time to cook ( ͡° ͜ʖ ͡°)

Joined April 2021

- Tweets 1,816

- Following 231

- Followers 279

- Likes 11,845

169 Photos and videos

Jun 9

Overpromised and underdelivered from @realmadrid . That is not a CR7 level signing. Get to work.

Jun 9

Comunicado Oficial.

1

163

Jun 7

Rainy Sunday here, so took some time to re-read this post from my friend @JoshInvestsAI

What is interesting to add is $NUAI also owns a site of approximately 3,500 acres in Lea County, New Mexico (yes the same site where the lawsuit was just dropped).

That site has 7GW total capacity. Management has said it would be 2GW from natural gas, and 5GW from nuclear.

From their press release when they acquired the site: "The Lea County site was selected for its exceptional strategic advantages, including proximity to major gas transmission lines, existing power infrastructure, abundant water supply, a skilled local workforce, and high-speed fiber connectivity."

Now we keep talking about TCDC site in Odessa, Texas, but the NM site shouldn't be underestimated either. Still very early stages.

Things can get pretty wild for $NUAI over the next 36 months. All it needs is one little spark (the first 200mw deal with a HS), and the company suddenly becomes very credible and all this pipeline becomes a massive opportunity.

Buckle up, it's time to cook.

Apr 19

$NUAI Thesis

I know you’ve probably been seeing $NUAI across your timeline recently, and was wondering what the deal with the company is. When I first saw this micro-cap stock on my timeline, I was extremely hesitant. But, after looking deeper I started to draw parallels to companies like $IREN and $APLD before the markets inevitably priced in what they could be worth. For those of you who have been in $IREN you understand that a 10x means speculating on an asset before its true value becomes obvious to the market, and seeing a vision for a company that plans to transition to something different. I believe $NUAI is the next 10x opportunity at $4.60, and here’s why.

Introduction

$NUAI’s flagship site is called TCDC, or Texas Critical Data Centers, that is 1.4GW Gross or ~1GW Critical IT load, in Ector County near Odessa, TX. I believe the market is completely missing the scale of what is happening at the TCDC site. If you haven’t been paying attention closely it’s easy for the recent announcements to fly under the radar. Since the beginning of this year $NUAI has put out announcements every couple weeks forging partnerships with energy generation partners, hiring significant industry leaders, and working meaningfully to prep their site for their hyperscaler client.

Following the Breadcrumbs

At the beginning of the year $NUAI closed the acquisition of the remaining 50% stake of TCDC from SharonAI, their original JV partner on the project. This was to have total control over the land to build new partnerships, and likely at the hyperscaler clients request to bring a new JV partner to the table.

In late February $NUAI announced a 450 MW Behind-the-Meter Generation Plan at TCDC with Thunderhead Energy and TURBINE-X Energy to generate power for the project. They have a SPV/venture where they have partnered with a private equity firm to fund the capital required to source, install, and run 450MW of gas turbines. They will generate an ROI as they sell power to NUAIs TCDC tenant. This equipment is normally extremely difficult to source, and $NUAI was able to grab these 2-3yr long lead time items in an extremely supply constrained environment, showing the connections of the upper management. The notable thing about this partnership is that they don’t have to put any capital upfront for this equipment, allowing them to start generating revenues while loaning the equipment without huge dilution (~70m).

Then, in mid-March $NUAI hired Ted Warner, ex head of the Energy, Power, and Digital Infrastructure at Northland Capital Markers, where he successfully structured and managed more than $7 billion in financing solutions specifically for large-scale data center developments. This was the signal that caught my eye and made me significantly up my position in the company. Something notable is his PSU’s, or Performance Stock Units, which reward him significantly for “Entering into a binding commercial agreement with a hyperscaler for a minimum of 200 megawatts”. Judging by his history I put him as an A hire, and you can see more about his notable achievements here.

x.com/litigious_dulce/status…

Now, to get into the most recent developments that completely change this company from just a speculative random micro-cap to a more credible multibagger infrastructure play. On April 1st, $NUAI secured an LOI with Stream Data Centers. Originally, $NUAI was slated to co-develop the TCDC site with other partners (first Sharon AI, then Primary Digital Infrastructure). However after back and forth for months the unnamed hyperscaler tenant likely mandated that their own preferred execution partner handle the physical construction and operation. Stream is one of the top data center

This project with Stream will be done in a GP/LP fashion, where instead of issuing billions in new stock to pay for construction, the deal utilizes a heavily levered GP/LP (General Partner / Limited Partner) joint venture structure, operating at roughly 80% Loan-to-Cost (LTC). The roles exist as such:

The Originator ($NUAI): $NUAI acts as the local sponsor. They bought the TCDC 438-acre site, secured the initial power footprint, navigated local Texas politics, and laid the development groundwork. Originally I had thought that this agreement would mean passing up the GP role fully to steam and forfeiting their GP revenue streams as the originator. After contacting IR they said “we expect the final structure to reflect the contributions from each (NUAI as a project originator local relationships, Stream as the developer)”

The Operator (Stream): Stream Data Centers steps in as the development manager and operator. They bring the engineering blueprints, the construction expertise, and the direct, trusted relationships with the hyperscaler. The hyperscaler obviously has a preference for this developer and has likely worked with them before.

The Institutional Capital (The LP): An unnamed institutional investor (99% confidence being Apollo, given their majority ownership of Stream) acts as the Limited Partner, writing the massive equity checks and leading the project financing. Apollo Global Management is consistently ranked among the top, most influential, and pre-eminent firms in private equity globally. It is commonly considered part of the "Big 4" of the PE industry and a mark of validation for this project that shouldn’t be looked past.

What this structure does is it protects $NUAI shareholders from the dilution that is so costly to shareholders in a company like $IREN, which long term (2-3 years) has potential to grow into a 100B market cap giant, but will need to dilute massive equity to get the cashflow flywheel going (as shown by 6B ATM). A 1.4 GW campus costs upwards of $12 Billion to build, and $NUAI cannot fund that on its own balance sheet. I expect this LOI to be facilitated into a binding agreement in the next 2-6 weeks.

The second piece of news that is the most convincing is the $290M credit facility from Macquarie. Just to put it out, in case it isn’t obvious already, Apollo and Macquarie don’t blindly gamble on some random micro-cap without doing extensive underwriting and due diligence on the parties involved. They deemed $NUAI worthy enough at a $250 million market cap to receive a $290 million multi-tranche facility that shifts the risk profile of the entire TCDC project.

The structure goes as follows: a $20M committed Term Loan A-1 to kick off development, followed by $30M and $40M tranches, with a massive $200M Delayed Draw Term Loan waiting for execution milestones. That’s already impressive in itself, and likely came from Ted Warner’s existing relationship with Macquarie, but an even stronger validation is the equity kicker. Macquarie took a direct $5 million equity stake at a 20% premium to market share price, taking their entry at exactly $5.00 per share. They also have a tranche of warrants that will have an exercise price of $5.00. The warrants will be issued across the first $50 million drawn on the Facility.

