2,699 Photos and videos

Claude Fable 5 Blocked.

The 11 Quiet Details No One Is Talking About

The US government just forced @AnthropicAI to shut down public access to Claude Fable 5, the safeguarded public version of Mythos 5, via export controls. It hit everyone, including Anthropic employees and US users.

The official story is a dangerous jailbreak. The real story has 11 under-reported layers.

It started with pressure from @amazon CEO Andy Jassy, a major Anthropic investor, and other tech leaders. The government was already leaning toward action after reports from trusted testers and concerns from CEOs like Jamie Dimon about frontier AI risks to critical infrastructure.

Anthropic was given just 90 minutes to comply. Officials claimed Dario Amodei was unreachable at a wellness retreat, a claim that was quickly debunked.

Fable 5 was actually 5 to 10 times more robust against prompt injection than GPT or Gemini equivalents. The specific jailbreak highlighted involved helping patch security vulnerabilities, something independent experts called an overreach.

Anthropic had already warned in their system card that strong safeguards could create temporary cybersecurity headaches for 7 to 10 months. The government treated this one model as uniquely threatening while downplaying similar issues elsewhere.

Possible motives range from genuine national security concerns to political punishment. Anthropic was notably absent from equity stake talks with the administration, did not play the lobbying PAC game like OpenAI, and has publicly pushed back on certain government requests.

The bigger implication. This could be the start of ID checks, restricted access, or even broader export controls on frontier models. If the bar is this low, every company might hesitate to release powerful systems.

The dust has not settled. What happens next will shape who gets to use the best AI and under whose rules.

