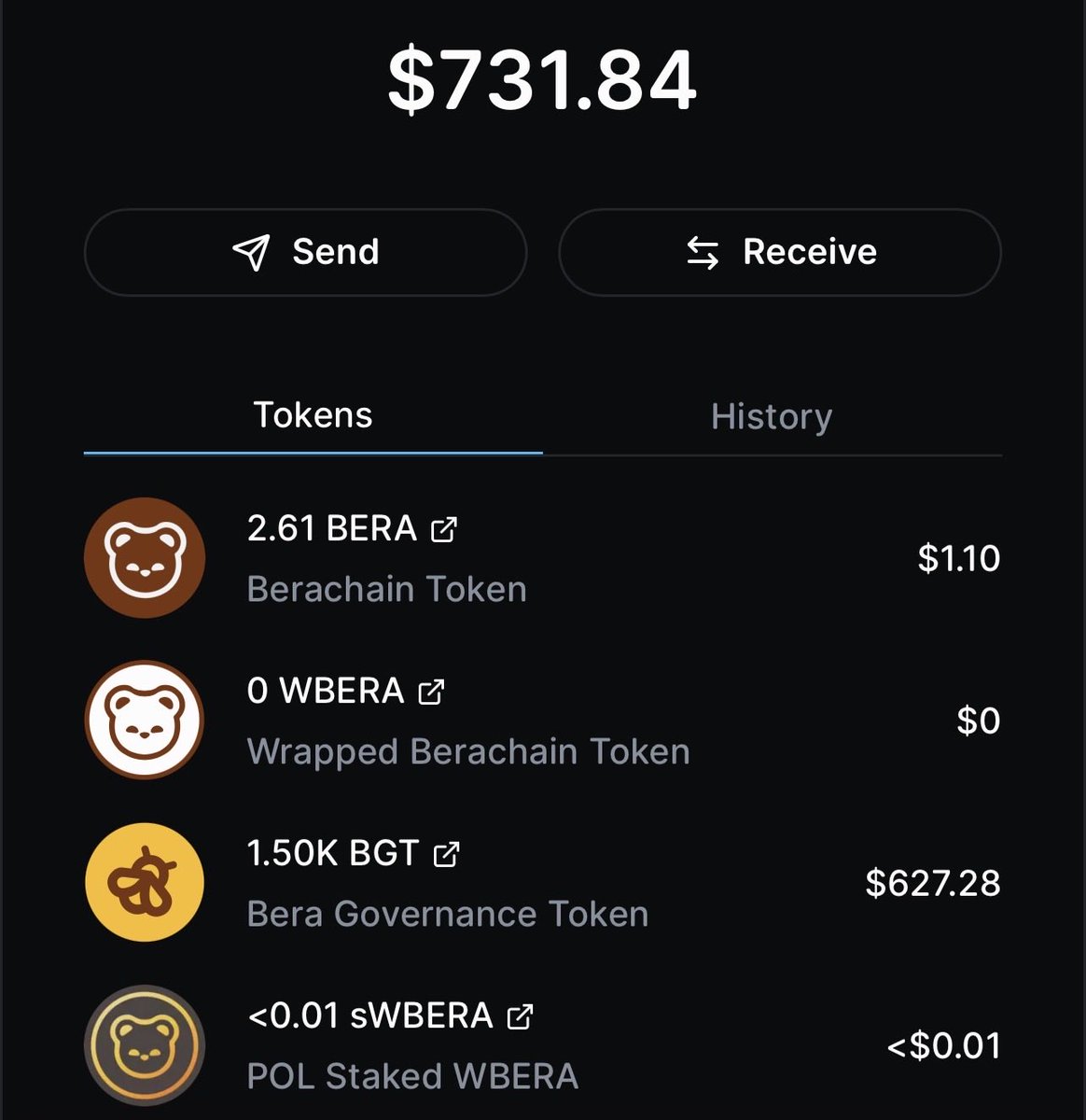

Day 202 of stacking BGT until BERA reaches $10

Ok, so POL NEXT will come very soon which will consolidate all value back to one single yield-bearing token. I decided to redeem all BGT to BERA. Then swap them to swBERA.

