launch and run your vc firm from your phone

Joined July 2020

- Tweets 603

- Following 100

- Followers 2,034

- Likes 1,587

101 Photos and videos

Odin retweeted

Jun 12

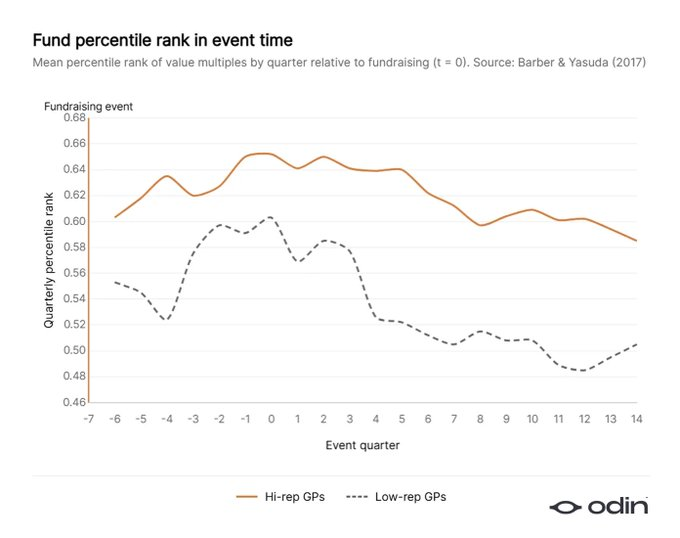

“So long as the loss in NPV isn’t too great, the GP’s optimal strategy is to select the alternative investment whose probability distribution places the most weight on outcomes which will result in a new fund.”

Venture capital and career concerns, by Nicholas G. Crain

This quote describes an unfortunate paradox in venture capital.

The greatest returns inherently come from unexpected places, but it's much easier to raise new funds based on the promise of expected opportunities.

GPs consistently paint themselves into a corner to make fundraising easier, which limits the prospect of outperformance later in their funds life.

Who better to talk to about this than @arian_ghashghai, who invests in "weird things on the fringe" at @EarthlingVC.

In this episode of Going Solo, Dan sat down with @arian_ghashghai, who founded @EarthlingVC in 2023 to back weird, fringe, early-stage companies across future computing, robotics, AR/VR, AI, bio, and more.

Arian shares his thoughts on the challenges of raising in one of the hardest LP markets in memory, why a wonky strategy can be an asset, and some of the myths and incentive structures distorting venture capital today.

01:24 - Raising fund one in a frosty market

04:18 - Finding non-consensus LPs

07:41 - Looking beyond AI, investing on the fringe

15:05 - Company building myths

17:36 - The challenges of scaling idiosyncrasy

20:56 - How to pick emerging managers

20:35 - The AI bubble and comparisons to 2021

32:35 - Smaller exits work for smaller funds

36:15 - Alpha versus access in venture capital

39:20 - There will always be bubbles

41:50 - Sacrificing the future

3

5

27

4,867

In this episode of Going Solo, Dan sat down with @arian_ghashghai, who founded @EarthlingVC in 2023 to back weird, fringe, early-stage companies across future computing, robotics, AR/VR, AI, bio, and more.

Arian shares his thoughts on the challenges of raising in one of the hardest LP markets in memory, why a wonky strategy can be an asset, and some of the myths and incentive structures distorting venture capital today.

01:24 - Raising fund one in a frosty market

04:18 - Finding non-consensus LPs

07:41 - Looking beyond AI, investing on the fringe

15:05 - Company building myths

17:36 - The challenges of scaling idiosyncrasy

20:56 - How to pick emerging managers

20:35 - The AI bubble and comparisons to 2021

32:35 - Smaller exits work for smaller funds

36:15 - Alpha versus access in venture capital

39:20 - There will always be bubbles

41:50 - Sacrificing the future

2

9

5,603

Odin retweeted

Jun 11

Great research by @JoinOdin on the role of SPVs in our VC ecosystem!

With common concerns about LP alignment, GPs are increasingly aware of the need for transparency and skin in the game when using SPVs.

We asked some of the best early-stage managers how they think about getting this right.

Full report available here: spvsurvey.joinodin.com/

1

2

10

1,909

Odin retweeted

Jun 9

People talk about "going earlier" because prices are high

Don't go earlier. Investing in the same company but "earlier" is likely just adverse selection.

