Programming teacher, comunications, iot projects, 3d printing...

Joined November 2017

- Tweets 837

- Following 126

- Followers 38

- Likes 338

22 Photos and videos

Josep Maria Llubes retweeted

Jun 8

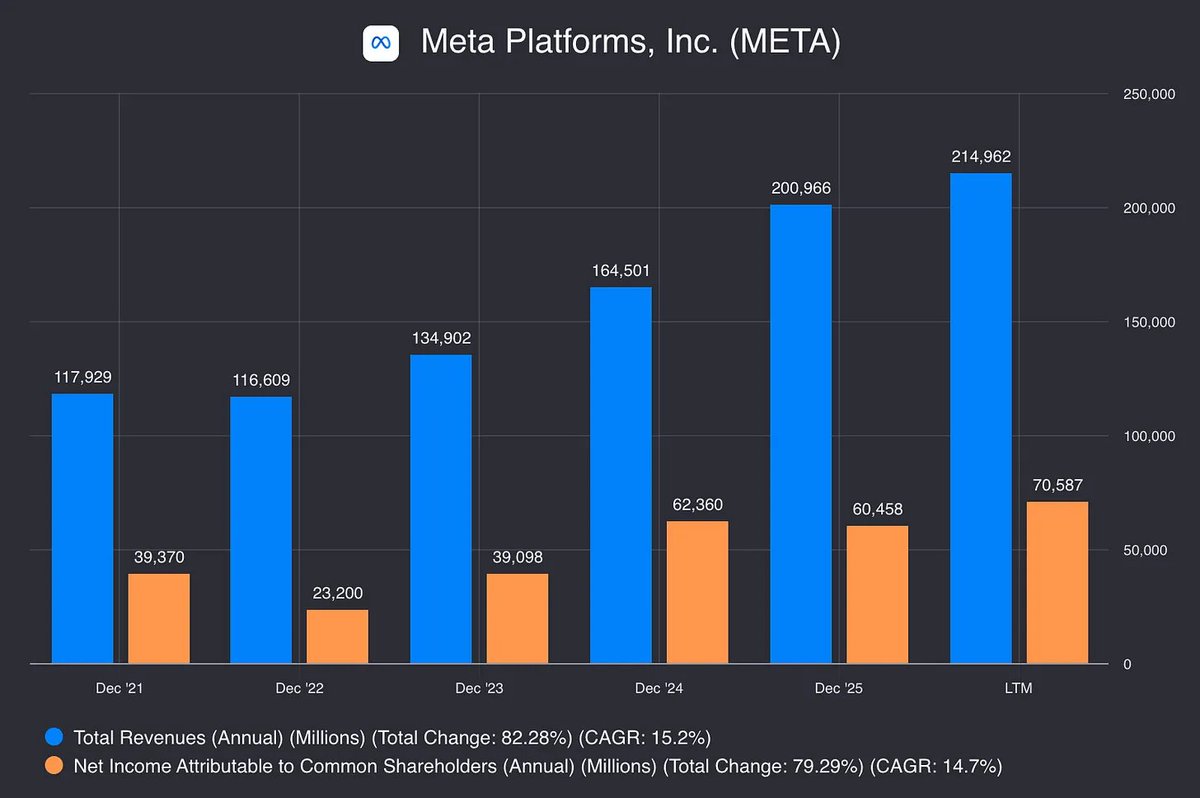

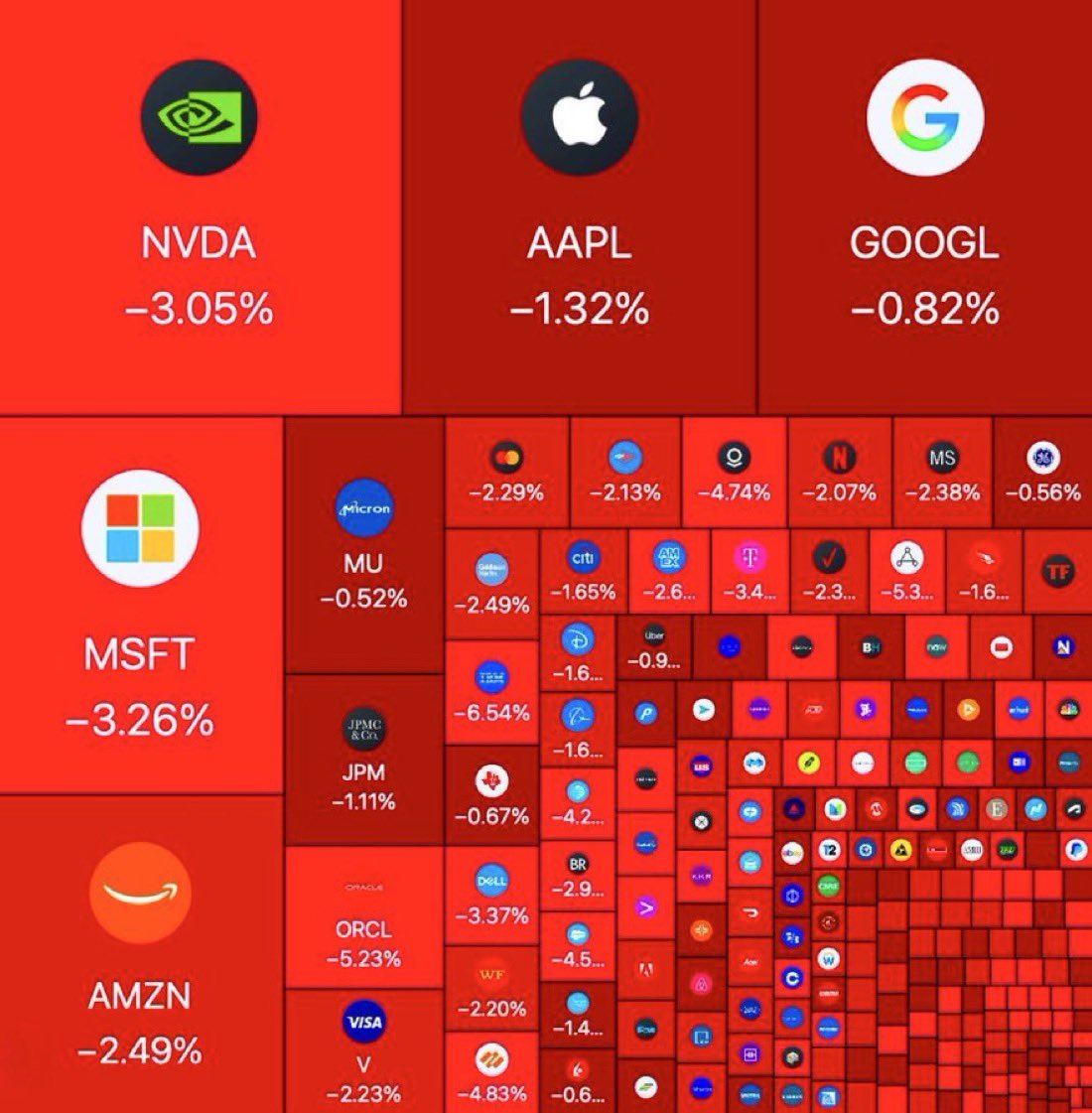

Bill Ackman says investors are repeating the same mistake from 2000 by chasing hot stocks and ignoring quality.

Here are 10 quality stocks trading at attractive valuations:

1. $META

5-Year Revenue CAGR: 15.2%

Forward P/E: 18

Consensus Price Target: $826

Implied Upside: 39%

56

114

1,072

420,680

Josep Maria Llubes retweeted

Jun 3

$META investors while the rest of the market is crashing:

4

6

94

5,969

Josep Maria Llubes retweeted

Jun 3

Meta Platforms $META está vendiendo por primera vez a las empresas acceso a un agente de IA, su último esfuerzo para generar ingresos que compensen las fuertes inversiones de la compañía.

El gigante de las redes sociales comenzará a cobrar a algunos clientes por lo que llama Meta Business Agent a partir de este miércoles.

La funcionalidad principal del agente es chatear con los clientes de una empresa a través de WhatsApp, Messenger e Instagram.

Las empresas más grandes que usen el agente pagarán a Meta por los datos utilizados para alimentarlo (tokens). Las empresas más pequeñas también tendrán que pagar por el agente mediante una de las nuevas ofertas de suscripción de Meta. Meta, que ofrece múltiples suscripciones para empresas, se negó a comentar en qué nivel de suscripción estará disponible el agente. La compañía había ofrecido anteriormente agentes IA para interacciones con clientes, pero no cobraba por esa función.

5

5

75

10,829

Josep Maria Llubes retweeted

4

15

1,276

Josep Maria Llubes retweeted

Esses efeitos práticos estão impressionantes... Não, pera...

292

2,647

32,437

2,832,368

Josep Maria Llubes retweeted

Cuanto menos curioso!

