Retired tech exec, playing music in an idyllic beach town.

Joined December 2025

- Tweets 2,320

- Following 151

- Followers 220

- Likes 287

119 Photos and videos

Jun 14

Ridiculous assertion. In the music world, everyone covers Springsteen, more so than Bob Dylan.

Almost no one covers Bob Seger songs. When they come up in a band context, everyone be like “nah, let’s pick something else.

Jun 13

My most controversial middle aged sportswriter take:

Bob Seger has better songs than Bruce Springsteen

1

44

Jun 14

As an American who has travelled extensively in Europe, Asia and the Americas, I’m thoroughly enjoying our overseas visitors discovering all the blessings we take for granted.

I experienced decades of people drunkenly trying to justify why their country was “better” than the US.

I would always respond with “you have no idea”

Now they get to see for themselves.

1

37

Jun 13

I love seeing how our European visitors are fallling in love with the US. Having spent serious time in Europe, I understand the appeal!

My wife and I decided the best way to explore the US required a specialized vehicle, namely a used 2016 LTV Serenity.

It's built on the legendary Mercedes Sprinter chassis and sips diesel while others guzzle. It's strong enough to tow a Jeep Wrangler over the Continental Divide, although you'll be in the slow lane.

Sleeps two comfortably. Self-contained when you need it. It's been to all 48 contiguous states. Reliable as it gets.

We'll go out for maybe 5-6 weeks at a time around May, and just wander through different regions, starting in the southwest and ending up in the northeast.

They don't make them anymore, but if you find one used and are so inclined, it's truly an exceptional ride at a very reasonable price.

1

1

39

Jun 13

The joke goes that there are people who divide the world into two categories, and those that don't.

My two categories are "embracers" and "escapers".

Embracers take on whatever comes their way, and make the best of it. They patiently and quietly work to make the world a better place.

Embracers understand the world works the way it does for reasons. Understand the reasons and you'll do fine.

Escapers live in a perpetual state of denial and anxiety. They can't control the world around them, so they escape: drugs, activism, cosplay and other generally anti-social behavior.

They complain loudly at every perceived injustice, it sounds like the Grief Olympics. No effort is made in understanding why things are the way they are.

"It's not fair" is their rallying cry. News alert: the universe isn't fair and has never been fair.

If we could measure people's propensity to either embrace or escape, we'd have an excellent measure of their potential value to society.

Much more useful than IQ. Lots of really smart people live in an escapist mindset, which is -- well -- dumb. The universe will not change to suit your mood.

The hardest conversation you'll ever have is bringing reality to an escapist. They will deflect, deny and accuse you of being an awful person.

I remind them it has nothing to do with me. It's the way the world works that you're arguing with.

2

23

Jun 11

Cancer occurs when otherwise well-behaved cells decide to stop acting in a cooperative fashion, and revert to more primitive self-dealing.

They refuse to respond to external signals, and simply start growing and multiplying as they once did in a more primitive form.

Cancers end up killing the organism that hosts them if the uncooperative cells aren't destroyed.

It's literally kill or be killed.

Now, think about:

- systemic election fraud

- self-dealing govt officials

- murderous, fraudulent cultural imports

- dysfunctional segments of society

- billionaire-funded NGO networks

- etc.

These are all cancers in our high-trust, high-productivity society.

If this was pre-med, we'd be discussing all the different approaches to eradication: starvation, poisoning, surgical removal, radiation therapy and more.

Nothing would be held back, as cancerous cells are very dangerous, and medical science knows they need to be removed as quickly as possible.

Specifically, cancer cells are not fed, not housed, not funded, etc. as there is ZERO chance that cancerous cells revert to a more cooperative state in the future.

How long before the social sciences acknowledge the same?

1

19

Jun 9

Heavy reliance on H-1B has quickly become a material risk for shareholders, and will be forced to be disclosed.

These are serious salaries as well that would have gone to US citizens in most cases.

This is also undoubtedly going to hit the real estate market as well as certain mortgage lenders. Lots of property going up for sale before long.

