Fixing leaky narratives, blocked cash flows and valuation pipes. Investor & finance writer @FinancialMail. Markets, moats, mispricing.

Joined April 2026

- Tweets 43

- Following 305

- Followers 80

- Likes 19

9 Photos and videos

Pinned Tweet

What does The Investment Plumber do?

I look for leaks in the investment story.

(1) Fictional cash flows.

(2) Blocked drains in the boardroom.

(3) CEOs flushing shareholder money down the toilet.

(4) CEOs who think we are stupid.

(5) Goofball valuations held together with hope, duct tape and adjusted EBITDA.

Leaks. Lies. Clogged Valuations. Flushing Nonsense.

2

179

SpaceX is a great investment - 100x revenue. The smart money is chasing it. For every rand you invest you get 0.0001 cents of pure cash flow in ten years from now. #sarcasm #spacex #techbubble

71

🚨 COMMERCIAL REAL ESTATE INDUSTRY PARTICIPANTS — CONFIDENTIAL ENGAGEMENT INVITED 🚨

I am currently engaging with brokers, former employees, legal professionals, recruiters, and other industry participants regarding restraint-of-trade practices, recruitment restrictions, commission disputes, and potential anti-competitive conduct within South Africa’s Commercial Real Estate sector.

If you have experienced or witnessed:

• excessive restraint clauses

• intimidation linked to resignations or movement between firms

• commission withholding disputes

• coercive exit practices

• restrictive recruitment conduct

• pressure tactics designed to suppress competition

you are invited to contact me confidentially via LinkedIn.

🔒 Anonymous engagement is welcomed.

📄 Supporting documentation may be shared confidentially.

⚖️ Information received will be assessed responsibly and independently.

As a journalist and contributor to leading South African financial and business publications, I am currently conducting an independent public-interest investigation into these practices and their broader legal, ethical, and competition-law implications.

Industry participants should understand:

⚠️ restrictive contractual practices are not immune from scrutiny

⚠️ unreasonable restraints may not withstand legal examination

⚠️ conduct affecting competition and labour mobility can attract regulatory attention

⚠️ internal communications, enforcement patterns, and historical practices may become relevant where lawfully obtained

For years, many younger brokers and employees have entered agreements without meaningful bargaining power, without independent advice, and often without fully understanding the long-term implications of restrictive provisions imposed upon them.

These concerns are no longer being discussed quietly.

Questions are increasingly being raised regarding:

• competition law

• constitutional principles

• fairness in contracting

• labour mobility

• corporate governance

• ethical business conduct within the industry

This initiative is being pursued in the public interest.

Those with relevant information are encouraged to make contact.

#CommercialRealEstate #CompetitionLaw #CorporateGovernance #SouthAfrica #PropertyIndustry #RestraintOfTrade

1

1

73

Master Drilling sits right in the middle of the mining cycle. In my latest Financial Mail article, I looked at why Master Drilling’s deferred dividend is an important issue that requires a closer look. The issue is not just the dividend itself. It is what the deferral says about cash conversion, capital intensity, fleet utilisation, and whether accounting earnings are turning into distributable cash.

#MasterDrilling #MiningCycle #CashConversion #CapitalIntensity #DistributableCash

financialmail.businessday.co…

70

This is an excellent article. However, this remains a coal business, and the focus should be on coal-related matters, which are, unfortunately, still its core business. CEOs who stray too far from the core business often destroy value for all stakeholders. That is not in South Africa’s interest, especially when the country’s most urgent problem is unemployment, not climate policy. #CoalMining

#SouthAfrica

#EnergySecurity

#JobsMatter

#CorporateStrategy

#Thungela

miningmx.com/news/energy/651…

49

Check out my latest article: Balwin's buyout: flattering the wrong number linkedin.com/pulse/balwins-b… via @LinkedIn

63

Magnus buys securities or shares, while Piet buys businesses. That is why Magnus can't understand what Piet is doing and vice versa. Fact is - if you buy 100% of a business you will never pay a PE of above 20x. #JSE

#SouthAfricanBusiness

#SAInvesting

#ValueInvestingSA

#PrivateEquitySA

May 13

🔗 Link in Bio

Piet Viljoen’s local value bet vs. Magnus Heystek’s offshore strategy: The results are in, and the gap is closing. Who truly has the upper hand in this high-stakes showdown?

