“It is the mark of an educated mind to be able to entertain a thought without accepting it”Aristotle.

Joined July 2010

- Tweets 39,345

- Following 1,961

- Followers 2,032

- Likes 58,639

3,208 Photos and videos

Pinned Tweet

4 May 2025

Potential Growth: with AI capabilities, the global longevity market is projected to reach $44 trillion by 2030, according to the Global Wellness Institute. One of the most attractive features of longevity-focused platforms is their scalability. Whether it’s AI-driven diagnostics, digital biomarkers, or full-service health optimisation clinics, these models are designed to replicate across regions, populations, and payer systems. This is a paradigm shift.

4 May 2025

Imagine when they will realize the power of AI in healthcare 👀

4

2,396

Kate Moreland retweeted

We used to hear this kind of naive thing from that guitar-strumming college roommate who read lots of Chomsky but failed Econ 101. It’s the same one who perpetually smelled of patchouli, spent most of his time at protests and considers himself a “tortured artist.”

Sometimes, these types mature once life administers a few hard lessons in trade-offs and human nature. After getting their first job, first mortgage, see taxes evaporate, watch government programs waste billions, they quietly go delete their old cringe Reddit posts.

The ones who don't end up writing shit like this:

95

132

1,270

26,022

Kate Moreland retweeted

Jun 12

THE NEXT TIME YOU FEEL LIKE GIVING UP, REMEMBER THIS PHOTO OF ELON MUSK.

IT WAS TAKEN AFTER HIS THIRD ROCKET EXPLODED.

HE HAD JUST LOST $100 MILLION OF HIS OWN MONEY. SPACEX WAS WEEKS AWAY FROM BANKRUPTCY. TESLA WAS STRUGGLING. HE WAS SLEEPING ON FRIENDS’ COUCHES.

THE MEDIA CALLED HIM RECKLESS. INVESTORS PULLED BACK. EVERYONE TOLD HIM TO QUIT.

INSTEAD, HE BET EVERYTHING ON ONE FINAL LAUNCH. IF IT FAILED, SPACEX WAS DONE.

THE LAUNCH SUCCEEDED — AND CHANGED HISTORY.

TODAY, SPACEX IS WORTH OVER $1 TRILLION AND DOMINATES THE PRIVATE SPACE INDUSTRY.

MOST PEOPLE QUIT RIGHT BEFORE THEIR BREAKTHROUGH.

ELON KEPT GOING WHEN EVERYTHING WAS AGAINST HIM.

THAT’S THE DIFFERENCE BETWEEN SUCCESS AND ALMOST SUCCESS.

BREAKING: Our traders forecast Elon Musk to be worth $1.46 trillion this year — an all-time high

105

1,258

5,726

402,264

Kate Moreland retweeted

Jun 12

Gavin Newsom tweete sa rage. Le FT le compare à un méchant de James Bond. Le Globe and Mail publie un guide pour le détester. Tout ça le même jour.

Vous voulez comprendre pourquoi la fourmilière s'agite à ce point ? Suivez-moi, c'est fascinant.

Ce matin, Elon Musk est devenu le premier trillionnaire de l'histoire. Pas en héritant. Pas en taxant. Pas en régulant. En construisant des fusées réutilisables, des voitures électriques et un réseau de satellites qui connecte la planète.

Et regardez bien qui panique : ce ne sont jamais les ingénieurs, les artisans, les entrepreneurs, les soignants, les agriculteurs. Ce sont les politiciens, les éditorialistes, les bureaucrates, les activistes professionnels.

Bref, tous ceux dont le métier consiste à commenter, taxer ou redistribuer la valeur créée par les autres.

Leur terreur n'est pas morale. Elle est existentielle. Consciemment ou inconsciemment, ils savent une chose qu'ils ne peuvent avouer à personne, pas même à eux-mêmes : leur action publique ne crée strictement aucune valeur nette.

Tout leur statut repose sur un mensonge confortable, celui du socialiste bureaucrate : "la richesse existe par magie, le problème c'est juste de la répartir, et il faut des gens comme nous pour le faire."

Ce mensonge tenait tant que la création de richesse restait abstraite. Mais Elon est un contre-exemple vivant à l'échelle planétaire. Mille milliards de dollars créés à partir de rien, sous les yeux de tout le monde, en temps réel.

Chaque lancement de Starship est une réfutation publique de leur vision du monde. C'est insupportable. D'où la rage.