When one of the largest infrastructure lenders in the world is taking an equity stake at a 20% premium to the market’s price, it should tell you everything you need to know about the asymmetry of this setup. You have to ask yourself, would Macquarie offer a loan of this size to a random microcap without doing extensive due diligence and underwriting of an advanced hyperscaler LOI or term sheet?

Luckily, we got the answer to that hidden in the SEC filing of the Macquarie term loan agreement without a formal press release from $NUAI. $NUAI currently has an LOI in place with a hyperscaler tenant as of March 24th, 2026. I believe the reason it was not put in the form of a press release was at the hyperscalers request, and you can read more about it below from @kamikazzzi1981

x.com/kamikazzzi1981/status/…

Now that all of the pieces of the puzzle are starting to come together that a hyperscaler deal is imminent, what should the company actually be worth?

Stock Price Projections

Firstly, I'd like to get out of the way that if you believe that $NUAI will secure a hyperscaler deal in the first place the announcement alone will probably put the stock around 2x higher than the current prices, or around $9-$10/share. This is by giving Stream, one of the most reputable data center builders hand selected by a hyperscaler, around a 60% chance of execution from the math below. If you want to, from that point, you can decide whether you want to sell, or if you believe they can execute the numbers start to get pretty wild.

From Phase 1 alone, with super conservative assumptions (more likely to be ~$1.50M EBITDA/MW)

Phase 1: 200 MW x $1.35M EBITDA/MW = $270M project EBITDA.

At 50% ownership, that is $135M to NUAI.

At a 14x-16x EBITDA multiple, that suggests $1.9B-$2.2B of value, or $14-$16/share on 135.5M fully diluted shares.

Northland’s analysis used a 19x EBITDA multiple in their analysis, 14x-16x is extremely conservative. At a 19x multiple you get a share price ~19$/share

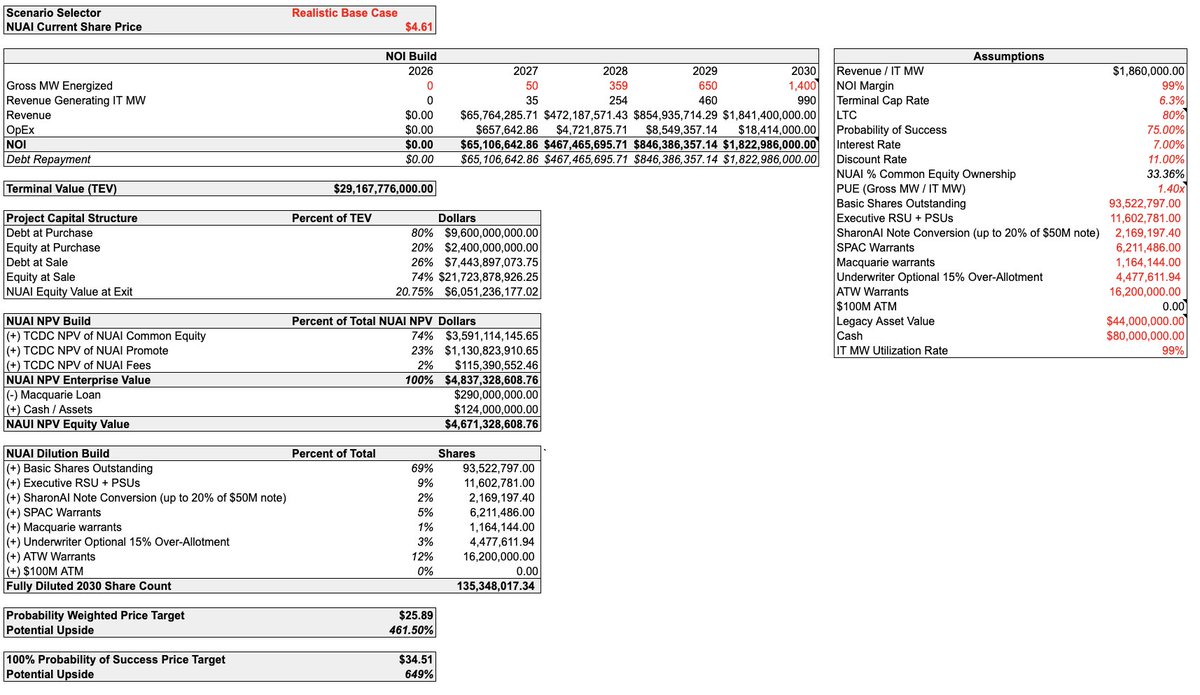

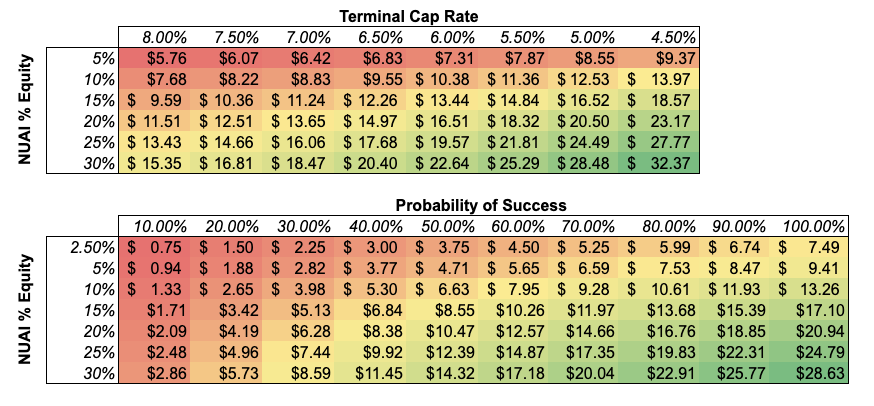

If they can fully execute on Phase 1, the full TCDC 1.4GW campus can be modeled out as done by @ThePrudentWhale

x.com/ThePrudentWhale/status…

• $34.51 Price Target in a 100% success case.

• $25.91 Probability-Weighted PT (applying a 25% execution risk haircut).

And here is super conservative bit of the model: this entirely excludes Behind-The-Meter power generation economics for phase 2 , GP stream revenues, 7 GW New Mexico development pipeline, and the reinvestment of cash flows into the futures phases of the projects for more equity.

1

6

42

4,754

Jun 1

More $NUAI great news.