Instead, go weirder.

Weird and right has way better returns than consensus at a 20% discount.

6

4

64

4,833

Odin retweeted

Jun 11

SPVs allow VCs to move more quickly, offer larger positions in attractive companies, and support founders through later rounds of fundraising.

However, the principal–agent problem is real, deals may be opaque, and it can be a challenge for LPs to build a solid portfolio with these investments.

Understanding the strengths and the weaknesses of these vehicles is crucial if you want to build an enduring firm with a happy and loyal LP base.

The best managers ensure a healthy balance of risk and upside for LPs, with transparency and skin in the game. We encourage this discipline.

"I think the principal-agent problem is real, and I do think a lot about how to align incentives. I did SPVs prior to the fund and always got a bit queasy about the no downside / all upside dynamics. I think big mgmt fees are a red flag and I’m sensitive to having skin in the game as well for any vehicle."

- @arian_ghashghai, GP at @EarthlingVC

"I see too many fund managers host SPVs when their LPs aren't in a position to make a sophisticated decision on whether or not to participate (which means that these vehicles stay open for far too long). SPVs are for your winners, that's it."

- @DStrachman, GP at @1517fund

"I don’t believe in SPVs until the companies are large, almost certain winners, in a crossover round or something like that it’s probably fine. There is so much risk of companies failing, there’s a reason to do them in a fund. I don’t like losing my LPs money, I take that very seriously, and I think a whole generation of fund managers are going to lose LP money in SPVs"

- @sarah_cone, GP at @socialimpactcap

Check out the full report, based on a candid survey with 56 venture capital managers, below:

With common concerns about LP alignment, GPs are increasingly aware of the need for transparency and skin in the game when using SPVs.

We asked some of the best early-stage managers how they think about getting this right.

Full report available here: spvsurvey.joinodin.com/

1

8

29

4,731

With common concerns about LP alignment, GPs are increasingly aware of the need for transparency and skin in the game when using SPVs.

We asked some of the best early-stage managers how they think about getting this right.

Full report available here: spvsurvey.joinodin.com/

7

22

7,742

Years in which a higher share of capital went to first-time venture capital funds, rather than funds from established firms, appear to produce more value at exit.

This finding implies that emerging VC firms have a particular edge when it comes to recognising great founders and ideas at the earliest stages.

This is one of the many reasons that the emerging manager category must remain healthy and well funded. Not only do these firms produce surprisingly strong returns, but they also support a large amount of downstream value.

Read more about how these factors play a part in keeping the venture capital ecosystem healthy in our latest article.

2

3

12

2,299

Patrick Ryan (@ry_paddy) Co-Founder of @JoinOdin explains how Anthropic's SPV voiding reduces Section 12G exposure while actively manages a $1.5 trillion valuation narrative ahead of their IPO:

"They're getting price discovery. They're getting... lots of retail trading of their stock or interests linked to their stock."

"They get insider liquidity that drives employee retention... but they avoid the disclosure regime of public companies. So they get all the benefits of being a public company without any of the downsides."

"If the SEC turns around and says, 'Look, we think you've actually been a public company for the last three years,' that creates a real headache for them. So they want to get rid of that."

"Stuff's trading at between a trillion and 1/2 trillion in the secondary market. If you're worried about supporting that kind of valuation at IPO, you want to kind of calm people down a bit in advance... to be like, 'I want you to pay less.'"

From @ry_paddy appearance in May.

Jun 8

Leopold Aschenbrenner's Situational Awareness fund is up by 270% 🟢 after fees so far in 2026 through May and up 1,000% since being created

20% of the fund is currently in Anthropic

Leopold first bought in Anthropic in February 2025 at a valuation of $61.5 Billion

Today Anthropic is now worth $965B and Leopold's stake in the company is worth around $4 Billion

(Source WSJ)

7

15

5,743

Odin retweeted

Jun 8

Years with a larger share of capital going to first-time funds show consistently stronger exit values in the adjusted horizon.

The correlation is there, and allocators are still ignoring it.

Jun 7

When people say "venture capital doesn't scale", they are usually referring to the size of firms and funds.

However, there's a strong argument to scale venture capital by increasing the number of firms.

Solo GPs and small partnerships are the most efficient early-stage allocators. There simply aren't enough of them relative to the scale of the market, for solvable structural reasons.

