Null is All -------------! Building everything from to zero----------------------------- DM for Inquiry 📩

Joined August 2022

- Tweets 130

- Following 766

- Followers 917

- Likes 1,038

70 Photos and videos

Kernels retweeted

25 Nov 2025

If you've ever seen someone tweet some cool shader and thought "I don't really even know what a shader is and at this point I'm too afraid to ask" - I've written something just for you.

makingsoftware.com/chapters/…

156

684

7,262

712,311

Kernels retweeted

24 Dec 2025

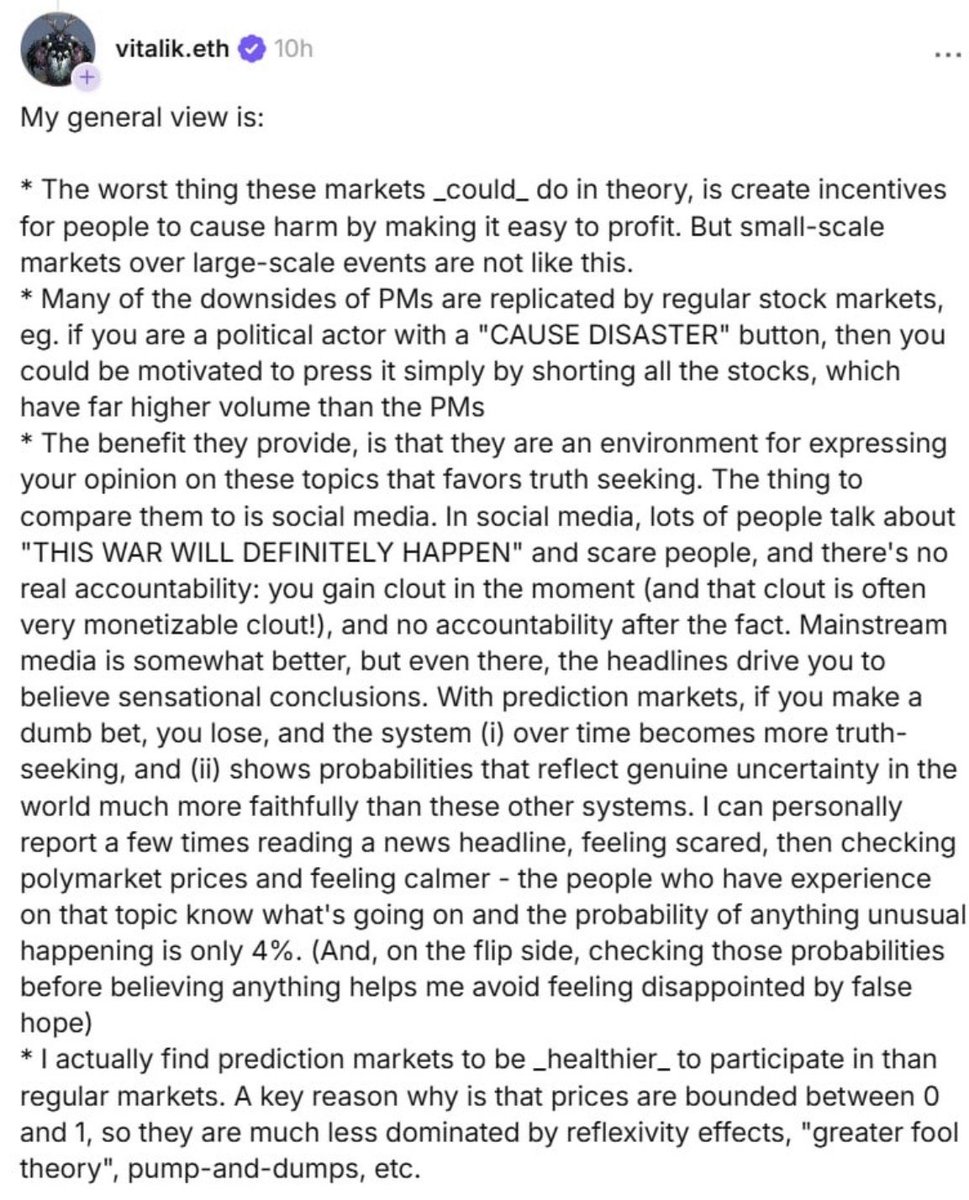

The Platonic prediction market

@VitalikButerin's "healthier prediction markets" only exist in an idealized textbook version. Today in practice, it is anything but that.