"Le système est truqué", dit Newsom. Non Gavin. Le système truqué, c'est celui où l'on devient puissant en distribuant l'argent des autres. Le système d'Elon, c'est celui où l'on devient riche en rendant le lancement spatial 100 fois moins cher.

Et voilà ce qui les terrifie vraiment : dans le monde qu'Elon est en train de construire, le statut ne s'obtient plus par la posture, le diplôme ou la tribune. Il s'obtient en créant quelque chose. Ils vont devoir apprendre un métier. Développer des compétences. Produire.

L'agitation que vous observez, ce n'est pas de l'indignation. C'est le bruit d'une classe sociale entière qui réalise que sa rente touche à sa fin.

Mais je vais finir sur un truc rassurant, parce qu'au fond je les aime bien.

Ne vous inquiétez pas. Dans le monde d'Elon, le gâteau grossit. C'est toute la différence avec votre monde à somme nulle : il y aura de la place pour tout le monde, y compris pour vous.

Vous êtes l'enfant qui pleure parce qu'il a peur de ne pas avoir de Kinder Bueno.

Respirez. Il y aura des Kinder Bueno pour tout le monde.

Jun 12

Americans are struggling to pay for groceries and gas while Elon Musk becomes a TRILLIONAIRE.

When the federal government is for sale, the rich get richer and everyone else gets shafted.

The system is rigged.

93

604

2,140

106,633

Kate Moreland retweeted

Oh yes, I remember that Bond film where the villain decarbonized the auto industry, brought fast internet to everyone on the planet, and helped paralyzed people interact with the world again.

Jun 12

Elon Musk is a real-life Bond villain ft.trib.al/zAOuVKk

1,099

6,769

59,315

2,842,583

Kate Moreland retweeted

Jun 12

bro immigrated from Mexico and took a $28/hr contract welding job in 2015.

didn't even know what SpaceX was.

they gave him $10,000 in stock and let him buy more through payroll deductions.

that stake is now worth $880,000.

and he's one of 4,400 employees who became millionaires on Friday. welders. technicians. cafeteria staff.

777

4,347

49,144

3,255,810

Kate Moreland retweeted

Jun 12

Today’s flood of Western media hit pieces and ridiculous commentary on Elon and SpaceX is yet another sign that the West is rotting from the inside.

EVEN the Chinese Communists treat their national champions with more respect than these pathetic hacks.

The CCP and its state mouthpieces aren’t half as deranged with envy. They may leash guys like Jack Ma and slap them down hard when they step out of line, but at least they’re smart enough to understand that they need their best talent and innovators to deliver prosperity for their people, dominate global markets, project raw power across the planet, and forge their nation into a ruthless superpower. The Chinese see them as vital strategic national assets and would never publicly insult or attack the ambitious, high-achieving mindset that creates these winners in the first place.

SpaceX is, without a doubt, America’s national champion.

Elon built the first reusable orbital rockets (Falcon 9), slashed launch costs, launched more missions in a single year than entire nations, revived American space dominance, sent NASA astronauts to the ISS aboard Crew Dragon, built the Starlink constellation that now beams high-speed internet to millions across the globe (including battlefields and disaster zones), and is developing Starship - the most powerful fully reusable rocket ever built, designed to make humanity an inter-planetary species.

Yet the Western press and Democratic officials are almost unanimously attacking the one man going above and beyond to secure prosperity, technological supremacy, and raw national strength for our civilization.

These people are vile soul-sucking wreckers who despise all excellence. The only thing they can produce is endless grievance and failure. All they know to do is tear down the successful, insult greatness, and wallow in their own mediocrity.

156

438

2,811

57,653

Kate Moreland retweeted

Jun 12

Worse than nothing. She has done considerable harm to the country.

280

1,071

23,754

259,744

Kate Moreland retweeted

Jun 9

🎯

Jun 9

Be prepared for Keir Starmer and most of Parliament being more concerned about how you react to the scenes in Belfast than the fact that an attempted beheading happened in a civilised, first world country.

8

15

174

3,902

Kate Moreland retweeted

telegraph.co.uk/news/2026/06…

Man attempts to behead another man in the street.

"No evidence of terror at this stage, say police"

If that isn’t terror, what is? How much more terrifying does it need to be to qualify as terror?