Indeed, not only does data show that smaller firms and emerging managers outperform, but also that there's a correlation between the % of capital going to first-time funds and total horizon exit value for venture capital.

On the other hand, the rise of megafunds is associated with slipping returns, consensus-seeking and stagnation. Their main claim to success rests on appropriating public market growth.

Essentially, an market with more new firms is inherently more competitive. A more competitive market will deliver stronger returns, being less likely to prop-up marginal companies or misallocate capital.

Indeed, the fundraising friction which scaled VC largely eliminates has always been a feature, not a bug. It is the mechanism by which weakness is screened out of the market and prices are kept rational.

Without Darwinian selection, there is limited appetite for the idiosyncratic risk that has driven venture capital's greatest success stories.

2

2

11

2,704

Odin retweeted

Jun 7

When people say "venture capital doesn't scale", they are usually referring to the size of firms and funds.

However, there's a strong argument to scale venture capital by increasing the number of firms.

Solo GPs and small partnerships are the most efficient early-stage allocators. There simply aren't enough of them relative to the scale of the market, for solvable structural reasons.

Indeed, not only does data show that smaller firms and emerging managers outperform, but also that there's a correlation between the % of capital going to first-time funds and total horizon exit value for venture capital.

On the other hand, the rise of megafunds is associated with slipping returns, consensus-seeking and stagnation. Their main claim to success rests on appropriating public market growth.

Essentially, an market with more new firms is inherently more competitive. A more competitive market will deliver stronger returns, being less likely to prop-up marginal companies or misallocate capital.

Indeed, the fundraising friction which scaled VC largely eliminates has always been a feature, not a bug. It is the mechanism by which weakness is screened out of the market and prices are kept rational.

Without Darwinian selection, there is limited appetite for the idiosyncratic risk that has driven venture capital's greatest success stories.

7

7

36

11,180

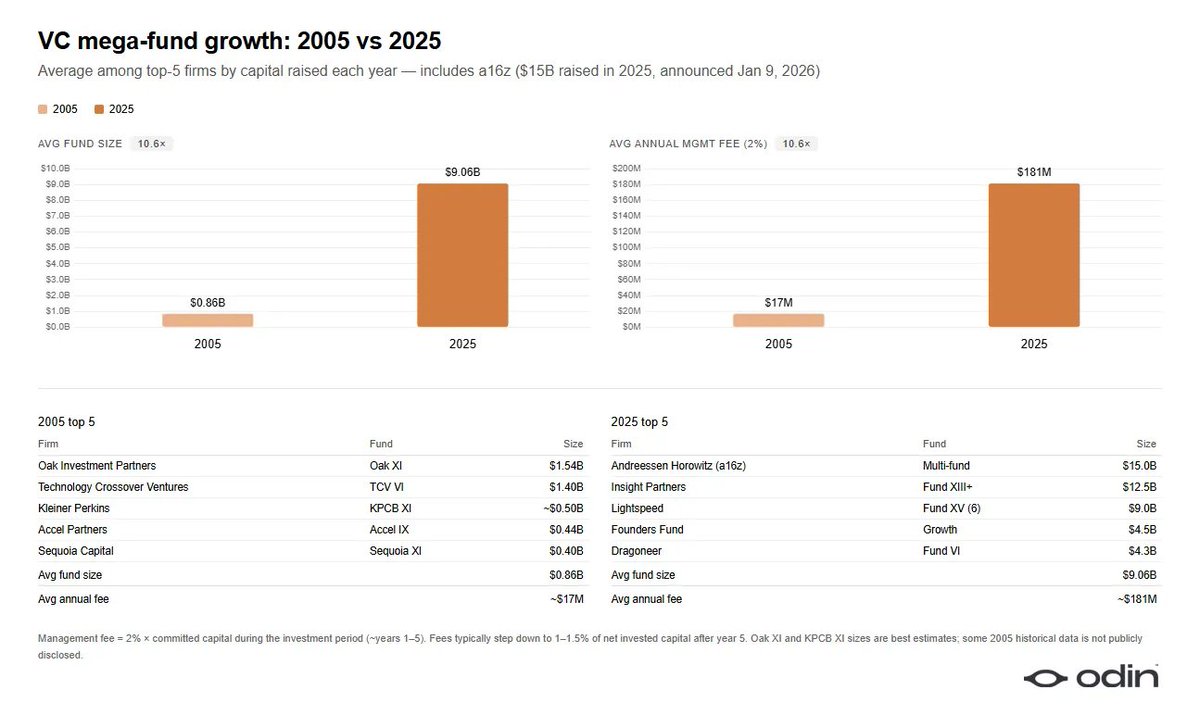

In 2005, the five VC firms that raised the most capital in that year each generated a total of ~$150M in subsequent fee income.