1) the mechanism of PM to turn private information into public knowledge is through subsidies. Historically this subsidy come from research or governments, but today it comes from institutional market makers who are in turn subsidized by the platforms’ VCs. It’s a classic Silicon Valley Uber burn cash to buy user playbook. A system that needs continuous burn to purchase information is not healthier, it’s artificially oxygenated.

2) market makers have to model the probability distribution of the underlying events, and often lack alternative avenues to hedge inventory risks. As a result, they can only provide liquidity on markets with rich historical data such as sports and politics. The kind of markets where tacit private knowledge resides actually have little to zero liquidity. This is structural as under the CTF design, subsidies can’t flow into these markets through professional MMs. If anything it hides the failure mode: you get a neat-looking probability interface on the exact categories that are already easy to model, while anything outside of sports or politics or crypto prices, are dead zones.

3) the price bound is only a cosmetic improvement. While pegging price to probability is intuitive, in practice users are not optimizing for precise probability calibration. They are optimizing for PnL. Someone who thinks the chance of raining tmrw is 42% is still going to buy as low as possible. This is evidenced by most of the activity is concentrated near resolution time (known as “banging resolution”) or sweeping the markets w/ 95% . Pegging individual trades to probability only surface mispricing opportunities. In fact, the bounded framing can increase shallow-game behavior: when the UI says “99%,” people treat it like a free yield product until the rare tail hits. The reflexivity doesn’t disappear; it just moves into (i) last-minute positioning, (ii) thin-book price impact games.

4) measuring the platform’s accuracy should be based on “do events forecasting 70% actually happen 70% of the time?” Not “events forecasting 70% actually did happen!” The bounded price is only meaningful if the platform can demonstrate calibration over a large sample, across time, otherwise it’s a storytelling device. You can’t claim “healthier” just because the number looks like a probability.

5) the lack of speculation actually makes the market worse. In any healthy financial markets, you can’t have highly homogenous group of sharp vs sharp. That easily creates stagnation. Liquidity begets liquidity. Information begets information. There’s no long-duration narrative carry, no natural hedging demand, and no deep speculative ecosystem to keep books thick. When flow is thin, every trade is “information,” which makes adverse selection worse, which makes market makers pull back, which makes the market even thinner. If the market systematically overprices favorites, underprices tails, and concentrates liquidity only at the end, then what you have is not calibrated truth-seeking. This is the opposite of healthy.

Vitalik is right that idealized version of prediction markets can lead to healthier structure, but today this is anything but. The uncomfortable reality is that the bounded probability story is a UX veneer on top of a subsidy-and-microstructure problem. If we keep deluding ourselves “healthier than regular markets” is just a slogan, and all we end up getting is just a glorified sportsbook and an even more devious form of options.