Day 179 of stacking BGT until BERA reaches $10

Long time no update due to "builder mode" turned on. But I still stay here and do go anywhere. And my cumulative BGT is 1,580 BGT.

3

1

20

1,292

How the hell you guys are so serious about IL term in this article?

For me, IL is the discrepancy between Buy & Hold 2 tokens in wallet vs. lping. That's all!

You cannot apply IL term to single-side USDC strategy. It's similar to trading spot. When you swap USDC to ETH, then ETH goes down. You don't say it's IL, right?

So, take it easy. IL or not IL is not the point. The point is the strategy can earn money for you consistently or not.

2

6

1,276

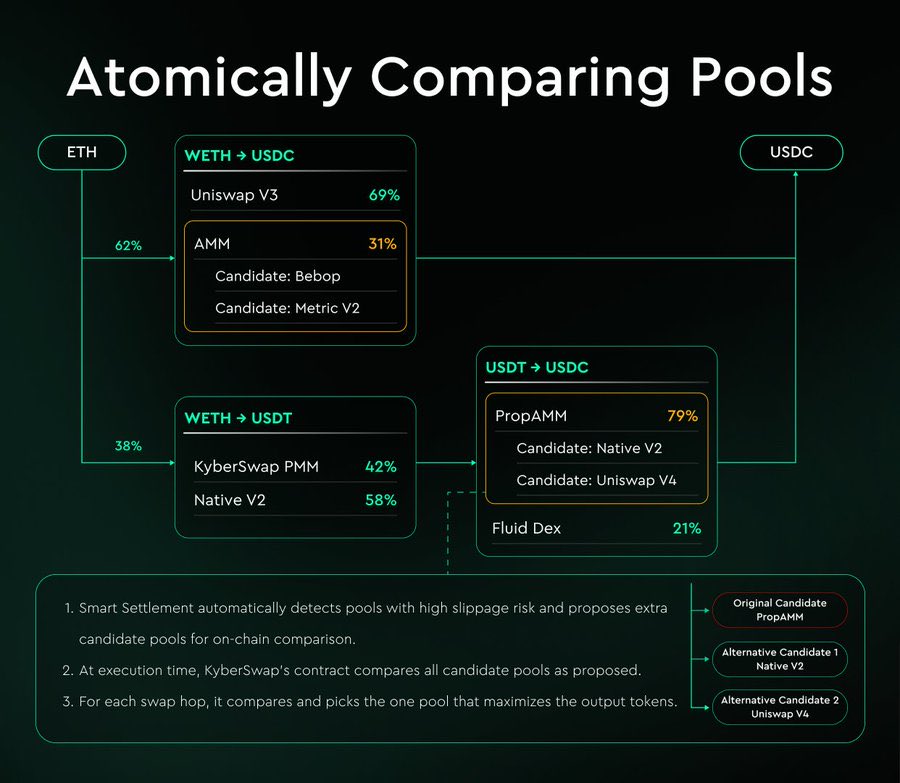

Smart Settlement is the exact feature that I'm looking for from the best aggregator. 🤩

So here is the quick take:

1- Issue:

Due to various reasons (sandwich attack from MEV bots, super volatile tokens like meme, PropAMM spoofing, etc.) that makes the final amountOUT takers can get isn't good as what they see on UI.

2- Solution:

@KyberNetwork do 2 things: (1) add an extra-spread on a unreliable quote to make it less competitive and (2) prepare more than 01 candidate for each hop to as a backup during the execution.

3- The result:

- Takers can get the best rates

- Number of failed transactions is reduced

- Create a fair competition between liquidity sources (if you want to win the transaction, you must provide reliable rates) which make more competitive rates to takers at the end of the day.

👉 Try a swap on Kyber to see real result here:

kyberswap.com/swap/ethereum/…

May 14

BREAKING: A major step forward for aggregator’s routing begins now on EVM.