1

1

724

Josep Maria Llubes retweeted

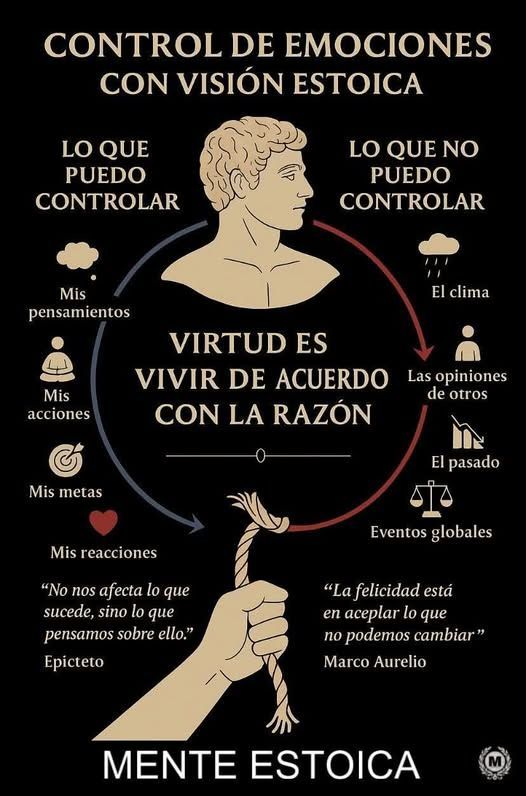

En tiempos de ruido constante, la verdadera rebeldía es la calma. No puedes controlar algoritmos, crisis ni opiniones… pero sí tu juicio.

2

142

624

22,274

Josep Maria Llubes retweeted

Apr 6

Clawnetes makes it super easy to change your OpenClaw models.

It's just one click away in the Clawnetes UI.

Not only that you can have different models for your multiple agents.

Get it today from aimodelscompass.gumroad.com/…

1

1

219

Josep Maria Llubes retweeted

Feb 27

$UUUU 2025 Earnings: Less "Mining Company," More "Sovereign Wealth Fund for the Periodic Table" ⚛️🇺🇸

Energy Fuels just dropped their 2025 results and 2026 guidance, and frankly, they are flexing on the entire critical minerals sector. When you combine high-grade uranium, a booming rare earth element (REE) business, and nearly $1 Billion in working capital, you aren't just surviving the cycle—you are dictating it.

Here is the breakdown of why the White Mesa Mill is becoming the most strategic real estate in the materials space, and why this sets up a brilliant foundation for Trading Around the Core.

☢️ The Uranium Engine: High Grade, Low Stress

The company didn't just meet 2025 guidance; it lapped it.

Production: 1.015 million lbs of finished U308 processed.

The Crown Jewel: The Pinyon Plain mine is yielding average grades of 1.62%, making it one of the highest-grade uranium mines in U.S. history.

The Margins: While the market fusses over $89.50/lb spot prices, UUUU is looking at weighted average production costs of $23–$30/lb for recovered uranium. In the commodity world, those aren't just margins; that's a safety net made of solid yellowcake.

🧲 Rare Earths: The Multi-Billion Dollar "Call Option"

If you want to build an EV or a defense system without asking for permission from certain geopolitical rivals, you need UUUU. They are moving from upstream securing of "molecules" to downstream processing.

The Math Gets Absurd: The newly released feasibility studies for the Phase 2 Mill expansion and the Vara Mada project (Madagascar) show a combined NPV of $3.7 billion. Let me translate that: that is $15.26 per share in value just from the REE side of the business.

Real World Proof: This isn't just a white paper. UUUU produced commercial-spec Dysprosium (99.9% purity) and has already seen its NdPr oxide successfully manufactured into permanent magnets for 1,500 EVs. An ex-China supply chain is officially being built.

💰 The Fortress Balance Sheet

They completed an upsized $700M convertible senior note offering, pushing total liquidity to $927.4 million. They have the war chest required to execute on vertical integration (like the proposed ASM acquisition) without breaking a sweat.

👔 Passing the Baton

Mark Chalmers will be handing the CEO reins to President Ross Bhappu in April 2026. Chalmers is leaving behind a fortified fortress, and staying on as a consultant to ensure the machine keeps humming. Oh, and they are continuing to advance their medical isotopes (Radium-226) program for cancer treatments, because why not add life-saving biotech optionality to the mix?

🦉Volatility in the uranium and critical minerals sector is a feature, not a bug. But when the underlying asset boasts rock-bottom production costs, massive liquidity, and an NPV on its secondary business that dwarfs its current valuation, it creates the ultimate setup.

5

11

106

6,300

Josep Maria Llubes retweeted

Feb 27

Un padre que crió a tres millonarios una vez dijo:

“Nunca les enseñé a ahorrar.”

Solo no permití un hábito en mi casa:

24

179

2,165

1,078,782

Josep Maria Llubes retweeted

LO VAS A LOGRAR.

66

443

21,557

Josep Maria Llubes retweeted

“Las circunstancias no hacen al hombre, solo lo revelan.”

– Epicteto

15

527

2,556

39,742

Josep Maria Llubes retweeted

Jan 30

🚨 El CEO de Anthropic acaba de lanzar una advertencia que debería preocupar a muchos.

Dario Amodei afirma que hasta el 50 % de los trabajos junior de oficina podrían verse afectados por la IA en los próximos 1–5 años, desde derecho hasta finanzas o consultoría.

Su consejo es claro: aprende a usar IA cuanto antes, o te quedarás atrás 👇

19

97

555

76,166