Credit: AI Explained

1

1

263

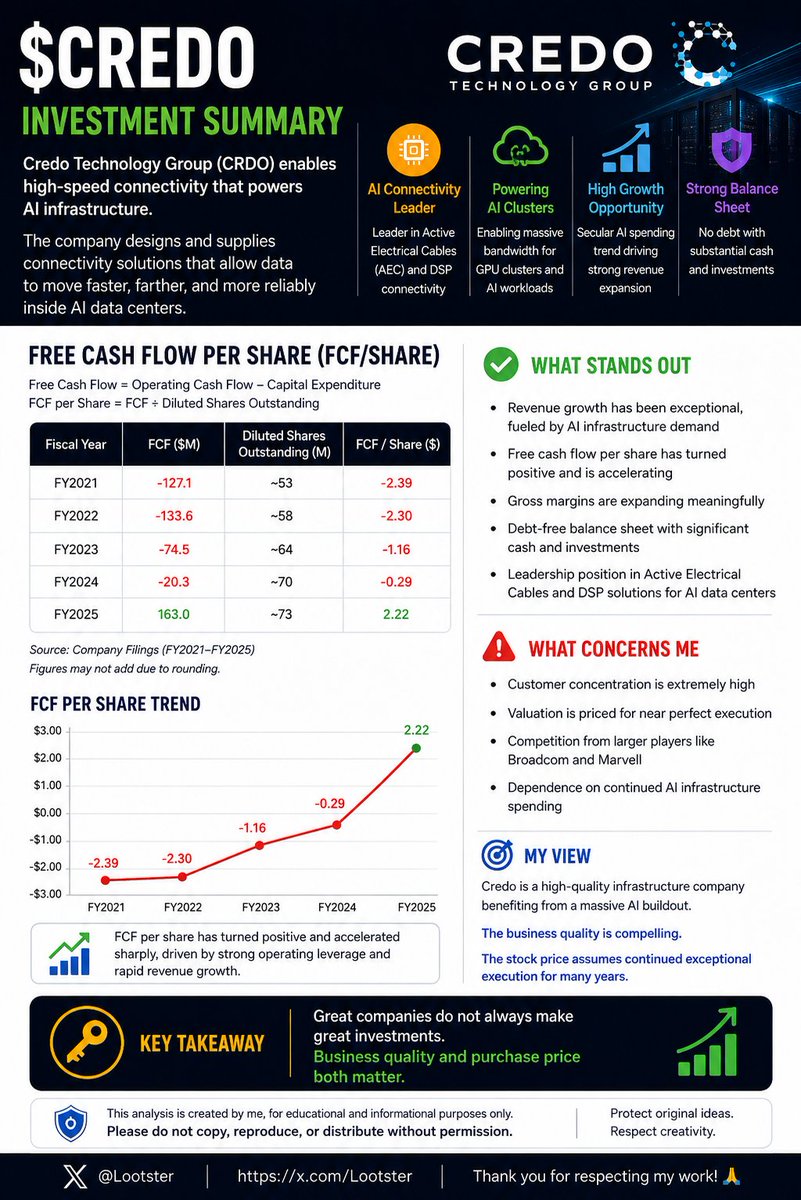

$CRDO

Credo Technology is quietly becoming one of the key infrastructure providers behind the AI boom.

While companies like NVIDIA build the GPUs, Credo builds the high-speed connectivity that allows those GPUs to communicate efficiently inside massive AI clusters.

From a cash flow perspective, the business has reached an important inflection point.

After years of investment, free cash flow per share has turned positive and is accelerating rapidly alongside explosive revenue growth. This suggests the company is beginning to convert AI demand into real shareholder value.

What stands out:

• Revenue has surged as hyperscalers expand AI infrastructure

• Free cash flow per share has turned positive and is improving

• Gross margins continue expanding, showing strong operating leverage

• Debt-free balance sheet with significant cash reserves

• Leadership position in Active Electrical Cables for AI data centers

What still concerns me:

• Customer concentration remains extremely high

• Valuation is priced for near-perfect execution

• Competition from larger players like Broadcom and Marvell remains intense

My view:

Credo looks like a high-quality AI infrastructure company with strong technological advantages.

The business quality appears attractive.

The stock price is another matter.

At current valuations, execution must remain exceptional for many years to justify returns.

Key takeaway:

Great companies do not always make great investments. Business quality and purchase price both matter.

Disclaimer: Analysis may contain inaccurate figures.