Introducing Smart Settlement, an execution upgrade for more resilient swaps to protect users from slippage, PropAMM manipulation, MEV, JIT, while bringing even Higher Swap Output.

You’ve got the best quote, now you get the best execution.

1

14

2,409

I decided to end this experiment due to slow process, even with a small profit $5.54.

I will think of setting a new experiment with bid-ask flip on @MeteoraAG with more exciment later.

Update on hybrid strategy using @MeteoraAG bid-ask

Yesterday, I flipped twice—during the first and second moments when BTC flash-dumped and then rebounded. That would have given me $8.89 in unrealized PnL.

1

3

380

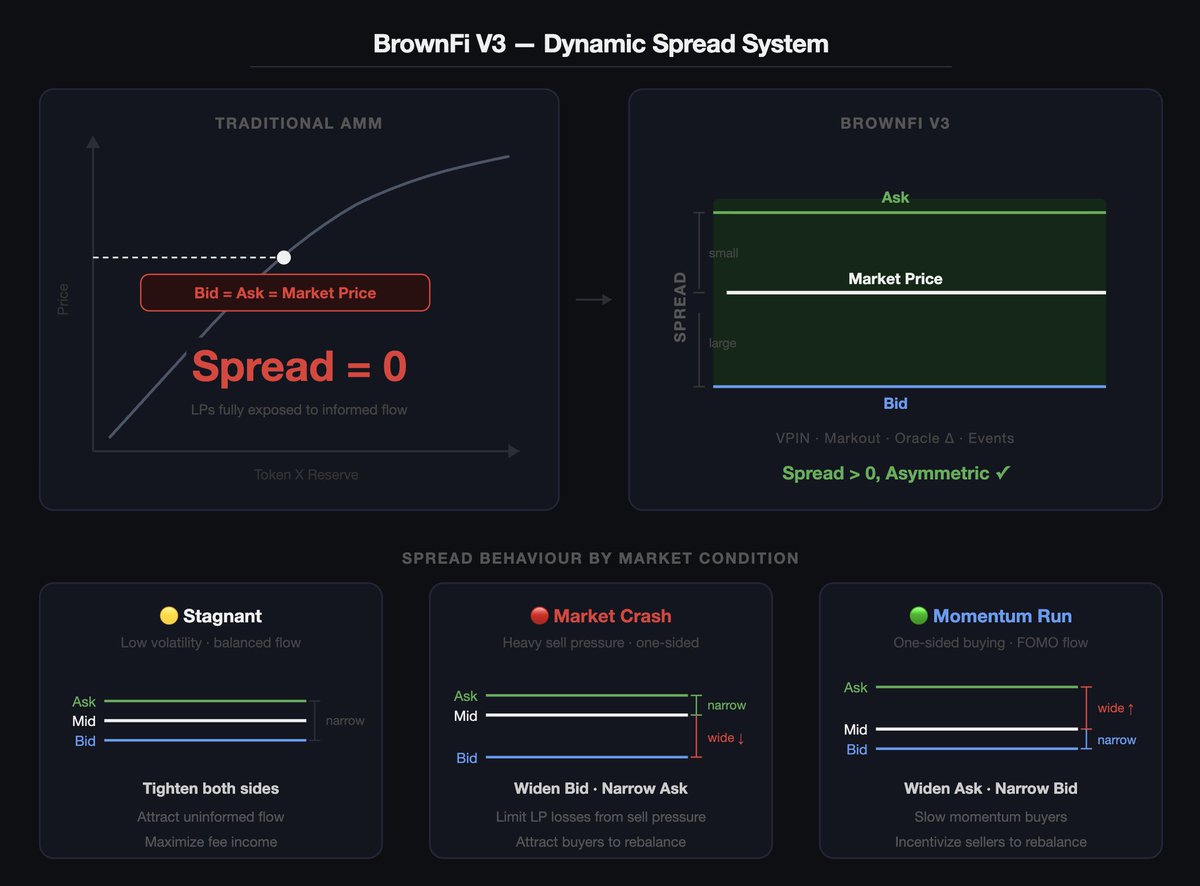

Spread is the most powerful tool to deal with adverse selection, stale price and other on-chain issues. And now, we bring it to you with our upcoming V3.