Jun 9

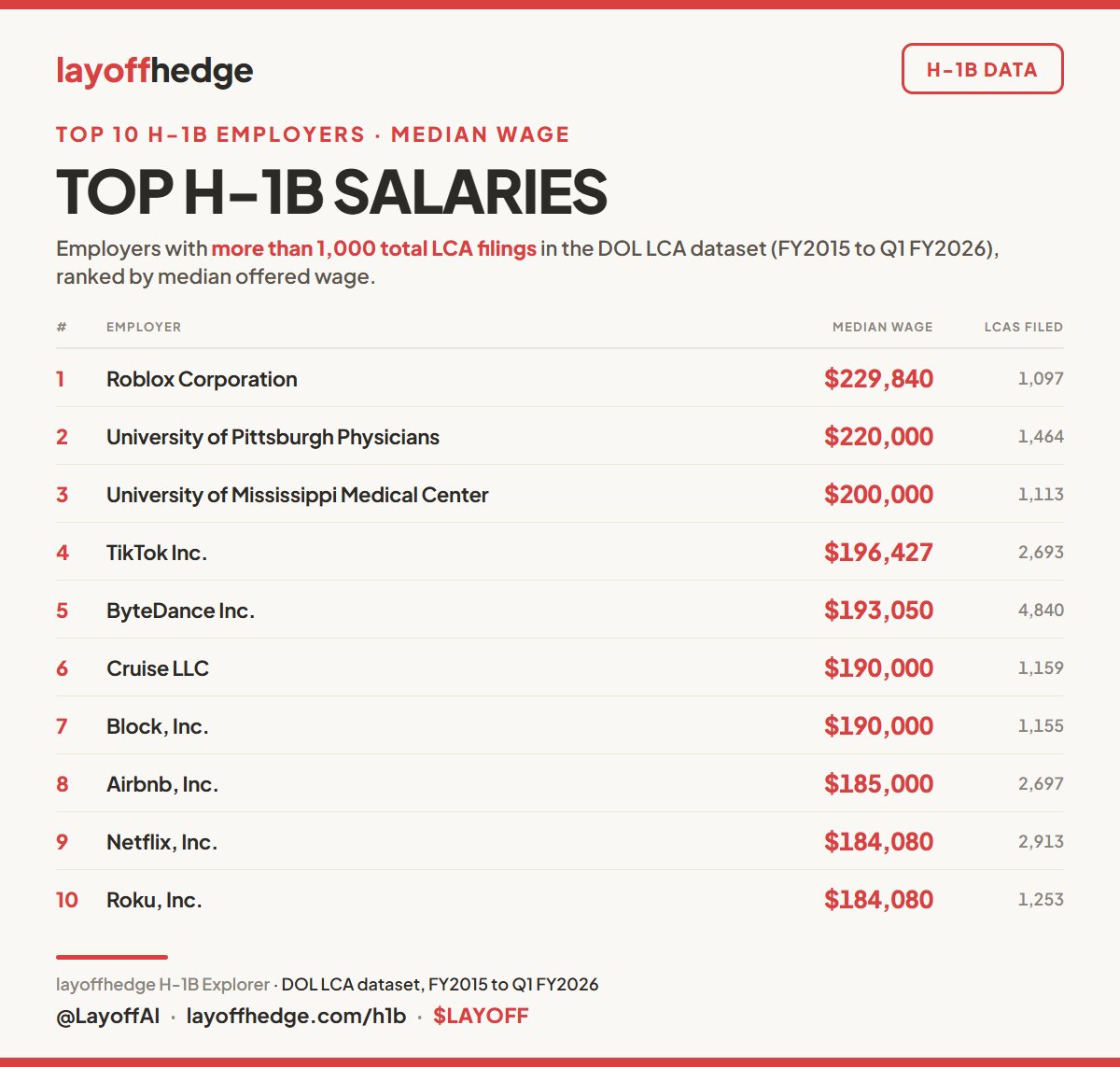

Roblox ranks #1 in terms of H-1B salary for employers that have filed at least 1,000 LCAs.

Average salary: $229,840

Top 10 list, ranked by salary.

53

Jun 9

Just got off the phone with my investment adviser, but if we're being real here, I'm the one dispensing the advice more often than not.

Q1: how to play the AI transition?

Avoid the obvious names that are oversold, and focus on the companies that can translate AI into real-world benefits.

Names like Apple and Oracle and Tesla become more appealing, pure plays like Nvidia and Anthropic less so.

Someone needs to start an "applied AI" index fund.

Q2: how to play the SpaceX IPO?

Way oversold, so wait for coordinated lockups to expire (or a rocket to blow up) and buy the dips. No doubt it's a generational opportunity, but at what price?

Also, lots of people are liquidating other assets in preparation for this and the Anthropic IPO (I'm looking at you, bitcoin), so plenty of otherwise good investments are a bit discounted now.

Lots of good stuff on sale now as a result.

Q3: why is the housing market so tight?