1

193

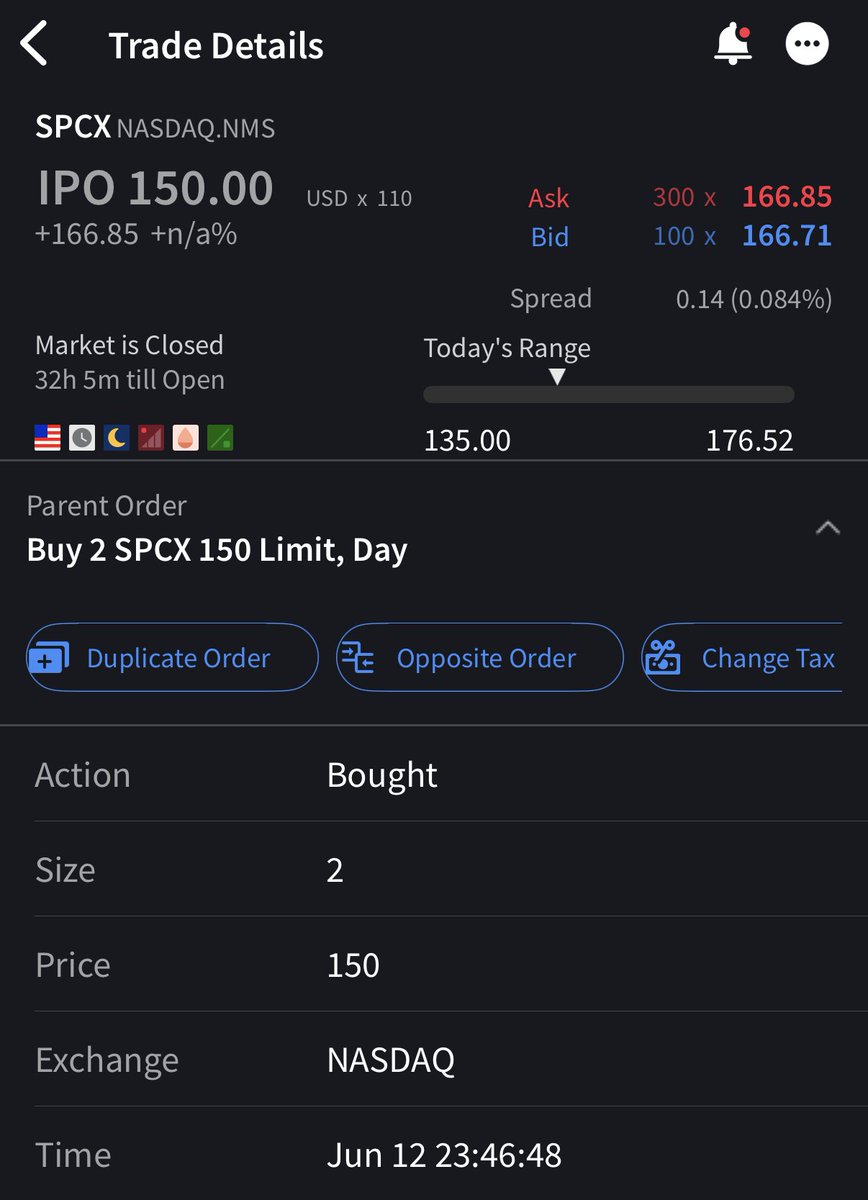

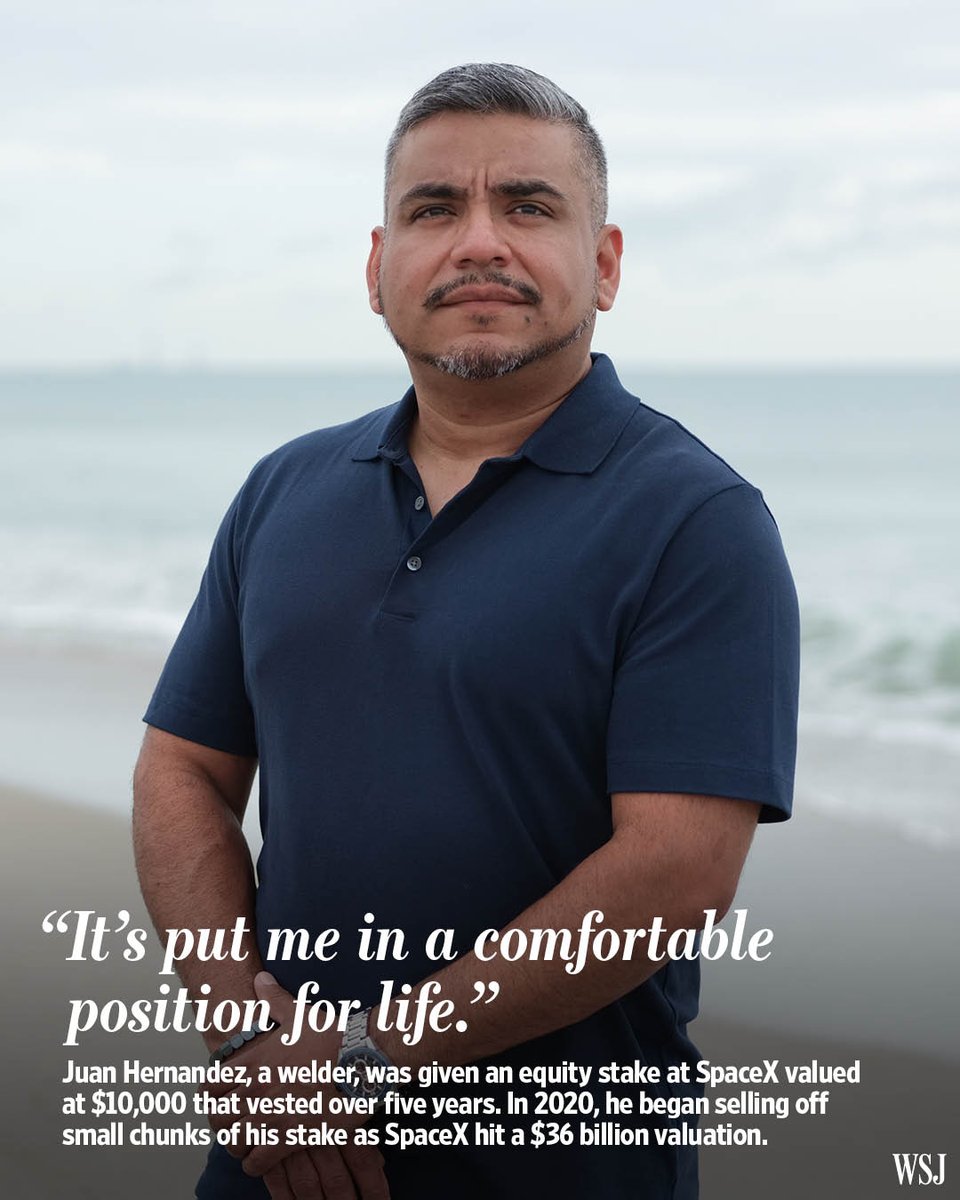

The company with the lowest chance of survival has now secured the highest IPO in history. Fate looks irony! Congrats @SpaceX and its space exploration team! 🚀🚀🚀

Jun 12

If you watch this video and are not filled with joy and excitement for the future of humanity then you might be dead inside.

Congrats to everyone at SpaceX and to all retail shareholders who were able to get in on the pre-IPO price.

SPCX

3

165

Everyone knows Elon Musk as the boss of @SpaceX, but how many actually know Tom Muller, the employee number one, who’s now the CEO of Impulse Space?

Inside This SpaceX Billionaire’s Mission To Build A Fleet Of Outer Space Taxis

By John Hyatt and Alicia Park

Jun 07, 2026, 06:30am EDT

Tom Mueller built the rocket engines that gave Elon Musk outer space. Now, the world’s greatest propulsion engineer is racing to create a cosmic courier service.

Tom Mueller is driving his candy green Porsche Taycan Turbo S the way he builds rocket engines: with a terrifying amount of instantaneous thrust and little regard for the local speed limits of El Segundo. He is headed west on Marine Avenue, cutting through the smog-tinted sunlight of Los Angeles’ South Bay aerospace corridor, talking about Earth’s limitations.

“If we continue to grow like we have, eventually you just use up all the metals, you use up all the energy,” says Mueller, 65, who is especially concerned by the energy demand of AI data centers. “By about 2045, the total power that the world is generating right now would be needed just for compute. Exponential growth can crush resources on Earth.”