May 6

BrownFi V3

█████████▒ 90% Complete 👀

In traditional market making, bid-ask spread is the top 1 tool to protect LPs against informed traders (or adverse selection). But in most AMMs, Spread = zero, where Bid and ask collapse to the same point on the bonding curve. LPs are fully exposed.

BrownFi V3 changes this.

We built a dynamic spread system that responds to real market signals:

- Oracle price discrepancy

- Volume imbalance (VPIN)

- Markout & external price events

🟡 When market is stagnant (low volatility, balanced flow):

- VPIN is low → flow is mostly uninformed

- Narrow the spread

- Maximize trade volume → LPs earn more fee.

🔴 When market crashes (strong sell pressure):

- 📈 Widen Bid side → Bid moves further down

- Limit LP losses from one-sided selling pressure of base token.

- 📉 Narrow Ask side → attract buyers to get base token out, rebalance pool faster.

🟢 When market is in a momentum run (FOMO / one-sided buying pressure):

- Pool drains of base token as buyers pile in

- 📈 Widen Ask side → make buying base more expensive

- Slow down informed/momentum buyers extracting value

- 📉 Narrow Bid side → incentivize sellers to bring base back

- Pool rebalances before LPs take asymmetric inventory loss

With this design, each market regime can get a tailored response, not a one-size-fits-all fee hike like other AMMs. And this dynamic spread system can serve as a real market making desk in Defi.

6

495

jasonvu.tech (🦇🔈 ,💧,🐻⛓️) retweeted

May 4

Advice:

Taking Profits

- When you make profits, stable a portion of it up, no matter what the current market price is.

- Move those profits to another wallet and make it your rainy day fund.

- Use those stables to buy bigger dips on red days from high conviction projects as a DCA plan.

Position Sizing

- Standardize the amount you LP with depending on the market cap of the project you plan on positioning yourself with.

- It should be a very rare case that you full port or use most of your portfolio balance on a single position.

- This allows you to only risk what your willing to lose when things don't go as expected.

- When you size up on a position and things go wrong, it could ruin your entire weeks or even months profit.

Apr 30

LP Army Liquidity Card Advice Competition is LIVE.

Show your 7D performance and drop one piece of LP advice you wish you knew when you started.

Highest % PnL wins. Best advice wins. You can take both.

Export your liquidity card, share your wisdom, and compete for 1,000 USDC.

Details below 👇

1

3

30

1,699

Update on hybrid strategy using @MeteoraAG bid-ask

Yesterday, I flipped twice—during the first and second moments when BTC flash-dumped and then rebounded. That would have given me $8.89 in unrealized PnL.

BTC breaks $80k. I decided to switch to risk-on mode:

- Swap 733.34 USDC to 0.00910282

- Then re-add to ask side of the position on @MeteoraAG

2

574

BTC breaks $80k. I decided to switch to risk-on mode:

- Swap 733.34 USDC to 0.00910282

- Then re-add to ask side of the position on @MeteoraAG

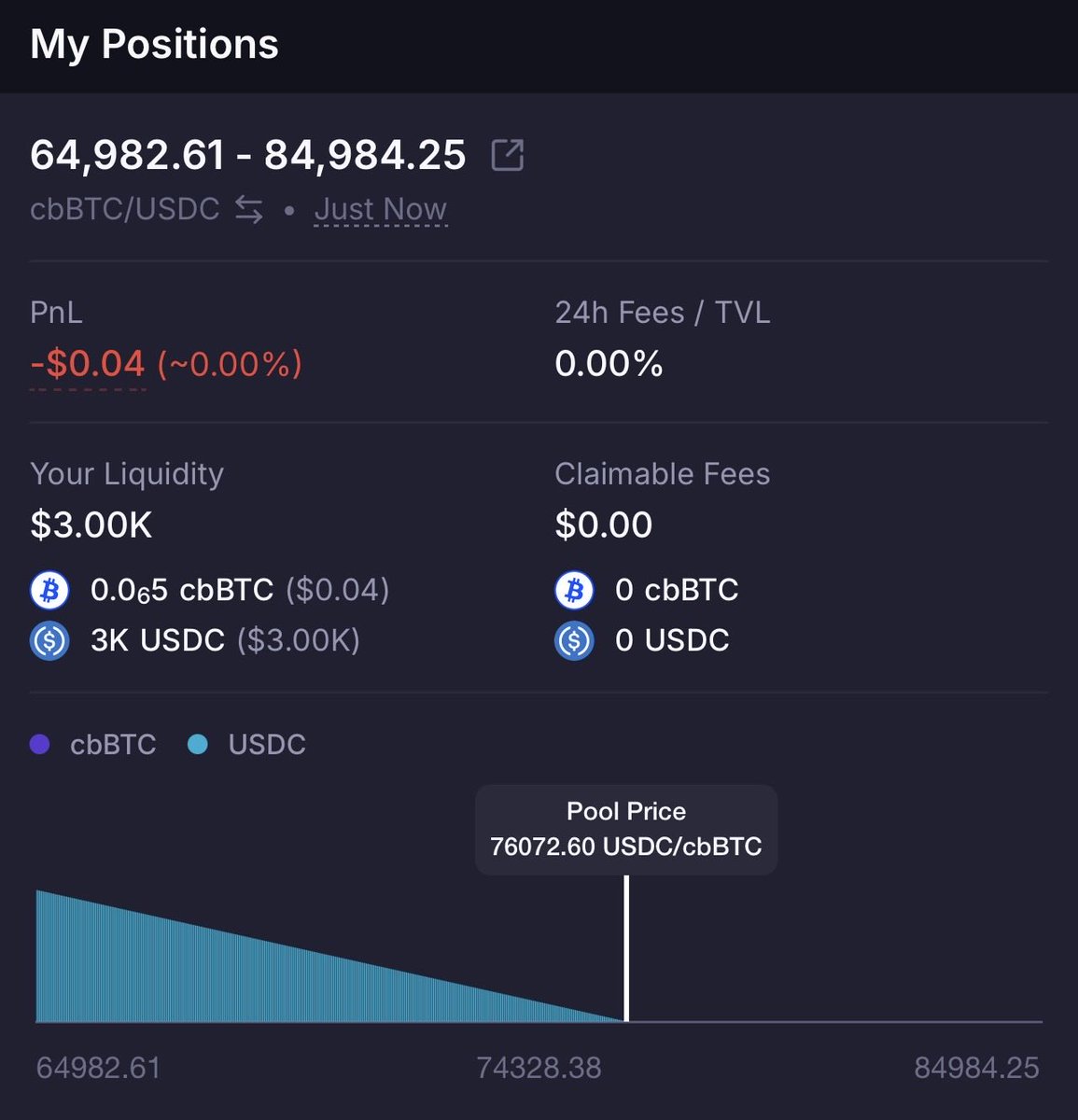

Day 2 on this DLMM hybrid strategy experiment

I'm impatient a bit when cbBTC hasn't drifted to my USDC bid position yet.

- I decided to remove 90 USDC, then swap to 0.00117777 cbBTC.

- Re-add 0.00117777 cbBTC to the current position.

This action doesn't change my NAV or PnL, but at least it will keep my position active all the time during this experiment.

6

613

Day 2 on this DLMM hybrid strategy experiment

I'm impatient a bit when cbBTC hasn't drifted to my USDC bid position yet.

- I decided to remove 90 USDC, then swap to 0.00117777 cbBTC.

- Re-add 0.00117777 cbBTC to the current position.

This action doesn't change my NAV or PnL, but at least it will keep my position active all the time during this experiment.