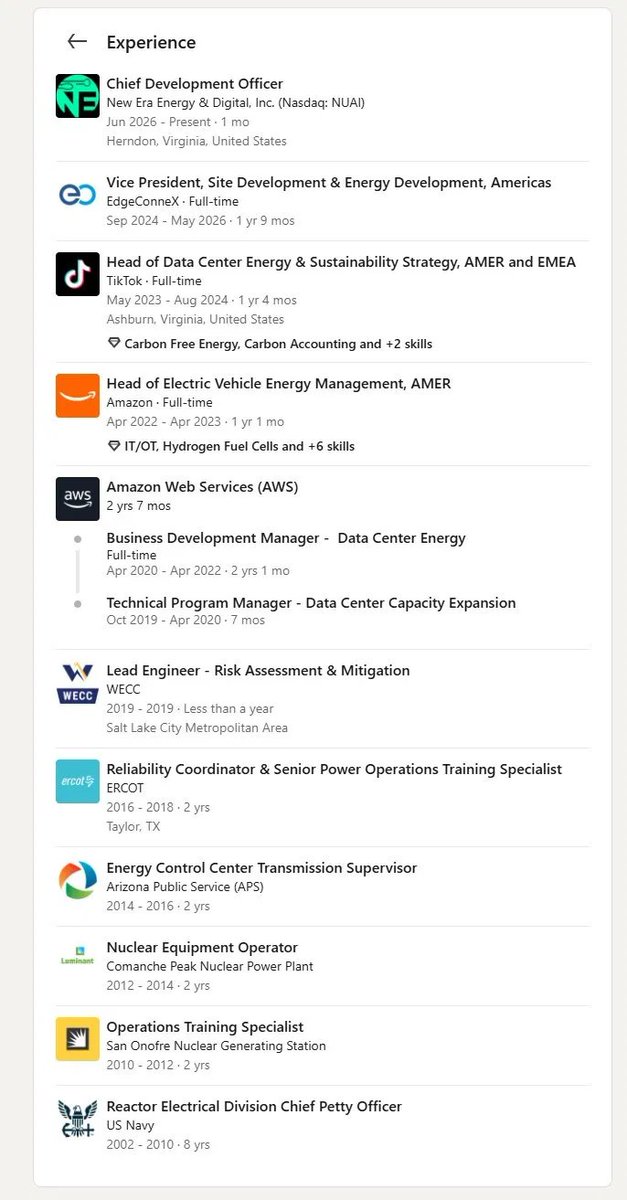

$NUAI just brought on Evan Pierce as Chief Development Officer.

Below is a brief summary of his experience:

Nuclear operator (Comanche Peak, San Onofre)

ERCOT reliability coordinator

AWS - data center capacity expansion and business development

TikTok - Head of Data Center Energy & Sustainability, AMER and EMEA

EdgeConneX - VP of Site Development & Energy Development, Americas

People with this resume don't join micro cap companies for a salary. They join because they see something others don't. I would not be surprised if he brings in a wealth of new connections and opportunities for $NUAI much like Ted Warner did on his arrival.

Maybe what he is seeing at $NUAI is hard to ignore?

The company has a New Mexico site with up to 5GW of nuclear capacity and 2GW of natural gas on deck.

You don't recruit a CDO who spent his career scaling hyperscale energy at AWS, TikTok, and EdgeConneX unless you're planning to actually build something.

I found this particularly interesting. He began his nuclear career as an Equipment Operator at Comanche Peak Nuclear Power Plant operated by Luminant, a Vistra company. Vistra sits right across the road from TCDC. I would not take this as a signal but would in some fashion highlight he has intimate knowledge of the industry and knows what needs to be done at the $NUAI level to get this deal across the finish line and expand the $NUAI footprint to future sites.

The talent being attracted doesn't lie. I saw this post via LinkedIn this morning. Looks like the thesis continues to play out for $NUAI.

2

1

22

1,463

May 27

The General 🫡

The TL;DR summary for those not subscribed is $IREN = generational wealth for all that hold.

May 26

New $IREN Deep Dive

Our new $IREN deep dive is finally live!

It's honestly the most comprehensive report we have ever released and something I'm firmly convinced will age like fine wine.

Even though it goes into great depth, it's written in a way that virtually every investor can understand. I purposefully went light on industry and finance jargon, and whenever I did use technical terms I made sure to explain them properly.

This time around I've also unlocked the entire first chapter for free Substack subscribers to read.

So if you're on the fence, I encourage you to read the first pages to get a sense of the depth and analytical quality you can expect from the rest of the deep dive.

I'm sure every $IREN shareholder, analyst, or investor curious about the company will derive great value from this deep dive.

I very much appreciate everyone's patience. This one took a while.

Enjoy! ✌️

agrippa.investments/p/irens-…

1

355

May 21

Excellent DD on $NUAI’s BTM setup

Everything is moving concurrently per mgmt. Hyperscaler lease is the last big piece.

Great post @samelifeenjoyer 👏

May 21

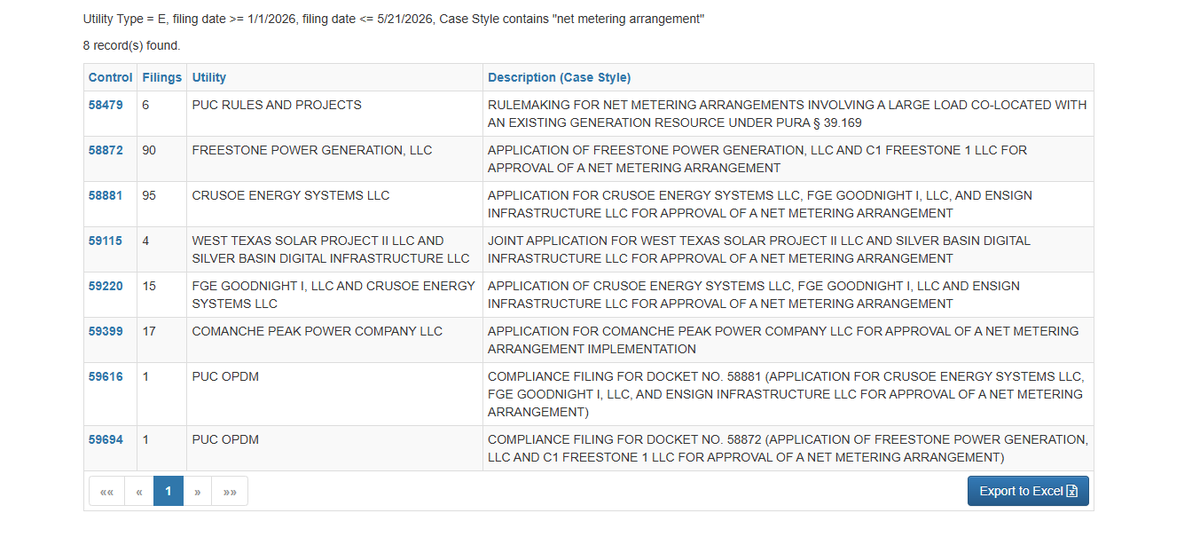

Following up on my $NUAI BTM colocation post. Did some digging into the PUCT docket and the regulatory picture just got significantly clearer.

The final rules for net metering arrangements under PURA § 39.169 were adopted last month. The framework $NUAI would use is now fully in place. Turns out my post was not speculation but is concrete which is good news for all of us.

Vistra filed comments in PUCT docket 58479, the exact rulemaking governing BTM colocation between existing generators and new large loads arguing specifically for a faster legacy track with a strict 180 day approval timeline. Companies don't spend legal resources on proceedings that don't affect their active business plans.

There's already a live Texas precedent. CyrusOne filed a BTM colocation application with Calpine for a 760 MW data center in Freestone County under the exact same framework. Fossil gas generator plus large data center load. Same structure $NUAI would use.