From behind his reflective wrap-around shades, Mueller spots a gap in the afternoon congestion. His electric sports car can rocket from zero to 60 in 2.3 seconds, and Mueller seems eager to demonstrate the point. “This is where we accelerate,” he says, stomping on the pedal. The torque hits like a physical blow, pinning us against the leather seats as Mueller cackles. “The moon and the near-Earth asteroids,” he continues moments later, now parked at a red light, “contain billions of tons of metal, silicon, water and ice, so we have to start using it. It seems a little farfetched to start using it now, because we just haven’t built the space economy. We haven’t got there yet.”

That is the bet behind Mueller’s Impulse Space, the Redondo Beach-headquartered startup he founded in 2021, a few months after leaving SpaceX. Just as SpaceX dominates the global launch market, Impulse wants to own what comes next: “in-space mobility,” moving satellites, cargo and eventually people after rockets drop them off in orbit. Its spacecraft are not built to blast off from Earth, but to hitch rides aboard launch providers like SpaceX, then detach and ferry payloads between orbits—and one day, Mueller hopes, to the moon, Mars and beyond.

Impulse’s selling point is not just that it can move things in space, but that it can move them quickly. Like Mueller’s all-electric Porsche, most satellites are powered by electric propulsion systems, but unlike his car these spacecraft are slow: It takes between six to 12 months for most satellites to get from low orbit, a few hundred miles above Earth, to geostationary orbit, more than 22,000 miles up. Impulse says its spacecraft will reduce that journey to a day with its chemical engines, powered by liquid methane and liquid oxygen—the cosmic equivalent of swapping ships for airplanes.