Entry level is loosening up as more illegals are deported. The coming crackdown on H-1Bs will free up many more mid-tier properties. Lots of mortgages will be scrutinized, as it's become a material risk.

A few million properties here, a few million properties there, and all of the sudden there's not really a "housing shortage".

Yes, there are that many renters and property owners that are illegal to some degree.

Q4: what's up with CA, OR and WA? (investment advisor lives on west coast).

Sell now before the rush. The states are coming after anyone who is productive and has assets. You've been warned.

Personal opinion only, not investment advice.

2

2

52

Jun 9

This is how Florida rain works.

Jun 9

Tonlarca suyun acımasız gücü: Araba saniyeler içinde kağıt gibi ezildi

31

Jun 9

This tracks.

Most people think the real cost of a data center is all the hardware sitting in racks, which depreciates ridiculously fast.

The land, the building, the staff, the cooling, the energy costs, the risk of political targeting, etc. -- all point to a space-based solution.

Hardware and launch costs decline rapidly. All those other factors don't.

All you really need is a cost-effective launch mechanism 😀

Quick napkin math

Vera Rubin rack is $8 million

SpaceX AI1 satellite weighs 2 tons

Launch cost $200K

All in, including solar etc, about $10M to put a Vera Rubin rack in space, vs roughly $12M per rack on the ground with cooling and other infra.

Free electricity saves more than $100,000/year on 120 kW.

1

29

Jun 9

Apple's recent Siri move makes sense, and this is why.

AI has redefined our notions of user interface, applications and all of that.

If historical patterns hold, there will be three battlegrounds for market dominance:

- enormous compute clusters used primarily for model training

- midrange compute clusters owned by organizations that do primarily inference and limited training

- personal computing devices owned by individuals that do mostly inference and very little training.

The Apple Siri announcement is aimed at that third audience -- people who just want their personal tech to work together seamlessly.

Their only real competitor is Tesla, who is working on doing the same thing for the next wave of personal tech: cars, robots and direct brain interfaces.

The choice of AI model matters much less than delivering a consistent experience across all devices.

Jun 9

apple’s siri AI looks dumb until you realise it’s about to launch on 3.5 billion devices overnight, tap into the richest data set in consumer history and easily improve the lives of its users in some obvious ways:

-> siri’s always on (even offline), works across any app.

-> trained on your texts, calendar history, email etc = instantly the best personal agent

-> apple not charging for use (unless usage limit result?)

-> models run privately on-device via google cloud.

best part is apple can use any ai model. they could easily partner with anthropic or openai to serve their models, they’re agnostic - but in doing so siri ends up being the orchestrator.

genius patience from apple to chase the model hype and focus on distro.

27

Jun 9

Like many conservative Floridians, deciding who to vote for in the primary isn't the easiest choice.

We've been spoiled by history's greatest governor for two terms, and now there are some hard choices ahead.

Not speaking for others, but I now believe that @jaycollinsFL will do the best job of preserving FL's amazing policy run.

The other candidates are staking out somewhat radical and ill-advised positions, eroding any confidence I might have in them.

Sometimes the best course of action is to simply stay the course.

11

Jun 9

Question:

Who is funding the "Florida Policy Project" to post this pro-taxation propaganda?

Local govt labor unions? Some other kickback scheme?

No one seriously believes any of your nonsense.

Who is paying you?

Jun 8

Question:

Is Florida’s five-year residency requirement constitutional?

Supporters say new residents already wait for homestead benefits.

That’s true.

But once you qualify for homestead today, every Floridian receives the same exemption.

This proposal changes that.

A homeowner who established residency in 2025 receives one benefit.

A veteran who retires after 30 years of military service and moves to Florida in 2027 receives a smaller benefit for years.

Same neighborhood.

Same assessed value.

Same homestead status.

Different tax benefit.

The U.S. Supreme Court struck down California’s attempt to give newer residents lower benefits simply because they arrived later.

Can it tell a veteran, “Thank you for your service and welcome to Florida. Please pay higher taxes for five years because you haven’t earned the full benefit”?

Maybe.

Maybe not.

But if this amendment passes, don’t be surprised when the courts ask a simple question:

Can Florida create probationary Floridians? After 30 years serving his country, should a veteran have to spend five more years earning equal treatment?