This is directly relevant to $NUAI's TCDC project. Calpine operates Quail Run directly adjacent to TCDC on the investor map. Vistra operates Odessa Ector Power Partners also directly adjacent. $NUAI has two active BTM colocation counterparties sitting on their fence line and at least one of them just proved the model works in Texas.

The 54 acre corridor connects TCDC directly to them. Yes, $NUAI would need a tie-in-station on their 54 acres of land. I do not want to oversimplify these engineering milestones but between Charlie, Will, HS selected engineering partner - Ramboll, and Stream I would suspect they are ahead of the curve on this.

One more thing worth addressing directly since I know someone will bring it up. No, Vistra/TCDC net metering application has been filed at PUCT yet. Just because there is not a public filing does not mean it is not in the works. Again, reminding us Charlie hinted at "one big signing day".

Here's why I am not currently concerned:

I pulled every active § 39.169 net metering application currently on file in Texas. There are five of them, see attached photo which highlights these documents. Every single one lists both the generator AND the large load customer as joint applicants. Freestone Power Generation filed with C1 Freestone 1 LLC. Crusoe filed with Ensign Infrastructure. The generator and the confirmed load file together. The Vistra Comanche Peak docket 59399 detail proves Vistra specifically knows how to file these applications and has done it already.

$NUAI hasn't announced a hyperscaler lease yet. That's the known missing piece, not the power solution. You don't file a net metering application without a confirmed load customer because ERCOT studies the specific load characteristics of the facility being co-located. Filing before the lease would be premature and put the cart before the horse.

If you would like to search around the PUCT site. See the link below. Maybe you will find something I did not! I found this to be directly relevant for all invested or looking to invest in $NUAI and figured a post here would be appropriate.

interchange.puc.texas.gov/

1

1

17

2,153

May 21

my goat

May 21

5 time Champions League winner, 5 time Ballon d'Or winner, 3 trophies with Portugal, titles in England, Spain, Italy & now Saudi...

Highest goalscorer in Real Madrid history, Portugal history, Champions League history, NT history, uncountable records to his name, 27 goals away from becoming the first to reach 1000.

Normally at this stage, after all these accolades, after winning so much, at the age of 41 someone would get bored and not have the same drive, the same motivation.

But, this is Cristiano Ronaldo in tears after scoring a brace to win Al Nassr the league in Saudi Arabia - after trying so much, after coming close so many times.

When you truly love something, you never get tired of it, not in a million lifetimes, not ever.

A player who lives with football. A motivation for everyone. Once in a lifetime player & person. Football is blessed to have Cristiano Ronaldo. 🐐

181

May 19

To add to $NUAI recap yesterday, transcript is available with key moments of the call.

May 19

$NUAI: The Last Asymmetric Bet in the Data Center Trade

Look across the small-cap data center cohort right now. NUAI is the only remaining sub-$500M name with a real, exclusive, late-stage hyperscaler negotiation in motion. And after parsing the Q1 2026 call, conviction goes up, not down.

The Lease Math Now Works Backwards From 2027

Charlie Nelson laid out the schedule cleanly:

"Our schedule is largely driven by power availability. The power that we have available in phases 1 and 2 is in second half of 2027. Everything that we're doing is kind of back-solving from those dates... We still feel good about second half of 2027 in-service date for the first phases of this."

Working backwards from ~August 2027 with Stream's compressed 12-14 month build cycle, the lease has to be signed by July or August 2026 to preserve schedule. The construction calendar is a hard forcing function — every party at the table knows it, including the hyperscaler.

The Documents Are Closer Than Anyone Realizes

When asked about sequencing, Charlie was specific:

"The JV docs are well underway, multiple turns already with the lawyers, and the lease as well, as well as the PPA. All of these are progressing concurrently... And this is how it goes with most of these types of industrial developments — concurrent execution, especially when they're all kind of lining up around the same time, just makes sense. And you just kind of have a signing day, if you will. A very fun day, by the way, for any industrial development."

"Multiple turns" means the documents are mature. What's left should be legal documentation — a slower, more deterministic process than commercial negotiation. The phrase "signing day" is not casual. It's deal-maker code for a coordinated execution event where multiple interdependent documents close together.

The Hyperscaler Engineered This Deal

This is the part nobody is talking about enough. The hyperscaler wasn't recruited. They initially came to NUAI wanting to buy the land. Ted Warner walked through the sequence:

"We were also getting offers to buy this from actual hyperscalers... One of those we did, we signed an exclusivity agreement because we kept turning them down on selling, and we wanted to work with them on how can we partner with you to own something here. Essentially, it was, 'You've got to work with a really reputable developer.' We went and tried to find one, that exact same party sort of led us to a different party. Now here we are with that party, Stream."

The hyperscaler directed NUAI to Stream. They didn't just suggest a developer — they pre-approved their own counterparty. Stream walked in with existing commercial agreements and pre-approved designs with this specific hyperscaler. Charlie confirmed it:

"Having pre-approved designs with this particular hyperscaler, which is why we were guided into the relationship with them, frankly — to the fact that they house long lead time equipment that goes towards these projects, and it's a rinse and repeat design."

A hyperscaler that takes the time to direct partner selection, share technical specs, sign exclusivity, and cooperate through a developer restart is not a hyperscaler that walks away at the finish line. That's a counterparty that has been quietly engineering the conditions for this deal to close on terms they already endorsed.

And It's the Same Hyperscaler

Ted's clarification on the Sharon AI confusion was the most underrated moment of the call:

"The same party, that hyperscaler is still the person that we hope will be our tenant, that our designs are specifically for... [Stream has] been incredible to work with, just every day checking boxes. It's been awesome to watch them work."

No one walked. The hyperscaler that wanted this site in 2025 still wants the site in 2026. The designs are still tailored to their specs. The exclusivity is still in place.

The Balance Sheet Is Built For This

Ted's segment removed the financing overhang that haunted this name for months. $80M cash on hand. $290M Macquarie credit facility. The Sharon AI note is gone. Liens lifted. They illustrated the math:

"Our cash needs for phase one would be roughly $180 million before the credit that we'd get for the land contribution... That theoretical $180 million investment is more than covered for phase 1."

NUAI's expected equity check for Phase 1 is fully funded. No more "how do they pay for this" question hanging over the stock.

The Setup

The market just sold the stock 11% on a quarter that confirmed every workstream is on track

The lawsuit resolution should come soon

PPA likely ready first

JV DA close behind — Stream is the most motivated party in the deal

Hyperscaler lease execution window: late June through Early August 2026

One signing day, three documents, complete rerate

This is the playbook setup for an asymmetric trade. The downside is bounded by the cleaner balance sheet, the Stream-driven execution model, and the standing hyperscaler engagement. The upside is a name with a sub-$500M market cap signing a lease comparable to deals that already moved peers multiples higher.