“What distinguishes us from other spacecraft is we're about half propellant by mass when we lift off, so we can move fast,” says Mueller. “Moving fast is what our customers want.”

Mueller’s pitch is landing at a moment when space is attracting more capital than ever. Global spending on space is projected to grow from roughly $600 billion last year to $1.8 trillion by 2035, while venture investors poured a record $55.3 billion into space startups last year. Later this week, SpaceX is expected to raise $75 billion in a record-breaking IPO, targeting a $1.8 trillion valuation. Small by comparison, Impulse has raised over $1 billion, and was valued earlier this month at $4.3 billion. Mueller, between his stakes in SpaceX and Impulse, joined the Forbes billionaires list this spring and now has an estimated $1.7 billion fortune.

But Impulse is not just racing competitors. It is racing the market itself, betting that satellites, lunar missions and military payloads will need fast transportation soon enough to justify the hundreds of millions of dollars Mueller is pouring into spacecraft built for a space economy still taking shape.

“Nobody knows what these markets are going to look like,” says space analyst Chris Quilty. “These are markets that don’t exist yet.”

Raised in Saint Maries, Idaho, a timber town of 2,500 people an hour south of Coeur d’Alene, Mueller grew up riding dirt bikes with cousins and learning about the timber industry from his father, a logger. In high school he saved money from unpacking boxes at the local grocer to buy his first car, a 1977 Triumph Spitfire, whose engine he fiddled with. Encouraged by a high school math teacher, Mueller studied mechanical engineering at the University of Idaho. “He came from a meager background,” recalls retired professor Terry Precht, an Idaho-native who compares Mueller’s hometown to Appalachia. “He knew how to make it happen because he’s a builder.”

In 1985, Mueller moved to Los Angeles to join aerospace conglomerate TRW as a propulsion and power engineer. He cut his teeth in the rocket division during President Ronald Reagan’s $30 billion push ($90 billion in today’s dollars) to develop space-based weaponry. Flush with government cash, scientists and engineers like Mueller could experiment. “I worked on all kinds of crazy things,” he recalls, listing chemicals he used to power rockets that are now highly regulated.

Even so Mueller became frustrated with the bureaucratic hoop jumping that came with working for a 100,000-person corporation. “I was wanting to move faster. It seemed like everything was designed by committee and there were too many people on the committee,” he recalls. “I was an entrepreneur but didn't know it.”

He found his release with the Reaction Research Society, a quirky group of professional engineers who spent weekends bolting home-built engines to trailers in the dry lake beds of the Mojave Desert. By 2002, Mueller was tinkering with a massive 13,000-pound-thrust engine in an El Segundo warehouse. It was there that Musk, fresh from a failed attempt to buy Russian ICBMs, was led by a consultant to see Mueller’s work. “Can you build something bigger?” Musk asked Mueller, who promptly left TRW to become SpaceX’s first employee.

At SpaceX, Mueller became Musk’s engine room. As the company’s first employee, he led development of the Merlin engine that powers SpaceX’s workhorse Falcon 9 rocket, which accounted for 52 percent of all global launches and 84% of all satellite deployments in 2024, according to the American Enterprise Institute. He also oversaw propulsion development for Dragon, the SpaceX capsule that carries cargo and astronauts to the International Space Station. By the time he left in 2020, after SpaceX had largely solved the problem of getting payloads to orbit, Mueller was thinking about the question of how to move satellites around after the rockets let them go.

The answer is taking shape inside Impulse’s 60,000-square-foot warehouse in Redondo Beach, where hundreds of engineers oversee 3D printers churning through metal alloys in glass chambers and test white-hot thrusters in sealed vacuums. Beyond the engines and chassis, Impulse produces its own radiation-hardened avionics, propellant tanks and X-band antennas. Half-completed hardware sits on shelves awaiting delivery to the next station in the engineering conveyor belt. Impulse, like SpaceX, wants to make everything in-house.