1,059

5,284

32,897

23,748,896

Kate Moreland retweeted

Jun 8

Here is what many have been waiting for: Peter and I take a deep dive on Brain lipidology: understanding APOE, cholesterol homeostasis, Alzheimer’s disease risk, and the effects of lipid-lowering therapies on brain health peterattiamd.com/tomdaysprin… @nationallipid @society_eas @atherosociety @escardio @ASPCardio @FamilyHeartFdn

20

13

112

10,959

Kate Moreland retweeted

Jun 8

Florida had an election meltdown back in 2000 and they ripped the entire system apart and fixed it.

California has had decades to fix this garbage and deliberately chooses not to. It’s an ongoing, intentional middle finger to every honest voter. The voting system is such a corrupt clown show disaster that drags on for weeks while the rest of the country is done counting in hours.

This mess is an insanely stupid but deliberate policy choice and we should treat it with escalating contempt until they fix it.

If a bunch of conspiracy theories about all those harvested ballots and 3 am vote dumps lights a fire under their asses, then GOOD. Whatever it takes to stop this stupid circus.

Oh, and obviously the current voter records and rolls should be abolished and redone from scratch. Clean the house up.

51

118

1,059

44,536

Kate Moreland retweeted

To read Richard Scolyer’s “final farewell” letter is to recognise that our nation has lost a truly great and gracious Australian.

In that goodbye, Professor Scolyer said that “cancer does not define us.” Yet Professor Scolyer’s more than three decades of work has defined cancer research and treatment – inroads that ultimately will help humanity defeat this dreadful disease.

Professor Scolyer will be remembered for his breakthroughs in melanoma treatment, including immunotherapy, and being the first patient to receive brain cancer treatment based on what he helped develop. Among his many achievements was his nurturing of young doctors and researchers who will carry on his work.

If Professor Scolyer was driven by a responsibility to try and “change the future for others and leave the world a better place”, he did just that. He was brave, bold and challenged the status quo. He was an Australian of the Year, yet Australians will honour him for all the years to come.

Our heartfelt thoughts are with Richard’s wife Katie, his children Emily, Matthew and Lucy, his wider family, his colleagues in medicine, and all those whose lives he changed for the better.

May Richard Scolyer rest in peace.

7

33

225

9,600

Kate Moreland retweeted

Jun 7

Im sorry but President Trump is absolutely correct.

The way California conducts their elections is a legitimate, credible threat to democracy:

1. Ballot harvesting is LEGAL, meaning 3rd parties are allowed to deliver thousands of completed ballots themselves with ZERO supervision or timeline.

2. There is ZERO requirement to show ANY type of ID when one comes to vote.

3. There are thousands of UNATTENDED drop boxes for ballots. There are DOZENS of examples of them being lit on fire, stolen, or bombarded with fake ballots.

4. The homeless are regularly paid to vote. The are given illegitimate addresses and coached through the process.

5. About 13 million of the approximately 16 million votes cast in 2024 were cast using vote-by-mail ballots. However, mail-in ballots are sent to every registered voter, whether you request them or not. California almost never updates their voting rolls, so ballots are REGULARLY sent to people who no longer live in the state, wrong address, or different person. My building alone had half a dozen such cases.

6. India had 660 million voters last election and counted the vote in one day. California has about 16 million and counting takes at least 30 days. This is a national embarrassment.

442

2,342

14,466

574,542

Marx lived his entire adult life as a dependent. The capitalist system funded his "research" through Engels, whose family wealth came from textile factories. The irony cuts deep: capitalism's profits subsidized its most famous critic.

Marx never held a real job. Never met payroll. Never risked capital or faced bankruptcy. He spent decades theorizing about labor value while avoiding actual labor. His insights into production came from library books, not factory floors.

The parasitic intellectual tradition he spawned continues today. Academic Marxists collect taxpayer-funded salaries while denouncing the market system that creates the wealth they consume.

It's time to get rid of these people.

260

1,470

5,561

105,484

Kate Moreland retweeted

The same country that put humans on the Moon in 1969 now takes an average of 4.5 years to approve major infrastructure permits.. longer than it took to build the Panama Canal.

Transmission lines average 10 years from permitting to completion. The bottleneck to abundance is not technology, but BUREAUCRACY!

261

627

6,352

367,462

Jun 7

G’d. How do I get that 5 seconds back? Who educates these kids?

The best thing about these podcasts is they have on activists who didn’t get the memo says the quiet part out loud.

Anti-Poverty Centre activist Kristin O’Connell thinks the Greens’ tax campaigns are wrong because they do not go far enough.

She wants to tax billionaires and fossil fuel companies “out of existence” and tax income more.