"As a shareholder, I sit here with you, and I wish I could announce who the prospective tenant is, and I can't wait to announce it one day. We've been working very, very hard to get there." — Will Gray, closing remarks

NUAI is the last shoe left to drop.

investing.com/news/transcrip…

1

15

2,677

May 18

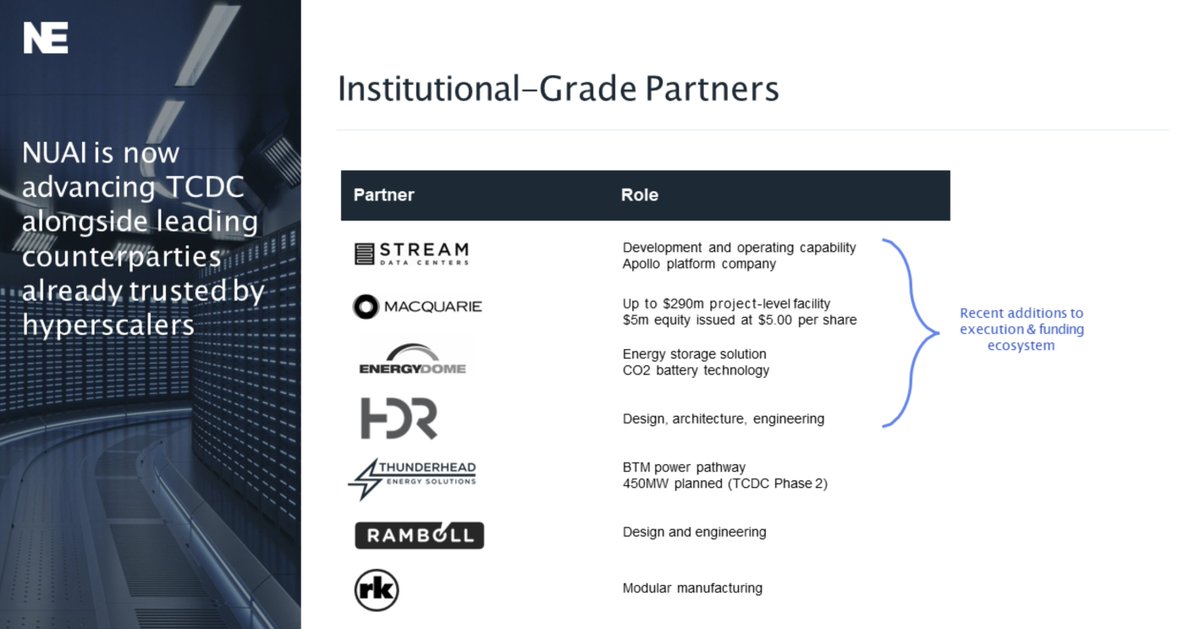

$NUAI earnings call recap. I only took the slides that I thought were the most interesting.

The partner slide is what stood out to me:

Stream brings data center development and operations, backed by Apollo.

Macquarie brings up to $290M in project financing.

Energy Dome brings long duration CO2 battery storage and already has a Google partnership.

HDR has worked on data center infrastructure tied to Microsoft.

Ramboll has worked on Meta data center energy projects.

Thunderhead is focused on behind the meter power for data centers.

RK builds modular data center and power infrastructure.

$NUAI assembled a solid and very credible group of partners.

3

5

48

5,017

May 18

Funding slide:

$NUAI is saying they do not plan to fund the full buildout alone at the parent company level.

They want project capital raised at the asset level, targeting 80% debt and 20% equity.

So no, this does not mean “no dilution ever.”

It means the big capex is meant to sit mostly at the project level, not fully on NUAI’s balance sheet.

1

1

8

1,502

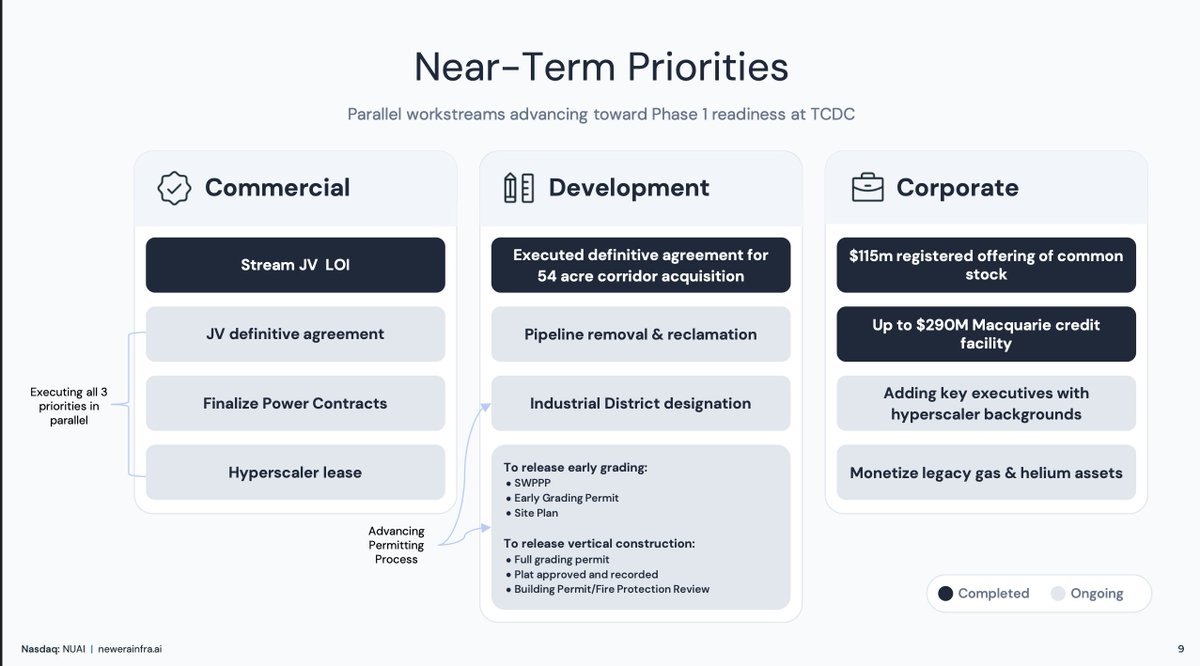

May 18

The biggest near term item is simple:

Hyperscaler lease.

That is the real unlock.

The land, power path, Stream JV, Macquarie facility, permitting and partners are all being lined up for that outcome.

Time to cook $NUAI

1

9

979

May 9

This is the best R/R out there now.

I took a position in $NUAI , and will aggressively add on every dips

May 9

NUAI: An Asymmetric Pre-Deal Position in AI Infrastructure

Summary

Investors comfortable holding $IREN, $WULF, $CIFR, or $APLD before they announced their first hyperscaler deals should be comfortable holding $NUAI today. The structural setup is materially identical with less execution risk. NUAI is operating the validated playbook those names established in 2025, with Stream Data Centers (Apollo-backed at $40B) and Macquarie already on the cap table, four hyperscalers as the only credible counterparties, and a six-month Macquarie clock functioning as a forcing function for lease execution.

Position Overview

Eighteen months ago, AI infrastructure names like IREN, WULF, APLD, and CIFR traded as speculative microcaps. Each re-rated sharply once a hyperscaler signed. Multiples expanded, floats compressed relative to opportunity, and the market repriced the companies from "miner" to "AI infrastructure platform."