#BizNews #MagnusHeystek #PietViljoen #StockMarket #LocalVsOffshore

94

The Investment Plumber | Jeandré Pike retweeted

May 14

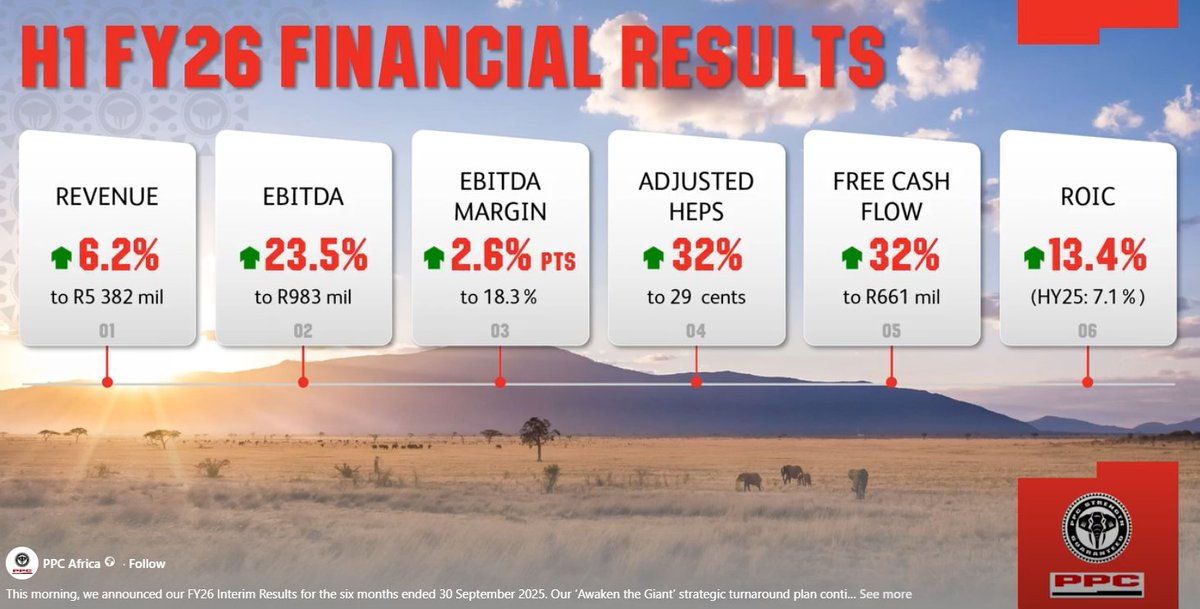

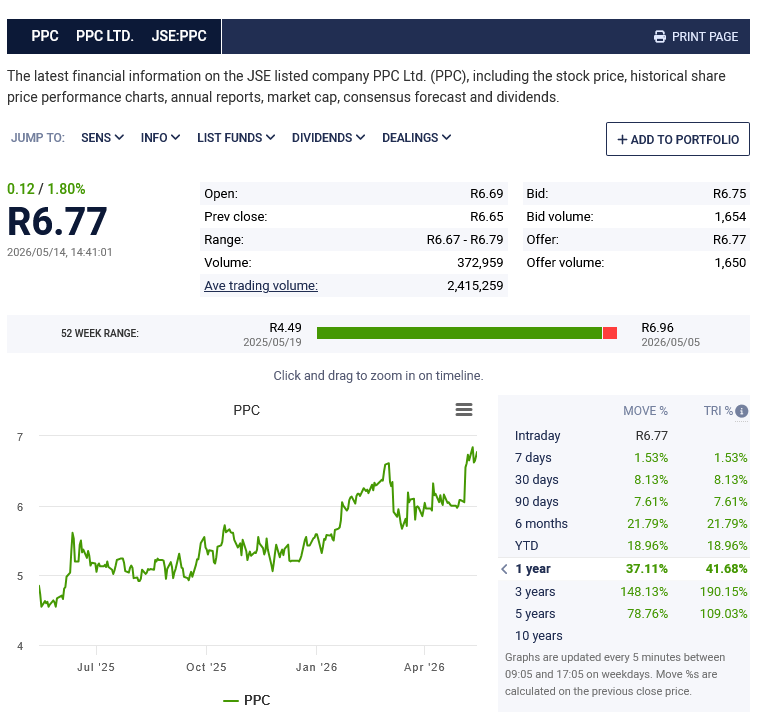

Teutonic tilt at PPC?

"...A rumour based on a heap of commercial sense might be worth paying attention to — particularly in a strategic industry where a long-dominant player could be a target."

financialmail.businessday.co…

2

1

801

If you are buying securities or shares offshore, I understand the argument. The S&P 500 at 25.8x earnings gives you a 3.9% earnings yield, which is barely above US inflation. That does not make much sense unless you fully buy into the hype and the growth story.

If you are buying businesses, which not many fund managers truly do, then South Africa can make more sense. There are companies offering sustainable earnings yields of around 15%, against local bonds near 8.8% and inflation just above 3%.