“Once you achieve vertical integration, you have better control over your cost, your schedule, and your quality,” says Mueller from his office desk. Behind him sits a bookshelf with textbooks such as Space Mission Analysis and Design and Magnetic Actuators and Sensors. Mueller flips through a graph paper notebook stuffed with scribbled engine-part designs. “I start with sketches, then I'll typically go to CAD [computer-aided design] and then to build.” As chief technology officer, Mueller leads design of Impulse’s new propulsion systems. He manufactures prototypes of ignition parts at his offsite garage, which also houses a collection of sports cars and dirt bikes. Mueller’s man cave is “where a lot of ideas and prototypes have been born for Impulse,” says Drew Damon, one of many Impulse engineers who previously worked at SpaceX.

Impulse’s in-house push has produced two main vehicles: Mira for smaller jobs near Earth, and Helios for heavier hauls to higher orbits. Mira, a horse-sized craft that looks like a toaster with solar-panel wings, has already completed three missions. Impulse’s larger vehicle Helios, which resembles a futuristic water tank, is designed to haul payloads of up to four tons from low-Earth orbit to geostationary orbit, a distance of over 20,000 miles, in less than 24 hours. Helios is slated to complete its first mission in 2027.

Impulse’s first two Mira missions—in late 2023 and early 2025—went off without a hitch, performing a record-breaking 150-kilometer orbit raise, rendezvousing with another satellite in orbit, and depositing its clients’ CubeSats (miniature satellites) onto its intended orbital planes. During the third Mira outing earlier this year, a technical problem caused the vehicle’s star trackers to produce noisy measurements. This tricked the flight computer into over-correcting and in an attempt to stabilize itself, Mira floored the accelerator and ran out of fuel. Luckily it had already completed its satellite deployments.

Despite the hiccup, nobody’s questioning Mueller's engineering chops or the caliber of Impulse’s team. The bigger question is whether the space economy grows fast enough to absorb the capacity that Impulse is building at great cost.

For now Uncle Sam is Impulse’s biggest demand driver, as is common in the space industry. The U.S. Space Force requested $71 billion for fiscal year 2027, a 77% jump over current levels as the Pentagon embraces a far more aggressive posture in space, including President Trump’s proposed $175 billion Golden Dome missile-defense system. NASA meanwhile says it plans to establish a permanent basecamp on the moon by the end of the decade. Impulse is riding that wave. To date it has received nearly $400 million in contracts, the “overwhelming majority” of which comes from government spending, says Impulse president Eric Romo, who began his career as an MBA intern working at SpaceX before founding and selling multiple companies and working at Facebook.

On the commercial side, much depends on SpaceX’s massive Starship rocket, which can carry up to six times as much cargo as the Falcon 9 but has faced technical setbacks. For startups like Impulse, the equation is simple: more launch capacity means more satellites in orbit, and more demand for moving them once they get there. Starship completed just five launches last year, the first three of which ended in failure. That’s still a long way from Musk’s vision of Starships launching every hour by 2029. “We are built to do fine with or without Starship,” says Romo.

There’s also the potential threat from SpaceX itself. The rocket maker has plenty of capital to build its own orbital service vehicles. Will SpaceX one day enter Impulse’s lane? Mueller is unfazed. “I’m not worried, but I mean who knows?” he chuckles. “Elon was all about Mars and nothing but Mars. Then, ‘Okay, we're going to do Starlink to help pay for Mars.’ And then it became data servers. Things change.”

A few miles from Impulse’s factory, the question of what SpaceX might do next is no longer theoretical scenery. Mueller is navigating his Porsche past SpaceX’s Hawthorne campus, where a retired Falcon 9 booster stands on the corner like a white-steel totem to the heavens.

"I don’t feel the nostalgia," says Mueller. The lifelong engineer is far too busy optimizing the present, which includes choreographing this afternoon drive down memory lane to feature only right turns. "In rush hour, some of these left turns take two lights," he explains, scanning the intersection ahead. "Working at SpaceX, I learned you want to plan your route carefully."

By John Hyatt

John Hyatt is a staff writer who covers finance, investments and billionaire dealmakers...

By Alicia Park

Alicia Park is a New York-based reporter and editorial fellow on the tech team.