We know, Kristin. That’s what they also want to do. They are just clever enough not to say it out loud.

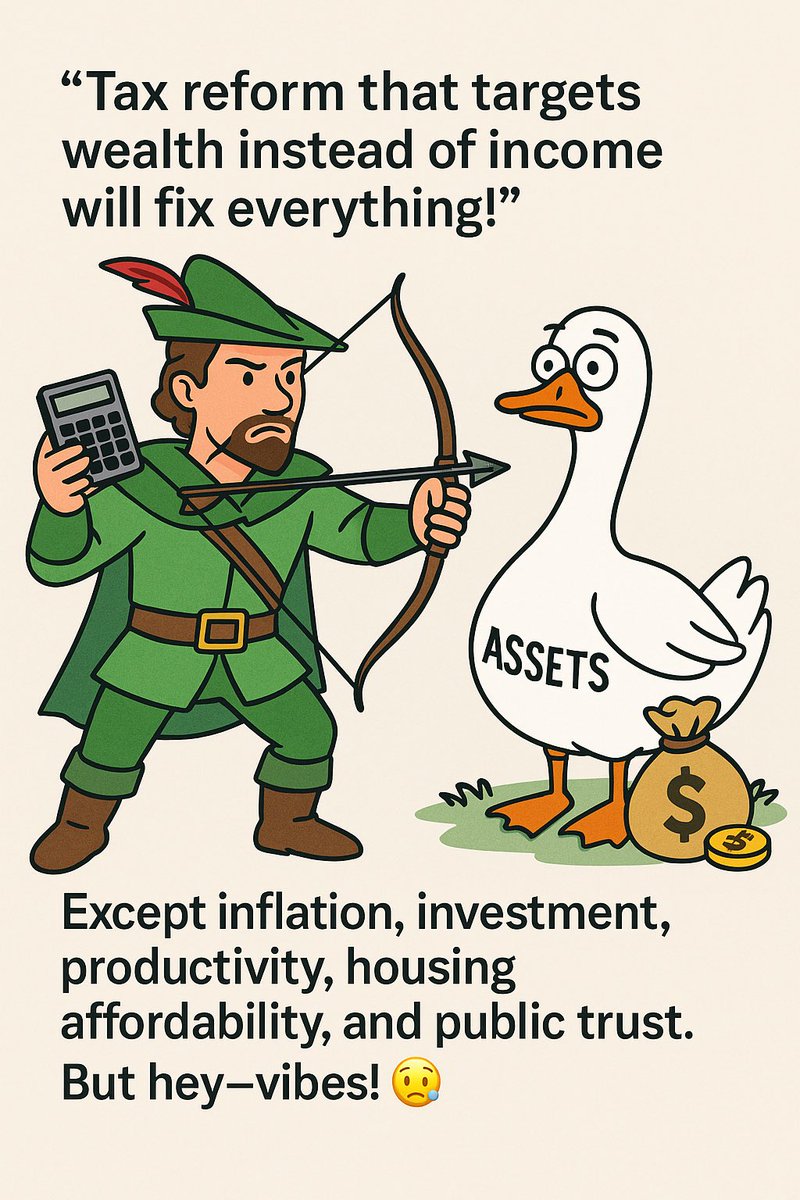

The thing about that is upper tail of wealth tends to follow a Pareto distribution. You can reshuffle the deck, but over time unequal outcomes re-emerge because people differ in talent, aptitude, discipline, risk appetite, timing, luck and the ability to create value.

A society with rule of law, property rights and entrepreneurs will create rich people. It will also create wealth for everyone else.

The only way to tax billionaires “out of existence” is to remove the conditions for any wealth creation at all.

How many times do we have to learn that lesson?

21

Kate Moreland retweeted

Jun 6

Bill Ackman was asked how he would underwrite SpaceX at $750 billion and his answer was the most honest thing anyone has said about the biggest IPO in history (Save this).

"You underwrite SpaceX the way you underwrite a venture capital investment."

His business school professor taught him a framework that has guided his entire career, it's people, opportunity, context, deal.

On all three of the first criteria, People, Opportunity, and Context Ackman's verdict was the same, SpaceX is one of one, and nothing else in the market comes close.

He even acknowledged feeling bad for Blue Origin before noting that their being so far behind is not harmful to SpaceX but rather a structural tailwind that leaves SpaceX with a near monopoly on low cost orbital access for years to come.