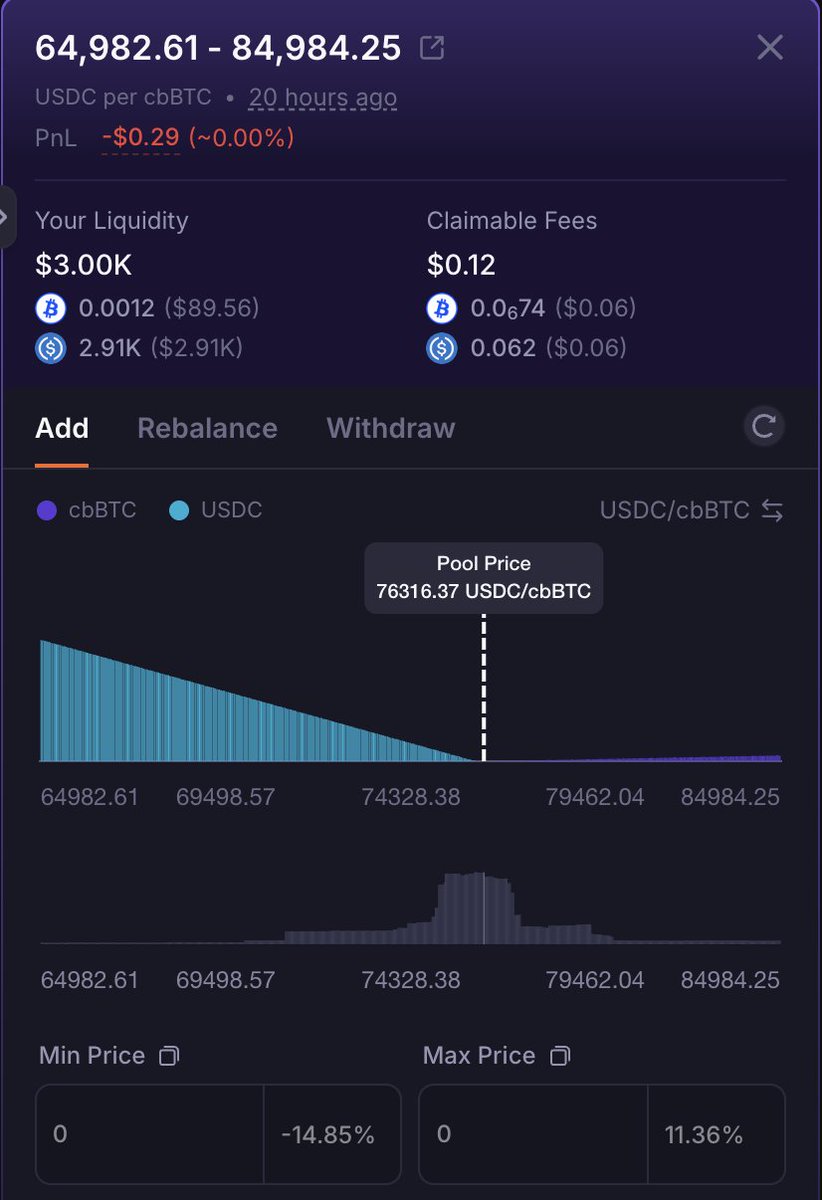

Hybrid strategy with DLMM

Trading volume across Defi space is reaching to ATL. Less volume, so less fees LPing can bring to you.

Instead of narrowing down the range to boost APR (but get higher IL) or lping into memes, I decided to experience a hybrid strategy combining between Lping & trading. I believe this strategy can bring me better pnl during this bear market.

And here is my setup:

- Initial capital: 3,000 USDC.

- Lping (bid-ask shape) into cbBTC/USDC on @MeteoraAG . I choose this pair because BTC has the lowest volatility among crypto assets during this tough market. And I also have the most confidence with this asset.

- Range: (65,000; 85,000)

- All yields/profits will be realized to USDC to simplify this experiment.

- I will create a Google Sheets for tracking in the upcoming days.

1

2

664

Hybrid strategy with DLMM

Trading volume across Defi space is reaching to ATL. Less volume, so less fees LPing can bring to you.

Instead of narrowing down the range to boost APR (but get higher IL) or lping into memes, I decided to experience a hybrid strategy combining between Lping & trading. I believe this strategy can bring me better pnl during this bear market.