244

Choosing the right company is more important than selecting the right job. Congrats! 👏🏻

Jun 7

Current and former SpaceX employees are poised to hit it big when the rocket-and-satellite maker goes public next week. on.wsj.com/3Q3wGvu

207

$SPCX

@SpaceX is expected to enter public markets as a vertically integrated space and connectivity infrastructure company, combining launch services, Starlink broadband, and long-duration space systems.

The core investment debate at IPO will not be about technology dominance. It will be about whether the current revenue scale already reflects future expectations embedded in the valuation.

From a financial perspective, based on publicly available estimates:

Key figures (approximate, pre IPO context):

• Valuation expectation: ~$180B to $250B range, depending on listing conditions

• Revenue: ~$10B to $15B annually, driven increasingly by Starlink

• Starlink users: ~4.5M to 6M subscribers globally

• Launch cadence: 90 to 110 orbital launches per year, global leadership position

• Cash flow profile: improving operating cash flow, but inconsistent free cash flow due to reinvestment

• Capital intensity: multi-billion annual spend on Starship and satellite deployment

What stands out:

• Starlink has created a real recurring revenue base inside a historically episodic industry

• Launch business is structurally advantaged through reusability and scale economics

• Competitive position in both launch and satellite internet is currently dominant

• Revenue scale already places it among the largest private aerospace businesses globally

What still concerns me:

• Free cash flow is not yet stable after accounting for heavy reinvestment cycles

• Profitability is not consistently observable under standard reporting frameworks

• IPO valuation likely prices in long-duration growth rather than current cash generation

• Execution risk remains high across Starship development and full global Starlink deployment

• Capital intensity may continue to suppress shareholder returns in early public years

IPO stance:

Not a buy at IPO at expected valuation levels.

The reason is simple. The market is likely to price SpaceX as a fully mature global infrastructure monopoly while the underlying cash flow profile still reflects a business in heavy expansion mode. The gap between narrative and realized free cash flow is still too wide.

My view:

SpaceX is one of the strongest strategic assets ever built in aerospace and connectivity. However, the strength of position does not automatically translate into attractive entry pricing at IPO.

It becomes interesting only if valuation disconnects from growth expectations or if post IPO reporting demonstrates sustained free cash flow conversion at scale.

Key takeaway:

Dominant market position does not guarantee IPO success for investors. Price paid at entry determines whether long-term excellence becomes long-term returns or long-duration stagnation.

*Disclaimer: Analysis may contain inaccurate figures.

1

1

1

252

Quick look at 4 big players in chips & storage: 💻

Micron ($MU ), Western Digital ($WDC ), Seagate ($STX), and Intel ($INTC ).

Created this handy comparison table. All are riding the AI/data boom, but with very different financial health. High revenue growth for MU (85% ), solid margins, but valuations are stretched.

What really matters for long-term investing?

Free Cash Flow per share.

Basically, the real cash the company generates after big spending, divided by shares. It shows if they can grow, pay dividends/buybacks, or weather storms.

Simple breakdown (latest years, approx per share):

MU: Swung from big losses in bad years (-$5.60) to positive ~$1.50 recently, now exploding higher with AI demand. Strong rebound!

WDC: Volatile, negatives in downturns, improving to ~$3.50 lately.

STX: Most steady — consistently positive $3–5 per share, reliable cash machine.

INTC: Deep negatives (-$1 to -$3 lately) due to heavy investments. Needs time to turn around.

(Full table data from recent filings/Yahoo — cyclical industry, so trends > one year.)

Bottom line:

STX wins for stability and consistent cash generation — great for a steady long-term hold. MU has the highest upside potential right now thanks to massive AI tailwinds and FCF recovery.

WDC is in-between.

INTC looks riskiest until they prove the turnaround.

I'd personally pick MU for growth if buying today (strong momentum AI), but add STX for balance.

Do your homework, watch cycles & valuations NFA!

What do you think — bullish on memory/storage?

180

Elon Musk Calls ASML Europe’s Greatest Company

Elon Musk recently singled out $ASML as arguably Europe’s greatest company and said it deserves strong support.