For 2025, it’s closer to ~$1.6B in fee income, each.

It's hard to beat the AUM business!

5

10

1,829

Odin retweeted

Jun 2

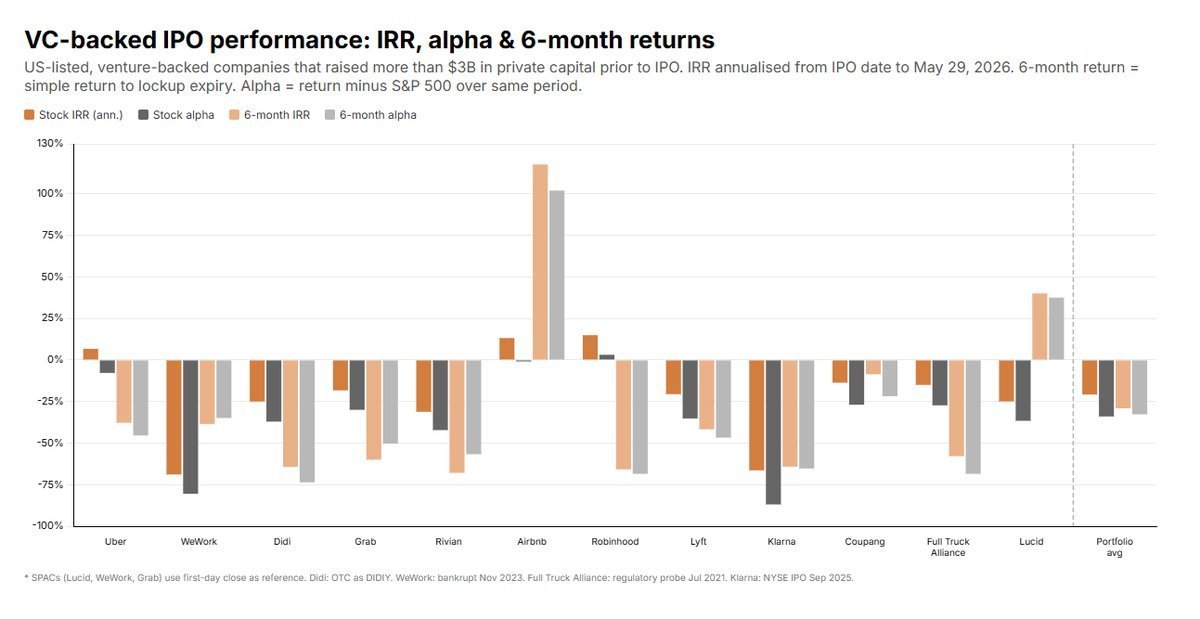

There are 12 venture-backed companies that raised >$3B in private markets and then listed in the US.

Only one that has a positive return today, relative to the S&P 500's performance over the same period.

Most are deeply negative (aggregate -117%).

Only two that were positive at lockup expiry, neither stayed that way.

The high cost of private capital means the companies that raise the most, and stay private longer, are almost inevitably overvalued as insiders raise the price of funding events aggressively to stay NPV positive.