And here is my setup:

- Initial capital: 3,000 USDC.

- Lping (bid-ask shape) into cbBTC/USDC on @MeteoraAG . I choose this pair because BTC has the lowest volatility among crypto assets during this tough market. And I also have the most confidence with this asset.

- Range: (65,000; 85,000)

- All yields/profits will be realized to USDC to simplify this experiment.

- I will create a Google Sheets for tracking in the upcoming days.

7

588

Day 179 of stacking BGT until BERA reaches $10

Long time no update due to "builder mode" turned on. But I still stay here and do go anywhere. And my cumulative BGT is 1,580 BGT.

Day 167 of stacking BGT until BERA reaches $10

And my cumultive BGT is 1,500 now. Don't know what POL - vNEXT will bring up to, but it seems a good news after all.

3

28

2,718

3

15

90

14,799

Don't really understand why people still mislead transaction fees as "chain revenue":

1- Take Berachain for instant, with tnx fee = 0.000000353 BERA, it means 3mil tnxs will cost you only 1 BERA ($0.4).

2- Tnx fees are captured by validators, and for now most of chains even Bitcoin and Ethereum, validators still need to rely on block rewards to survive.

Apr 23

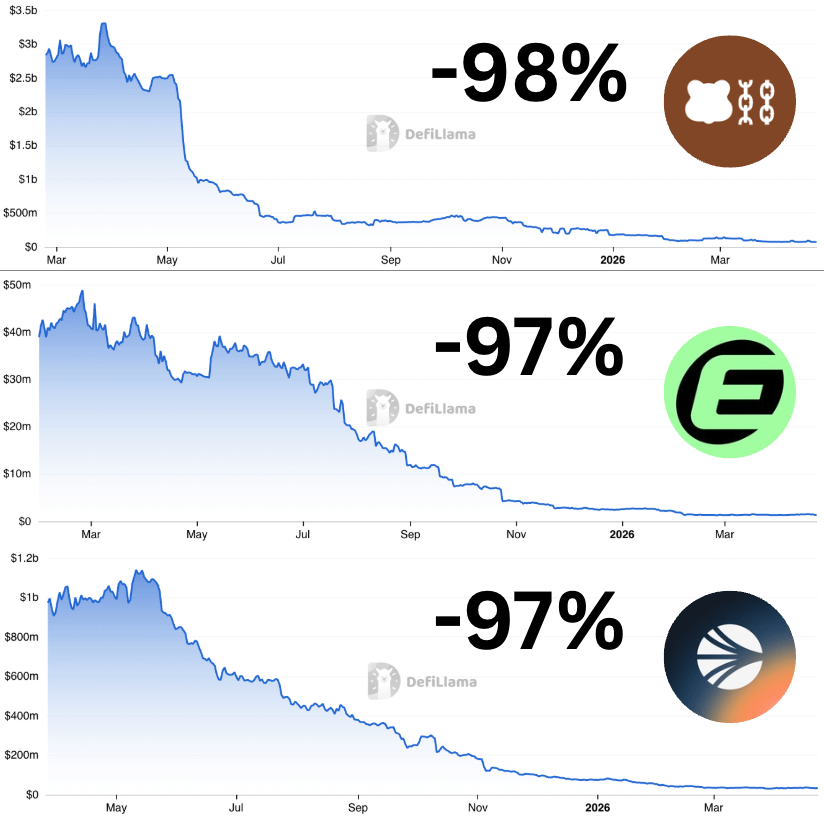

The 3 biggest chain flops of 2025:

1 | Berachain:

- TVL: $73.2M (-98%)

- Chain Revenue 24h: $34

- Raised: $142.1M

2 | Eclipse:

- TVL: $1.5M (-97%)

- Chain Revenue 24h: $0

- Raised: $65.1M

3 | Sonic:

- TVL: $33.3M (-97% in a year)

- Chain Revenue 24h: $125

- Raised: $61.3M

4

1

18

2,958