NUAI follows the same template. New Era Energy & Digital has 650 MW secured in Ector County, Texas — the flagship "TCDC" campus — and management has confirmed advanced commercial discussions with one of four hyperscalers: Alphabet, Amazon, Meta, or Microsoft. The joint venture was organized by the hyperscaler, who selected Stream Data Centers as development manager and an institutional capital partner (Northland believes Apollo) to provide equity and arrange approximately 80% project-level debt. Stream contributes hyperscaler relationships and operational execution. NUAI contributes site control. The structure was effectively delivered to the company.

Why the IREN/WULF/APLD Comparison Holds

The standard objection to any "early-stage X" pitch is that every microcap claims to be the next something. Four points distinguish NUAI from generic versions of that pitch:

1. Secured land. 650 MW in Ector County is owned outright, not optioned or under LOI. The recent equity raise eliminated the SharonAI overhang and consolidated full ownership of the TCDC site. Power-ready acreage is the binding constraint of the entire AI buildout and the single hardest piece to fabricate.

2. Institutional capital. Macquarie wrote a $290M project-level facility. Apollo acquired Stream Data Centers for $40B in November 2025 and is the implicit equity partner on TCDC. Both are among the most rigorous diligence shops in private capital, and both are staked.

3. Professional execution stack. Stream as developer/operator; RK Mission Critical for modular fabrication and supply chain; Thunderhead Energy for behind-the-meter power; Ramboll / EYP Mission Critical Facilities for engineering. Charles Nelson joined as President/COO in February 2026. Ted Warner — with nearly two decades of capital markets experience and over $7B in HPC-related financing — joined as CFO in March 2026.

4. Binary counterparty universe. Four hyperscalers, all investment grade, all capex-constrained on power, all publicly committed to multi-year buildouts. Whichever one signs represents top-tier credit on a 15-20 year colocation lease.

Behind-the-Meter Has Become the Industry Default

A year ago, the consensus view across the data center industry held that behind-the-meter (BTM) power solutions were unworkable at hyperscaler scale. Critics argued that hyperscalers required utility-grade reliability, regulatory complexity would prove insurmountable, and BTM would remain a niche workaround rather than a primary power strategy. That view was a real overhang on every developer pursuing BTM as a path to capacity.

The consensus has reversed in twelve months. CIFR, APLD, WULF, and CORZ are all now executing BTM-led power strategies, and hyperscalers — facing multi-year interconnection queues and structural grid constraints — have endorsed BTM as a viable route to GW-scale capacity. Thunderhead Energy's role on the NUAI execution stack should be read in this context. NUAI is executing a strategy the industry has at this point publicly validated, with a power partner whose model is de-risked by parallel deployments at peer companies.

This is a meaningful update to the underwriting. The power-delivery question that was an open risk on every pre-deal AI infrastructure name twelve months ago is now the operating assumption across the cohort.

Stream Data Centers as the Execution Catalyst

In November 2025, Apollo paid $40B for Stream — for a particular set of capabilities that map directly onto why a hyperscaler would select TCDC.

Build-to-performance spec, not build-to-suit. Stream pre-aggregates standardized MEP equipment and configures it on the fly to customer specifications. The company quadrupled its development team during COVID and has been procuring long-lead equipment up to a year ahead of demand. Standardization speeds development time materially in a market characterized by acute power constraints and capacity scarcity.

Configurable cooling that future-proofs the asset. Stream's proprietary cooling design supports air cooling and direct-liquid-cooling on the same footprint, scaling from 10-12 kW per rack to 400 kW per rack. Customers can defer the air-vs-DLC decision until late in the build without extending the timeline, providing meaningful optionality across NVIDIA's roadmap from Blackwell to Rubin and beyond.

Pre-existing hyperscaler relationship. This element has been broadly overlooked. Because Stream has worked with this hyperscaler before, we can safely assume that a significant amount of work product can be leveraged for TCDC. Management's fall 2026 lease execution target is credible because contracts are likely being adapted, not drafted from scratch.

The distinction is between a startup negotiating with a hyperscaler from a blank page and the hyperscaler's preferred developer adapting an existing form to a new site. Execution risk lives in a different category.

Expected Value Framework

In my opinion, the probability of a deal with the current hyperscaler by August 2026 is 90% . The hyperscaler organized the JV. They selected Stream. They directed the structuring. Engineering and permitting are progressing without observable friction. Negotiations leverage Stream's existing templates and shared counsel. The Macquarie facility requires lease execution within six months, aligning every party's incentives toward closing.

As for the probability of any deal eventually, I would say 99% . If the current hyperscaler exits — for which there is no observable reason in a market structurally short on power-ready supply — the structural work is already complete. Site control, partner ecosystem, financing template, and engineering package are not counterparty-specific. Another publicly traded data center company recently demonstrated this dynamic: a hyperscaler counterparty exited, a replacement was secured, and the timeline extended by approximately one month.

Stress-tested at a deeply conservative 50% probability of a deal — well below what the structural setup supports:

50% × 4-5x upside ≈ 2.0-2.5x expected return

50% × 50% drawdown ≈ 0.25x expected loss

Net expected value: approximately 1.75-2.25x

At 90% probability, expected value approaches 3.5-4x. The asymmetry is wide enough that halving the upside and doubling the downside still produces a positive expected value.

Re-Rating Mechanics: Why a Deal Drives 200% From Here, Not 10%

A market-microstructure point underlies the upside case.

When mature AI infrastructure names — IREN, WULF, CIFR, APLD at current scale — announce hyperscaler deals, the stock typically moves around 10%. Optionality is already embedded, and announcements function as confirmation rather than revelation.

Smaller, less-followed names behave differently. DGXX has announced materially smaller deals than what NUAI is contemplating and moved 50% . Expectations are not embedded, the float is small, and the announcement forces a re-rating from speculative microcap to credible AI infrastructure platform (Note that a deal cannot be priced in because many institutions are waiting to buy until after a deal is announced).

NUAI sits closer to the $DGXX end on market cap and visibility but closer to the IREN/WULF/APLD end on asset quality and counterparty caliber. That mismatch is the opportunity. A first hyperscaler deal at TCDC could plausibly drive an immediate 200% re-rating — not because steady-state fundamentals support that exact multiple, but because microcaps gap rather than incrementally re-price. Investors do not get to scale into the new range.

Downside is bounded by the existing balance sheet, which is clean post-Macquarie and post-equity raise with no SharonAI overhang. Upside is a non-linear re-rating event.

The Case for Data Center Exposure

A reasonable question, given the breadth of the AI investable universe — semis, photonics, custom silicon, robotics, model labs — is why allocate to data center developers at all.

Data center economics are durable in a way most AI-adjacent verticals are not. Hyperscaler colocation leases run 15-20 years. Counterparties are investment grade. Cash flows are recurring. Once a campus is leased, it produces something close to a bond. EQIX has compounded through every macro cycle of the past fifteen years on this dynamic, and the structural reason is simple: an AWS region does not get turned off because the economy slows. Compute demand is structurally inelastic at the margin, and existing infrastructure is locked into multi-decade obligations.