1

1

1,107

Jun 9

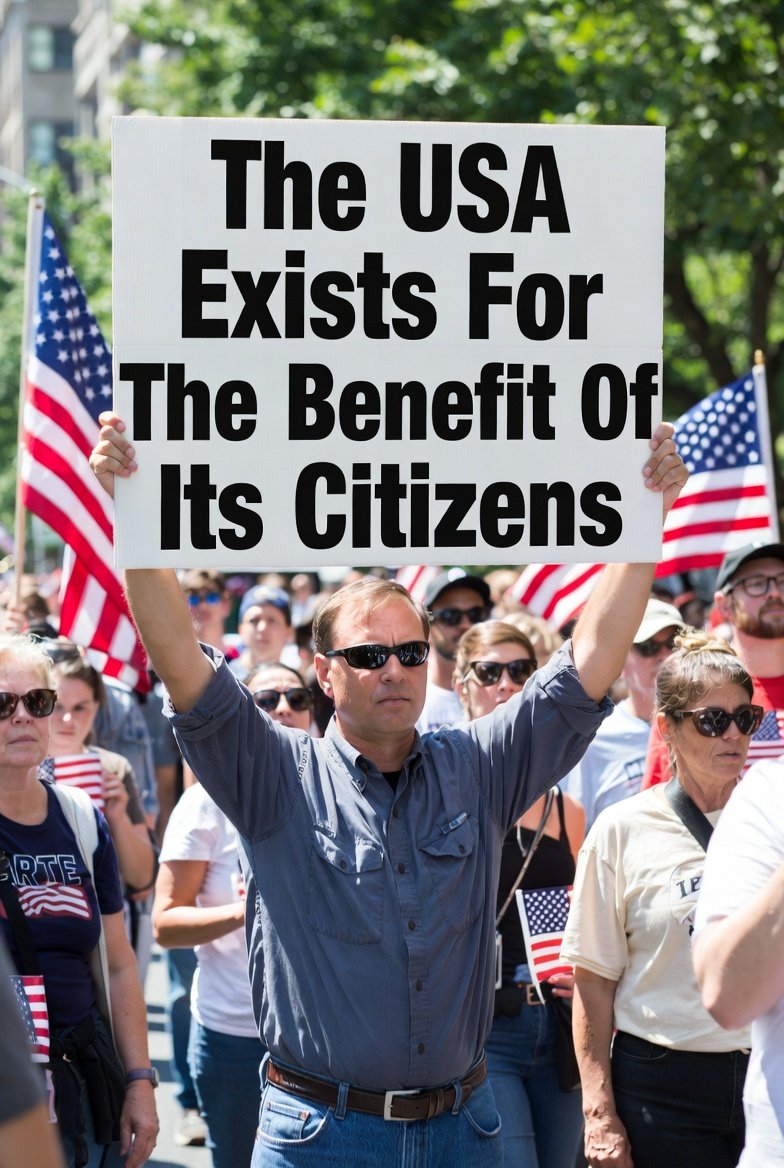

For the 2024 election, illegal immigration was the #1 issue, as it affected all the other issues people care about: crime, housing, jobs, social benefits, etc.

People realized that if you remove the illegals, crime went down, more entry housing became available, more entry-level jobs became available and government fraud was reduced.

Even though we've made progress, it's still the #1 issue in 2026.

We've realized that illegals contribute to election fraud, cause needless deaths on our highways and have gamed the H-1B system, thereby depriving American citizens of millions of good-paying jobs.

We're coming around to a simple truth: the USA exists for the benefit of its citizens and no one else.

If you aren't here legally, or aren't following the rules, it's time to go home.

13

Jun 8

Regardless of how this case is resolved, every H-1B visa holder has been put on notice, as well as every employer with a significant population of H-1B employees.

This administration, and likely the next one, will be working hard to reduce the number of H-1B visa holders.

From a corporate perspective, this is a new form of risk.

Companies are allergic to risk, especially new ones. Hiring platoons of H-1Bs as labor arbitrage might have made sense when it was risk-free.

But now it's not risk-free, and will likely be riskier in the future.

It won't be long before the corporate advisory class decides H-1B populations are a material risk and thus must be disclosed to investors.