33

18

171

72,584

Kernels retweeted

26 Dec 2025

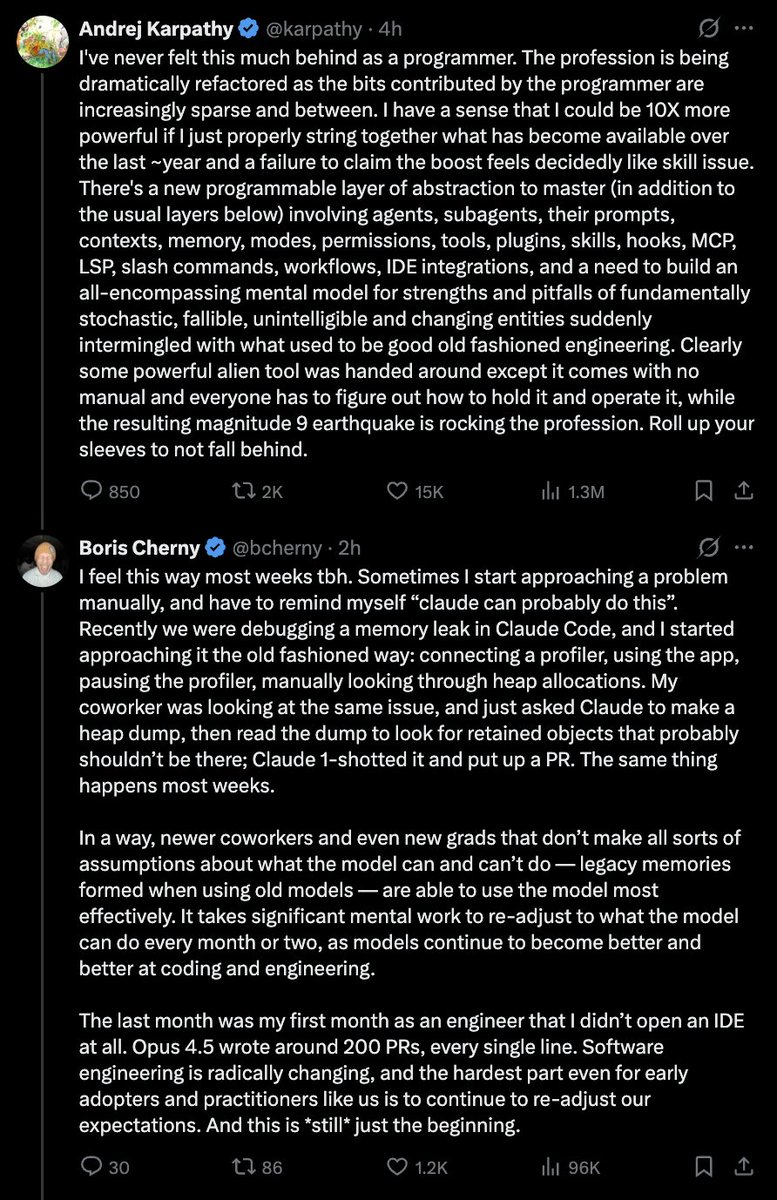

Two great engineers reflecting on how the profession is fundamentally changing with AI

144

884

8,208

532,389

11 Nov 2025

x402 revolution :)

4

171

Kernels retweeted

3 Nov 2025

Ethereum developers use tools like Hardhat and Foundry to fork mainnet and test contracts with live data.

Now, @Aptos developers can do the same—faster, simpler, safer.

Transaction Simulation Sessions bring real-world testing to the Aptos CLI 🧵

15

20

109

31,445

DIRECT ANSWER on how much you can earn running a @shelbyserves node, according to @jump_'s math:

1. RPC Node Operators :

• Assuming they will be Serving 324,000 GB/month

• Total Revenue Generated : $2,235.60 revenue

• Monthly operational cost : $1,488.12 (includes @Aptos & @DoubleZero fees).

• Profit after costs : $747.48 (~50% margin).

2. Storage Providers :

• Assuming they will be Storing 125 TB data

a. Write fees : $600.

b. Read fees (each byte read 4 times/month) : $1,725

• Total Revenue Generated : $2,325

• Monthly operational cost : $945 (includes @Aptos & @DoubleZero fees).

• Profit: ~$1,380 (146% ROI)

Note:

1. Jump’s calculations include assumptions. Actual numbers may vary when @Shelby goes live on mainnet. This is just an estimate.

2. RPC and Storage Providers may need to stake Shelby tokens to run nodes. This investment is separate and not included in the calculations.

November is shaping up to be a big month for @Aptos

With @DecibelTrade testnet launching and @shelbyserves devnet already live, tons of opportunities are about to unfold.

Many of you have DM’d asking - “How can we position ourselves to make the most out of Shelby?”

Simple Answer → Run a node (when its availale ofc).

Running a Shelby node is designed to be profitable, the cost model ensures node runners never operate at a loss.

Below is the post where I broke down Shelby’s cost modeling in detail.

7

3

18

1,801

Kernels retweeted

23 Oct 2025

Just finished reading @shelbyserves 's cost modeling and I’m convinced it can actually compete with AWS on price. Here’s my ELI5 version to save you some time. 👀

AWS’s single-point failure seems unavoidable. Most people assume it’s the most efficient model, but it’s really not. Decentralized hot storage could actually have a real cost advantage over AWS.

Shelby gives profit back to storage providers (SPs) and RPC nodes, keeping their incentives aligned.