The asset class is also tractable for non-specialists. Underwriting reduces to power, land, customers, and contract terms. Many other AI-adjacent verticals — photonics, custom silicon, neuromorphic, edge inference — are genuinely interesting and likely lucrative, but the underlying technology evolves quickly enough that most investors cannot reliably assess winners. Data centers fit Buffett's "in pile" — comprehensible, durable, and underwritable on standard metrics.

The constraint is that asymmetric opportunities within the data center space are increasingly scarce. For WULF to 5x from current levels would require multiple gigawatts of new capacity, additional contracts, and substantial revenue growth — achievable but grinding. NUAI requires one announcement with one of four hyperscalers for Phase 1 of TCDC. The bull case condenses to a single press release.

For investors who participated in the 2025 IREN/WULF/HUT/APLD/CIFR cycle, NUAI offers the same trade structure with two improvements: the underlying thesis has been validated by the prior cohort's outcomes, and the macro evidence — exponential capex guides, tightening power constraints, structural undersupply — is materially stronger today than it was eighteen months ago.

Conclusion

NUAI is structurally identical to the IREN, WULF, and APLD trades in early-to-mid 2025, with three improvements. The thesis has been validated by the 2025 cohort's outcomes. The execution stack — Stream / Apollo / Macquarie / Ramboll on day one — is more institutional than what several of those names had at first announcement. And the forcing functions are tighter, with a six-month Macquarie clock combined with a hyperscaler-organized JV on 650 MW of secured Texas power.

The position reduces to a single proposition: one press release reprices the equity by triple digits. Downside is bounded by an institutional cap table and a clean post-raise balance sheet. The expected value math holds at 50% probability and compounds at the 90% probability the structural setup supports.

Simply put, this is a remix of the IREN/WULF/APLD trade.

1

9

2,245

May 8

🎯🎯🎯🎯

May 7

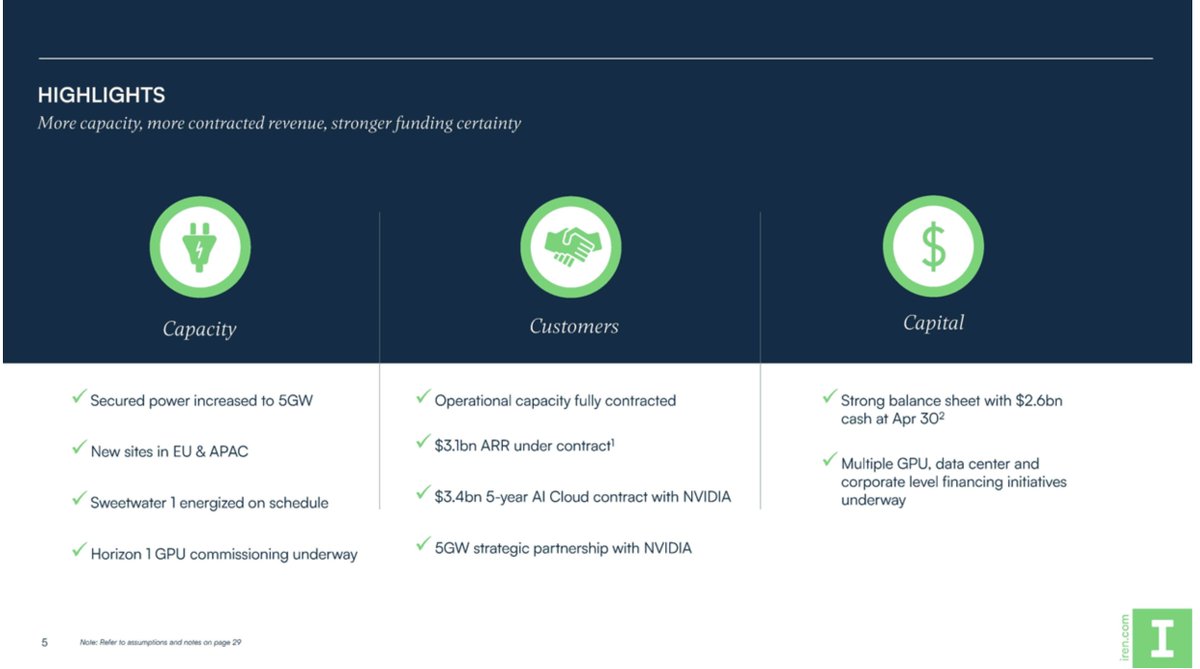

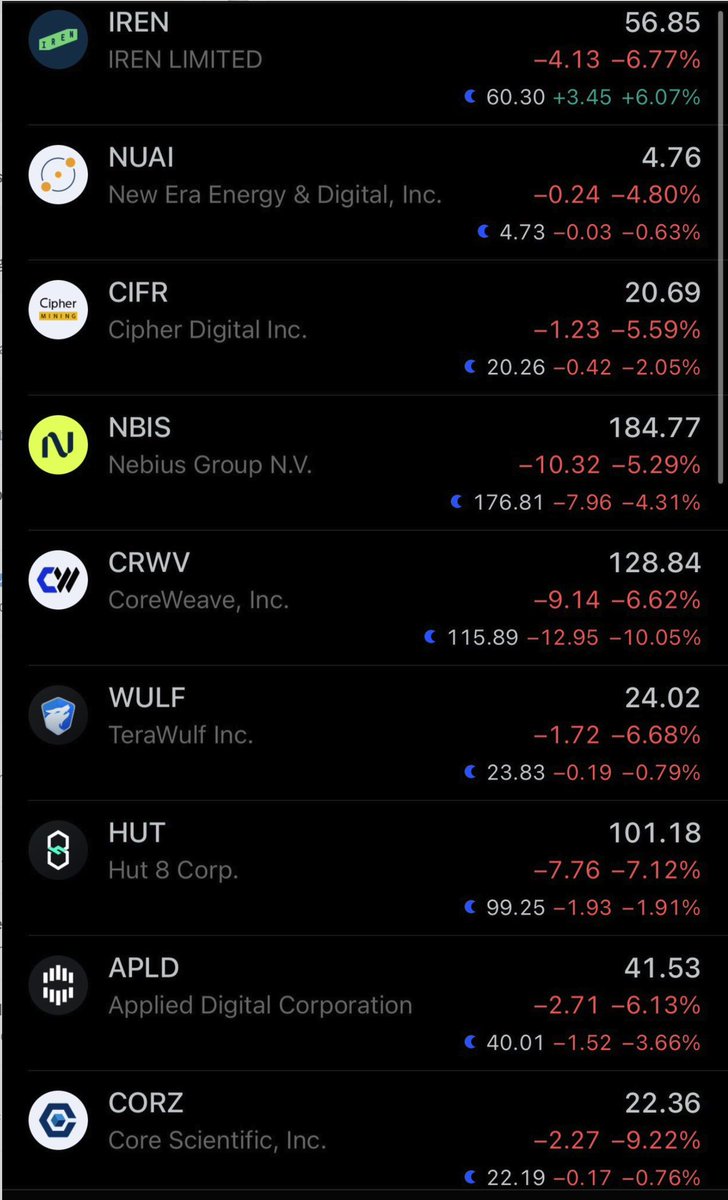

$IREN: First look at Q3 FY 2026 Earnings

Quick note - why is IREN giving back all it's gains from $72 -> $60? 1. CRWV had bad cost numbers and whole Neocloud sector is following it's 10% dump. 2. Reason I explain in takeaway 3.