9

30

210

118,386

seems relevant considering what's coming down the pike this year

May 31

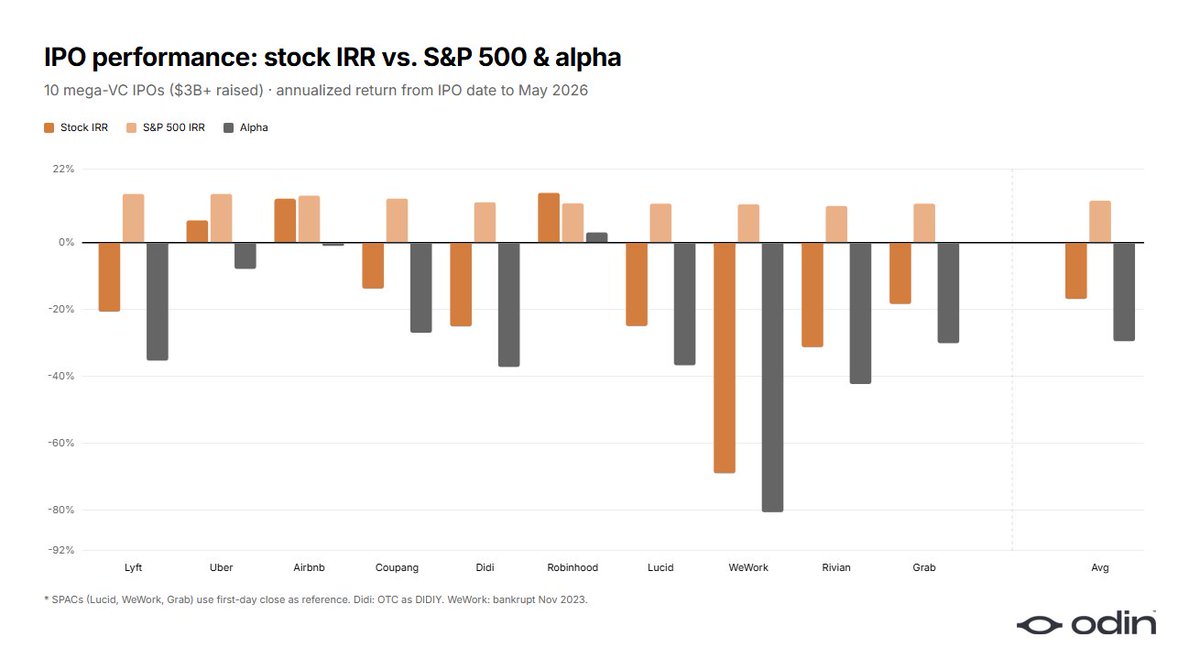

You would be forgiven for thinking that the companies which raise the most from VCs are surely the most important and promising of their generation.

Unfortunately, most are failures.

A portfolio of the top 10 would be at –120.5% today, relative to the S&P 500.

The more capital a firm manages, the more it selects for scalability and market signals, rather than any deeper qualities or outlier potential.

This is a result of the top-down incentives from their own investors; careerist allocators who only really care about reliable IRR on large pools of capital.

Fundamentally, the goal is no longer to "back great founders", but to find the most dramatically scalable vessels to consume allocation.

So, growth is pulled from public markets, where fees are a mere 0.05-0.7%, into private markets where they are a more lucrative 2%. This much larger fee layer essentially becomes a tax on innovation.

The 5 largest VC firms extract more than 10x the management fees they used to, despite a clear weakening of the venture market over that period.

None of this improves until the market realises it's clearly dumb to apply the same compensation structure to radically different scales and strategies.

2

6

42

8,241

Odin retweeted

May 31

You would be forgiven for thinking that the companies which raise the most from VCs are surely the most important and promising of their generation.

Unfortunately, most are failures.

A portfolio of the top 10 would be at –120.5% today, relative to the S&P 500.

The more capital a firm manages, the more it selects for scalability and market signals, rather than any deeper qualities or outlier potential.

This is a result of the top-down incentives from their own investors; careerist allocators who only really care about reliable IRR on large pools of capital.

Fundamentally, the goal is no longer to "back great founders", but to find the most dramatically scalable vessels to consume allocation.

So, growth is pulled from public markets, where fees are a mere 0.05-0.7%, into private markets where they are a more lucrative 2%. This much larger fee layer essentially becomes a tax on innovation.

The 5 largest VC firms extract more than 10x the management fees they used to, despite a clear weakening of the venture market over that period.

None of this improves until the market realises it's clearly dumb to apply the same compensation structure to radically different scales and strategies.

17

21

120

36,170

"I'm already completely convinced that we'll sit here in three years and talk about a space bubble."

Venture capitalist, robot fighter and notorious contrarian @arian_ghashghai, managing partner at @EarthlingVC, believes we'll roll right from an AI bubble into a space bubble as the private market hunts for opportunity.

But is this a condition that LPs are going to be happy with in perpetuity?