Jun 8

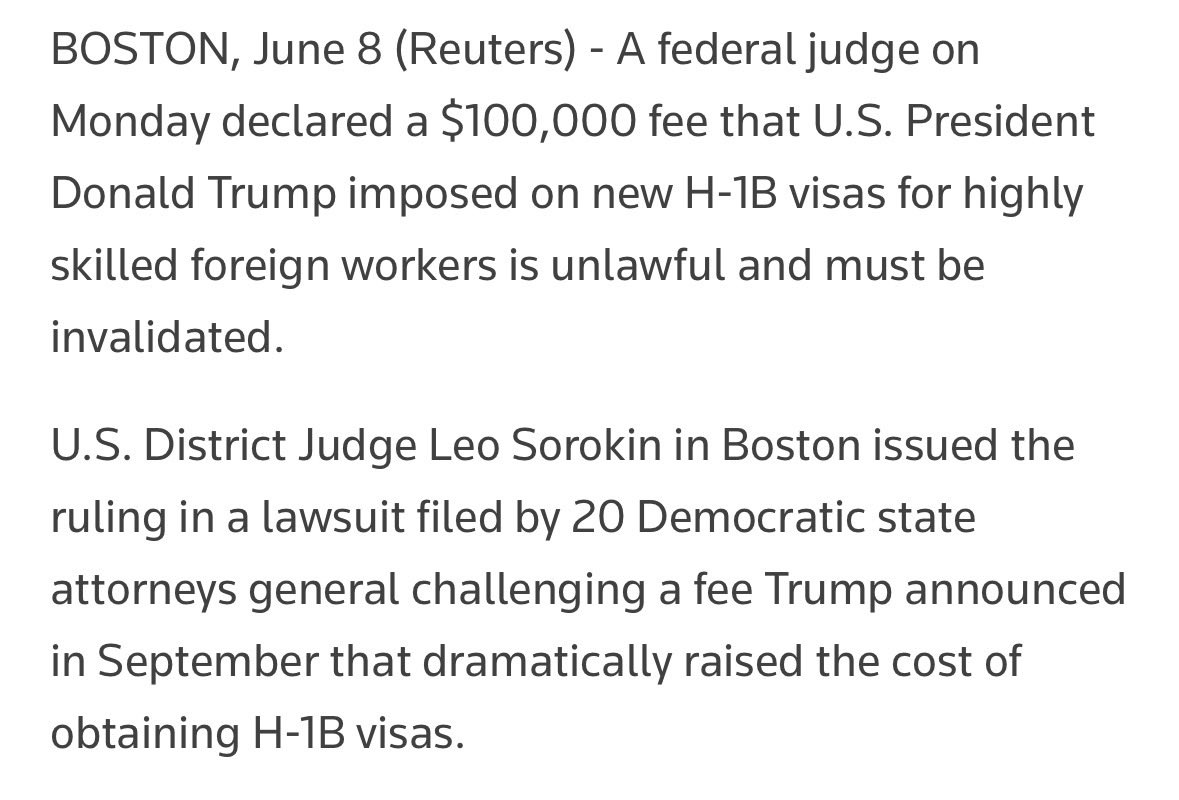

A Federal Judge in Boston, MA just ruled the $100k H-1B fee is and unlawful tax and must be invalidated.

The worst part is 20 Neo-Confederate state AGs lead the charge to defend unnecessary and bound labor in the United States.

How different would things be if lawyers and the legal industry weren’t gate kept by the American Bar Association?

Why not make lawyers compete with infinite foreign labor in an open market, like the rest of us?

Now can we get @KenPaxtonTX to sue and challenge OPT/CPT as an illegal jobs program, it’s loose disguise as a training program should be litigated.

2

55

Jun 8

Behind the scenes, this was excellent legislative work to minimize legal system abuses, which had become quite the industry in FL.

Lower the cost for insurers to operate in FL, and ratepayers see the benefits.

Grok had this to say:

------

SB 2-A (2022, property insurance focus):

Banned post-loss Assignment of Benefits (AOB) for policies issued after Jan. 1, 2023 — This stopped homeowners from assigning claims to contractors/public adjusters who often inflated repairs and filed aggressive lawsuits.

Eliminated “one-way” attorney fees in property insurance disputes — Previously, insurers often paid the plaintiff’s fees even if they lost; now parties generally cover their own.

Shorter claim filing deadlines (e.g., 1 year for new claims vs. 2), faster insurer response times (e.g., pay/deny in 60 days vs. 90), and other anti-fraud/claims process tweaks.

HB 837 (2023, broader tort reform affecting auto, property, and general litigation):

Shortened the statute of limitations for negligence claims from 4 years to 2 years.

Eliminated or restricted “phantom damages” (awarding damages for medical bills beyond what was actually paid/owed).

Reformed attorney fee calculations (lodestar method as presumptively reasonable; ended routine multipliers).

Modified comparative negligence rules and added protections (e.g., presumptions against liability for third-party crimes in secured properties).

Bad faith claim changes (e.g., safe harbor if insurers tender policy limits quickly).