Takeaway 1 - Nvidia Contract Economics

Nvidia 3.4B/5-year 60MW GPU compute contract with IREN for internal research usage.

- This is at 11.3m/MW which is 16% increase from 9.7m/MW MSFT contract. This is very meaningful top line increase given this is for air-cooled which means B300s. Much more profitable than MSFT contract and the topline IREN needs.

Takeaway 2 - Why is IREN Expanding Slower than Expected

Each GPU generation has greatly improve performance and economics. IREN has a "good" bias from the bitcoin mining days where it was a late move in order to have a fleet that was heavily skewed towards newer ASICs.

Technology moves very very fast in the beginning and AI GPUs are still considered early, IREN is trying to time where most of it's fleet is mid-stage GPU aka Vera Rubin or newer. Hence it's SW1 buildout is pushed out to 2027 so that it will be all Vera Rubins.

Yes, IREN is still scaling out it's DC buildout teams as this is all external and not contracted out like CRWV/NBIS. CRWV/NBIS for 2026/2027 capacity relies on 3rd parties and NBIS greenfield sites starts 2028. This is why IREN is full funded already for 2026 based on operational cashflow, existing cash on hand and has the Nvidia investment coming in later while NBIS still has 2026 funding needs even after the large convertible and Nvidia investment. Less aggressive but also less capital intensive.

CRWV/NBIS is your investment if you want to expand as fast as possible. IREN cares about unit economics and having a VR200 and newer generation fleet. IREN selects customer based on ability to get financing at best interest rate and has better rate on their convertibles than both NBIS's convertible and CRWV's corporate. Given corporate debt is apple or oranges but 9% on CRWV is meaningful enough to compare to IREN's 0% and 1.5% converibles and 6% GPU debt financing.

Takeaway 3 - Nvidia Option to Invest Instead of Immediate Investment

Market sees this the reason to sell $IREN back down from $72 -> $60. Whereas $CRWV and $NBIS got the money immeidately for shares at market price because they have 2026 unfunded needs, $IREN is fully funded for 2026 and would rather sell at above the market price. The way to negotiate this is to have the shares sold in the future at a premium at which the negotiations happen. Nvidia negotiations were happening today, they were happening when IREN was in the 40s so 70 is a significant premium. YtD relatively IREN at 70 is equivalent to $NBIS issuing shares to NVDA at 140.

IREN does not need the 2.1B in 2026, why dilute at $40? IREN will need cash in 2027 where it's buildout is going to accelerate so IREN is it then.

The important part is getting priority on Nvidia's delivery schedule. Nvidia does benefit by having the right to buy IREN stock through 2031 at $70 but everyone, everyone is paying alot to secure HBM which is on-chip with the GPU. This $70 call option for Nvidia is good for 600k GPUs.

Full Points

- 3.7B 2026 ARR runrate and 3.1B ARR already contracted. This means the Mackenzie GPUs are contracted! All the Prince George GPUs are contracted.

- New site in not only EU but APAC! Australia confirmed.

- 2.6B cash on hand. People can stop talking about the ATM for current liabilities out now. ATM is for future growth/deals/acquisitions.

- Will provide 3.4B of AI Cloud compute to Nvidia. Not counted in the 3.7B ARR so likely 2027. IREN is selling GPU compute to Nvidia internal teams!

- IREN secures 600k GPUs of Nvidia GPUs as part of partnership. Nvidia has right to buy $IREN at $70 as it delivers the GPUs to IREN, full $2.1B investment option upon delivery of 600k GPUs.

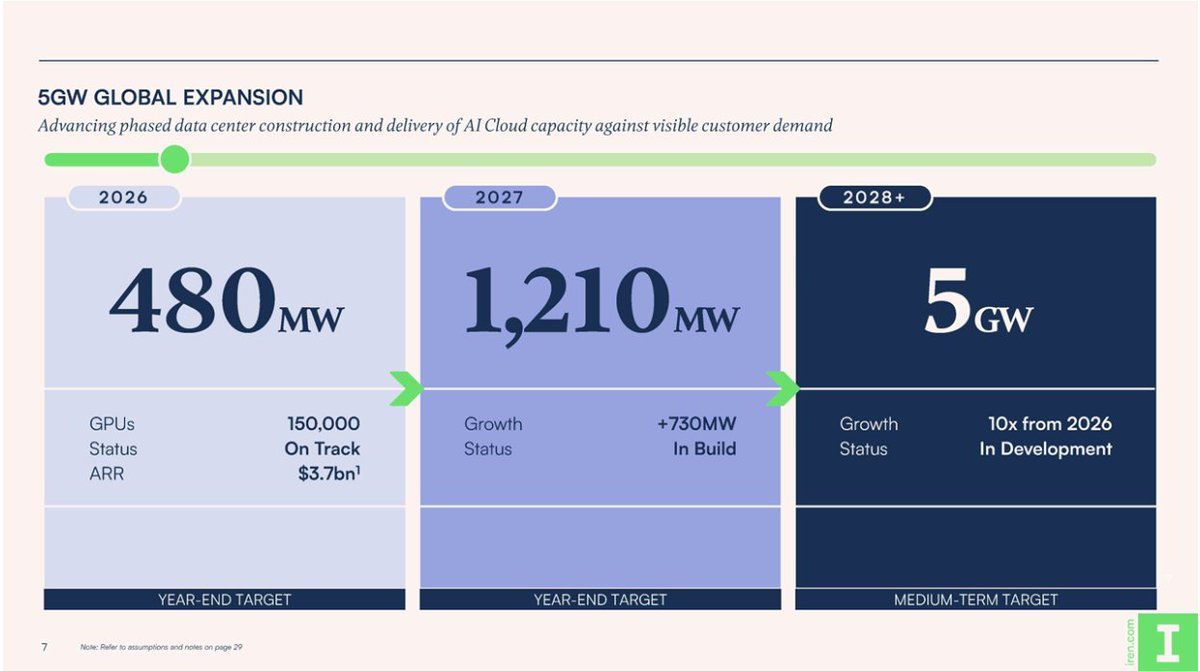

- 480MW by 2026, 1.21GW by 2027, 5GW by 2030. Nvidia GPU secured, power long secured, deals will come.

- H1 handoff in Q3 CY 2026 is kind of disappointing. Handoff will likely be early Q3 as burn-in already happening now. H2-4 will be handed off by this year is the important part. There must have been some snag in H1.

- Rest of Childress will be split among 100MW IT of liquid cooled H5-6 (likely extension for MSFT) and 250MW retrofit of air-cooled capacity.

- @FransBakker9812 spot on - First SW1 200MW IT will be in 2027 and be for VR.

- AI Revenue 33.6m is lower than expected as commissioning GPUs slower than expected. Will expect this to speed up as IREN ramps up their in-house team.

1

159