Most fund managers buy securities or shares, not businesses, which is why offshore makes more sense for them. #ValueInvesting

#OffshoreInvesting

#SouthAfricanStocks

May 13

Magnus Heystek: Why I (and my clients) still prefer offshore investments biznews.com/investor-insight… #

87

The Investment Plumber | Jeandré Pike retweeted

Thanks @FinancialMail @MarcHasenfuss Jeandre Pike for the copy on my comments regards the recent puff in the $JSEPPC PPC Ltd share price on rumours of a bid from the German company Heidelberg Materials

Teutonic tilt at PPC? financialmail.businessday.co…

1

2

5

1,717

The Investment Plumber | Jeandré Pike retweeted

May 7

🚨 BURRY: THIS IS WORSE THAN 1999

THE MAN WHO PREDICTED THE 2008 COLLAPSE NOW SEES TODAY'S NASDAQ AS A MORE DANGEROUS BUBBLE THAN THE DOT-COM ERA

$SNDK is up 4,000% in the 12 months

$QCOM's 1999 peak was 2,620% and marked the final top

Three months later, Nasdaq collapsed 78%

Current S&P concentration is just ugly

The top 10 stocks now make up a record 41.2% of the S&P 500 — the most lopsided US market in 150 years

Michael Burry has placed his BILLION SHORT: $912M in $PLTR and $187M in $NVDA puts as of his last 13F

He predicts 3 paths from here:

1. MELT-UP — Momentum sucks in the last FOMO buyers. The top gets more extreme, the crash gets even worse. Target: -75%, dot-com style

2. LIQUIDITY SHOCK — A rate surprise, a geopolitical event, something BREAKS. Markets reprice in hours. Target: -40% in a single quarter

3. DISTRIBUTION — Insiders sell into strength. Sideways chop lulls everyone, then the rollover. Target: -50% over 12-18 months

All three end with mean reversion that wipes out latecomers

Burry shorted housing when everyone called him crazy. Now everyone thinks his crazy again

May 5

🚨 BREAKING

MICHAEL BURRY IS BACK BETTING AGAINST $PLTR

$PLTR IS ALREADY GETTING CRUSHED AFTER EARNINGS

THIS IS THE SAME GUY WHO MADE HIS NAME CALLING BIG BUBBLES EARLY

HE’S SURE THIS DROP ISN’T OVER

VERY BAD FOR BULLS

196

262

1,513

940,942

The Heidelberg–PPC rumor has too much truth in it and sounds too deliberate, but the market has barely priced it in. PPC’s share price is only up ~10% on the rumour. If no bid comes, the downside may be that 10% fades. If a real control bid lands, the upside could be 30–50% from pre-rumor levels. That makes the speculative trade interesting: limited rumor premium, but meaningful bid optionality. #PPC_Cement

44

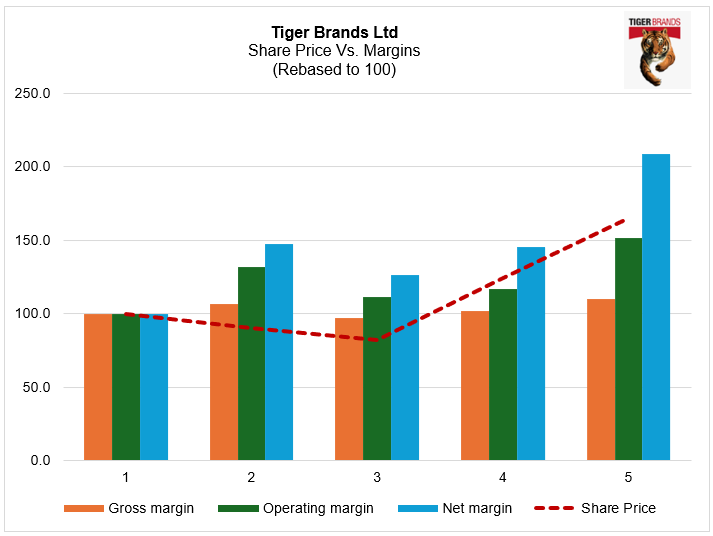

How important are margins?

Tiger Brands shows why operating margin matters most.

Gross margin tells you the product story. Net margin tells you the shareholder outcome. But operating margin tells you whether the core business is actually improving. In Tiger Brands’ case, the share price did not really follow gross margin. Gross margin improved only modestly, while operating margin rose much more sharply. That points to better cost control, operating leverage and stronger earnings conversion.

For valuation, that is often where the real story sits.

#TigerBrands #OperatingMargin #EquityValuation #SharePriceAnalysis #InvestingSouthAfrica

1

38

Zeder’s Zaad Disposal: Value Realisation or the End of the Road? investinginstocks.co.za/2026… via @JeandrePike

31

Extremely well deserved — if only. But it is also deeply unsustainable. There are no meaningful services, no money to spend properly on infrastructure, and when money is available, too much of it is lost to middlemen and corruption. I would be surprised if this investment yields even 0.5 cents on the rand. That is a 0.5% return on investment against a cost of capital above 8% — a sure formula for bankruptcy. This is why I hate talking about politics. Garbage all round. #PublicServants

#WageIncrease #PublicSector #SouthAfrica #GovernmentSpending

26