------

Basically, it stopped people from gaming the system and put a bunch of billboard lawyers out of work.

I'm OK with that

Jun 8

USAA is returning $1 billion to Florida policyholders due to Florida’s successful market reforms.

1

42

Jun 8

During my career working for IT vendors, I saw many large shops go from 90% US citizen to 90% H1B in about a decade.

There was an entire outsourcing industry built around cheap H1B labor cost differentials. I saw hundreds of thousands of skilled roles change hands, so maybe many millions overall in my industry?

One of the all-time scams perpetrated on the American worker.

Jun 7

The H1B program is rife with fraud. How many Americans have been hurt by this farce?

1

26

Jun 8

Everyone who is watching the Mayoral primary in LA and wondering "how can that happen?" needs to understand it's largely legal.

Ballot harvesting is legal. Anyone can vote, even if they're dead, not a legal citizen or don't live in the area.

That's what they mean when they say "count every vote".

Anecdotally, the market rate for a harvested vote is $8-$12 each with prices increasing with demand. It's a business.

Need 20,000 votes in a hurry? Maybe $250k, certainly affordable by a donor or too. No groundswell of support required.

That's why the SAVE Act is required to fix the problem.

11

Jun 6

Just a reminder?

Every illegal alien working in the US is one less unskilled job available for an American citizen.

Every H1-B visa holder working in the US is one less skilled job available for an American citizen.

The housing they rent or buy means fewer options for American citizens who must pay more.

The social benefits they consume means less available for needy American citizens.

Easy prediction: as enforcement continues, unemployment will continue to drop, wages will continue to increase, housing will become more affordable and more social benefits will be available to the truly needy.

Jun 6

🚨#BREAKING: A MASSIVE IDENTITY THEFT RING that let nearly 50 ILLEGAL IMMIGRANTS work using the STOLEN identities of real Americans has just been taken down...

...and the EMPLOYERS WHO DID IT, HAVE BEEN ARRESTED!!!!

The American employers, a plant manager and an HR director were both INDICTED for KNOWINGLY HIRING ILLEGAL ALIENS!!!!

Four more people were indicted for running the operation that made fake Social Security cards, fake driver's licenses, and fake immigration documents...

...using the STOLEN identities of real American citizens.

The state of South Carolina wanted to act for YEARS, but the Biden administration refused to help them.

MORE OF THIS!!!!!!

START ARRESTING THE EMPLOYERS!!!!!!!

22

Jun 6

A low-IQ maladjusted kid kills another unprovoked.

His low-IQ family starts a race war as a defense.

His low-IQ lawyer sacrifices the kid for his own ego.

When people talk about the "cycle of ignorance" seen in human behavior, this is what they're talking about.

Each unfortunate decision leads to the next.

Also, this is how evolution works.

Defense attorney Mike Howard is trying to pull off an inside straight to get the jury to acquit Karmelo Anthony.

Under Texas law, he needs to prove ALL of the following to the jury:

-Anthony had a right to be present at that location (Stand Your Ground Doctrine);

-did not provoke the person against whom the force was used (Initial Aggressor Rule);

-was not otherwise engaged in criminal activity at the time , such as carrying the knife on school grounds (Part of the Stand Your Ground Doctrine);

-reasonably believed that deadly force was immediately necessary to protect against the other’s use or attempted use of unlawful deadly force (Reasonable Belief Doctrine);

-and that the threat of unlawful deadly force (or serious bodily injury) was imminent (Imminent Harm Requirement)

This is absolutely ludicrous.

13

Jun 5

I see this as a classic @elonmusk double-down move.

Would he rather have a compute farm with 110k Nvidia GPUs, or an additional ~$1B per month *right now* to invest in perfecting his rockets?

While other might be scratching their heads as to the reasoning here, he's got his eye on a much bigger prize that's demanding enormous amounts of cash just as it heads into IPO.

Everything he does is hyper-logical, you just have to think about things the way he does.

Jun 5

SpaceX has just announced that they have entered into a $920 million per month agreement with Google to provide compute capacity, according to a new filing.

"On June 5, 2026, we entered into a Cloud Service Agreement with Google with respect to access to compute capacity. The customer has agreed to pay us $920 million per month from October 2026 through June 2029, with capacity ramping up through September at a reduced fee. The compute capacity provided includes approximately 110,000 NVIDIA GPUs, CPUs, memory, and other related components.

After December 31, 2026, the agreement may be terminated by either party upon 90 days' notice. The customer will retain ownership of, and intellectual property rights in, its content, Al models, and related data."

25