We discussed this with him, along with a range of other topics related to fundraising and venture markets, in our recent episode of Going Solo. Links below. 👇

3

1

15

6,155

Going Solo - A podcast series with solo GPs and emerging mangers:

linktr.ee/goingsolowithodin

236

Odin retweeted

May 26

imo a lot of new founders don't understand the LP-GP dynamic well (i.e. that LPs keep GPs in business, and GPs are expected to pursue strategies they sold to LPs when fundraising). This usually leads to the following sequence of events:

> Fund-fundraising is very hard (I may take crap for this, but fundraising is the only task I think is harder for a GP than a founder). GPs simplify their job of selling their product to LPs by pitching the "hot" thing (e.g. AI), and inventing some narrative about how they are uniquely positioned to acquire the best positions in the "hot" thing (there is already pre-existing allocation interest in the "hot" thing)

> If you sold your LPs "access" to the hot thing, and the market becomes wholly irrational (like it is currently), you're basically stuck having to choose either: 1) overpaying for a "hot" company (questionable long-term DPI strategy) or 2) keeping discipline and passing (but with the risk that your LPs give you short-term crap — read: threat to your n 1 fund — for missing out on the kind of access you sold them on)

Most GPs here will optimize to not have short-term pain (i.e. overpay) and kick the can on returns down the road with (imo, unsubstantiated) platitudes like "what if it's the next Facebook?"

(this also means there is no room for your weird, non-AI startup in their portfolio btw)

May 26

To quote @skupor: “Sins of omission are worse than sins of commission. It’s okay for a VC to invest in a company that ultimately fails, that’s par for the course in this business. What’s not okay is to fail to invest in a company that becomes the next Facebook.”

This becomes a real problem for small and emerging managers if their proposition to LPs is access to consensus-type opportunities.

They end up with a dilemma; to face scrutiny for overpaying, or even greater scrutiny for missing out on seemingly obvious winners. There's also real systematic risk in tying a fund to a particular category where the window of opportunity may close at any moment.

Deal-by-deal SPVs are one answer, but that approach amplifies venture capital's principal-agent conflicts as GPs pass most of the risk to their LPs.

In truth, it's probably just not a strategy that small and emerging managers should pursue. The scaled venture platforms, on the other hand, are relatively price-insensitive, and can pay up when required.

Enjoyed chatting to @arian_ghashghai of @EarthlingVC about this, and many other topics, in the recent episode of Going Solo. Links below.

17

9

87

14,764

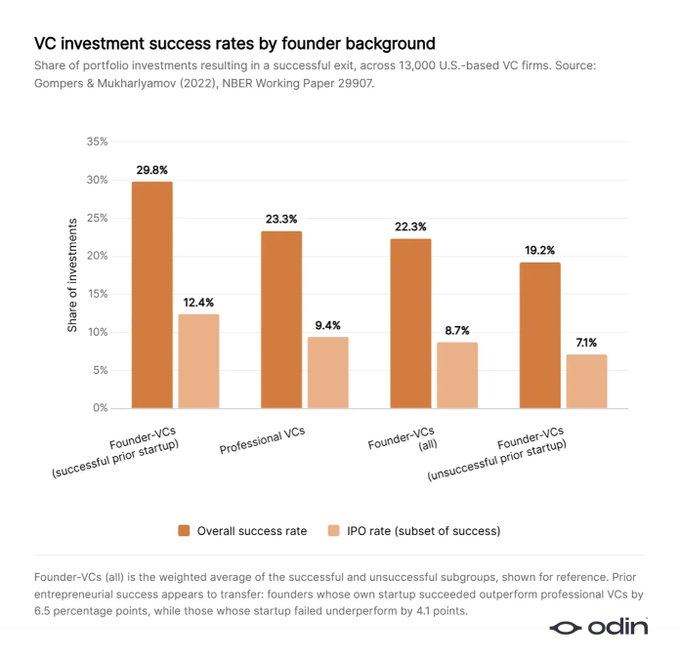

The success stories of biotech VC are remarkable.

The rate of successful exits in that category, even controlling for the survivorship bias of more intensive pre-incorporation periods, is outstanding.

@FlagshipPioneer is one of the best examples. From their Fund IV, in 2012, they made ~35 investments and produced 11 IPOs with a combined market cap of ~$14B.

This kind of performance doesn't happen by chance. Flagship's Founder and CEO, @NoubarAfeyan, has devoted his career to making innovation more process-oriented and systematic.

2

1

22

22,633