Here’s the idea:

- RPCs earn half of the read fees

- SPs earn write fees plus the other half of read fees

- The more often data gets read, the more both sides earn. Everyone wants the system to run efficiently and stay active.

Under the hood, Shelby also keeps costs down with two design choices:

- Lower redundancy (2x instead of 4.5x)

- Erasure coding for durability instead of simple replication

From the model:

- Write fee (W) ≈ $0.0096 per GB·month → SPs break even here

- Read fee (RF) ≈ $0.0138 per GB → RPCs start making profit

For context, Shelby’s write fee (W) is like AWS’s storage cost, and the read fee (RF) is like AWS’s egress fee — the charge for data leaving their servers.

Compare that to AWS:

- S3 Standard storage: $0.023 per GB·month

- Egress: $0.09 per GB

If those numbers hold up, Shelby could undercut AWS on both storage and read costs, while still being profitable for the people actually running the network. When read rates go up, users save more compared to AWS, and storage providers earn more.

Everyone wins when the system is used for what it’s built for: frequently accessed data. 👀🌐

Read the full post by @jump_ here: jumpcrypto.com/writing/shelb…

29

8

65

8,332

[🔥] ALPHA: @shelbyserves Cost Model Explained

@jump_ shared the cost modeling for @shelbyserves a few days ago.

If you don’t want to dive into all the math, here’s the TL;DR :

1. Storage Providers :

→ Yes, it’s profitable for SPs to store data. Even if nobody reads your stuff, the cost model lets you breakeven on storage fees.

a. Earnings = Storage Fees Read Fees

b. Profit = Earnings - (Storage Cost @Aptos Fees Fiber Fees)

More reads = more $$ in your pocket.

2. RPC Providers :

They’re set to eat too. Cost modeling designed around ≥50% yield on investment. They get a cut from read fees and are super crucial to the system.

Everything looks promising. I might run a node myself.

Are you thinking of running one too?

4

2

13

2,594

24 Oct 2025

It's been incredible fun building with @shelbyserves !!

-- such clean and intuitive infra with amazing dev resources 🙏✨ @affinity_matrix @rpranav

looking forward to building pipelines that connect tokenomics with users and continue to geek out on this new data ecosystem 😆✨

4

3

9

607

24 Oct 2025

Checkout amazing @shelbyserves GitHub Repos !

Shelby Examples - github.com/shelby/examplesSh…

Shelby Quickstart -github.com/shelby/shelby-qui…

2

2

164

Introducing Aptos Assembly 🌐

Aptos Foundation's 4-week program uniting builders, mentors, and ecosystem partners to focus, build, and launch products that move real value on Aptos.

Learn more. Apply now:

32

65

404

364,224

Kernels retweeted

15 Oct 2025

One Tap. Infinite Connections.

Introducing TAPT—the new standard for onchain authentication from Aptos Labs.

TAPT turns any NFC-enabled device into a trusted onchain interface. Tap to verify, sign, or transact.

Fast. Familiar. Frictionless.

Be first: tapt.network/

17

22

114

13,168

15 Oct 2025

Excited to attend the Aptos Experience with @rockyntheblock as an Ambassador for 🏝️ Resort Maker on @Aptos ✈️🗽

Here for RWAs, data, and some good time in NYC?

Let’s connect :)

Catch you at the conference !

@KernelsAI

@exponentlabshq

1

1

9

919

Kernels retweeted

16 Aug 2025

real communities don't need a schedule

this is pick-up basketball at scale

1

3

283

Kernels retweeted

14 Feb 2024

I am a nobody.. I have held

Magic internet money from 140k to 5mil mc

Bitcoin from 150k to 5mil mc

Smurfcat from 14k to 260k mc

All in the last 5 days give or take …

All thanks to @KernelsNFT…. Fuck your alpha chats… @findbleh giving us mfer on ground level a chance!!🫡

9

13

39

2,299

Kernels retweeted

13 Feb 2024

birdeye.so/token/EArkn8uVf8Y…

Late call because we got in at 12k mc but this the ticker next to a mil.. dyor nfa and ohh yeah, thanks @KernelsNFT for the @findbleh bot 🫡

3

4

389