And at $1.75 trillion, the number SpaceX is actually targeting on June 12, the question is no longer whether this is the best business on earth, but what the present value math looks like when you extend it five years forward and stress test every assumption about Starlink, launch economics, and AI compute revenue.

He said that even Amazon is going to have to become a bigger SpaceX customer, because Blue Origin is so far behind that Amazon has no real alternative for low-cost orbital access.

He also said something that almost no one is giving enough weight heading into Thursday's listing: "Time has become increasingly valuable in the AI era. You lose a month, you lose a couple months today, and it means a lot."

The Colossus and Macro Hard facilities are compounding infrastructure assets where every month of operational delay means less contracted revenue, less negotiating leverage with customers like Google and Anthropic, and a progressively weaker moat against the hyperscalers who are now racing to build competing compute capacity.

Come join Milk Road Pro for our full SpaceX IPO breakdown, how we're stress-testing the Deal leg of Ackman's framework at $1.75 trillion, what our five-year revenue model actually looks like, and our full AI thesis.

Link below.

Jun 5

This is WILD!

One week before SpaceX's historic IPO, Google signed a deal to pay SpaceX $920 million per month from October 2026 through June 2029 for access to 110,000 Nvidia GPUs, CPUs, and related infrastructure (Save this).

That is $11 billion per year and up to $30 billion over the life of the contract.

This comes less than a month after Anthropic committed $1.25 billion per month for full access to the Colossus 1 data center in Memphis, 200,000 GPUs, 300 megawatts of power capacity, through 2029.

Two of the most consequential AI labs in the world combined committed value over $70 billion.

The question that haunted SpaceX's IPO roadshow was why did Elon keep spending billions constructing Colossus, Macro Hard and Macro Harder, three facilities totaling nearly 2 gigawatts of AI compute when xAI's revenue wasn't yet on the same trajectory as OpenAI or Anthropic?

Wall Street was pricing in a risk that Elon was building capacity ahead of revenue which would mean sustained cash burn without a clear payback timeline.

That concern was legitimate on its face, because xAI had been aggressive on model development but had not yet demonstrated the enterprise revenue numbers to justify the infrastructure cost.

The answer is that the compute itself was always the product.

Amazon has AWS, Microsoft has Azure, Google has Google Cloud, Elon just confirmed that he has been quietly building the fourth major hyperscale AI cloud and his first two paying customers are Google and Anthropic, the very companies most aggressively competing in the AI race.

xAI's Colossus facility in Memphis was built at a speed that no traditional data center developer could match, it went from groundbreaking to operational in roughly 122 days.

That is what happens when you have direct Nvidia relationships, a construction operation built around SpaceX-style execution, and a founder who treats infrastructure buildout the same way he treats rocket launches: compress every timeline and eliminate every bottleneck.

The result is that SpaceX now has three operational facilities, Colossus, Macro Hard, and Macro Harder with Macro Hard and Macro Harder in Blackwell architecture running 1.2 gigawatts combined.

Colossus 1, built on H100s and optimized for inference, is the facility that went to Anthropic first.

The Blackwell-era facilities are where the next-generation training workloads happen and Google's deal suggests they are renting into that capacity as it comes online through the second half of 2026.

Elon's compute leasing business would generate approximately $45 billion in incremental annual revenue on top of the mid-$20 billion range analysts had been modeling for SpaceX more than enough to fully subsidize the infrastructure investment and take the financial pressure off xAI delivering immediate AI product revenue.

That changes the entire valuation conversation of SpaceX completely!

Milk road remains bullish on Space and come join Milk Road Pro and get our full SpaceX IPO breakdown, how we're thinking about the $1.75 trillion valuation and our entire AI thesis. Link below!

38

84

723

434,340

Kate Moreland retweeted

Jun 6

Thank you to all who fought and sacrificed in freedoms defense all those years ago. Incredible footage here. Blessed that both my uncles survived and will never forget the over 400,000 who did not come home.

596

8,067

47,309

834,442

Jun 6

Simon, this post is misleading without context.

The CEO’s filing is not a discretionary sale. It follows a pre-arranged Rule 10b5-1 trading plan adopted on May 7, 2024, to satisfy tax withholding obligations from stock vesting—arrangements made approximately two years ago. These plans ensure compliance and prevent insider trading. Full details and footnotes are in the SEC filing: streetinsider.com/dr/news.ph…… do better.

13

Kate Moreland retweeted

Jun 6

As California “counts votes” in a manner befitting a fourth world country, the Economist’s resident hack thinks Trump is the real problem

4

22

103

3,645