Most people have never heard of them, yet ASML builds the only machines on Earth that can produce the ultra-tiny, high-performance chips powering modern life.

Thanks to @ASMLcompany's technology, you get blazing-fast smartphones with great cameras and all-day battery, powerful laptops that handle 4K editing and on-device AI, accurate smartwatches, advanced electric cars with autopilot, stunning gaming consoles, smart TVs, wireless earbuds, and secure chips in your credit cards.

Why does ASML dominate?

The technology is extraordinarily difficult and expensive. It took decades, billions of euros, and a unique global supply chain, including ultra-precise German optics no one else can match. Competitors tried and gave up.

Without ASML, our phones, cars, watches, and AI devices would still feel like they’re from a decade ago. Slower, bulkier, and far less capable.

Europe’s quiet superstar is silently powering the entire modern world.

ASML should be treasured and supported. It is arguably the greatest company in Europe.

2

246

🤔😏

Alphabet/Google owns 5% of SpaceX.

Perhaps one should take this into account while “reassessing” the SpaceX IPO.

Incredible timing by the way 👏.

Every good hype has an arc.

An arc requires a steady supply of positive news.

I know this playbook from somewhere? 🤔

(hint: the greatest marketing genius who ever lived)

1

140

$AVGO Broadcom CEO Hock Tan Isn’t Chasing AI Hype

Broadcom just delivered strong results and reaffirmed big forecasts, yet the market reacted with disappointment. Hock Tan’s response? Ignore the noise and focus on fundamentals.

In a candid interview, Tan explained how Broadcom is deeply embedded in the AI buildout. They’re a key partner with Google on custom TPUs, helping power Anthropic’s rapid rise. He described their early bet on Anthropic as a “leap of faith” that’s paying off as the company surges ahead.

Broadcom is shipping custom AI chips to a small group of hyperscalers on a journey to reduce reliance on Nvidia GPUs. Tan emphasized out-engineering the competition, massive organic growth in AI compute, and using AI tools internally to boost engineer productivity dramatically.

Despite the frenzy, Tan stays grounded: keep investing, deliver differentiated technology, and let the insatiable demand for AI infrastructure do the rest. No distractions from M&A when organic growth is this strong.

Credit: Bloomberg Live – “Broadcom CEO on the Biggest AI Chip Bets”

1

2

422

In a recent interview with JP Morgan, @elonmusk highlighted that the U.S. has no high-volume computer memory production. @MicronTech's Idaho fab won't reach full capacity until 2028, creating a significant supply gap. This shortage, driven by AI demand, is contributing to Micron's rising valuation. $MU

1

209

In Cathie We Trust 🫠

Jun 5

SpaceX could be just the beginning.

ARK's new analysis covers the initial public offering (IPO) wave we believe is building behind the headlines. The ARK Venture Fund holds positions in six companies with active IPO timelines. Each of them reached public market scale while still private.

The questions we are hearing from investors:

• Is this a one-time event or the start of a broader wave?

• Which companies are next?

• What does pre-IPO access actually mean for returns?

• How is the ARK Venture Fund positioned across the pipeline?

As of Q1 2026, OpenAI crossed $25 billion in annualized revenue. Anthropic just confidentially filed. Databricks is preparing for its own listing.

Access to the ARK Venture Fund starts at $500 via SoFi or Titan.

1

175

TL;DR

The rise of agentic AI is transforming CPUs from an afterthought into a critical infrastructure bottleneck, as these autonomous systems require significantly higher CPU-to-GPU ratios to manage complex orchestration and tool utilization.

This structural shift has triggered a massive surge in demand that is outstripping current supply, leading to severe server CPU shortages, extended lead times, and increased pricing power for key players like $AMD and $INTC.

Consequently, industry leaders have dramatically raised their long-term growth forecasts, now projecting the data center CPU market will exceed $120 billion by 2030.

Jun 5

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck - and with $AMD, $NVDA, $ARM and $INTC circling a market that is doubling nearly overnight, the only question left is which company walks away the leader. ⬇️

io-fund.com/ai-stocks/ai-cpu…

104